MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.

Statistics

TAIndicatorsThis library offers a comprehensive suite of enhanced technical indicator functions, building upon TradingView's built-in indicators. The primary advantage of this library is its expanded flexibility, allowing you to select from a wider range of moving average types for calculations and smoothing across various indicators.

The core difference between these functions and TradingView's standard ones is the ability to specify different moving average types beyond the default. While a standard ta.rsi() is fixed, the rsi() in this library, for example, can be smoothed by an 'SMMA (RMA)', 'WMA', 'VWMA', or others, giving you greater control over your analysis.

█ FEATURES

This library provides enhanced versions of the following popular indicators:

Moving Average (ma): A versatile MA function that includes optional secondary smoothing and Bollinger Bands.

RSI (rsi): Calculate RSI with an optional smoothed signal line using various MA types, plus built-in divergence detection.

MACD (macd): A MACD function where you can define the MA type for both the main calculation and the signal line.

ATR (atr): An ATR function that allows for different smoothing types.

VWAP (vwap): A comprehensive anchored VWAP with multiple configurable bands.

ADX (adx): A standard ADX calculation.

Cumulative Volume Delta (cvd): Provides CVD data based on a lower timeframe.

Bollinger Bands (bb): Create Bollinger Bands with a customizable MA type for the basis line.

Keltner Channels (kc): Keltner Channels with selectable MA types and band styles.

On-Balance Volume (obv): An OBV indicator with an optional smoothed signal line using various MA types.

... and more to come! This library will be actively maintained, with new useful indicator functions added over time.

█ HOW TO USE

To use this library in your scripts, import it using its publishing link. You can then call the functions directly.

For example, to calculate a Weighted Moving Average (WMA) and then smooth it with a Simple Moving Average (SMA) :

import ActiveQuants/TAIndicators/1 as tai

// Calculate a 20-period WMA of the close

// Then, smooth the result with a 10-period SMA

= tai.ma("WMA", close, 20, "SMA", 10)

plot(myWma, color = color.blue)

plot(smoothedWma, color = color.orange)

█ Why Choose This Library?

If you're looking for more control and customization than what's offered by the standard built-in functions, this library is for you. By allowing for a variety of smoothing methods across multiple indicators, it enables a more nuanced and personalized approach to technical analysis. Fine-tune your indicators to better fit your trading style and strategies.

Deviation Trend Profile [BigBeluga]🔵 OVERVIEW

A statistical trend analysis tool that combines moving average dynamics with standard deviation zones and trend-specific price distribution.

This is an experimental indicator designed for educational and learning purposes only.

🔵 CONCEPTS

Trend Detection via SMA Slope: Detects trend shifts when the slope of the SMA exceeds a ±0.1 threshold.

Standard Deviation Zones: Calculates ±1, ±2, and ±3 levels from the SMA using ATR, forming dynamic envelopes around the mean.

Trend Distribution Profile: Builds a histogram that shows how often price closed within each deviation zone during the active trend phase.

🔵 FEATURES

Trend Signals: Immediate shift markers using colored circles at trend reversals.

SMA Gradient Coloring: The SMA line dynamically changes color based on its directional slope.

Trend Duration Label: A label above the histogram shows how many bars the current trend has lasted.

Trend Distribution Histogram: Visual bin-based profile showing frequency of price closes within deviation bands during trend lookback period.

Adjustable Bin Count: Set the granularity of the distribution using the “Bins Amount” input.

Deviation Labels and Zones: Clearly marked ±1, ±2, ±3 lines with consistent color scheme.

Trend Strength Insight:

• Wide profile skewed to ±2/3 = strong directional trend.

• Profile clustered near SMA = potential trend exhaustion or range.

🔵 HOW TO USE

Use trend shift dots as entry signals:

• 🔵 = Bullish start

• 🔴 = Bearish start

Trade with the trend when price clusters in outer zones (±2 or ±3).

Be cautious or fade the trend when price distribution contracts toward the SMA.

View across multiple timeframes for trend confluence or divergence.

🔵 CONCLUSION

Deviation Trend Profile visualizes how price distributes during trends relative to statistical deviation zones.

It’s a powerful confluence tool for identifying strength, exhaustion, and the rhythm of price behavior—ideal for swing traders and volatility analysts alike.

Luma DCA Simulator (BTC only)Luma DCA Simulator – Guide

What is the Luma DCA Simulator?

The Luma DCA Tracker shows how regular Bitcoin investments (Dollar Cost Averaging) would have developed over a freely selectable period – directly in the chart, transparent and easy to follow.

Settings Overview

1. Investment amount per interval

Specifies how much capital is invested at each purchase (e.g. 100).

2. Start date

Defines the point in time from which the simulation begins – e.g. 01.01.2020.

3. Investment interval

Determines how frequently investments are made:

– Daily

– Weekly

– Every 14 days

– Monthly

4. Language

Switches the info box display between English and German.

5. Show investment data (optional)

If activated, the chart will display additional values such as total invested capital, BTC amount, current value, and profit/loss.

What the Chart Displays

Entry points: Each DCA purchase is marked as a point in the price chart.

Average entry price: An orange line visualizes the evolving DCA average.

Info box (bottom left) with a live summary of:

– Total invested capital

– Total BTC acquired

– Average entry price

– Current portfolio value

– Profit/loss in absolute terms and percentage

Note on Accuracy

This simulation is for illustrative purposes only.

Spreads, slippage, fees, and tax effects are not included.

Actual results may vary.

Technical Note

For daily or weekly intervals, the chart timeframe should be set to 1 day or lower to ensure all purchases are accurately included.

Larger timeframes (e.g. weekly or monthly charts) may result in missed investments.

Currency Handling

All calculations are based on the selected chart symbol (e.g. BTCUSD, BTCEUR, BTCUSDT).

The displayed currency is automatically determined by the chart used.

Adaptive Multi-MA OptimizerAdaptive Multi-MA Optimizer

This indicator provides a powerful, customizable solution for traders seeking dynamically optimized moving averages with precision and control. It integrates multiple custom-built moving average types, applies real-time volatility-based optimization, and includes an optional composite smoothing engine.

🧠 Key Features

Dynamic Optimization:

Automatically selects the optimal lookback length based on market volatility stability using a custom standard deviation differential model.

Multiple Custom MA Types:

Includes fully custom implementations of:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

VWMA (Volume Weighted MA)

DEMA (Double EMA)

TEMA (Triple EMA)

Hull MA

ALMA (Arnaud Legoux MA)

Composite MA Option:

A unique "Composite" mode blends all supported MAs into a single average, then applies optional smoothing for enhanced signal clarity.

Dynamic Smoothing:

The composite mode supports volatility-adjusted smoothing (based on optimized lookback), making it adaptable to different market regimes.

Fully Custom Logic:

No built-in MA functions are used — every moving average is hand-coded for transparency and educational value.

⚙️ How It Works

Optimization:

The script evaluates a range of lengths (minLen to maxLen) using the standard deviation of price returns. It selects the length with the most stable recent volatility profile.

Calculation:

The selected MA type is calculated using that optimized length. If "Composite" is chosen, all MA types are averaged and smoothed dynamically.

Visualization:

The adaptive MA is plotted on the chart, changing color based on its position relative to price.

📌 Use Cases

Trend-following strategies that adapt to different market conditions.

Traders wanting a high-fidelity composite of multiple MAs.

Analysts interested in visualizing market smoothness without lag-heavy signals.

Coders looking to learn how to build custom indicators from scratch.

🧪 Inputs

MA Type: Choose from 8 MA types or a blended Composite.

Lookback Range: Control min/max and step size for optimization.

Source: Choose any price series (e.g., close, hl2).

⚠️ Disclaimer

This indicator is for educational and informational purposes only and does not constitute financial advice, trading advice, or investment recommendations. Use of this script is at your own risk. Past performance does not guarantee future results. Always perform your own analysis and consult with a qualified financial advisor before making trading decisions.

Adaptive Normalized Global Liquidity OscillatorAdaptive Normalized Global Liquidity Oscillator

A dynamic, non-repainting oscillator built on real central bank balance sheet data. This tool visualizes global liquidity shifts by aggregating monetary asset flows from the world’s most influential central banks.

🔍 What This Script Does:

Aggregates Global Liquidity:

Includes Federal Reserve (FED) assets and subtracts liabilities like the Treasury General Account (TGA) and Reverse Repo Facility (RRP), combined with asset positions from the ECB, BOJ, PBC, BOE, and over 10 other central banks. All data is normalized into USD using FX rates.

Adaptive Normalization:

Optimizes the lookback period dynamically based on rate-of-change stability—no fixed lengths, enabling adaptation across macro conditions.

Self-Optimizing Weighting:

Applies inverse standard deviation to balance raw liquidity, smoothed momentum (HMA), and standardized deviation from the mean.

Percentile-Ranked Highlights:

Liquidity readings are ranked relative to history—extremes are visually emphasized using gradient color and adaptive transparency.

Non-Repainting Design:

Data is anchored with bar index awareness and offset techniques, ensuring no forward-looking bias. What you see is what was known at that time.

⚠️ Important Interpretation Note:

This is not a zero-centered oscillator like RSI or MACD. The signal line does not represent neutrality at zero.

Instead, a dynamic baseline is calculated using a rolling mean of scaled liquidity.

0 is irrelevant on its own—true directional signals come from crosses above or below this adaptive baseline.

Even negative values may signal strength if they are rising above the moving average of past liquidity conditions.

✅ What to Watch For:

Crossover Above Dynamic Baseline:

Indicates liquidity is expanding relative to recent conditions—supports a risk-on interpretation.

Crossover Below Dynamic Baseline:

Suggests deteriorating liquidity conditions—may align with risk-off shifts.

Percentile Extremes:

Readings near the top or bottom historical percentiles can act as contrarian or confirmation signals, depending on momentum.

⚙️ How It Works:

Bounded Normalization:

The final oscillator is passed through a tanh function, keeping values within and reducing distortion.

Adaptive Transparency:

The strength of deviations dynamically adjusts plot intensity—visually highlighting stronger liquidity shifts.

Fully Customizable:

Toggle which banks are included, adjust dynamic optimization ranges, and control visual display options for plot and background layers.

🧠 How to Use:

Trend Confirmation:

Sustained rises in the oscillator above baseline suggest underlying monetary support for asset prices.

Macro Turning Points:

Reversals or divergences, especially near OB/OS zones, can foreshadow broader risk regime changes.

Visual Context:

Use the dynamic baseline to see if liquidity is supportive or suppressive relative to its own adaptive history.

📌 Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making trading or investment decisions.

Luma DCA Tracker (BTC)Luma DCA Tracker (BTC) – User Guide

Function

This indicator simulates a regular Bitcoin investment strategy (Dollar Cost Averaging). It calculates and visualizes:

Accumulated BTC amount

Average entry price

Total amount invested

Current portfolio value

Profit/loss in absolute and percentage terms

Settings

Investment per interval

Fixed amount to be invested at each interval (e.g., 100 USD)

Start date

The date when DCA simulation begins

Investment interval

Choose between:

daily, weekly, every 14 days, or monthly

Show investment data

Displays additional chart lines (total invested, value, profit, etc.)

Chart Elements

Orange line: Average DCA entry price

Grey dots: Entry points based on selected interval

Info box (bottom left): Live summary of all key values

Notes

Purchases are simulated at the closing price of each interval

No fees, slippage, or taxes are included

The indicator is a simulation only and not linked to an actual portfolio

GCM Price Based ColorIndicator Name:

GCM Price Based Color Indicator

Detailed Description:

The GCM Price Based Color Indicator is a unique tool designed to help traders spot potential "pump" events in the market. Unlike traditional Volume Rate of Change (VROC) indicators, this script is conditional: it calculates a VROC value only when both the average volume and the price are increasing. This focus helps filter out volume surges that don't accompany immediate price appreciation, highlighting more relevant "pump" signals.

Key Features & Calculation Logic:

Conditional Volume Rate of Change (VROC):

It first calculates a Simple Moving Average (SMA) of the volume over a user-defined length (lookback period).

It then checks two conditions:

Is the current SMA volume greater than the previous bar's SMA volume (i.e., volumeIncreasing)?

Is the current close price greater than the previous bar's close price (i.e., valueIncreasing)?

Only if both volume Increasing AND value Increasing are true, a VROC value is calculated as (current _ MA _ volume - previous _ MA _ volume) * (100 / previous _ MA _ volume). Otherwise, the VROC for that bar is 0.

Historical Normalization:

The raw VROC value is then normalized against its own historical maximum value observed since the indicator was applied. This scaling brings all VROC values into a common 0-100 range.

Why is this important? Normalization makes the indicator's readings comparable across different assets (e.g., high-volume vs. low-volume stocks/cryptos) and different timeframes, making it easier to interpret the strength of a "pump" relative to its own past.

Dynamic Plot Color (Price-Based):

The plot line's color itself provides an immediate visual cue about the current bar's price action:

Green: close is greater than close (price is up for the current bar).

Red: close is less than close (price is down for the current bar).

Grey: close is equal to close (price is flat for the current bar).

Important Note: The plot color reflects the price movement of the current bar, not the magnitude of the VROC Normalized value itself. This means you can have a high vrocNormalized value (indicating a strong conditional volume surge) but a red plot color if the very next bar's price closes lower, providing a multi-faceted view.

Thresholds & Alerts:

Two horizontal lines (small Pump Threshold and big Pump Threshold) are plotted to visually mark significant levels of normalized pump strength.

Customizable alerts can be set up to notify you when VROC Normalized reaches or exceeds these thresholds, helping you catch potential pump events in real-time.

How to Use It:

Identify Potential Pumps: Look for upward spikes in the VROC Normalized line. Higher spikes indicate stronger pump signals (i.e., a larger increase in average volume coinciding with an increasing price).

Monitor Thresholds: Pay attention when the VROC Normalized line crosses above your small Pump Threshold or big Pump Threshold. These are configurable levels to suit different assets and trading styles.

Observe Plot Color: The line color provides crucial context. A high VROC Normalized (strong pump signal) with a green line indicates current price momentum is still positive. If VROC Normalized is high but the line turns red, it might suggest the initial pump is losing steam or experiencing a pullback.

Combine with Other Tools: This indicator is best used in conjunction with other technical analysis tools (e.g., support/resistance, trend lines, other momentum indicators) for confirmation and a more holistic trading strategy.

Indicator Inputs:

Lookback period (1 - 4999) (default: 420): This length determines the period for the Simple Moving Average (SMA) of volume. A higher value will smooth the volume average more, reacting slower, while a lower value will make it more reactive. Adjust based on the timeframe and asset volatility.

Big Pump Threshold (0.01 - 99.99) (default: 10.0): The normalized VROC Normalized level that signifies a "Big Pump." When VROC Normalized reaches or exceeds this level, an alert can be triggered.

Small Pump Threshold (0.01 - 99.99) (default: 0.5): The normalized VROC Normalized level that signifies a "Small Pump." This is a lower threshold for earlier or less significant pump activity.

Alerts:

Small Pump: Triggers when VROC Normalized crosses above or equals the small Pump Threshold.

Big Pump: Triggers when VROC Normalized crosses above or equals the big Pump Threshold.

Best Practices & Considerations:

Timeframes: The indicator can be used on various timeframes, but its effectiveness may vary. Experiment to find what works best for your chosen asset and trading style.

Volatility: Highly volatile assets might require different threshold settings compared to less volatile ones.

Lag: Due to the use of a Simple Moving Average (SMA) for volume, there will be some inherent lag in the calculation.

Normalization Start: The historic Max for normalization starts with a default value of 10.0. For the very first bars, or if there hasn't been a significant VROC yet, the VROC Normalized might behave differently until a true historical maximum VROC establishes itself.

Not Financial Advice: This indicator is a tool for analysis and does not constitute financial advice. Always perform your own research and manage your risk.

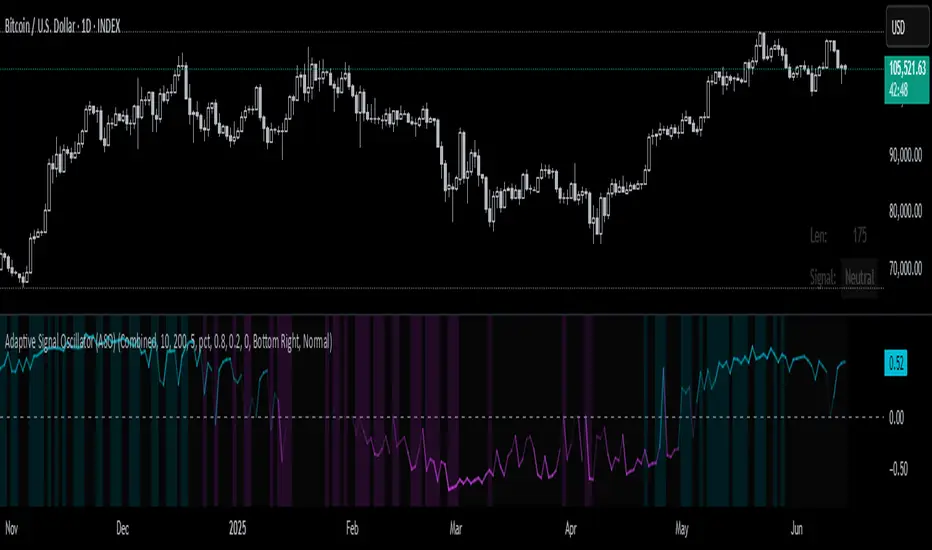

Adaptive Signal Oscillator (ASO)📘 Adaptive Signal Oscillator (ASO)

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range .

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.

Flux Capacitor (FC)# Flux Capacitor

**A volume-weighted, outlier-resistant momentum oscillator designed to expose hidden directional pressure from institutional participants.**

---

### Why "Flux Capacitor"?

The name pays homage to the fictional energy core in *Back to the Future* — an invisible engine that powers movement. Similarly, this indicator detects whether price movement is being powered by real market participation (volume) or if it's coasting without conviction.

---

### Methodology

The Flux Capacitor fuses three statistical layers:

- **Normalized Momentum**: `(Close – Open) / ATR`

Controls for raw price size and volatility.

- **Volume Scaling**:

Amplifies the effect of price moves that occur with elevated volume.

- **Robust Normalization**:

- *Winsorization* caps outlier spikes.

- *MAD-Z scoring* normalizes the signal across assets (crypto, futures, stocks).

- This produces consistent scaling across timeframes and symbols.

The result is a smooth oscillator that reliably indicates **liquidity-backed momentum** — not just price movement.

---

### Signal Events

- **Divergence (D)**: Price makes higher highs or lower lows, but Flux does not.

- **Absorption (A)**: Candle shows high volume and small body, while Flux opposes the candle direction — indicates smart money stepping in.

- **Compression (◆)**: High volume with low momentum — potential breakout zone.

- **Zero-Cross**: Indicates directional regime flip.

- **Flux Acceleration**: Histogram shows pressure rate of change.

- **Regime Background**: Color fades with weakening trend conviction.

All signals are color-coded and visually compact for easy pattern recognition.

---

### Interpreting Divergence & Absorption Correctly

Signal strength improves significantly when it appears **in the correct zone**:

#### Divergence:

| Signal | Zone | Meaning | Strength |

|--------|------------|------------------------------------------|--------------|

| Green D | Below 0 | Bullish reversal forming in weakness | **Strong** |

| Green D | Above 0 | Bullish, but less convincing | Moderate |

| Red D | Above 0 | Bearish reversal forming in strength | **Strong** |

| Red D | Below 0 | Bearish continuation — low warning value | Weak |

#### Absorption:

| Signal | Zone | Meaning | Strength |

|--------|------------|-----------------------------------------|--------------|

| Green A | Below 0 | Buyers absorbing panic-selling | **Strong** |

| Green A | Above 0 | Support continuation | Moderate |

| Red A | Above 0 | Sellers absorbing FOMO buying | **Strong** |

| Red A | Below 0 | Trend continuation — not actionable | Weak |

Look for **absorption or divergence signals in “enemy territory”** for the most actionable entries.

---

### Reducing Visual Footprint

If your chart shows a long line of numbers across the top of the Flux Capacitor pane (e.g. "FC 14 20 9 ... Bottom Right"), it’s due to TradingView’s *status line input display*.

**To fix this**:

Right-click the indicator pane → **Settings** → **Status Line** tab → uncheck “Show Indicator Arguments”.

This frees up vertical space so top-edge signals (like red `D` or yellow `◆`) remain visible and unobstructed.

---

### Features

- Original MAD-Z based momentum design

- True volume-based divergence and absorption logic

- Built-in alerts for all signal types

- Works across timeframes (1-min to weekly)

- Minimalist, responsive layout

- 25+ customizable parameters

- No future leaks, no repainting

---

### Usage Scenarios

- **Trend confirmation**: Flux > 0 confirms bullish trend strength

- **Reversal detection**: Divergence or absorption in opposite territory = high-probability reversal

- **Breakout anticipation**: Compression signal inside range often precedes directional move

- **Momentum shifts**: Watch for zero-crosses + flux acceleration spikes

---

### ⚠ Visual Note for BTC, ETH, Crude Oil & Futures

These high-priced or rapidly accelerating instruments can visually compress any linear oscillator. You may notice the Flux Capacitor’s line appears "flat" or muted on these assets — especially over long lookbacks.

> **This does not affect signal validity.** Divergence, absorption, and compression triggers still fire based on underlying logic — only the line’s amplitude appears reduced due to scaling constraints.

---

### Disclaimer

This indicator is for educational purposes only. It is not trading advice. Past results do not guarantee future performance. Use in combination with your own risk management and analysis.

Normalized Volume & True RangeThis indicator solves a fundamental challenge that traders face when trying to analyze volume and volatility together on their charts. Traditionally, volume and price volatility exist on completely different scales, making direct comparison nearly impossible. Volume might range from thousands to millions of shares, while volatility percentages typically stay within single digits. This indicator brings both measurements onto a unified scale from 0 to 100 percent, allowing you to see their relationship clearly for the first time.

The core innovation lies in the normalization process, which automatically calculates appropriate scaling factors for both volume and volatility based on their historical statistical properties. Rather than using arbitrary fixed scales that might work for one stock but fail for another, this system adapts to each instrument's unique characteristics. The indicator establishes baseline averages for both measurements and then uses statistical analysis to determine reasonable maximum values, ensuring that extreme outliers don't distort the overall picture.

You can choose from three different volatility calculation methods depending on your analytical preferences. The "Body" option measures the distance between opening and closing prices, focusing on the actual trading range that matters most for price action. The "High/Low" method captures the full daily range including wicks and shadows, giving you a complete picture of intraday volatility. The "Close/Close" approach compares consecutive closing prices, which can be particularly useful for identifying gaps and overnight price movements.

The indicator displays volume as colored columns that match your candlestick colors, making it intuitive to see whether high volume occurred during up moves or down moves. Volatility appears as a gray histogram, providing a clean background reference that doesn't interfere with volume interpretation. Both measurements are clipped at 100 percent, which represents their calculated maximum normal values, so any readings near this level indicate unusually high activity in either volume or volatility.

The baseline reference line shows you what "normal" volume looks like for the current instrument, helping you quickly identify when trading activity is above or below average. Optional moving averages for both volume and volatility are available if you prefer smoothed trend analysis over raw daily values. The entire system updates in real-time as new data arrives, continuously refining its statistical calculations to maintain accuracy as market conditions evolve.

This two-in-one indicator provides a straightforward way to examine how price movements relate to trading volume by presenting both measurements on the same normalized scale, making it easier to spot patterns and relationships that might otherwise remain hidden when analyzing these metrics separately.

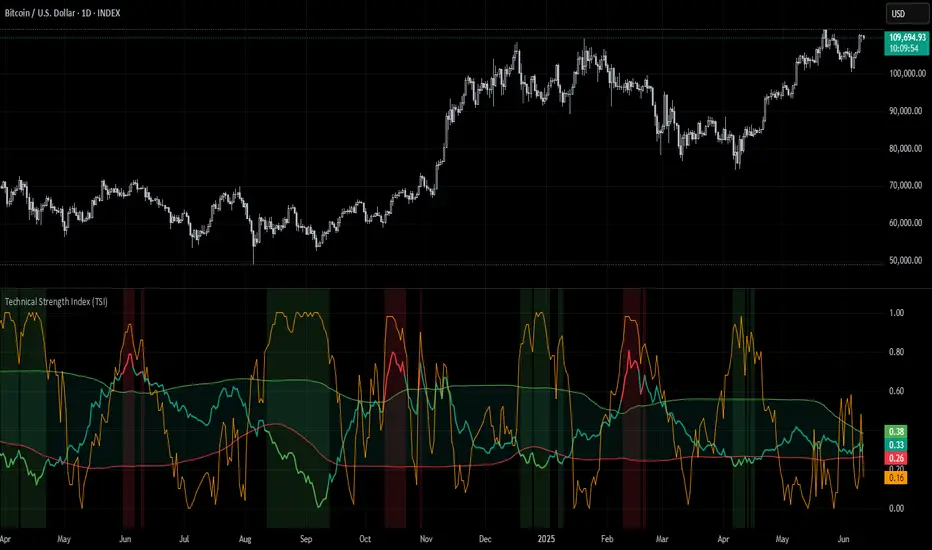

Technical Strength Index (TSI)📘 TSI with Dynamic Bands – Technical Strength Index

The TSI with Dynamic Bands is a multi-factor indicator designed to measure the statistical strength and structure of a trend. It combines several quantitative metrics into a single, normalized score between 0 and 1, allowing traders to assess the technical quality of market moves and detect overbought/oversold conditions with adaptive precision.

🧠 Core Components

This indicator draws from the StatMetrics library, blending:

📈 Trend Persistence: via the Hurst exponent, indicating whether price action is mean-reverting or trending.

📉 Risk-Adjusted Volatility: via the inverted , rewarding smoother, less erratic price movement.

🚀 Momentum Strength: using a combination of directional momentum and Z-score–normalized returns.

These components are normalized and averaged into the TSI line.

🎯 Features

TSI Line: Composite score of trend quality (0 = weak/noise, 1 = strong/structured).

Dynamic Bands: Mean ± 1 standard deviation envelopes provide adaptive context.

Overbought/Oversold Detection: Based on a rolling quantile (e.g. 90th/10th percentile of TSI history).

Signal Strength Bar (optional): Measures how statistically extreme the current TSI value is, helping validate confidence in trade setups.

Dynamic Color Cues: Background and bar gradients help visually identify statistically significant zones.

📈 How to Use

Look for overbought (red background) or oversold (green background) conditions as potential reversal zones.

Confirm trend strength with the optional signal strength bar — stronger values suggest higher signal confidence.

Use the TSI line and context bands to filter out noisy ranges and focus on structured price moves.

⚙️ Inputs

Lookback Period: Controls the smoothing and window size for statistical calculations.

Overbought/Oversold Quantiles: Adjust the thresholds for signal zones.

Plot Signal Strength: Enable or disable the signal confidence bar.

Overlay Signal Strength: Show signal strength in the same panel (compact) or not (cleaner TSI-only view).

🛠 Example Use Cases

Mean reversion traders identifying reversal zones with statistical backing

Momentum/Trend traders confirming structure before entries

Quantitative dashboards or multi-asset screening tools

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any financial instrument.

This AI is not a financial advisor; please consult your financial advisor for personalized advice.

Market Strength Buy Sell Indicator [TradeDots]A specialized tool designed to assist traders in evaluating market conditions through a multifaceted analysis of relative performance, beta-adjusted returns, momentum, and volume—allowing you to identify optimal points for long or short trades. By integrating multiple benchmarks (default S&P 500) and percentile-based thresholds, the script provides clear, actionable insights suitable for both day trading and higher-level timeframe assessments.

📝 HOW IT WORKS

1. Multi-Factor Composite Score

Relative Performance (RS Ratio): Compares your asset’s performance to a chosen benchmark (default: SPY). Values above 1.0 indicate outperformance, while below 1.0 suggest underperformance.

Beta-Adjusted Returns: Checks the ticker’s excess movement relative to expected market-related moves. This helps distinguish pure “alpha” from broad market effects.

Volume & Correlation: Volume spikes often confirm the momentum behind a move, while correlation measures how closely the asset tracks or diverges from its benchmark.

These components merge into a 0–100 composite score. Scores above 50 frequently imply bullish strength; drops below 50 often point to underperformance—potentially flagging short opportunities.

2. Intraday & Day Trading Focus

Monitoring Below 50: During the trading day, the script calculates live data against the benchmark, offering an intraday-sensitive composite score. A dip under 50 may indicate a short bias for that session, especially when accompanied by high volume or momentum shifts.

3. Higher Timeframe Monitoring

Daily Strategies: On daily or weekly charts, the script reveals overall relative strength or weakness compared to the S&P 500. This higher-level perspective helps form broader trading biases—crucial for swing or position trades spanning multiple days.

Long/Short Thresholds: Persistent readings above 50 on a daily chart typically reinforce a long bias, while consistent dips below 50 can sustain a short or cautious outlook.

4. Pair Trading Applications

Custom Benchmark Selection: By setting a specific ticker pair as your benchmark instead of the default S&P 500, you can identify spread trading opportunities between two correlated assets. This allows you to go long the outperforming asset while shorting the underperforming one when the spread reaches extreme levels.

4. Color-Coded Signals & Alerts

Visual Zones (25–75): Color-coded bands highlight strong outperformance (above 75) or pronounced underperformance (below 25).

Alerts on Strong Shifts: Automatic alerts can notify you of sudden entries or exits from bullish or bearish zones, so you can potentially act on new market information without delay.

⚙️ HOW TO USE

1. Select Your Timeframe: For scalping or day trading, lower intervals (e.g., 5-minute) offer immediate data resets at the session’s start. For multi-day insight, daily or weekly charts reveal broader performance trends.

2. Watch Key Levels Around 50: Intraday dips under 50 may be a cue to consider short trades, while bounces above 50 can confirm renewed strength.

3. Assess Benchmark Relationships: Compare your asset’s score and signals to the broader market. A stock falling below its pair’s relative strength line might lag overall market momentum.

4. Combine Tools & Validate: This script excels when integrated with other technical analysis methods (e.g., support/resistance, chart patterns) and fundamental factors for a holistic market view.

❗ LIMITATIONS

No Direction Guarantee: The indicator identifies relative strength but does not guarantee directional price moves.

Delayed Updates: Since calculations update after each bar close, sudden intrabar changes may not immediately reflect.

Market-Specific Behaviors: Some assets or unusual market conditions may deviate from typical benchmarks, weakening signal reliability.

Past ≠ Future: High or low relative strength in the past may not predict continued performance.

RISK DISCLAIMER

All forms of trading and investing involve risk, including the possible loss of principal. This indicator analyzes relative performance but cannot assure profits or eliminate losses. Past performance of any strategy does not guarantee future results. Always combine analysis with proper risk management and your broader trading plan. Consult a licensed financial advisor if you are unsure of your individual risk tolerance or investment objectives.

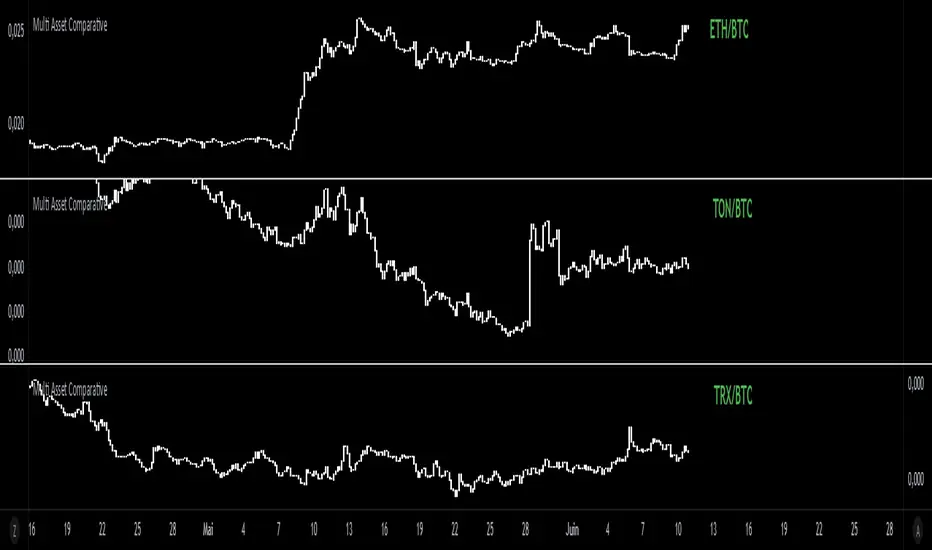

Multi Asset Comparative📊 Multi Asset Comparative – Compare Baskets of Cryptos Visually

This indicator allows you to compare the performance of two groups of cryptocurrencies (or any assets) over time, using a clean and intuitive chart.

Instead of looking at each asset separately, this tool gives you a global view by showing how one group performs relative to another — all displayed in the form of candlesticks.

🧠 What This Tool Is For

Markets constantly shift, and capital rotates between sectors or tokens. This script helps you visually track those shifts by answering a key question:

"Is this group of assets getting stronger or weaker compared to another group?"

For example:

Compare altcoins vs Bitcoin

Track the DeFi sector vs Ethereum

Analyze your custom portfolio vs the market

Spot moments when money flows from majors to smaller caps, or vice versa

🧩 How It Works (Simplified)

You select two groups of assets:

Group 1 (up to 20 assets) — the one you want to analyze

Group 2 (up to 5 assets) — your comparison baseline

The indicator then creates a single line of candles that represents the performance of Group 1 compared to Group 2. If the candles go up, it means Group 1 is gaining strength over Group 2. If the candles go down, it's losing ground.

This lets you see market dynamics in one glance, instead of switching charts or running calculations manually.

🚀 Why It's Unique

Unlike many indicators that just show data from one asset, this one provides a bird's-eye view of multiple assets at once — condensed into a simple visual ratio.

It’s:

Customizable (you choose the assets)

Visual and intuitive (no need to interpret tables or formulas)

Actionable (helps with trend confirmation, macro views, and market rotation)

Whether you're a swing trader, a macro analyst, or building your own strategy, this tool can help you spot opportunities hidden in plain sight.

✅ How to Use It

Choose your two groups of assets (e.g., altcoins vs BTC/ETH)

Watch the direction of the candles:

Uptrend = Group 1 gaining strength over Group 2

Downtrend = Group 1 weakening

Use it to confirm market shifts, anticipate rotations, or analyze sector strength

Approximate Entropy Zones [PhenLabs]Version: PineScript™ v6

Description

This indicator identifies periods of market complexity and randomness by calculating the Approximate Entropy (ApEn) of price action. As the movement of the market becomes complex, it means the current trend is losing steam and a reversal or consolidation is likely near. The indicator plots high-entropy periods as zones on your chart, providing a graphical suggestion to anticipate a potential market direction change. This indicator is designed to help traders identify favorable times to get in or out of a trade by highlighting when the market is in a state of disarray.

Points of Innovation

Advanced Complexity Analysis: Instead of relying on traditional momentum or trend indicators, this tool uses Approximate Entropy to quantify the unpredictability of price movements.

Dynamic Zone Creation: It automatically plots zones on the chart during periods of high entropy, providing a clear and intuitive visual guide.

Customizable Sensitivity: Users can fine-tune the ‘Entropy Threshold’ to adjust how frequently zones appear, allowing for calibration to different assets and timeframes.

Time-Based Zone Expiration: Zones can be set to expire after a specific time, keeping the chart clean and relevant.

Built-in Zone Size Filter: Excludes zones that form on excessively large candles, filtering out noise from extreme volatility events.

On-Chart Calibration Guide: A persistent note on the chart provides simple instructions for adjusting the entropy threshold, making it easy for users to optimize the indicator’s performance.

Core Components

Approximate Entropy (ApEn) Calculation: The core of the indicator, which measures the complexity or randomness of the price data.

Zone Plotting: Creates visual boxes on the chart when the calculated ApEn value exceeds a user-defined threshold.

Dynamic Zone Management: Manages the lifecycle of the zones, from creation to expiration, ensuring the chart remains uncluttered.

Customizable Settings: A comprehensive set of inputs that allow users to control the indicator’s sensitivity, appearance, and time-based behavior.

Key Features

Identifies Potential Reversals: The high-entropy zones can signal that a trend is nearing its end, giving traders an early warning.

Works on Any Timeframe: The indicator can be applied to any chart timeframe, from minutes to days.

Customizable Appearance: Users can change the color and transparency of the zones to match their chart’s theme.

Informative Labels: Each zone can display the calculated entropy value and the direction of the candle on which it formed.

Visualization

Entropy Zones: Shaded boxes that appear on the chart, highlighting candles with high complexity.

Zone Labels: Text within each zone that displays the ApEn value and a directional arrow (e.g., “0.525 ↑”).

Calibration Note: A small table in the top-right corner of the chart with instructions for adjusting the indicator’s sensitivity.

Usage Guidelines

Entropy Analysis

Source: The price data used for the ApEn calculation. (Default: close)

Lookback Length: The number of bars used in the ApEn calculation. (Default: 20, Range: 10-50)

Embedding Dimension (m): The length of patterns to be compared; a standard value for financial data. (Default: 2)

Tolerance Multiplier (r): Adjusts the tolerance for pattern matching; a larger value makes matching more lenient. (Default: 0.2)

Entropy Threshold: The ApEn value that must be exceeded to plot a zone. Increase this if too many zones appear; decrease it if too few appear. (Default: 0.525)

Time Settings

Analysis Timeframe: How long a zone remains on the chart after it forms. (Default: 1D)

Custom Period (Bars): The zone’s lifespan in bars if “Analysis Timeframe” is set to “Custom”. (Default: 1000)

Zone Settings

Zone Fill Color: The color of the entropy zones. (Default: #21f38a with 80% transparency)

Maximum Zone Size %: Filters out zones on candles that are larger than this percentage of their low price. (Default: 0.5)

Display Options

Show Entropy Label: Toggles the visibility of the text label inside each zone. (Default: true)

Label Text Position: The horizontal alignment of the text label. (Default: Right)

Show Calibration Note: Toggles the visibility of the calibration note in the corner of the chart. (Default: true)

Best Use Cases

Trend Reversal Trading: Identifying when a strong trend is likely to reverse or pause.

Breakout Confirmation: Using the absence of high entropy to confirm the strength of a breakout.

Ranging Market Identification: Periods of high entropy can indicate that a market is transitioning into a sideways or choppy phase.

Limitations

Not a Standalone Signal: This indicator should be used in conjunction with other forms of analysis to confirm trading signals.

Lagging Nature: Like all indicators based on historical data, ApEn is a lagging measure and does not predict future price movements with certainty.

Calibration Required: The effectiveness of the indicator is highly dependent on the “Entropy Threshold” setting, which needs to be adjusted for different assets and timeframes.

What Makes This Unique

Quantifies Complexity: It provides a numerical measure of market complexity, offering a different perspective than traditional indicators.

Clear Visual Cues: The zones make it easy to see when the market is in a state of high unpredictability.

User-Friendly Design: With features like the on-chart calibration note, the indicator is designed to be easy to use and optimize.

How It Works

Calculate Standard Deviation: The indicator first calculates the standard deviation of the source price data over a specified lookback period.

Calculate Phi: It then calculates a value called “phi” for two different pattern lengths (embedding dimensions ‘m’ and ‘m+1’). This involves comparing sequences of data points to see how many are “similar” within a certain tolerance (determined by the standard deviation and the ‘r’ multiplier).

Calculate ApEn: The Approximate Entropy is the difference between the two phi values. A higher ApEn value indicates greater irregularity and unpredictability in the data.

Plot Zones: If the calculated ApEn exceeds the user-defined ‘Entropy Threshold’, a zone is plotted on the chart.

Note: The “Entropy Threshold” is the most important setting to adjust. If you see too many zones, increase the threshold. If you see too few, decrease it.

SmartPhase Analyzer📝 SmartPhase Analyzer – Composite Market Regime Classifier

SmartPhase Analyzer is an adaptive regime classification tool that scores market conditions using a customizable set of statistical indicators. It blends multiple normalized metrics into a composite score, which is dynamically evaluated against rolling statistical thresholds to determine the current market regime.

✅ Features:

Composite score calculated from 13+ toggleable statistical indicators:

Sharpe, Sortino, Omega, Alpha, Beta, CV, R², Entropy, Drawdown, Z-Score, PLF, SRI, and Momentum Rank

Uses dynamic thresholds (mean ± std deviation) to classify regime states:

🟢 BULL – Strongly bullish

🟩 ACCUM – Mildly bullish

⚪ NEUTRAL – Sideways

🟧 DISTRIB – Mildly bearish

🔴 BEAR – Strongly bearish

Color-coded histogram for composite score clarity

Real-time regime label plotted on chart

Benchmark-aware metrics (Alpha, Beta, etc.)

Modular design using the StatMetrics library by RWCS_LTD

🧠 How to Use:

Enable/disable metrics in the settings panel to customize your composite model

Use the composite histogram and regime background for discretionary or systematic analysis

⚠️ Disclaimer:

This indicator is for educational and informational purposes only. It does not constitute financial advice or a trading recommendation. Always consult your financial advisor before making investment decisions.

StatMetricsLibrary "StatMetrics"

A utility library for common statistical indicators and ratios used in technical analysis.

Includes Z-Score, correlation, PLF, SRI, Sharpe, Sortino, Omega ratios, and normalization tools.

zscore(src, len)

Calculates the Z-score of a series

Parameters:

src (float) : The input price or series (e.g., close)

len (simple int) : The lookback period for mean and standard deviation

Returns: Z-score: number of standard deviations the input is from the mean

corr(x, y, len)

Computes Pearson correlation coefficient between two series

Parameters:

x (float) : First series

y (float) : Second series

len (simple int) : Lookback period

Returns: Correlation coefficient between -1 and 1

plf(src, longLen, shortLen, smoothLen)

Calculates the Price Lag Factor (PLF) as the difference between long and short Z-scores, normalized and smoothed

Parameters:

src (float) : Source series (e.g., close)

longLen (simple int) : Long Z-score period

shortLen (simple int) : Short Z-score period

smoothLen (simple int) : Hull MA smoothing length

Returns: Smoothed and normalized PLF oscillator

sri(signal, len)

Computes the Statistical Reliability Index (SRI) based on trend persistence

Parameters:

signal (float) : A price or signal series (e.g., smoothed PLF)

len (simple int) : Lookback period for smoothing and deviation

Returns: Normalized trend reliability score

sharpe(src, len)

Calculates the Sharpe Ratio over a period

Parameters:

src (float) : Price series (e.g., close)

len (simple int) : Lookback period

Returns: Sharpe ratio value

sortino(src, len)

Calculates the Sortino Ratio over a period, using only downside volatility

Parameters:

src (float) : Price series

len (simple int) : Lookback period

Returns: Sortino ratio value

omega(src, len)

Calculates the Omega Ratio as the ratio of upside to downside return area

Parameters:

src (float) : Price series

len (simple int) : Lookback period

Returns: Omega ratio value

beta(asset, benchmark, len)

Calculates beta coefficient of asset vs benchmark using rolling covariance

Parameters:

asset (float) : Series of the asset (e.g., close)

benchmark (float) : Series of the benchmark (e.g., SPX close)

len (simple int) : Lookback window

Returns: Beta value (slope of linear regression)

alpha(asset, benchmark, len)

Calculates rolling alpha of an asset relative to a benchmark

Parameters:

asset (float) : Series of the asset (e.g., close)

benchmark (float) : Series of the benchmark (e.g., SPX close)

len (simple int) : Lookback window

Returns: Alpha value (excess return not explained by Beta exposure)

skew(x, len)

Computes skewness of a return series

Parameters:

x (float) : Input series (e.g., returns)

len (simple int) : Lookback period

Returns: Skewness value

kurtosis(x, len)

Computes kurtosis of a return series

Parameters:

x (float) : Input series (e.g., returns)

len (simple int) : Lookback period

Returns: Kurtosis value

cv(x, len)

Calculates Coefficient of Variation

Parameters:

x (float) : Input series (e.g., returns or prices)

len (simple int) : Lookback period

Returns: CV value

autocorr(x, len)

Calculates autocorrelation with 1-lag

Parameters:

x (float) : Series to test

len (simple int) : Lookback window

Returns: Autocorrelation at lag 1

stderr(x, len)

Calculates rolling standard error of a series

Parameters:

x (float) : Input series

len (simple int) : Lookback window

Returns: Standard error (std dev / sqrt(n))

info_ratio(asset, benchmark, len)

Calculates the Information Ratio

Parameters:

asset (float) : Asset price series

benchmark (float) : Benchmark price series

len (simple int) : Lookback period

Returns: Information ratio (alpha / tracking error)

tracking_error(asset, benchmark, len)

Measures deviation from benchmark (Tracking Error)

Parameters:

asset (float) : Asset return series

benchmark (float) : Benchmark return series

len (simple int) : Lookback window

Returns: Tracking error value

max_drawdown(x, len)

Computes maximum drawdown over a rolling window

Parameters:

x (float) : Price series

len (simple int) : Lookback window

Returns: Rolling max drawdown percentage (as a negative value)

zscore_signal(z, ob, os)

Converts Z-score into a 3-level signal

Parameters:

z (float) : Z-score series

ob (float) : Overbought threshold

os (float) : Oversold threshold

Returns: -1, 0, or 1 depending on signal state

r_squared(x, y, len)

Calculates rolling R-squared (coefficient of determination)

Parameters:

x (float) : Asset returns

y (float) : Benchmark returns

len (simple int) : Lookback window

Returns: R-squared value (0 to 1)

entropy(x, len)

Approximates Shannon entropy using log returns

Parameters:

x (float) : Price series

len (simple int) : Lookback period

Returns: Approximate entropy

zreversal(z)

Detects Z-score reversals to the mean

Parameters:

z (float) : Z-score series

Returns: +1 on upward reversal, -1 on downward

momentum_rank(x, len)

Calculates relative momentum strength

Parameters:

x (float) : Price series

len (simple int) : Lookback window

Returns: Proportion of lookback where current price is higher

normalize(x, len)

Normalizes a series to a 0–1 range over a period

Parameters:

x (float) : The input series

len (simple int) : Lookback period

Returns: Normalized value between 0 and 1

composite_score(score1, score2, score3)

Combines multiple normalized scores into a composite score

Parameters:

score1 (float)

score2 (float)

score3 (float)

Returns: Average composite score

TitanGrid L/S SuperEngineTitanGrid L/S SuperEngine

Experimental Trend-Aligned Grid Signal Engine for Long & Short Execution

🔹 Overview

TitanGrid is an advanced, real-time signal engine built around a tactical grid structure.

It manages Long and Short trades using trend-aligned entries, layered scaling, and partial exits.

Unlike traditional strategy() -based scripts, TitanGrid runs as an indicator() , but includes its own full internal simulation engine.

This allows it to track capital, equity, PnL, risk exposure, and trade performance bar-by-bar — effectively simulating a custom backtest, while remaining compatible with real-time alert-based execution systems.

The concept was born from the fusion of two prior systems:

Assassin’s Grid (grid-based execution and structure) + Super 8 (trend-filtering, smart capital logic), both developed under the AssassinsGrid framework.

🔹 Disclaimer

This is an experimental tool intended for research, testing, and educational use.

It does not provide guaranteed outcomes and should not be interpreted as financial advice.

Use with demo or simulated accounts before considering live deployment.

🔹 Execution Logic

Trend direction is filtered through a custom SuperTrend engine. Once confirmed:

• Long entries trigger on pullbacks, exiting progressively as price moves up

• Short entries trigger on rallies, exiting as price declines

Grid levels are spaced by configurable percentage width, and entries scale dynamically.

🔹 Stop Loss Mechanism

TitanGrid uses a dual-layer stop system:

• A static stop per entry, placed at a fixed percentage distance matching the grid width

• A trend reversal exit that closes the entire position if price crosses the SuperTrend in the opposite direction

Stops are triggered once per cycle, ensuring predictable and capital-aware behavior.

🔹 Key Features

• Dual-side grid logic (Long-only, Short-only, or Both)

• SuperTrend filtering to enforce directional bias

• Adjustable grid spacing, scaling, and sizing

• Static and dynamic stop-loss logic

• Partial exits and reset conditions

• Webhook-ready alerts (browser-based automation compatible)

• Internal simulation of equity, PnL, fees, and liquidation levels

• Real-time dashboard for full transparency

🔹 Best Use Cases

TitanGrid performs best in structured or mean-reverting environments.

It is especially well-suited to assets with the behavioral profile of ETH — reactive, trend-intraday, and prone to clean pullback formations.

While adaptable to multiple timeframes, it shows strongest performance on the 15-minute chart , offering a balance of signal frequency and directional clarity.

🔹 License

Published under the Mozilla Public License 2.0 .

You are free to study, adapt, and extend this script.

🔹 Panel Reference

The real-time dashboard displays performance metrics, capital state, and position behavior:

• Asset Type – Automatically detects the instrument class (e.g., Crypto, Stock, Forex) from symbol metadata

• Equity – Total simulated capital: realized PnL + floating PnL + remaining cash

• Available Cash – Capital not currently allocated to any position

• Used Margin – Capital locked in open trades, based on position size and leverage

• Net Profit – Realized gain/loss after commissions and fees

• Raw Net Profit – Gross result before trading costs

• Floating PnL – Unrealized profit or loss from active positions

• ROI – Return on initial capital, including realized and floating PnL. Leverage directly impacts this metric, amplifying both gains and losses relative to account size.

• Long/Short Size & Avg Price – Open position sizes and volume-weighted average entry prices

• Leverage & Liquidation – Simulated effective leverage and projected liquidation level

• Hold – Best-performing hold side (Long or Short) over the session

• Hold Efficiency – Performance efficiency during holding phases, relative to capital used

• Profit Factor – Ratio of gross profits to gross losses (realized)

• Payoff Ratio – Average profit per win / average loss per loss

• Win Rate – Percent of profitable closes (including partial exits)

• Expectancy – Net average result per closed trade

• Max Drawdown – Largest recorded drop in equity during the session

• Commission Paid – Simulated trading costs: maker, taker, funding

• Long / Short Trades – Count of entry signals per side

• Time Trading – Number of bars spent in active positions

• Volume / Month – Extrapolated 30-day trading volume estimate

• Min Capital – Lowest equity level recorded during the session

🔹 Reference Ranges by Strategy Type

Use the following metrics as reference depending on the trading style:

Grid / Mean Reversion

• Profit Factor: 1.2 – 2.0

• Payoff Ratio: 0.5 – 1.2

• Win Rate: 50% – 70% (based on partial exits)

• Expectancy: 0.05% – 0.25%

• Drawdown: Moderate to high

• Commission Impact: High

Trend-Following

• Profit Factor: 1.5 – 3.0

• Payoff Ratio: 1.5 – 3.5

• Win Rate: 30% – 50%

• Expectancy: 0.3% – 1.0%

• Drawdown: Low to moderate

Scalping / High-Frequency

• Profit Factor: 1.1 – 1.6

• Payoff Ratio: 0.3 – 0.8

• Win Rate: 80% – 95%

• Expectancy: 0.01% – 0.05%

• Volume / Month: Very high

Breakout Strategies

• Profit Factor: 1.4 – 2.2

• Payoff Ratio: 1.2 – 2.0

• Win Rate: 35% – 60%

• Expectancy: 0.2% – 0.6%

• Drawdown: Can be sharp after failed breakouts

🔹 Note on Performance Simulation

TitanGrid includes internal accounting of fees, slippage, and funding costs.

While its logic is designed for precision and capital efficiency, performance is naturally affected by exchange commissions.

In frictionless environments (e.g., zero-fee simulation), its high-frequency logic could — in theory — extract substantial micro-edges from the market.

However, real-world conditions introduce limits, and all results should be interpreted accordingly.

Candle Range % vs 8-Candle AvgCandle % Indicator – Measure Candle Strength by Range %

**Overview:**

The *Candle % Indicator* helps traders visually and analytically gauge the strength or significance of a price candle relative to its recent historical context. This is particularly useful for detecting breakout moves, volatility shifts, or overextended candles that may signal exhaustion.

**What It Does:**

* Calculates the **percentage range** of the current candle compared to the **average range of the past N candles**.

* Highlights candles that exceed a user-defined threshold (e.g., 150% of the average range).

* Useful for **filtering out extreme candles** that might represent anomalies or unsustainable moves.

* Can be combined with other strategies (like EMA crossovers, support/resistance breaks, etc.) to improve signal quality.

**Use Case Examples:**

***Filter out fakeouts** in breakout strategies by ignoring candles that are overly large and may revert.

***Volatility control**: Avoid entries when market conditions are erratic.

**Confluence**: Combine with EMA or RSI signals for refined entries.

**How to Read:**

* If a candle is larger than the average range by more than the set percentage (default 150%), it's flagged (e.g., no entry signal or optional visual marker).

* Ideal for intraday, swing, or algorithmic trading setups.

**Customizable Inputs:**

**Lookback Period**: Number of previous candles to calculate the average range.

**% Threshold**: Maximum percentage a candle can exceed the average before being filtered or marked.

ALEX - ATR Extensions + ADR + TableALEX - ATR Extensions + ADR + Table

Overview

The ALEX ATR Extensions indicator is a comprehensive volatility and momentum analysis tool that combines Average True Range (ATR), Average Daily Range (ADR), and moving average distance calculations in a single, customizable display. This indicator helps traders assess current price action relative to historical volatility and key moving averages, providing crucial context for risk management and trade planning.

Key Features

Multi-Metric Analysis

- ATR Percentage: Current ATR as a percentage of price for volatility assessment

- ADR Percentage: Average Daily Range as a percentage for typical daily movement

- Low of Day Distance: Distance from current price to daily low

- Moving Average Distance: ATR-normalized distance from 21 and 50 period moving averages

Flexible Moving Average Options

- Configurable MA Types: Choose between EMA or SMA for both 21 and 50 period averages

- Customizable Periods: Adjust moving average lengths to suit your trading style

- Daily Timeframe Data: Uses daily moving averages regardless of chart timeframe

ATR Extension Levels

- Dynamic Price Targets: Calculate extension levels based on ATR multiples from moving averages

- Visual Reference Lines: Optional overlay lines showing ATR extension targets

- Customizable Multipliers: Adjust ATR multipliers for different risk/reward scenarios

Smart Visual Alerts

- Color-Coded Distance Metrics: Automatic color changes based on distance thresholds

- Symbol Plotting: Customizable chart symbols when distance thresholds are exceeded

- Threshold-Based Alerts: Visual cues when price reaches significant ATR distances

Comprehensive Data Table

- Real-Time Metrics: Live updating table with all key measurements

- Customizable Display: Toggle individual metrics on/off based on preference

- Professional Styling: Adjustable colors, fonts, and transparency

How to Use

Volatility Assessment

- High ATR%: Indicates elevated volatility, larger position sizing considerations

- Low ATR%: Suggests compressed volatility, potential for expansion

- ADR% Comparison: Compare current day's range to historical average

Moving Average Analysis

- ATR Distance 21/50: Normalized distance showing how extended price is from key levels

- Positive Values: Price above moving average (bullish positioning)

- Negative Values: Price below moving average (bearish positioning)

- Color Changes: Automatic alerts when reaching threshold levels

Extension Target Planning

- ATR Extension Lines: Visual price targets based on volatility-adjusted projections

- Risk/Reward Planning: Use extension levels for profit target placement

- Breakout Confirmation: Extension levels can confirm breakout validity

Symbol Alert System

- Chart Symbols: Automatic plotting when distance thresholds are breached

- Customizable Triggers: Set your own threshold levels for alerts

- Visual Scanning: Quick identification of extended conditions across multiple charts

Settings

Display Controls

- Show ADR%: Toggle average daily range percentage display

- Show ATR%: Toggle average true range percentage display

- Show LoD Distance: Toggle low of day distance calculation

- Show LoD Price: Toggle actual low of day price display

- Show ATR Distance from 21/50 DMA: Toggle moving average distance metrics

- Show 21/50 DMA Price: Toggle actual moving average price display

- Show ATR Extension Levels: Toggle extension target display in table

Moving Average Configuration

- 21/50 DMA Type: Choose between EMA or SMA calculation methods

- 21/50 DMA Period: Customize moving average lengths

- ADR/ATR Length: Adjust calculation periods for range measurements

Color Thresholds

- Threshold Levels: Set distance levels for color changes (default 2.0 and 5.0)

- Custom Colors: Choose colors for different threshold breaches

- Separate 21/50 Settings: Independent color schemes for each moving average

Symbol Settings

- Show Char Symbol: Toggle symbol plotting for each moving average

- Custom Symbols: Choose any character for chart plotting

- Symbol Colors: Customize colors for visual distinction

- Threshold Levels: Set trigger points for symbol appearance

ATR Extension Lines

- Show Extension Lines: Toggle visual extension level lines

- ATR Multipliers: Customize extension distance (default 2.0x)

- Line Colors: Choose colors for extension level visualization

Table Customization

- Background Color: Adjust table transparency and color

- Text Color: Customize default text appearance

- Font Size: Choose from tiny to huge font options

Advanced Applications

Trend Strength Analysis

- Large ATR distances suggest strong trending moves

- Small ATR distances indicate potential consolidation or reversal zones

- Compare current readings to recent historical ranges

Risk Management

- Use ATR% for position sizing calculations

- Extension levels provide natural profit target zones

- Distance metrics help identify overextended conditions

Multi-Timeframe Context

- Apply to different timeframes for comprehensive analysis

- Daily data provides consistency across all chart intervals

- Combine with weekly/monthly analysis for broader context

Market Regime Identification

- High volatility periods: Increased ATR% readings

- Low volatility periods: Compressed ATR% readings

- Trending markets: Sustained high distance readings

- Consolidating markets: Low distance readings with frequent color changes

Best Practices

Volatility-Adjusted Trading

- Increase position sizes during low volatility periods

- Reduce position sizes during high volatility periods

- Use ATR% for stop-loss placement relative to normal market movement

Extension Level Usage

- Primary targets: 1.5-2.0x ATR extensions

- Secondary targets: 2.5-3.0x ATR extensions

- Avoid chasing prices beyond 3x ATR extensions

Threshold Optimization

- Backtest different threshold levels for your trading style

- Consider market conditions when setting alert levels

- Adjust thresholds based on instrument volatility characteristics

Integration Strategies

- Combine with momentum indicators for confirmation

- Use alongside support/resistance levels

- Incorporate into systematic trading approaches

Technical Specifications

- Compatible with Pine Script v6

- Uses daily timeframe data for consistency

- Optimized for real-time performance

- Works on all chart types and timeframes

- Supports all tradeable instruments

Ideal For

- Swing traders using daily charts

- Position traders seeking volatility context

- Day traders needing intraday reference levels

- Risk managers requiring volatility metrics

- Systematic traders building rule-based strategies

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis, proper risk management techniques, and consider your individual trading plan and risk tolerance. Past performance does not guarantee future results.

Compatible with Pine Script v6 | Optimized for daily timeframe analysis | Works across all markets and instruments

21DMA Structure Counter (EMA/SMA Option)21DMA Structure Counter (EMA/SMA Option)

Overview

The 21DMA Structure Counter is an advanced technical indicator that tracks consecutive periods where price action remains above a 21-period moving average structure. This indicator helps traders identify momentum phases and potential trend exhaustion points using statistical analysis.

Key Features

Moving Average Structure

- Configurable MA Type: Choose between EMA (Exponential Moving Average) or SMA (Simple Moving Average)

- 21-Period Default: Optimized for the widely-watched 21-period moving average

- Triple MA Structure: Tracks high, close, and low moving averages for comprehensive analysis

Statistical Analysis

- Cycle Counting: Automatically counts consecutive periods above the MA structure

- Historical Data: Maintains up to 2,500 historical cycles (approximately 10 years of daily data)

- Z-Score Calculation: Provides statistical context using mean and standard deviation

- Multiple Standard Deviation Levels: Displays +1, +2, and +3 standard deviation thresholds

Visual Indicators

Color-Coded Bars:

- Gray: Below 10-year average

- Yellow: Between average and +1 standard deviation

- Orange: Between +1 and +2 standard deviations

- Red: Between +2 and +3 standard deviations

- Fuchsia: Above +3 standard deviations (extreme readings)

Breadth Integration

- Multiple Breadth Options: NDFI, NDTH, NDTW (NASDAQ breadth indicators), or VIX

- Background Shading: Visual alerts when breadth reaches extreme levels

- High/Low Thresholds: Customizable levels for breadth analysis

- Real-time Display: Current breadth value shown in data table

Smart Reset Logic

- High Below Structure Reset: Automatically resets count when daily high falls below the lowest MA

- Flexible Hold Period: Continues counting during temporary weakness as long as structure isn't violated

- Precise Entry/Exit: Strict criteria for starting cycles, flexible for maintaining them

How to Use

Trend Identification

- Rising Counts: Indicate sustained momentum above key moving average structure

- Extreme Readings: Z-scores above +2 or +3 suggest potential trend exhaustion

- Historical Context: Compare current cycles to 10-year statistical averages

Risk Management

- Breadth Confirmation: Use breadth shading to confirm market-wide strength/weakness

- Statistical Extremes: Exercise caution when readings reach +3 standard deviations

- Reset Signals: Pay attention to structure violations for potential trend changes

Multi-Timeframe Application

- Daily Charts: Primary timeframe for swing trading and position management

- Weekly/Monthly: Longer-term trend analysis

- Intraday: Shorter-term momentum assessment (adjust MA period accordingly)

Settings

Moving Average Options

- Type: EMA or SMA selection

- Period: Default 21 (customizable)

- Reset Days: Days below structure required for reset

Visual Customization

- Standard Deviation Lines: Toggle and customize colors for +1, +2, +3 SD

- Breadth Selection: Choose from NDFI, NDTH, NDTW, or VIX

- Threshold Levels: Set custom high/low breadth thresholds

- Table Styling: Customize text colors, background, and font size

Technical Notes

- Data Retention: Maintains 2,500 historical cycles for robust statistical analysis

- Real-time Updates: Calculations update with each new bar

- Breadth Integration: Uses security() function to pull external breadth data

- Performance Optimized: Efficient array management prevents memory issues

Best Practices

1. Combine with Price Action: Use alongside support/resistance and chart patterns

2. Monitor Breadth Divergences: Watch for breadth weakness during strong readings

3. Respect Statistical Extremes: Exercise caution at +2/+3 standard deviation levels

4. Context Matters: Consider overall market environment and sector rotation

5. Risk Management: Use appropriate position sizing, especially at extreme readings

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis and proper risk management techniques.

Compatible with Pine Script v6 | Optimized for daily timeframes | Best used on major indices and liquid stocks

Pair TradingPAIR TRADING

Description:

This indicator is a simple and intuitive tool for rotating between two assets based on their relative price ratio. By comparing the prices of Asset A and Asset B, it plots a “ratio line” (gray) with dynamic upper and lower boundaries (red and blue).

When the ratio reaches the red line, Asset A is expensive → rotate out of A and into B.

When the ratio touches the blue line, Asset A is cheap → rotate back into A.

The chart also shows:

🔹 Background highlights for visual cues

🔹 “Rotate to A” or “Rotate to B” markers for easy decisions

🔹 A live summary table with mean ratio, upper/lower boundaries, and current ratio

How to Use:

Select Asset A and Asset B in the settings.

Adjust the Lookback Period and Threshold if needed.

Watch the gray ratio line as it moves:

Above red line? → Consider rotating into B

Below blue line? → Consider rotating into A

Use the background color changes and rotation labels to spot clear rotation opportunities!

Why Pair Trading?

Pair trading is a powerful way to manage a portfolio because it neutralizes market direction risk and focuses on relative value.

By rotating between correlated assets, you can:

Smooth out returns

Avoid holding a weak asset too long

Capture reversion when assets diverge too far

This approach can enhance risk-adjusted returns and help keep your portfolio balanced and nimble!

How to Pick Pairs:

Choose assets with strong correlation or similar drivers.

Look for common trends (sector, macro).

Start with assets you know best (high-conviction ideas).

Make sure both have good liquidity for reliable trading!

TO HELP FIND CORRELATED ASSETS:

Use the Correlation Coefficient indicator in TradingView:

Click Indicators