Premarket High/Low LinesTHis is another script about premarket lines, the previous one is a label and this one really plot the lines, so you dont have to do it yourself. hope it helps :)

Statistics

Premarket High/Low Label (Single Line)it shows you what the premarket high low label is on a single line, saving you the hassale of fidning it yourself. :) hope it helps.

Previous Day Levels (High, Low, Open, Close)This TradingView Pine Script indicator plots the previous day’s price levels (High, Low, Open, and Close) as horizontal rays that extend across the current trading day.

Green lines mark the Previous Day High and Previous Day Low.

Yellow lines mark the Previous Day Open and Previous Day Close.

Labels are automatically displayed at the right edge of the chart, positioned above each line, making it easy to identify the corresponding level in real time.

The levels are updated daily and always begin at the start of the current day, ensuring that they cover the entire intraday session.

This tool helps traders quickly visualize key support and resistance levels from the previous trading day and incorporate them into intraday strategies.

Volume Footprint Anomaly Scanner [PhenLabs]📊 PhenLabs - Volume Footprint Anomaly Scanner (VFAS)

Version: PineScript™ v6

📌 Description

The PhenLabs Volume Footprint Anomaly Scanner (VFAS) is an advanced Pine Script indicator designed to detect and highlight significant imbalances in buying and selling pressure within individual price bars. By analyzing a calculated "Delta" – the net difference between estimated buy and sell volume – and employing statistical Z-score analysis, VFAS pinpoints moments when buying or selling activity becomes unusually dominant. This script was created not in hopes of creating a "Buy and Sell" indicator but rather providing the user with a more in-depth insight into the intrabar volume delta and how it can fluctuate in unusual ways, leading to anomalies that can be capitalized on.

This indicator helps traders identify high-conviction points where strong market participants are active, signaling potential shifts in momentum or continuation of a trend. It aims to provide a clearer understanding of underlying market dynamics, allowing for more informed decision-making in various trading strategies, from identifying entry points to confirming trend strength.

🚀 Points of Innovation

● Z-Score for Delta Analysis : Utilizes statistical Z-scores to objectively identify statistically significant anomalies in buying/selling pressure, moving beyond simple, arbitrary thresholds.

● Dynamic Confidence Scoring : Assigns a multi-star confidence rating (1-4 stars) to each signal, factoring in high volume, trend alignment, and specific confirmation criteria, providing a nuanced view of signal strength.

● Integrated Trend Filtering : Offers an optional Exponential Moving Average (EMA)-based trend filter to ensure signals align with the broader market direction, reducing false positives in ranging markets.

● Strict Confirmation Logic : Implements specific confirmation criteria for higher-confidence signals, including price action and a time-based gap from previous signals, enhancing reliability.

● Intuitive Info Dashboard : Provides a real-time summary of market trend and the latest signal's direction and confidence directly on the chart, streamlining information access.

🔧 Core Components

● Core Delta Engine : Estimates the net buying/selling pressure (bar Delta) by analyzing price movement within each bar relative to volume. It also calculates average volume to identify bars with unusually high activity.

● Anomaly Detection (Z-Score) : Computes the Z-score for the current bar's Delta, indicating how many standard deviations it is from its recent average. This statistical measure is central to identifying significant anomalies.

● Trend Filter : Utilizes a dual Exponential Moving Average (EMA) cross-over system to define the prevailing market trend (uptrend, downtrend, or range), providing contextual awareness.

● Signal Processing & Confidence Algorithm : Evaluates anomaly conditions against trend filters and confirmation rules, then calculates a dynamic confidence score to produce actionable, contextualized signal information.

🔥 Key Features

● Advanced Delta Anomaly Detection : Pinpoints bars with exceptionally high buying or selling pressure, indicating potential institutional activity or strong market conviction.

● Multi-Factor Confidence Scoring : Each signal comes with a 1-4 star rating, clearly communicating its reliability based on high volume, trend alignment, and specific confirmation criteria.

● Optional Trend Alignment : Users can choose to filter signals, so only those aligned with the prevailing EMA-defined trend are displayed, enhancing signal quality.

● Interactive Signal Labels : Displays compact labels on the chart at anomaly points, offering detailed tooltips upon hover, including signal type, direction, confidence, and contextual information.

● Customizable Bar Colors : Visually highlights bars with Delta anomalies, providing an immediate visual cue for strong buying or selling activity.

● Real-time Info Dashboard : A clean, customizable dashboard shows the current market trend and details of the latest detected signal, keeping key information accessible at a glance.

● Configurable Alerts : Set up alerts for bullish or bearish Delta anomalies to receive real-time notifications when significant market pressure shifts occur.

🎨 Visualization

Signal Labels :

* Placed at the top/bottom of anomaly bars, showing a "📈" (bullish) or "📉" (bearish) icon.

* Tooltip: Hovering over a label reveals detailed information: Signal Type (e.g., "Delta Anomaly"), Direction, Confidence (e.g., "★★★☆"), and a descriptive explanation of the anomaly.

* Interpretation: Clearly marks actionable signals and provides deep insights without cluttering the chart, enabling quick assessment of signal strength and context.

● Info Dashboard :

* Located at the top-right of the chart, providing a clean summary.

* Displays: "PhenLabs - VFAS" header, "Market Trend" (Uptrend/Downtrend/Range with color-coded status), and "Direction | Conf." (showing the last signal's direction and star confidence).

* Optional "💡 Hover over signals for details" reminder.

* Interpretation: A concise, real-time summary of the market's pulse and the most recent high-conviction event, helping traders stay informed at a glance.

📖 Usage Guidelines

Setting Categories

⚙️ Core Delta & Volume Engine

● Minimum Volume Lookback (Bars)

○ Default: 9

○ Range: Integer (e.g., 5-50)

○ Description: Defines the number of preceding bars used to calculate the average volume and delta. Bars with volume below this average won't be considered for high-volume signals. A shorter lookback is more reactive to recent changes, while a longer one provides a smoother average.

📈 Anomaly Detection Settings

Delta Z-Score Anomaly Threshold

○ Default: 2.5

○ Range: Float (e.g., 1.0-5.0+)

○ Description: The number of standard deviations from the mean that a bar's delta must exceed to be considered a significant anomaly. A higher threshold means fewer, but potentially stronger, signals. A lower threshold will generate more signals, which might include less significant events. Experiment to find the optimal balance for your trading style.

🔬 Context Filters

Enable Trend Filter

○ Default: False

○ Range: Boolean (True/False)

○ Description: When enabled, signals will only be generated if they align with the current market trend as determined by the EMAs (e.g., only bullish signals in an uptrend, bearish in a downtrend). This helps to filter out counter-trend noise.

● Trend EMA Fast

○ Default: 50

○ Range: Integer (e.g., 10-100)

○ Description: The period for the faster Exponential Moving Average used in the trend filter. In combination with the slow EMA, it defines the trend direction.

● Trend EMA Slow

○ Default: 200

○ Range: Integer (e.g., 100-400)

○ Description: The period for the slower Exponential Moving Average used in the trend filter. The relationship between the fast and slow EMA determines if the market is in an uptrend (fast > slow) or downtrend (fast < slow).

🎨 Visual & UI Settings

● Show Info Dashboard

○ Default: True

○ Range: Boolean (True/False)

○ Description: Toggles the visibility of the dashboard on the chart, which provides a summary of market trend and the last detected signal.

● Show Dashboard Tooltip

○ Default: True

○ Range: Boolean (True/False)

○ Description: Toggles a reminder message in the dashboard to hover over signal labels for more detailed information.

● Show Delta Anomaly Bar Colors

○ Default: True

○ Range: Boolean (True/False)

○ Description: Enables or disables the coloring of bars based on their delta direction and whether they represent a significant anomaly.

● Show Signal Labels

○ Default: True

○ Range: Boolean (True/False)

○ Description: Controls the visibility of the “📈” or “📉” labels that appear on the chart when a delta anomaly signal is generated.

🔔 Alert Settings

Alert on Delta Anomaly

○ Default: True

○ Range: Boolean (True/False)

○ Description: When enabled, this setting allows you to set up alerts in TradingView that will trigger whenever a new bullish or bearish delta anomaly is detected.

✅ Best Use Cases

Early Trend Reversal / Continuation Detection: Identify strong surges of buying/selling pressure at key support/resistance levels that could indicate a reversal or the continuation of a strong move.

● Confirmation of Breakouts: Use high-confidence delta anomalies to confirm the validity of price breakouts, indicating strong conviction behind the move.

● Entry and Exit Points: Pinpoint precise entry opportunities when anomalies align with your trading strategy, or identify potential exhaustion signals for exiting trades.

● Scalping and Day Trading: The indicator’s sensitivity to intraday buying/selling imbalances makes it highly effective for short-term trading strategies.

● Market Sentiment Analysis: Gain a real-time understanding of underlying market sentiment by observing the prevalence and strength of bullish vs. bearish anomalies.

⚠️ Limitations

Estimated Delta: The script uses a simplified method to estimate delta based on bar close relative to its range, not actual order book or footprint data. While effective, it’s an approximation.

● Sensitivity to Z-Score Threshold: The effectiveness heavily relies on the `Delta Z-Score Anomaly Threshold`. Too low, and you’ll get many false positives; too high, and you might miss valid signals.

● Confirmation Criteria: The 4-star confidence level’s “confirmation” relies on specific subsequent bar conditions and previous confirmed signals, which might be too strict or specific for all contexts.

● Requires Context: While powerful, VFAS is best used in conjunction with other technical analysis tools and price action to form a comprehensive trading strategy. It is not a standalone “buy/sell” signal.

💡 What Makes This Unique

Statistical Rigor: The application of Z-score analysis to bar delta provides an objective, statistically-driven way to identify true anomalies, moving beyond arbitrary thresholds.

● Multi-Factor Confidence Scoring: The unique 1-4 star confidence system integrates multiple market dynamics (volume, trend alignment, specific follow-through) into a single, easy-to-interpret rating.

● User-Friendly Design: From the intuitive dashboard to the detailed signal tooltips, the indicator prioritizes clear and accessible information for traders of all experience levels.

🔬 How It Works

1. Bar Delta Calculation:

● The script first estimates the “buy volume” and “sell volume” for each bar. This is done by assuming that volume proportional to the distance from the low to the close represents buying, and volume proportional to the distance from the high to the close represents selling.

● How this contributes: This provides a proxy for the net buying or selling pressure (delta) within that specific price bar, even without access to actual footprint data.

2. Volume & Delta Z-Score Analysis:

● The average volume over a user-defined lookback period is calculated. Bars with volume less than twice this average are generally considered of lower interest.

● The Z-score for the calculated bar delta is computed. The Z-score measures how many standard deviations the current bar’s delta is from its average delta over the `Minimum Volume Lookback` period.

● How this contributes: A high positive Z-score indicates a bullish delta anomaly (significantly more buying than usual), while a high negative Z-score indicates a bearish delta anomaly (significantly more selling than usual). This identifies statistically unusual levels of pressure.

3. Trend Filtering (Optional):

● Two Exponential Moving Averages (Fast and Slow EMA) are used to determine the prevailing market trend. An uptrend is identified when the Fast EMA is above the Slow EMA, and a downtrend when the Fast EMA is below the Slow EMA.

● How this contributes: If enabled, the indicator will only display bullish delta anomalies during an uptrend and bearish delta anomalies during a downtrend, helping to confirm signals within the broader market context and avoid counter-trend signals.

4. Signal Generation & Confidence Scoring:

● When a delta Z-score exceeds the user-defined anomaly threshold, a signal is generated.

● This signal is then passed through a multi-factor confidence algorithm (`f_calculateConfidence`). It awards stars based on: high volume presence, alignment with the overall trend (if enabled), and a fourth star for very strong Z-scores (above 3.0) combined with specific follow-through candle patterns after a cooling-off period from a previous confirmed signal.

● How this contributes: Provides a qualitative rating (1-4 stars) for each anomaly, allowing traders to quickly assess the potential significance and reliability of the signal.

💡 Note:

The PhenLabs Volume Footprint Anomaly Scanner is a powerful analytical tool, but it’s crucial to understand that no indicator guarantees profit. Always backtest and forward-test the indicator settings on your chosen assets and timeframes. Consider integrating VFAS with your existing trading strategy, using its signals as confirmation for entries, exits, or trend bias. The Z-score threshold is highly customizable; lower values will yield more signals (including potential noise), while higher values will provide fewer but potentially higher-conviction signals. Adjust this parameter based on market volatility and your risk tolerance. Remember to combine statistical insights from VFAS with price action, support/resistance levels, and your overall market outlook for optimal results.

Daily ATR Stop Loss Buffer- Calculates Daily ATR: Uses the daily timeframe ATR (Average True Range) - a measure of price volatility

- Applies Your Buffer: Takes a percentage of that ATR that you set in the settings (e.g., 5% of daily ATR)

- Creates Stop Levels: Calculates where to place stop losses based on current price plus/minus your ATR buffer

ALFA ATC LondonThis indicator is a data indicator focused on the algorithmic opening prices of stock exchanges and shows these areas. Bias can be obtained from these areas. Trades can be executed by taking advantage of the price's ability to test and hold these areas. The indicator, AS ATC5, includes opening information for the CM New York, London, Frankfurt, and Tokyo stock exchanges. This indicator is designed solely for London and Frankfurt.

Spot vs. Derivatives BasisThis indicator calculates the basis between average spot and average perpetual futures prices across selected exchanges. It helps identify deviations between spot and perp markets — a key signal for funding pressure, arbitrage, or market dislocation.

Key Features:

Manual Pair Control – Enable or disable specific trading pairs as needed

Flexible Basis Smoothing – Apply SMA, EMA, WMA, or VWMA to filter noise

Anomaly Highlighting – Automatically flags basis deviations beyond ±0.1%

Support/Resistance MTF Merge ZonesIndicator Introduction

Support/Resistance MTF Merge Zones is an advanced technical analysis tool that automatically identifies and merges key support/resistance zones by analyzing highs and lows from multiple timeframes (15M, 1H, 4H, Daily).

Key Features

Multi-Timeframe Analysis: Integrates data from 15M, 1H, 4H, and Daily charts

Smart Zone Merging: Automatically consolidates levels within a specified percentage range into unified zones

Dynamic Color System: Distinguishes support/resistance zones based on position relative to current price

Strength Indication: Highlights zones where multiple levels converge as strong zones

Usage Guide

Configuration Parameters

Lookback Period (10): Period for calculating highs/lows

Adjustable range: 5-30

Higher values detect more long-term levels

Zone Merge % (0.5): Percentage threshold for zone merging

Range: 0.1-2.0%

Higher values merge levels across wider price ranges

Min Levels for Zone (2): Minimum number of levels required to form a zone

Range: 2-5 levels

Higher values display only more confirmed zones

Box Opacity (7): Transparency level of zone boxes

Range: 0-100%

Color Scheme

Red: Resistance zones above current price

Blue: Support zones below current price

Orange: Strong zones (3+ merged levels)

Custom NY Opening Bell - Today OnlyThis indicator shows NYC ET opening bell.

It will displace a dashed line on it.

This can be very useful for trades journaling their trades with screenshots.

My indicator will let you know when opening bell happened.

It is also very great when doing backtesting.

Nifty Buy/Sell Signals with RSI & Fisheruy Signal when:

RSI crosses above 40 from below.

Fisher Transform crosses above its signal line (bullish crossover).

Sell Signal when:

RSI crosses below 60 from above.

Fisher Transform crosses below its signal line (bearish crossover).

Hypothesis TF Strategy EvaluationThis script provides a statistical evaluation framework for trend-following strategies by examining whether mean returns (measured here as 1-period Rate of Change, ROC) differ significantly across different price quantile groups.

Specifically, it:

Calculates rolling 25th (Q1) and 75th (Q3) percentile levels of price over a user-defined window.

Classifies returns into three groups based on whether price is above Q3, between Q1 and Q3, or below Q1.

Computes mean returns and sample sizes for each group.

Performs Welch's t-tests (which account for unequal variances) between groups to assess if their mean returns differ significantly.

Displays results in two tables:

Summary Table: Shows mean ROC and number of observations for each group.

Hypothesis Testing Table: Shows pairwise t-statistics with significance stars for 95% and 99% confidence levels.

Key Features

Rolling quantile calculations: Captures local price distributions dynamically.

Robust hypothesis testing: Welch's t-test allows for heteroskedasticity between groups.

Significance indicators: Easy visual interpretation with "*" (95%) and "**" (99%) significance levels.

Visual aids: Plots Q1 and Q3 levels on the price chart for intuitive understanding.

Extensible and transparent: Fully commented code that emphasizes the evaluation process rather than trading signals.

Important Notes

Not a trading strategy: This script is intended as a tool for research and validation, not as a standalone trading system.

Look-ahead bias caution: The calculation carefully avoids look-ahead bias by computing quantiles and ROC values only on past data at each point.

Users must ensure look-ahead bias is removed when applying this or similar methods, as look-ahead bias would artificially inflate performance and statistical significance.

The statistical tests rely on the assumption of independent samples, which might not fully hold in financial time series but still provide useful insights

Usage Suggestions

Use this evaluation framework to validate hypotheses about the behavior of returns under different price regimes.

Integrate with your strategy development workflow to test whether certain market conditions produce statistically distinct return distributions.

Example

In this example, the script was run with a quantile length of 20 bars and a lookback of 500 bars for ROC classification.

We consider a simple hypothetical "strategy":

Go long if the previous bar closed above Q3 the 75th percentile).

Go short if the previous bar closed below Q1 (the 25th percentile).

Stay in cash if the previous close was between Q1 and Q3.

The screenshot below demonstrates the results of this evaluation. Surprisingly, the "long" group shows a negative average return, while the "short" group has a positive average return, indicating mean reversion rather than trend following.

The hypothesis testing table confirms that the only statistically significant difference (at 95% or higher confidence) is between the above Q3 and below Q1 groups, suggesting a meaningful divergence in their return behavior.

This highlights how this framework can help validate or challenge intuitive assumptions about strategy performance through rigorous statistical testing.

Markov Chain Trend ProbabilityA Markov Chain is a mathematical model that predicts future states based on the current state, assuming that the future depends only on the present (not the past). Originally developed by Russian mathematician Andrey Markov, this concept is widely used in:

Finance: Risk modeling, portfolio optimization, credit scoring, algorithmic trading

Weather Forecasting: Predicting sunny/rainy days, temperature patterns, storm tracking

Here's an example of a Markov chain: If the weather is sunny, the probability that will be sunny 30 min later is say 90%. However, if the state changes, i.e. it starts raining, how the probability that will be raining 30 min later is say 70% and only 30% sunny.

Similar concept can be applied to markets price action and trends.

Mathematical Foundation

The core principle follows the Markov Property: P(X_{t+1}|X_t, X_{t-1}, ..., X_0) = P(X_{t+1}|X_t)

Transition Matrix :

-------------Next State

Current----

--------P11 P12

-----P21 P22

Probability Calculations:

P(Up→Up) = Count(Up→Up) / Count(Up states)

P(Down→Down) = Count(Down→Down) / Count(Down states)

Steady-state probability: π = πP (where π is the stationary distribution)

State Definition:

State = UPTREND if (Price_t - Price_{t-n})/ATR > threshold

State = DOWNTREND if (Price_t - Price_{t-n})/ATR < -threshold

How It Works in Trading

This indicator applies Markov Chain theory to market trends by:

Defining States: Classifies market conditions as UPTREND or DOWNTREND based on price movement relative to ATR (Average True Range)

Learning Transitions: Analyzes historical data to calculate probabilities of moving from one state to another

Predicting Probabilities: Estimates the likelihood of future trend continuation or reversal

How to Use

Parameters:

Lookback Period: Number of bars to analyze for trend detection (default: 14)

ATR Threshold: Sensitivity multiplier for state changes (default: 0.5)

Historical Periods: Sample size for probability calculations (default: 33)

Trading Applications:

Trend confirmation for entry/exit decisions

Risk assessment through probability analysis

Market regime identification

Early warning system for potential trend reversals

The indicator works on any timeframe and asset class. Enjoy!

Clarix 5m Scalping Breakout StrategyPurpose

A 5-minute scalping breakout strategy designed to capture fast 3-5 pip moves, using premium/discount zone filters and market bias conditions.

How It Works

The script monitors price action in 5-minute intervals, forming a 15-minute high and low range by tracking the highs and lows of the first 3 consecutive 5-minute candles starting from a custom time. In the next 3 candles, it waits for a breakout above the 15m high or below the 15m low while confirming market bias using custom equilibrium zones.

Buy signals trigger when price breaks the 15m high while in a discount zone

Sell signals trigger when price breaks the 15m low while in a premium zone

The strategy simulates trades with fixed 3-5 pip take profit and stop loss values (configurable). All trades are recorded in a backtest table with live trade results and an automatically updated win rate.

Features

Designed exclusively for the 5-minute timeframe

Custom 15-minute high/low breakout logic

Premium, Discount, and Equilibrium zone display

Built-in backtest tracker with live trade results, statistics, and win rate

Customizable start time, take profit, and stop loss settings

Real-time alerts on breakout signals

Visual markers for trade entries and failed trades

Consistent win rate exceeding 90–95% on average when following market conditions

Usage Tips

Use strictly on 5-minute charts for accurate signal performance. Avoid during high-impact news releases.

Important: Once a trade is opened, manually set your take profit at +3 to +5 pips immediately to secure the move, as these quick scalps often hit the target within a single candle. This prevents missed exits during rapid price action.

GLOBEX BOX v1.0All credit to the creator and teacher of this strategy, @RS.

The "GOBEX BOX v1.0" indicator draws customizable horizontal rectangles (with optional midlines and labels) around specific opening candles in the EST timezone ("America/New_York").

It highlights:

The 09:30–09:31 EST 1-minute candle high/low for Monday through Friday.

The 18:00–18:05 EST 5-minute candle high/low for Sunday through Thursday.

Various customizable features are in the indicator settings.

Happy trading!

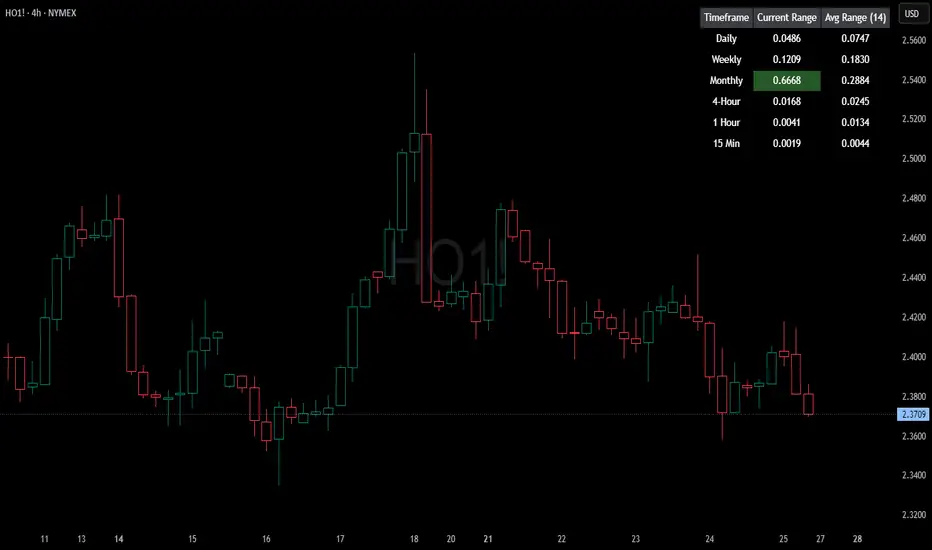

HTF Current/Average RangeThe "HTF(Higher Timeframe) Current/Average Range" indicator calculates and displays the current and average price ranges across multiple timeframes, including daily, weekly, monthly, 4 hour, and user-defined custom timeframes.

Users can customize the lookback period, table size, timeframe, and font color; with the indicator efficiently updating on the final bar to optimize performance.

When the current range surpasses the average range for a given timeframe, the corresponding table cell is highlighted in green, indicating potential maximum price expansion and signaling the possibility of an impending retracement or consolidation.

For day trading strategies, the daily average range can serve as a guide, allowing traders to hold positions until the current daily range approaches or meets the average range, at which point exiting the trade may be considered.

For scalping strategies, the 15min and 5min average range can be utilized to determine optimal holding periods for fast trades.

Other strategies:

Intraday Trading - 1h and 4h Average Range

Swing Trading - Monthly Average Range

Short-term Trading - Weekly Average Range

Also using these statistics in accordance with Power 3 ICT concepts, will assist in holding trades to their statistical average range of the chosen HTF candle.

CODE

The core functionality lies in the data retrieval and table population sections.

The request.security function (e.g., = request.security(syminfo.tickerid, "D", , lookahead = barmerge.lookahead_off)) retrieves high and low prices from specified timeframes without lookahead bias, ensuring accurate historical data.

These values are used to compute current ranges and average ranges (ta.sma(high - low, avgLength)), which are then displayed in a dynamically generated table starting at (if barstate.islast) using table.new, with conditional green highlighting when the current range is greater than average range, providing a clear visual cue for volatility analysis.

ES Gap Trading Levels# ES Gap Trading Levels

## Overview

A professional gap trading indicator designed specifically for ES Futures traders. This indicator automatically captures the closing price at 3:59 PM ET (NYSE close) and immediately displays key gap levels for the evening trading session starting at 6:00 PM ET.

## Key Features

### ✅ **Automatic Gap Level Detection**

- Captures ES Futures closing price at 3:59-4:00 PM ET

- Instantly displays gap levels for immediate session planning

- Resets daily for fresh gap analysis

### ✅ **Six Critical Gap Levels**

- **±10 Points** (White lines) - Short-term gap targets

- **±20 Points** (Light Blue lines) - Medium gap targets

- **±30 Points** (Red lines) - Extended gap targets

### ✅ **Professional Display**

- Clean horizontal lines with customizable colors

- Clear labels showing point values (+30, +20, +10, -10, -20, -30)

- Gap levels table showing exact price targets

- Optional closing price reference line

### ✅ **Customizable Settings**

- Adjustable line colors, width, and extension

- Toggle labels and reference table on/off

- Manual closing price override for testing

- Debug mode for troubleshooting

### ✅ **Smart Management**

- Automatic cleanup of previous day's levels

- Lines appear immediately after market close

- Optimized for ES1!, MES1!, and other ES futures contracts

## How It Works

1. **Market Close Capture**: At 3:59 PM ET, the indicator captures the ES closing price

2. **Instant Display**: Gap levels immediately appear on your chart

3. **Evening Session Ready**: Lines are positioned for 6:00 PM ET session start

4. **Daily Reset**: Old levels are automatically cleared each new trading day

## Perfect For:

- Gap trading strategies

- Overnight futures trading

- ES futures scalping

- Session transition analysis

- Risk management levels

## Usage Tips:

- Best used on 1-15 minute ES futures charts

- Ensure chart timezone shows ET times

- Use manual mode for backtesting specific dates

- Combine with volume and momentum indicators

## Settings Guide:

- **Display Settings**: Control lines, labels, and table visibility

- **Colors**: Customize each gap level color scheme

- **Manual Settings**: Override closing price for testing

- **Debug**: View time detection and diagnostic information

*Designed by traders, for traders. Clean, professional, and reliable gap level detection for serious ES futures trading.*

Waterfall ScreenerHow to Use This to Screen Stocks: A Step-by-Step Guide

Save the Screener Script: Open the Pine Editor, paste the code above, and save it with a clear name like "Waterfall Screener".

Open the Stock Screener: Go to the TradingView homepage or any chart page and click the "Screener" tab at the bottom. Make sure you are on the "Stock" screener.

Set Your Market: Choose the market you want to scan (e.g., NASDAQ, NYSE).

Add Your Custom Filter (The Magic Step):

Click the "Filters" button on the right side of the screener panel.

In the search box that appears, type the name of your new script: "Waterfall Screener".

It will appear as a selectable filter. Click it.

Configure the Filter:

A new filter will appear in your screener list named "Waterfall Screener".

You can now set conditions for the "ScreenerSignal" value we plotted.

To find stocks with a new, actionable trade plan, set the filter to:

Waterfall Screener | Equal | 1

Refine and Scan:

Add other essential filters to reduce noise, such as:

Volume > 1M (to find liquid stocks)

Market Cap > 1B (to find established companies)

The screener will now automatically update and show you a list of all stocks that currently have a "PENDING_ENTRY" setup according to the indicator's logic and your chosen timeframe (e.g., Daily).

Market to NAV Premium Arbitrage Alpha IndicatorBitcoin treasury companies such as Microstrategy are known for trading at significant premiums. but how big exactly is the premium? And how can we measure it in real time?

I developed this quantitative tool to identify statistical mispricings between market capitalization and net asset value (NAV), specifically designed for arbitrage strategies and alpha generation in Bitcoin-holding companies, such as MicroStrategy or Sharplink Gaming, or SPACs used primarily to hold cryptocurrencies, Bitcoin ETFs, and other NAV-based instruments. It can probably also be used in certain spin-offs.

KEY FEATURES:

✅ Real-time Premium/Discount Calculation

• Automatically retrieves market cap data from TradingView

• Calculates precise NAV based on underlying asset holdings (for example Bitcoin)

• Formula: (Market Cap - NAV) / NAV × 100

✅ Statistical Analysis

• Historical percentile rankings (customizable lookback period)

• Standard deviation bands (2σ) for extreme value detection (close to these values might be seen as interesting points to short or go long)

• Smoothing period to reduce noise

✅ Multi-Source Market Cap Detection

• You can add the ticker of the NAV asset, but if necessary, you can also put it manually. Priority system: TradingView data → Calculated → Manual override

✅ Advanced NAV Modeling

• Basic NAV: Asset holdings + cash.

• Adjusted NAV: Includes software business value, debt, preferred shares. If the company has a lot of this kind of intrinsic value, put it in the "cash" field

• Support for any underlying asset (BTC, ETH, etc.)

TRADING APPLICATIONS:

🎯 Pairs Trading Signals

• Long/Short opportunities when premium reaches statistical extremes

• Mean reversion strategies based on historical ranges

• Risk-adjusted position sizing using percentile ranks

🎯 Arbitrage Detection

• Identifies when market pricing significantly deviates from fair value

• Quantifies the magnitude of mispricing for profit potential

• Historical context for timing entry/exit points

CONFIGURATION OPTIONS:

• Underlying Asset: Any symbol (default: COINBASE:BTCUSD) NEEDS MANUAL INPUT

• Asset Quantity: Precise holdings amount (for example, how much BTC does the company currently hold). NEEDS MANUAL INPUT

• Cash Holdings: Additional liquid assets. NEEDS MANUAL INPUT

• Market Cap Mode: Auto-detect, calculated, or manual

• Advanced Adjustments: Business value, debt, preferred shares

• Display Settings: Lookback period, smoothing, custom colors

IT CAN BE USED BY:

• Quantitative traders focused on statistical arbitrage

• Institutional investors monitoring NAV-based instruments

• Bitcoin ETF and MSTR traders seeking alpha generation

• Risk managers tracking premium/discount exposures

• Academic researchers studying market efficiency (as you can see, markets are not efficient 😉)

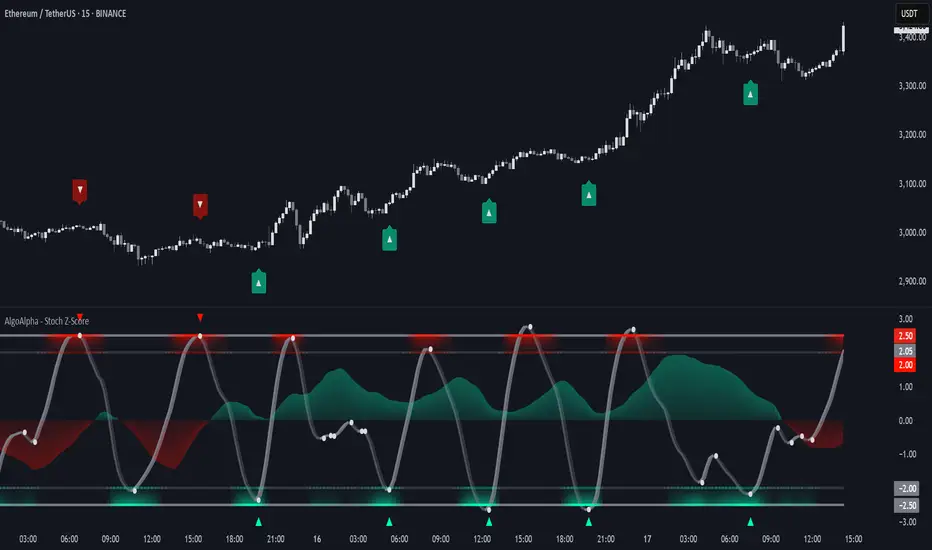

Stochastic Z-Score [AlgoAlpha]🟠 OVERVIEW

This indicator is a custom-built oscillator called the Stochastic Z-Score , which blends a volatility-normalized Z-Score with stochastic principles and smooths it using a Hull Moving Average (HMA). It transforms raw price deviations into a normalized momentum structure, then processes that through a stochastic function to better identify extreme moves. A secondary long-term momentum component is also included using an ALMA smoother. The result is a responsive oscillator that reacts to sharp imbalances while remaining stable in sideways conditions. Colored histograms, dynamic oscillator bands, and reversal labels help users visually assess shifts in momentum and identify potential turning points.

🟠 CONCEPTS

The Z-Score is calculated by comparing price to its mean and dividing by its standard deviation—this normalizes movement and highlights how far current price has stretched from typical values. This Z-Score is then passed through a stochastic function, which further refines the signal into a bounded range for easier interpretation. To reduce noise, a Hull Moving Average is applied. A separate long-term trend filter based on the ALMA of the Z-Score helps determine broader context, filtering out short-term traps. Zones are mapped with thresholds at ±2 and ±2.5 to distinguish regular momentum from extreme exhaustion. The tool is built to adapt across timeframes and assets.

🟠 FEATURES

Z-Score histogram with gradient color to visualize deviation intensity (optional toggle).

Primary oscillator line (smoothed stochastic Z-Score) with adaptive coloring based on momentum direction.

Dynamic bands at ±2 and ±2.5 to represent regular vs extreme momentum zones.

Long-term momentum line (ALMA) with contextual coloring to separate trend phases.

Automatic reversal markers when short-term crosses occur at extremes with supporting long-term momentum.

Built-in alerts for oscillator direction changes, zero-line crosses, overbought/oversold entries, and trend confirmation.

🟠 USAGE

Use this script to track momentum shifts and identify potential reversal areas. When the oscillator is rising and crosses above the previous value—especially from deeply negative zones (below -2)—and the ALMA is also above zero, this suggests bullish reversal conditions. The opposite holds for bearish setups. Reversal labels ("▲" and "▼") appear only when both short- and long-term conditions align. The ±2 and ±2.5 thresholds act as momentum warning zones; values inside are typical trends, while those beyond suggest exhaustion or extremes. Adjust the length input to match the asset’s volatility. Enable the histogram to explore underlying raw Z-Score movements. Alerts can be configured to notify key changes in momentum or zone entries.

Synthetic VX3! & VX4! continuous /VX futuresTradingView is missing continuous 3rd and 4th month VIX (/VX) futures, so I decided to try to make a synthetic one that emulates what continuous maturity futures would look like. This is useful for backtesting/historical purposes as it enables traders to see how their further out VX contracts would've performed vs the front month contract.

The indicator pulls actual realtime data (if you subscribe to the CBOE data package) or 15 minute delayed data for the VIX spot (the actual non-tradeable VIX index), the continuous front month (VX1!), and the continuous second month (VX2!) continually rolled contracts. Then the indicator's script applies a formula to fairly closely estimate how 3rd and 4th month continuous contracts would've moved.

It uses an exponential mean‑reversion to a long‑run level formula using:

σ(T) = θ+(σ0−θ)e−kT

You can expect it to be off by ~5% or so (in times of backwardation it might be less accurate).