Simple Position CalculatorThis indicator provides a real-time position sizing calculator designed for fast momentum trading. It instantly calculates optimal trade size based on your risk parameters, entry/exit prices, and exchange conditions (fees/slippage). Perfect for high-speed entries during candle closes and breakouts.

Statistics

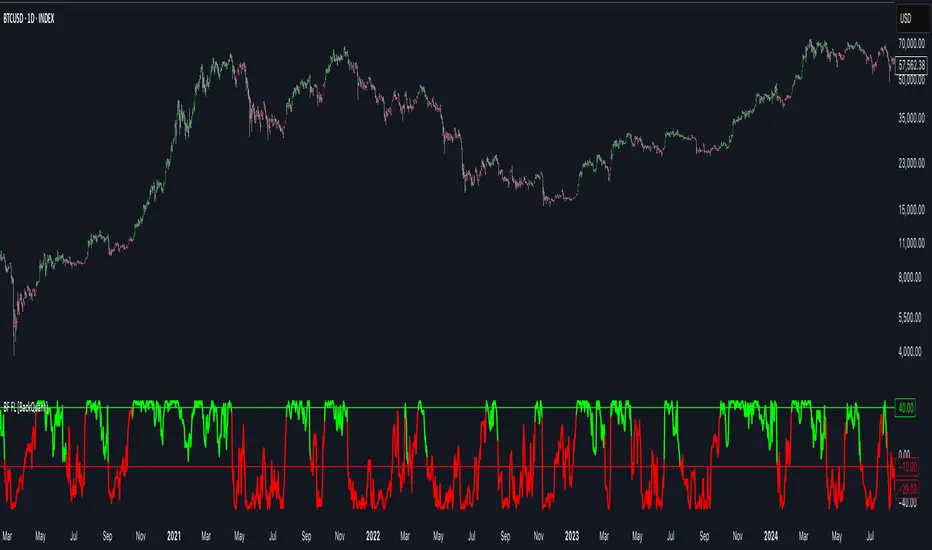

Bilateral Filter For Loop [BackQuant]Bilateral Filter For Loop

The Bilateral Filter For Loop is an advanced technical indicator designed to filter out market noise and smooth out price data, thus improving the identification of underlying market trends. It employs a bilateral filter, which is a sophisticated non-linear filter commonly used in image processing and price time series analysis. By considering both spatial and range differences between price points, this filter is highly effective at preserving significant trends while reducing random fluctuations, ultimately making it suitable for dynamic trend-following strategies.

Please take the time to read the following:

Key Features

1. Bilateral Filter Calculation:

The bilateral filter is the core of this indicator and works by applying a weight to each data point based on two factors: spatial distance and price range difference. This dual weighting process allows the filter to preserve important price movements while reducing the impact of less relevant fluctuations. The filter uses two primary parameters:

Spatial Sigma (σ_d): This parameter adjusts the weight applied based on the distance of each price point from the current price. A larger spatial sigma means more smoothing, as further away values will contribute more heavily to the result.

Range Sigma (σ_r): This parameter controls how much weight is applied based on the difference in price values. Larger price differences result in smaller weights, while similar price values result in larger weights, thereby preserving the trend while filtering out noise.

The output of this filter is a smoothed version of the original price series, which eliminates short-term fluctuations, helping traders focus on longer-term trends. The bilateral filter is applied over a rolling window, adjusting the level of smoothing dynamically based on both the distance between values and their relative price movements.

2. For Loop Calculation for Trend Scoring:

A for-loop is used to calculate the trend score based on the filtered price data. The loop compares the current value to previous values within the specified window, scoring the trend as follows:

+1 for upward movement (when the filtered value is greater than the previous value).

-1 for downward movement (when the filtered value is less than the previous value).

The cumulative result of this loop gives a continuous trend score, which serves as a directional indicator for the market's momentum. By summing the scores over the window period, the loop provides an aggregate value that reflects the overall trend strength. This score helps determine whether the market is experiencing a strong uptrend, downtrend, or sideways movement.

3. Long and Short Conditions:

Once the trend score has been calculated, it is compared against predefined threshold levels:

A long signal is generated when the trend score exceeds the upper threshold, indicating that the market is in a strong uptrend.

A short signal is generated when the trend score crosses below the lower threshold, signaling a potential downtrend or trend reversal.

These conditions provide clear signals for potential entry points, and the color-coding helps traders quickly identify market direction:

Long signals are displayed in green.

Short signals are displayed in red.

These signals are designed to provide high-confidence entries for trend-following strategies, helping traders capture profitable movements in the market.

4. Trend Background and Bar Coloring:

The script offers customizable visual settings to enhance the clarity of the trend signals. Traders can choose to:

Color the bars based on the trend direction: Bars are colored green for long signals and red for short signals.

Change the background color to provide additional context: The background will be shaded green for a bullish trend and red for a bearish trend. This visual feedback helps traders to stay aligned with the prevailing market sentiment.

These features offer a quick visual reference for understanding the market's direction, making it easier for traders to identify when to enter or exit positions.

5. Threshold Lines for Visual Feedback:

Threshold lines are plotted on the chart to represent the predefined long and short levels. These lines act as clear markers for when the market reaches a critical threshold, triggering a potential buy (long) or sell (short) signal. By showing these threshold lines on the chart, traders can quickly gauge the strength of the market and assess whether the trend is strong enough to warrant action.

These thresholds can be adjusted based on the trader's preferences, allowing them to fine-tune the indicator for different market conditions or asset behaviors.

6. Customizable Parameters for Flexibility:

The indicator offers several parameters that can be adjusted to suit individual trading preferences:

Window Period (Bilateral Filter): The window size determines how many past price values are used to calculate the bilateral filter. A larger window increases smoothing, while a smaller window results in more responsive, but noisier, data.

Spatial Sigma (σ_d) and Range Sigma (σ_r): These values control how sensitive the filter is to price changes and the distance between data points. Fine-tuning these parameters allows traders to adjust the degree of noise reduction applied to the price series.

Threshold Levels: The upper and lower thresholds determine when the trend score crosses into long or short territory. These levels can be customized to better match the trader's risk tolerance or asset characteristics.

Visual Settings: Traders can customize the appearance of the chart, including the line width of trend signals, bar colors, and background shading, to make the indicator more readable and aligned with their charting style.

7. Alerts for Trend Reversals:

The indicator includes alert conditions for real-time notifications when the market crosses the defined thresholds. Traders can set alerts to be notified when:

The trend score crosses the long threshold, signaling an uptrend.

The trend score crosses the short threshold, signaling a downtrend.

These alerts provide timely information, allowing traders to take immediate action when the market shows a significant change in direction.

Final Thoughts

The Bilateral Filter For Loop indicator is a robust tool for trend-following traders who wish to reduce market noise and focus on the underlying trend. By applying the bilateral filter and calculating trend scores, this indicator helps traders identify strong uptrends and downtrends, providing reliable entry signals with minimal market noise. The customizable parameters, visual feedback, and alerting system make it a versatile tool for traders seeking to improve their timing and capture profitable market movements.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

CRYPTO:SOLUSD

DCA Investment Tracker Pro [tradeviZion]DCA Investment Tracker Pro: Educational DCA Analysis Tool

An educational indicator that helps analyze Dollar-Cost Averaging strategies by comparing actual performance with historical data calculations.

---

💡 Why I Created This Indicator

As someone who practices Dollar-Cost Averaging, I was frustrated with constantly switching between spreadsheets, calculators, and charts just to understand how my investments were really performing. I wanted to see everything in one place - my actual performance, what I should expect based on historical data, and most importantly, visualize where my strategy could take me over the long term .

What really motivated me was watching friends and family underestimate the incredible power of consistent investing. When Napoleon Bonaparte first learned about compound interest, he reportedly exclaimed "I wonder it has not swallowed the world" - and he was right! Yet most people can't visualize how their $500 monthly contributions today could become substantial wealth decades later.

Traditional DCA tracking tools exist, but they share similar limitations:

Require manual data entry and complex spreadsheets

Use fixed assumptions that don't reflect real market behavior

Can't show future projections overlaid on actual price charts

Lose the visual context of what's happening in the market

Make compound growth feel abstract rather than tangible

I wanted to create something different - a tool that automatically analyzes real market history, detects volatility periods, and shows you both current performance AND educational projections based on historical patterns right on your TradingView charts. As Warren Buffett said: "Someone's sitting in the shade today because someone planted a tree a long time ago." This tool helps you visualize your financial tree growing over time.

This isn't just another calculator - it's a visualization tool that makes the magic of compound growth impossible to ignore.

---

🎯 What This Indicator Does

This educational indicator provides DCA analysis tools. Users can input investment scenarios to study:

Theoretical Performance: Educational calculations based on historical return data

Comparative Analysis: Study differences between actual and theoretical scenarios

Historical Projections: Theoretical projections for educational analysis (not predictions)

Performance Metrics: CAGR, ROI, and other analytical metrics for study

Historical Analysis: Calculates historical return data for reference purposes

---

🚀 Key Features

Volatility-Adjusted Historical Return Calculation

Analyzes 3-20 years of actual price data for any symbol

Automatically detects high-volatility stocks (meme stocks, growth stocks)

Uses median returns for volatile stocks, standard CAGR for stable stocks

Provides conservative estimates when extreme outlier years are detected

Smart fallback to manual percentages when data insufficient

Customizable Performance Dashboard

Educational DCA performance analysis with compound growth calculations

Customizable table sizing (Tiny to Huge text options)

9 positioning options (Top/Middle/Bottom + Left/Center/Right)

Theme-adaptive colors (automatically adjusts to dark/light mode)

Multiple display layout options

Future Projection System

Visual future growth projections

Timeframe-aware calculations (Daily/Weekly/Monthly charts)

1-30 year projection options

Shows projected portfolio value and total investment amounts

Investment Insights

Performance vs benchmark comparison

ROI from initial investment tracking

Monthly average return analysis

Investment milestone alerts (25%, 50%, 100% gains)

Contribution tracking and next milestone indicators

---

📊 Step-by-Step Setup Guide

1. Investment Settings 💰

Initial Investment: Enter your starting lump sum (e.g., $60,000)

Monthly Contribution: Set your regular DCA amount (e.g., $500/month)

Return Calculation: Choose "Auto (Stock History)" for real data or "Manual" for fixed %

Historical Period: Select 3-20 years for auto calculations (default: 10 years)

Start Year: When you began investing (e.g., 2020)

Current Portfolio Value: Your actual portfolio worth today (e.g., $150,000)

2. Display Settings 📊

Table Sizes: Choose from Tiny, Small, Normal, Large, or Huge

Table Positions: 9 options - Top/Middle/Bottom + Left/Center/Right

Visibility Toggles: Show/hide Main Table and Stats Table independently

3. Future Projection 🔮

Enable Projections: Toggle on to see future growth visualization

Projection Years: Set 1-30 years ahead for analysis

Live Example - NASDAQ:META Analysis:

Settings shown: $60K initial + $500/month + Auto calculation + 10-year history + 2020 start + $150K current value

---

🔬 Pine Script Code Examples

Core DCA Calculations:

// Calculate total invested over time

months_elapsed = (year - start_year) * 12 + month - 1

total_invested = initial_investment + (monthly_contribution * months_elapsed)

// Compound growth formula for initial investment

theoretical_initial_growth = initial_investment * math.pow(1 + annual_return, years_elapsed)

// Future Value of Annuity for monthly contributions

monthly_rate = annual_return / 12

fv_contributions = monthly_contribution * ((math.pow(1 + monthly_rate, months_elapsed) - 1) / monthly_rate)

// Total expected value

theoretical_total = theoretical_initial_growth + fv_contributions

Volatility Detection Logic:

// Detect extreme years for volatility adjustment

extreme_years = 0

for i = 1 to historical_years

yearly_return = ((price_current / price_i_years_ago) - 1) * 100

if yearly_return > 100 or yearly_return < -50

extreme_years += 1

// Use median approach for high volatility stocks

high_volatility = (extreme_years / historical_years) > 0.2

calculated_return = high_volatility ? median_of_returns : standard_cagr

Performance Metrics:

// Calculate key performance indicators

absolute_gain = actual_value - total_invested

total_return_pct = (absolute_gain / total_invested) * 100

roi_initial = ((actual_value - initial_investment) / initial_investment) * 100

cagr = (math.pow(actual_value / initial_investment, 1 / years_elapsed) - 1) * 100

---

📊 Real-World Examples

See the indicator in action across different investment types:

Stable Index Investments:

AMEX:SPY (SPDR S&P 500) - Shows steady compound growth with standard CAGR calculations

Classic DCA success story: $60K initial + $500/month starting 2020. The indicator shows SPY's historical 10%+ returns, demonstrating how consistent broad market investing builds wealth over time. Notice the smooth theoretical growth line vs actual performance tracking.

MIL:VUAA (Vanguard S&P 500 UCITS) - Shows both data limitation and solution approaches

Data limitation example: VUAA shows "Manual (Auto Failed)" and "No Data" when default 10-year historical setting exceeds available data. The indicator gracefully falls back to manual percentage input while maintaining all DCA calculations and projections.

MIL:VUAA (Vanguard S&P 500 UCITS) - European ETF with successful 5-year auto calculation

Solution demonstration: By adjusting historical period to 5 years (matching available data), VUAA auto calculation works perfectly. Shows how users can optimize settings for newer assets. European market exposure with EUR denomination, demonstrating DCA effectiveness across different markets and currencies.

NYSE:BRK.B (Berkshire Hathaway) - Quality value investment with Warren Buffett's proven track record

Value investing approach: Berkshire Hathaway's legendary performance through DCA lens. The indicator demonstrates how quality companies compound wealth over decades. Lower volatility than tech stocks = standard CAGR calculations used.

High-Volatility Growth Stocks:

NASDAQ:NVDA (NVIDIA Corporation) - Demonstrates volatility-adjusted calculations for extreme price swings

High-volatility example: NVIDIA's explosive AI boom creates extreme years that trigger volatility detection. The indicator automatically switches to "Median (High Vol): 50%" calculations for conservative projections, protecting against unrealistic future estimates based on outlier performance periods.

NASDAQ:TSLA (Tesla) - Shows how 10-year analysis can stabilize volatile tech stocks

Stable long-term growth: Despite Tesla's reputation for volatility, the 10-year historical analysis (34.8% CAGR) shows consistent enough performance that volatility detection doesn't trigger. Demonstrates how longer timeframes can smooth out extreme periods for more reliable projections.

NASDAQ:META (Meta Platforms) - Shows stable tech stock analysis using standard CAGR calculations

Tech stock with stable growth: Despite being a tech stock and experiencing the 2022 crash, META's 10-year history shows consistent enough performance (23.98% CAGR) that volatility detection doesn't trigger. The indicator uses standard CAGR calculations, demonstrating how not all tech stocks require conservative median adjustments.

Notice how the indicator automatically detects high-volatility periods and switches to median-based calculations for more conservative projections, while stable investments use standard CAGR methods.

---

📈 Performance Metrics Explained

Current Portfolio Value: Your actual investment worth today

Expected Value: What you should have based on historical returns (Auto) or your target return (Manual)

Total Invested: Your actual money invested (initial + all monthly contributions)

Total Gains/Loss: Absolute dollar difference between current value and total invested

Total Return %: Percentage gain/loss on your total invested amount

ROI from Initial Investment: How your starting lump sum has performed

CAGR: Compound Annual Growth Rate of your initial investment (Note: This shows initial investment performance, not full DCA strategy)

vs Benchmark: How you're performing compared to the expected returns

---

⚠️ Important Notes & Limitations

Data Requirements: Auto mode requires sufficient historical data (minimum 3 years recommended)

CAGR Limitation: CAGR calculation is based on initial investment growth only, not the complete DCA strategy

Projection Accuracy: Future projections are theoretical and based on historical returns - actual results may vary

Timeframe Support: Works ONLY on Daily (1D), Weekly (1W), and Monthly (1M) charts - no other timeframes supported

Update Frequency: Update "Current Portfolio Value" regularly for accurate tracking

---

📚 Educational Use & Disclaimer

This analysis tool can be applied to various stock and ETF charts for educational study of DCA mathematical concepts and historical performance patterns.

Study Examples: Can be used with symbols like AMEX:SPY , NASDAQ:QQQ , AMEX:VTI , NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:GOOGL , NASDAQ:AMZN , NASDAQ:TSLA , NASDAQ:NVDA for learning purposes.

EDUCATIONAL DISCLAIMER: This indicator is a study tool for analyzing Dollar-Cost Averaging strategies. It does not provide investment advice, trading signals, or guarantees. All calculations are theoretical examples for educational purposes only. Past performance does not predict future results. Users should conduct their own research and consult qualified financial professionals before making any investment decisions.

---

© 2025 TradeVizion. All rights reserved.

Session Status Table📌 Session Status Table

Session Status Table is an indicator that displays the real-time status of the four major trading sessions:

* 🇯🇵 Asia (Tokyo)

* 🇬🇧 London

* 🇺🇸 New York AM

* 🇺🇸 New York PM

It shows which sessions are currently open, how much time remains until they open or close, and optionally sends alerts in advance.

🧩 Features:

* Real-time session table — shows the status of each session on the chart.

* Color-coded statuses:

* 🟢 Green – Session is open

* 🔴 Red – Session is closed

* ⚪ Gray – Weekend

* Countdown timers until session open or close.

* User alerts — receive a notification a custom number of minutes before a session starts.

⚙️ Customization:

* Table position — fully configurable.

* Session colors — customizable for open, closed, and weekend states.

* Session labels — customizable with icons.

* Notifications:

* Enabled through TradingView's Alerts panel.

* User-defined lead time before session opens.

🕒 Time Zones:

All times are calculated in UTC to ensure consistency across different markets and regions, avoiding discrepancies from time zones and daylight saving time.

🚨 How to enable alerts:

1. Open the "Alerts" panel in TradingView.

2. Click "Create Alert".

3. In the condition dropdown, choose "Session Status Table".

4. Set to any alert() trigger.

5. Save — you'll be notified a set number of minutes before each session begins.

ℹ️ Technical Notes:

* Built with Pine Script version 6.

* Logically divided into clear sections: inputs, session calculations, table rendering, and alerts.

* Optimized for performance and reliability on all timeframes.

Ideal for traders who use session activity in their strategies — especially in Forex, crypto, and futures markets.

Money Risk Management with Trade Tracking

Overview

The Money Risk Management with Trade Tracking indicator is a powerful tool designed for traders on TradingView to simplify trade simulation and risk management. Unlike the TradingView Strategy Tester, which can be complex for beginners, this indicator provides an intuitive, beginner-friendly interface to evaluate trading strategies in a realistic manner, mirroring real-world trading conditions.

Built on the foundation of open-source contributions from LuxAlgo and TCP, this indicator integrates external indicator signals, overlays take-profit (TP) and stop-loss (SL) levels, and provides detailed money management analytics. It empowers traders to visualize potential profits, losses, and risk-reward ratios, making it easier to understand the financial outcomes of their strategies.

Key Features

Signal Integration: Seamlessly integrates with external long and short signals from other indicators, allowing traders to overlay TP/SL levels based on their preferred strategies.

Realistic Trade Simulation: Simulates trades as they would occur in real-world scenarios, accounting for initial capital, risk percentage, leverage, and compounding effects.

Money Management Dashboard: Displays critical metrics such as current capital, unrealized P&L, risk amount, potential profit, risk-reward ratio, and trade status in a customizable, beginner-friendly table.

TP/SL Visualization: Plots TP and SL levels on the chart with customizable styles (solid, dashed, dotted) and colors, along with optional labels for clarity.

Performance Tracking: Tracks total trades, win/loss counts, win rate, and profit factor, providing a clear overview of strategy performance.

Liquidation Risk Alerts: Warns traders if stop-loss levels risk liquidation based on leverage settings, enhancing risk awareness.

Benefits for Traders

Beginner-Friendly: Simplifies the complexities of the TradingView Strategy Tester, offering an intuitive interface for new traders to simulate and evaluate trades without confusion.

Real-World Insights: Helps traders understand the actual profit or loss potential of their strategies by factoring in capital, risk, and leverage, bridging the gap between theoretical backtesting and real-world execution.

Enhanced Decision-Making: Provides clear, real-time analytics on risk-reward ratios, unrealized P&L, and trade performance, enabling informed trading decisions.

Customizable and Flexible: Allows customization of TP/SL settings, table positions, colors, and sizes, catering to individual trader preferences.

Risk Management Focus: Encourages disciplined trading by highlighting risk amounts, potential profits, and liquidation risks, fostering better financial planning.

Why This Indicator Stands Out

Many traders struggle to translate backtested strategy results into real-world outcomes due to the abstract nature of percentage-based profitability metrics. This indicator addresses that challenge by providing a practical, user-friendly tool that simulates trades with real-world parameters like capital, leverage, and compounding. Its open-source nature ensures accessibility, while its integration with other indicators makes it versatile for various trading styles.

How to Use

Add to TradingView: Copy the Pine Script code into TradingView’s Pine Editor and add it to your chart.

Configure Inputs: Set your initial capital, risk percentage, leverage, and TP/SL values in the indicator settings. Select external long/short signal sources if integrating with other indicators.

Monitor Dashboards: Use the Money Management and Target Dashboard tables to track trade performance and risk metrics in real time.

Analyze Results: Review win rates, profit factors, and P&L to refine your trading strategy.

Credits

This indicator builds upon the open-source contributions of LuxAlgo and TCP , whose efforts in sharing their code have made this tool possible. Their dedication to the trading community is deeply appreciated.

PLR-Z For Loop🧠 Overview

PLR-Z For Loop is a trend-following indicator built on the Power Law Residual Z-score model of Bitcoin price behavior. By measuring how far price deviates from a long-term power law regression and applying a custom scoring loop, this tool identifies consistent directional pressure in market structure. Designed for BTC, this indicator helps traders align with macro trends.

🧩 Key Features

Power Law Residual Model: Tracks deviations of BTC price from its long-term logarithmic growth curve.

Z-Score Normalization: Applies long-horizon statistical normalization (400/1460 bars) to smooth residual deviations into a usable trend signal.

Loop-Based Trend Filter: Iteratively scores how often the current Z-score exceeds prior values, emphasizing trend persistence over volatility.

Optional Smoothing: Toggleable exponential smoothing helps filter noise in choppier market conditions.

Directional Regime Coloring: Aqua (bullish) and Red (bearish) visuals reinforce trend alignment across plots and candles.

🔍 How It Works

Power Law Curve: Price is compared against a logarithmic regression model fitted to historical BTC price evolution (starting July 2010), defining structural support, resistance, and centerline levels.

Residual Z-Score: The residual is calculated as the log-difference between price and the power law center.

This residual is then normalized using a rolling mean (400 days) and standard deviation (1460 days) to create a long-term Z-score.

Loop Scoring Logic:

A loop compares the current Z-score to a configurable number of past bars.

Each higher comparison adds +1, and each lower one subtracts -1.

The result is a trend persistence score (z_loop) that grows with consistent directional momentum.

Smoothing Option: A user-defined EMA smooths the score, if enabled, to reduce short-term signal noise.

Signal Logic:

Long signal when trend score exceeds long_threshold.

Short signal when score drops below short_threshold.

Directional State (CD): Internally manages the current market regime (1 = long, -1 = short), controlling all visual output.

🔁 Use Cases & Applications

Macro Trend Alignment: Ideal for traders and analysts tracking Bitcoin’s structural momentum over long timeframes.

Trend Persistence Filter: Helps confirm whether the current move is part of a sustained trend or short-lived volatility.

Best Suited for BTC: Built specifically on the BNC BLX price history and Bitcoin’s power law behavior. Not designed for use with other assets.

✅ Conclusion

PLR-Z For Loop reframes Bitcoin’s long-term power law model into a trend-following tool by scoring the persistence of deviations above or below fair value. It shifts the focus from valuation-based mean reversion to directional momentum, making it a valuable signal for traders seeking high-conviction participation in BTC’s broader market cycles.

⚠️ Disclaimer

The content provided by this indicator is for educational and informational purposes only. Nothing herein constitutes financial or investment advice. Trading and investing involve risk, including the potential loss of capital. Always backtest and apply risk management suited to your strategy.

Last Week's APM & Daily % Move(Corrected)Last Week's Average Price Movement + Daily Percentage Move (based on NY time)

This indicator accurately displays last week's Average Pip Movement (APM) consistently across all timeframes and tracks the true daily percentage move relative to that APM in a clear table in the top-right corner.

Key Features:

-Consistent Last Week's APM: Calculates the average pip movement from Monday to Friday of the previous trading week (based on daily wick-to-wick ranges, divided by 5). This APM value is now stable and the same across all chart timeframes.

-Accurate Live Daily % Move: Tracks the maximum percentage the price has moved (either up or down) since the 5 PM New York time daily open, compared to last week's APM. The percentage holds the maximum value reached during the day and resets at the next 5 PM NY open.

-NY Time Alignment: All time-based calculations are aligned with the New York time zone

Pip Adjustment: Automatically adjusts for JPY pairs.

⚠️ Important: For the intended display and relevance of the daily percentage move, this indicator is best used on timeframes 4-hour and under. On Daily and Weekly timeframes, the APM display will show a message indicating this.

We hope this indicator enhances your trading analysis.

Daily ADR TableDaily ADR Table Indicator

The Daily Average Daily Range (ADR) Table displays real-time volatility statistics directly on your chart. It shows both the current day's range and the historical average daily range as percentages of the current price, providing essential volatility metrics for trading decisions.

The indicator tracks today's range in real-time throughout the trading session using session-based calculations to ensure accuracy. It compares this against a customizable historical average (default 20 days, adjustable from 1-500 days) to help traders assess whether current volatility is above or below normal levels.

All values are displayed as percentages for easy comparison across different price levels and formatted to two decimal places for precision. The table position, text size, alignment, and colors are fully customizable with nine position options and professional default styling optimized for readability.

This indicator is valuable for day traders, swing traders, and market analysts who need to quickly assess current market volatility relative to historical norms. It assists in position sizing decisions, setting stop losses, and identifying potential breakout or consolidation scenarios based on range expansion or contraction.

ATR-InfoWHAT IT SHOWS

- ATR (): Average True Range of the chosen timeframe, printed with the instrument’s native tick precision (format.mintick).

- ATR % PRICE: ATR divided by the latest close, multiplied by 100 – the range as a percentage of current price.

- LEN / TF: The ATR length and timeframe you selected (shown in small print).

INPUTS

- ATR Length (default 14)

- ATR Timeframe (for example 60, D, W)

- Design settings: table position, font size, colours, border

EXAMPLES

BTC-USD: price 67 800, ATR 2 450, ATR % 3.6

NQ E-Mini: price 18 230, ATR 355, ATR % 1.9

CL WTI: price 76.40, ATR 2.10, ATR % 2.8

EUR-USD: price 1.0860, ATR 0.0075, ATR % 0.69

USE CASES

Volatility-adjusted stops: place your stop roughly one ATR beyond the entry price.

Position sizing: money at risk divided by ATR gives the number of contracts or coins.

Market selection: trade assets only when their ATR % sits in your preferred range.

Strategy filter: trigger entries or exits only when ATR % crosses a chosen threshold.

LIMITS

ATR is descriptive; it does not predict future moves.

Illiquid symbols may show exaggerated ATR spikes.

ATR % ignores differing session lengths (24/7 crypto versus exchange-traded hours).

WLSMA: fast approximation🙏🏻 Sup TV & @alexgrover

O(N) algocomplexity, just one loop inside. No, you can't do O(1) @ updates in moving window mode, only expanding window will allow that.

Now I have time series & stats models of my own creation, nowhere else available, just TV and my github for now, ain’t no legacy academic industry I always have fun about, but back in 2k20 when I consciously ain’t known much about quant, I remember seeing post by @alexgrover recreating Moving Regression Endpoint dropped on price chart (called LSMA here) as a linear filter combination of filters (yea yeah DSP terms) as 3WMA - 2SMA. Now it’s my time to do smth alike aye?

...

This script is remake of my 1st degree WLSMA via linear filter combo. It’s much faster, we aint calculate moving regression per se, we just match its freq response. You can see it on the screen (WLSMAfa) almost perfectly matching the original one (WLSMA).

...

While humans like to overfit, I fw generalizations. So your lovely WMA is actually just one case of a more general weight pattern: pow(len - i, e), where pow is the power function and e is the exponent itself. So:

- If e = 0, then we have SMA (every number in 0th power is one)

- If e = 1, we get WMA

- If e = 2, we get quadratic weights.

We can recreate WLSMA freq response then by combining 2 filters with e = 1 and e = 2.

This is still an approximation, even tho enormously precise for the tasks you’ve shared with me. Due to the non-linear nature of the thing it’s all we can do, and as window size grows, even this small discrepancy converges with true WLSMA value, so we’re all good. Pls don’t try to model this 0.00xxxx discrepancy, it’s not natural.

...

DSP approach is unnatural for prices, but you can put this thing on volume delta and be happy, or on other metrics of yours, if for some reason u dont wanna estimate thresholds by fitting a distro.

All good TV

∞

P.S.: strangely, the first script made & dropped in the location in Saint P where my actual quant way has started ~5 years ago xD, very thankful

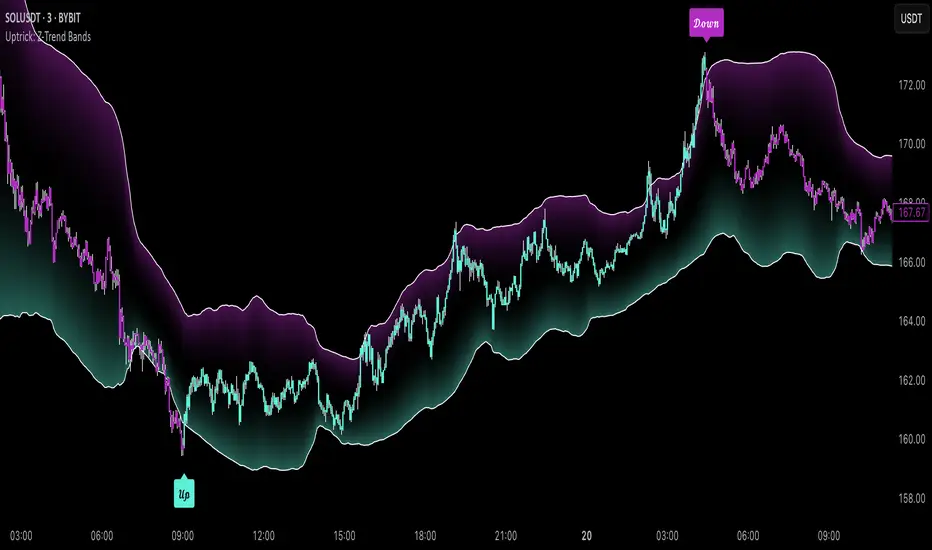

Uptrick: Z-Trend BandsOverview

Uptrick: Z-Trend Bands is a Pine Script overlay crafted to capture high-probability mean-reversion opportunities. It dynamically plots upper and lower statistical bands around an EMA baseline by converting price deviations into z-scores. Once price moves outside these bands and then reenters, the indicator verifies that momentum is genuinely reversing via an EMA-smoothed RSI slope. Signal memory ensures only one entry per momentum swing, and traders receive clear, real-time feedback through customizable bar-coloring modes, a semi-transparent fill highlighting the statistical zone, concise “Up”/“Down” labels, and a live five-metric scoring table.

Introduction

Markets often oscillate between trending and reverting, and simple thresholds or static envelopes frequently misfire when volatility shifts. Standard deviation quantifies how “wide” recent price moves have been, and a z-score transforms each deviation into a measure of how rare it is relative to its own history. By anchoring these bands to an exponential moving average, the script maintains a fluid statistical envelope that adapts instantly to both calm and turbulent regimes. Meanwhile, the Relative Strength Index (RSI) tracks momentum; smoothing RSI with an EMA and observing its slope filters out erratic spikes, ensuring that only genuine momentum flips—upward for longs and downward for shorts—qualify.

Purpose

This indicator is purpose-built for short-term mean-reversion traders operating on lower–timeframe charts. It reveals when price has strayed into the outer 5 percent of its recent range, signaling an increased likelihood of a bounce back toward fair value. Rather than firing on price alone, it demands that momentum follow suit: the smoothed RSI slope must flip in the opposite direction before any trade marker appears. This dual-filter approach dramatically reduces noise-driven, false setups. Traders then see immediate visual confirmation—bar colors that reflect the latest signal and age over time, clear entry labels, and an always-visible table of metric scores—so they can gauge both the validity and freshness of each signal at a glance.

Originality and Uniqueness

Uptrick: Z-Trend Bands stands apart from typical envelope or oscillator tools in four key ways. First, it employs fully normalized z-score bands, meaning ±2 always captures roughly the top and bottom 5 percent of moves, regardless of volatility regime. Second, it insists on two simultaneous conditions—price reentry into the bands and a confirming RSI slope flip—dramatically reducing whipsaw signals. Third, it uses slope-phase memory to lock out duplicate signals until momentum truly reverses again, enforcing disciplined entries. Finally, it offers four distinct bar-coloring schemes (solid reversal, fading reversal, exceeding bands, and classic heatmap) plus a dynamic scoring table, rather than a single, opaque alert, giving traders deep insight into every layer of analysis.

Why Each Component Was Picked

The EMA baseline was chosen for its blend of responsiveness—weighting recent price heavily—and smoothness, which filters market noise. Z-score deviation bands standardize price extremes relative to their own history, adapting automatically to shifting volatility so that “extreme” always means statistically rare. The RSI, smoothed with an EMA before slope calculation, captures true momentum shifts without the false spikes that raw RSI often produces. Slope-phase memory flags prevent repeated alerts within a single swing, curbing over-trading in choppy conditions. Bar-coloring modes provide flexible visual contexts—whether you prefer to track the latest reversal, see signal age, highlight every breakout, or view a continuous gradient—and the scoring table breaks down all five core checks for complete transparency.

Features

This indicator offers a suite of configurable visual and logical tools designed to make reversal signals both robust and transparent:

Dynamic z-score bands that expand or contract in real time to reflect current volatility regimes, ensuring the outer ±zThreshold levels always represent statistically rare extremes.

A smooth EMA baseline that weights recent price more heavily, serving as a fair-value anchor around which deviations are measured.

EMA-smoothed RSI slope confirmation, which filters out erratic momentum spikes by first smoothing raw RSI and then requiring its bar-to-bar slope to flip before any signal is allowed.

Slope-phase memory logic that locks out duplicate buy or sell markers until the RSI slope crosses back through zero, preventing over-trading during choppy swings.

Four distinct bar-coloring modes—Reversal Solid, Reversal Fade, Exceeding Bands, Classic Heat—plus a “None” option, so traders can choose whether to highlight the latest signal, show signal age, emphasize breakout bars, or view a continuous heat gradient within the bands.

A semi-transparent fill between the EMA and the upper/lower bands that visually frames the statistical zone and makes extremes immediately obvious.

Concise “Up” and “Down” labels that plot exactly when price re-enters a band with confirming momentum, keeping chart clutter to a minimum.

A real-time, five-metric scoring table (z-score, RSI slope, price vs. EMA, trend state, re-entry) that updates every two bars, displaying individual +1/–1/0 scores and an averaged Buy/Sell/Neutral verdict for complete transparency.

Calculations

Compute the fair-value EMA over fairLen bars.

Subtract that EMA from current price each bar to derive the raw deviation.

Over zLen bars, calculate the rolling mean and standard deviation of those deviations.

Convert each deviation into a z-score by subtracting the mean and dividing by the standard deviation.

Plot the upper and lower bands at ±zThreshold × standard deviation around the EMA.

Calculate raw RSI over rsiLen bars, then smooth it with an EMA of length rsiEmaLen.

Derive the RSI slope by taking the difference between the current and previous smoothed RSI.

Detect a potential reentry when price exits one of the bands on the prior bar and re-enters on the current bar.

Require that reentry coincide with an RSI slope flip (positive for a lower-band reentry, negative for an upper-band reentry).

On first valid reentry per momentum swing, fire a buy or sell signal and set a memory flag; reset that flag only when the RSI slope crosses back through zero.

For each bar, assign scores of +1, –1, or 0 for the z-score direction, RSI slope, price vs. EMA, trend-state, and reentry status.

Average those five scores; if the result exceeds +0.1, label “Buy,” if below –0.1, label “Sell,” otherwise “Neutral.”

Update bar colors, the semi-transparent fill, reversal labels, and the scoring table every two bars to reflect the latest calculations.

How It Actually Works

On each new candle, the EMA baseline and band widths update to reflect current volatility. The RSI is smoothed and its slope recalculated. The script then looks back one bar to see if price exited either band and forward to see if it reentered. If that reentry coincides with an appropriate RSI slope flip—and no signal has yet been generated in that swing—a concise label appears. Bar colors refresh according to your selected mode, and the scoring table updates to show which of the five conditions passed or failed, along with the overall verdict. This process repeats seamlessly at each bar, giving traders a continuous feed of disciplined, statistically filtered reversal cues.

Inputs

All parameters are fully user-configurable, allowing you to tailor sensitivity, lookbacks, and visuals to your trading style:

EMA length (fairLen): number of bars for the fair-value EMA; higher values smooth more but lag further behind price.

Z-Score lookback (zLen): window for calculating the mean and standard deviation of price deviations; longer lookbacks reduce noise but respond more slowly to new volatility.

Z-Score threshold (zThreshold): number of standard deviations defining the upper and lower bands; common default is 2.0 for roughly the outer 5 percent of moves.

Source (src): choice of price series (close, hl2, etc.) used for EMA, deviation, and RSI calculations.

RSI length (rsiLen): period for raw RSI calculation; shorter values react faster to momentum changes but can be choppier.

RSI EMA length (rsiEmaLen): period for smoothing raw RSI before taking its slope; higher values filter more noise.

Bar coloring mode (colorMode): select from None, Reversal Solid, Reversal Fade, Exceeding Bands, or Classic Heat to control how bars are shaded in relation to signals and band positions.

Show signals (showSignals): toggle on-chart “Up” and “Down” labels for reversal entries.

Show scoring table (enableTable): toggle the display of the five-metric breakdown table.

Table position (tablePos): choose which corner (Top Left, Top Right, Bottom Left, Bottom Right) hosts the scoring table.

Conclusion

By merging a normalized z-score framework, momentum slope confirmation, disciplined signal memory, flexible visuals, and transparent scoring into one Pine Script overlay, Uptrick: Z-Trend Bands offers a powerful yet intuitive tool for intraday mean-reversion trading. Its adaptability to real-time volatility and multi-layered filter logic deliver clear, high-confidence reversal cues without the clutter or confusion of simpler indicators.

Disclaimer

This indicator is provided solely for educational and informational purposes. It does not constitute financial advice. Trading involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Always conduct your own testing and apply careful risk management before trading live.

Day Separator with Day LabelsAdjustable day separator that paints vertical lines through the start of day. Default set to GMT however totally customisable.

Has the day of week ladled also which is also optional in position.

there is a check box for a light chart background chart but default is dark background.

Vertical lines are customisable regarding thickness and colour.

Pretty new to it all so welcome feedback and amendment ideas.

PCA Regime-Adjusted MomentumSummary

The PCA Regime-Adjusted Momentum (PCA-RAM) is an advanced market analysis tool designed to provide nuanced insights into market momentum and structural stability. It moves beyond traditional indicators by using Principal Component Analysis (PCA) to deconstruct market data into its most essential patterns.

The indicator provides two key pieces of information:

A smoothed momentum signal based on the market's dominant underlying trend.

A dynamic regime filter that gauges the stability and clarity of the market's structure, advising you when to trust or fade the momentum signals.

This allows traders to not only identify potential shifts in momentum but also to understand the context and confidence behind those signals.

Core Concepts & Methodology

The strength of this indicator lies in its sound, data-driven methodology.

1. Principal Component Analysis (PCA)

At its core, the indicator analyzes a rolling window (default 50 periods) of standardized market data (Open, High, Low, Close, and Volume). PCA is a powerful statistical technique that distills this complex, 5-dimensional data into its fundamental, uncorrelated components of variance. We focus on the First Principal Component (PC1), which represents the single most dominant pattern or "theme" driving the market's behavior in the lookback window.

2. The Momentum Signal

Instead of just looking at price, we project the current market data onto this dominant underlying pattern (PC1). This gives us a raw "projection score" that measures how strongly the current bar aligns with the historically dominant market structure. This raw score is then smoothed using two an exponential moving averages (a fast and a slow line) to create a clear, actionable momentum signal, similar in concept to a MACD.

3. The Dynamic Regime Filter

This is arguably the indicator's most powerful feature. It answers the question: "How clear is the current market picture?"

It calculates the Market Concentration Ratio, which is the percentage of total market variance explained by PC1 alone.

A high ratio indicates that the market is moving in a simple, one-dimensional way (e.g., a clear, strong trend).

A low ratio indicates the market is complex, multi-dimensional, and choppy, with no single dominant theme.

Crucially, this filter is dynamic. It compares the current concentration ratio to its own recent average, allowing it to adapt to any asset or timeframe. It automatically learns what "normal" and "choppy" look like for the specific chart you are viewing.

How to Interpret the Indicator

The indicator is displayed in a separate pane with two key visual elements:

The Momentum Lines (White & Gold)

White Line: The "Fast Line," representing the current momentum.

Gold Line: The "Slow Line," acting as the trend confirmation.

Bullish Signal: A crossover of the White Line above the Gold Line suggests a shift to positive momentum.

Bearish Signal: A crossover of the White Line below the Gold Line suggests a shift to negative momentum.

The Regime Filter (Purple & Dark Red Background)

This is your confidence gauge.

Navy Blue Background (High Concentration): The market structure is stable, simple, and trending. Momentum signals are more reliable and should be given higher priority.

Dark Red Background (Low Concentration): The market structure is complex, choppy, or directionless. Momentum signals are unreliable and prone to failure or "whipsaws." This is a signal to be cautious, tighten stops, or potentially stay out of the market.

Potential Trading Strategies

This tool is versatile and can be used in several ways:

1. Primary Signal Strategy

Condition: Wait for the background to turn Purple, confirming a stable, high-confidence regime.

Entry: Take the next crossover signal from the momentum lines (White over Gold for long, White under Gold for short).

Exit/Filter: Consider exiting positions or ignoring new signals when the background turns Navy.

2. As a Confirmation or Filter for Your Existing Strategy

Do you have a trend-following system? Only enable its long and short signals when the PCA-RAM background is Purple.

Do you have a range-trading or mean-reversion system? It might be most effective when the PCA-RAM background is Navy, indicating a lack of a clear trend.

3. Advanced Divergence Analysis

Look for classic divergences between price and the momentum lines. For example, if the price is making a new high, but the Gold Line is making a lower high, it may indicate underlying weakness in the trend, even on a Purple background. This divergence signal is more powerful because it shows that the new price high is not being confirmed by the market's dominant underlying pattern.

Price Statistical Strategy-Z Score V 1.01

Price Statistical Strategy – Z Score V 1.01

Overview

A technical breakdown of the logic and components of the “Price Statistical Strategy – Z Score V 1.01”.

This script implements a smoothed Z-Score crossover mechanism applied to the closing price to detect potential statistical deviations from local price mean. The strategy operates solely on price data (close) and includes signal spacing control and momentum-based candle filters. No volume-based or trend-detection components are included.

Core Methodology

The strategy is built on the statistical concept of Z-Score, which quantifies how far a value (closing price) is from its recent average, normalized by standard deviation. Two moving averages of the raw Z-Score are calculated: a short-term and a long-term smoothed version. The crossover between them generates long entries and exits.

Signal Conditions

Entry Condition:

A long position is opened when the short-term smoothed Z-Score crosses above the long-term smoothed Z-Score, and additional entry conditions are met.

Exit Condition:

The position is closed when the short-term Z-Score crosses below the long-term Z-Score, provided the exit conditions allow.

Signal Gapping:

A minimum number of bars (Bars gap between identical signals) must pass between repeated entry or exit signals to reduce noise.

Momentum Filter:

Entries are prevented during sequences of three or more consecutively bullish candles, and exits are prevented during three or more consecutively bearish candles.

Z-Score Function

The Z-Score is calculated as:

Z = (Close - SMA(Close, N)) / STDEV(Close, N)

Where N is the base period selected by the user.

Input Parameters

Enable Smoothed Z-Score Strategy

Enables or disables the Z-Score strategy logic. When disabled, no trades are executed.

Z-Score Base Period

Defines the number of bars used to calculate the simple moving average and standard deviation for the Z-Score. This value affects how responsive the raw Z-Score is to price changes.

Short-Term Smoothing

Sets the smoothing window for the short-term Z-Score. Higher values produce smoother short-term signals, reducing sensitivity to short-term volatility.

Long-Term Smoothing

Sets the smoothing window for the long-term Z-Score, which acts as the reference line in the crossover logic.

Bars gap between identical signals

Minimum number of bars that must pass before another signal of the same type (entry or exit) is allowed. This helps reduce redundant or overly frequent signals.

Trade Visualization Table

A table positioned at the bottom-right displays live PnL for open trades:

Entry Price

Unrealized PnL %

Text colors adapt based on whether unrealized profit is positive, negative, or neutral.

Technical Notes

This strategy uses only close prices — no trend indicators or volume components are applied.

All calculations are based on simple moving averages and standard deviation over user-defined windows.

Designed as a minimal, isolated Z-Score engine without confirmation filters or multi-factor triggers.

MVRV Ratio [Alpha Extract]The MVRV Ratio Indicator provides valuable insights into Bitcoin market cycles by tracking the relationship between market value and realized value. This powerful on-chain metric helps traders identify potential market tops and bottoms, offering clear buy and sell signals based on historical patterns of Bitcoin valuation.

🔶 CALCULATION The indicator processes MVRV ratio data through several analytical methods:

Raw MVRV Data: Collects MVRV data directly from INTOTHEBLOCK for Bitcoin

Optional Smoothing: Applies simple moving average (SMA) to reduce noise

Status Classification: Categorizes market conditions into four distinct states

Signal Generation: Produces trading signals based on MVRV thresholds

Price Estimation: Calculates estimated realized price (Current price / MVRV ratio)

Historical Context: Compares current values to historical extremes

Formula:

MVRV Ratio = Market Value / Realized Value

Smoothed MVRV = SMA(MVRV Ratio, Smoothing Length)

Estimated Realized Price = Current Price / MVRV Ratio

Distance to Top = ((3.5 / MVRV Ratio) - 1) * 100

Distance to Bottom = ((MVRV Ratio / 0.8) - 1) * 100

🔶 DETAILS Visual Features:

MVRV Plot: Color-coded line showing current MVRV value (red for overvalued, orange for moderately overvalued, blue for fair value, teal for undervalued)

Reference Levels: Horizontal lines indicating key MVRV thresholds (3.5, 2.5, 1.0, 0.8)

Zone Highlighting: Background color changes to highlight extreme market conditions (red for potentially overvalued, blue for potentially undervalued)

Information Table: Comprehensive dashboard showing current MVRV value, market status, trading signal, price information, and historical context

Interpretation:

MVRV ≥ 3.5: Potential market top, strong sell signal

MVRV ≥ 2.5: Overvalued market, consider selling

MVRV 1.5-2.5: Neutral market conditions

MVRV 1.0-1.5: Fair value, consider buying

MVRV < 1.0: Potential market bottom, strong buy signal

🔶 EXAMPLES

Market Top Identification: When MVRV ratio exceeds 3.5, the indicator signals potential market tops, highlighting periods where Bitcoin may be significantly overvalued.

Example: During bull market peaks, MVRV exceeding 3.5 has historically preceded major corrections, helping traders time their exits.

Bottom Detection: MVRV values below 1.0, especially approaching 0.8, have historically marked excellent buying opportunities.

Example: During bear market bottoms, MVRV falling below 1.0 has identified the most profitable entry points for long-term Bitcoin accumulation.

Tracking Market Cycles: The indicator provides a clear visualization of Bitcoin's market cycles from undervalued to overvalued states.

Example: Following the progression of MVRV from below 1.0 through fair value and eventually to overvalued territory helps traders position themselves appropriately throughout Bitcoin's market cycle.

Realized Price Support: The estimated realized price often acts as a significant

support/resistance level during market transitions.

Example: During corrections, price often finds support near the realized price level calculated by the indicator, providing potential entry points.

🔶 SETTINGS

Customization Options:

Smoothing: Toggle smoothing option and adjust smoothing length (1-50)

Table Display: Show/hide the information table

Table Position: Choose between top right, top left, bottom right, or bottom left positions

Visual Elements: All plots, lines, and background highlights can be customized for color and style

The MVRV Ratio Indicator provides traders with a powerful on-chain metric to identify potential market tops and bottoms in Bitcoin. By tracking the relationship between market value and realized value, this indicator helps identify periods of overvaluation and undervaluation, offering clear buy and sell signals based on historical patterns. The comprehensive information table delivers valuable context about current market conditions, helping traders make more informed decisions about market positioning throughout Bitcoin's cyclical patterns.

Arnaud Legoux Trend Aggregator | Lyro RSArnaud Legoux Trend Aggregator

Introduction

Arnaud Legoux Trend Aggregator is a custom-built trend analysis tool that blends classic market oscillators with advanced normalization, advanced math functions and Arnaud Legoux smoothing. Unlike conventional indicators, 𝓐𝓛𝓣𝓐 aggregates market momentum, volatility and trend strength.

Signal Insight

The 𝓐𝓛𝓣𝓐 line visually reflects the aggregated directional bias. A rise above the middle line threshold signals bullish strength, while a drop below the middle line indicates bearish momentum.

Another way to interpret the 𝓐𝓛𝓣𝓐 is through overbought and oversold conditions. When the 𝓐𝓛𝓣𝓐 rises above the +0.7 threshold, it suggests an overbought market and signals a strong uptrend. Conversely, a drop below the -0.7 level indicates an oversold condition and a strong downtrend.

When the oscillator hovers near the zero line, especially within the neutral ±0.3 band, it suggests that no single directional force is dominating—common during consolidation phases or pre-breakout compression.

Real-World Example

Usually 𝓐𝓛𝓣𝓐 is used by following the bar color for simple signals; however, like most indicators there are unique ways to use an indicator. Let’s dive deep into such ways.

The market begins with a green bar color, raising awareness for a potential long setup—but not a direct entry. In this methodology, bar coloring serves as an alert mechanism rather than a strict entry trigger.

The first long position was initiated when the 𝓐𝓛𝓣𝓐 signal line crossed above the +0.3 threshold, suggesting a shift in directional acceleration. This entry coincided with a rising price movement, validating the trade.

As price advanced, the position was exited into cash—not reversed into a short—because the short criteria for this use case are distinct. The exit was prompted by 𝓐𝓛𝓣𝓐 crossing back below the +0.3 level, signaling the potential weakening of the long trend.

Later, as 𝓐𝓛𝓣𝓐 crossed below 0, attention shifted toward short opportunities. A short entry was confirmed when 𝓐𝓛𝓣𝓐 dipped below -0.3, indicating growing downside momentum. The position was eventually closed when 𝓐𝓛𝓣𝓐 crossed back above the -0.3 boundary—signaling a possible deceleration of the bearish move.

This logic was consistently applied in subsequent setups, emphasizing the role of 𝓐𝓛𝓣𝓐’s thresholds in guiding both entries and exits.

Framework

The Arnaud Legoux Trend Aggregator (ALTA) combines multiple technical indicators into a single smoothed signal. It uses RSI, MACD, Bollinger Bands, Stochastic Momentum Index, and ATR.

Each indicator's output is normalized to a common scale to eliminate bias and ensure consistency. These normalized values are then transformed using a hyperbolic tangent function (Tanh).

The final score is refined with a custom Arnaud Legoux Moving Average (ALMA) function, which offers responsive smoothing that adapts quickly to price changes. This results in a clear signal that reacts efficiently to shifting market conditions.

⚠️ WARNING ⚠️: THIS INDICATOR, OR ANY OTHER WE (LYRO RS) PUBLISH, IS NOT FINANCIAL OR INVESTMENT ADVICE. EVERY INDICATOR SHOULD BE COMBINED WITH PRICE ACTION, FUNDAMENTALS, OTHER TECHNICAL ANALYSIS TOOLS & PROPER RISK. MANAGEMENT.

Support and Resistance Logistic Regression | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Logistic Regression Support / Resistance indicator! This tool leverages advanced statistical modeling "Logistic Regressions" to identify and project key price levels where the market is likely to find support or resistance. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Logistic Regression Support / Resistance Features :

Intelligent S/R Identification : The indicator uses a logistic regression model to intelligently identify and plot significant support and resistance levels.

Predictive Probability : Each identified level comes with a calculated probability, indicating how likely it is to act as a true support or resistance based on historical data.

Retest & Break Labels : The indicator clearly marks on your chart when a detected support or resistance level is retested (price touches and respects the level) or broken (price decisively crosses through the level).

Alerts : Real-time alerts for support retests, resistance retests, support breaks, and resistance breaks.

Customizable : You can change support & resistance line style, width and colors.

🚩 UNIQUENESS

What makes this indicator truly unique is its application of logistic regression to the concept of support and resistance. Instead of merely identifying historical highs and lows, our indicator uses a statistical model to predict the future efficacy of these levels. It analyzes underlying market conditions (like RSI and body size at pivot formation) to assign a probability to each potential S/R zone. This predictive insight, combined with dynamic, real-time labeling of retests and breaks, provides a more robust and adaptive understanding of market structure than traditional, purely historical methods.

📌HOW DOES IT WORK ?

The Logistic Regression Support / Resistance indicator operates in several key steps:

First, it identifies significant pivot highs and lows on the chart based on a user-defined "Pivot Length." These pivots are potential areas of support or resistance.

For each detected pivot, the indicator extracts relevant market data at that specific point, including the RSI (Relative Strength Index) and the Body Size (the absolute difference between the open and close price of the candle). These serve as input features for the model.

The core of the indicator lies in its logistic regression model. This model is continuously trained on past pivot data and their subsequent behavior (i.e., whether they were "respected" as support/resistance multiple times). It learns the relationship between the extracted features (RSI, Body Size) and the likelihood of a pivot becoming a significant S/R level.

When a new pivot is identified, the model uses its learned insights to calculate a prediction value—a probability (from 0 to 1) that this specific pivot will act as a strong support or resistance.

If the calculated probability exceeds a user-defined "Probability Threshold," the pivot is designated a "Regression Pivot" and drawn on the chart as a support or resistance line. The indicator then actively tracks how price interacts with these levels, displaying "R" labels for retests when the price bounces off the level and "B" labels for breaks when the price closes beyond it.

⚙️ SETTINGS

1. General Configuration

Pivot Length: This setting defines the number of bars used to determine a significant high or low for pivot detection.

Target Respects: This input specifies how many times a level must be "respected" by price action for it to be considered a strong support or resistance level by the underlying model.

Probability Threshold: This is the minimum probability output from the logistic regression model for a detected pivot to be considered a valid support or resistance level and be plotted on the chart.

2. Style

Show Prediction Labels: Enable or disable labels that display the calculated probability of a newly identified regression S/R level.

Show Retests: Toggle the visibility of "R" labels on the chart, which mark instances where price has retested a support or resistance level.

Show Breaks: Toggle the visibility of "B" labels on the chart, which mark instances where price has broken through a support or resistance level.

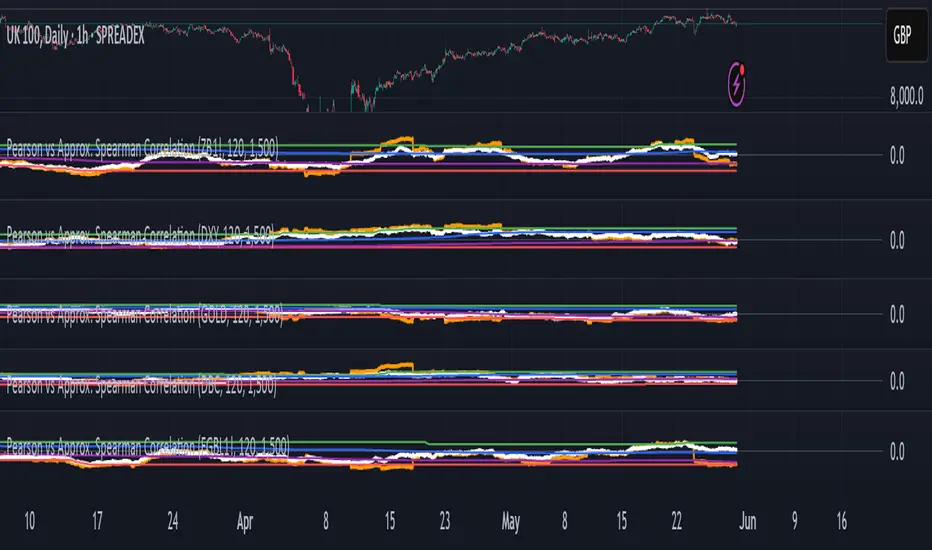

Pearson vs Approx. Spearman CorrelationThis indicator displays the rolling Pearson and approximate Spearman correlation between the chart's asset and a second user-defined asset, based on log returns over a customizable window.

Features:

- Pearson correlation of log returns (standard linear dependency measure)

- Approximate Spearman correlation, using percentile ranks to better capture nonlinear and monotonic relationships

/ Horizontal lines showing:

Maximum and minimum correlation values over a statistical window

1st quartile (25%) and 3rd quartile (75%) — helpful for identifying statistically high or low regimes

This script is useful for identifying dynamic co-movements, regime changes, or correlation breakdowns between assets — applicable in risk management, portfolio construction, and pairs trading strategies.

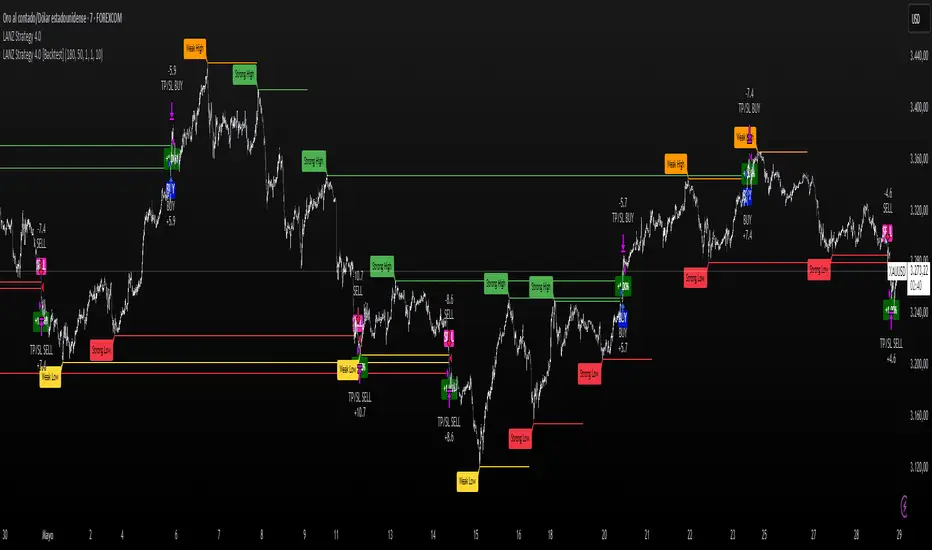

LANZ Strategy 4.0 [Backtest]🔷 LANZ Strategy 4.0 — Strategy Execution Based on Confirmed Structure + Risk-Based SL/TP

LANZ Strategy 4.0 is the official backtesting engine for the LANZ Strategy 4.0 trading logic. It simulates real-time executions based on breakout of Strong/Weak Highs or Lows, using a consistent structural system with SL/TP dynamically calculated per trade. With integrated risk management and lot size logic, this script allows traders to validate LANZ Strategy 4.0 performance with real strategy metrics.

🧠 Core Components:

Confirmed Breakout Entries: Trades are executed only when price breaks the most recent structural level (Strong High or Strong Low), detected using swing pivots.

Dynamic SL and TP Logic: SL is placed below/above the breakout point with a customizable buffer. TP is defined using a fixed Risk-Reward (RR) ratio.

Capital-Based Risk Management: Lot size is calculated based on account equity, SL distance, and pip value (e.g. $10 per pip on XAUUSD).

Clean and Controlled Executions: Only one trade is active at a time. No new entries are allowed until the current position is closed.

📊 Visual Features:

Automatic plotting of Entry, SL, and TP levels.

Full control of swing sensitivity (swingLength) and SL buffer.

SL and TP lines extend visually for clarity of trade risk and reward zones.

⚙️ How It Works:

Detects pivots and classifies trend direction.

Waits for breakout above Strong High (BUY) or below Strong Low (SELL).

Calculates dynamic SL and TP based on buffer and RR.

Computes trade size automatically based on risk per trade %.

Executes entry and manages exits via strategy engine.

📝 Notes:

Ideal for evaluating the LANZ Strategy 4.0 logic over historical data.

Must be paired with the original indicator (LANZ Strategy 4.0) for live trading.

Best used on assets with clear structural behavior (gold, indices, FX).

📌 Credits:

Backtest engine developed by LANZ based on the official rules of LANZ Strategy 4.0. This script ensures visual and logical consistency between live charting and backtesting simulations.

AltcoinEvreni Entry/TP RR ToolMulti-Entry / Take-Profit Risk-Reward Tool

This indicator is designed to help traders visually plan and manage their trade entries, take-profit targets, stop-loss levels, and risk/reward calculations directly on the chart.

Key Features:

--- Up to 3 customizable entry levels with separate position sizing for each.

--- Up to 5 take-profit (TP) levels, each with individual allocation percentages.

--- Automatic calculation of weighted average entry price.

--- Dynamic risk and potential profit calculation based on your inputs.

--- Visual colored zones for entry, stop-loss, and take-profit areas on the chart.

--- Adjustable leverage and margin for position sizing.

--- Informative floating table displaying position type, entries, stop-loss, risk in $, potential

--- profit in $, and overall RR ratio.

--- Fully customizable appearance (colors, box width, table font size, etc.).

How to Use:

1- Set your trade direction (Long or Short).

2- Enter your planned entry prices, allocation percentages, and stop-loss.

3- Configure your take-profit levels and their respective allocation percentages.

4- Adjust margin, leverage, and visual preferences as desired.

5- The tool will display all relevant zones and statistics, helping you make better risk-managed trading decisions.

Notes:

--- All calculations and drawings update dynamically as you change your parameters.

--- Works on any symbol and timeframe.

--- For educational and planning purposes – always use your own judgment and risk management.

Candle/Keltner Channels BUY SELLWhy Use Candlesticks?

They help traders visualize price action

Used in technical analysis and price pattern recognition (e.g., Doji, Engulfing, Hammer)

Assist in determining entry and exit points

Why Traders Use Keltner Channels?

Keltner Channels are widely used by traders for identifying trends, detecting volatility, and spotting trade opportunities.

1. Trend Identification

The middle line (EMA) shows the general trend.

If price consistently stays above the middle line, it indicates a strong uptrend.

If price stays below, it signals a downtrend.

Use: Traders follow the trend direction to enter trades in line with momentum.

2. Volatility Measurement

The width of the channel expands and contracts based on Average True Range (ATR).

Wider channels = high volatility, tighter channels = low volatility.

Use: Helps traders decide when to expect breakouts or calm periods.

3. Breakout Signals

A break above the upper band can signal a bullish breakout.

A break below the lower band can signal a bearish breakout.

Use: Traders use this for momentum trading and breakout entries.

4. Overbought/Oversold Conditions

Price touching or crossing the upper band may suggest it's overbought.

Price touching or crossing the lower band may suggest it's oversold.

Use: Traders combine this with RSI or MACD to confirm reversal setups.

5. Trade Entry and Exit

When price pulls back to the middle EMA during a trend, it may present a buy/sell opportunity.

Exits can also be planned if price returns inside the bands after a breakout.

Use: Helps with precise entry and exit timing.

6. Combines Well With Other Indicators

Commonly used with:

RSI (for confirmation)

MACD (for momentum)

Candlestick patterns (for price action signals)

Combining Candlestick Patterns with Keltner Channels gives traders a powerful method to confirm entries, spot reversals, and improve accuracy. Here’s why this combination works so well:

1. Context for Candlestick Signals

Candlestick patterns (like doji, engulfing, or pin bars) show potential price reversals, but they need context to be reliable. Keltner Channels provide that context:

A bullish candlestick near the lower band suggests a stronger buy signal.

A bearish candlestick near the upper band strengthens a sell signal.

2. Filtering False Signals

Candlestick patterns occur frequently, and not all are meaningful.

The location within the Keltner Channel helps filter out weak or false patterns.

Example: A bullish engulfing candle outside the lower band = high-probability reversal.

3. Improved Entry Timing

Traders wait for a candlestick pattern confirmation when price touches or crosses a Keltner band.

This avoids premature entries and allows tighter stop-losses.

4. Better Risk-Reward Setup

Candlestick entry near channel extremes (upper/lower band) lets traders place stop-losses just beyond recent highs/lows.

The target can be the opposite side of the channel or the middle EMA.

5. Visual Simplicity

Keltner Channels + Candles are visually intuitive.

Even beginner traders can easily recognize:

Overextended candles near channel edges.

Confirmed breakouts or reversals.

This Timeframe 5 min : XAUUSD

Correlation Coefficient📊 Correlation Coefficient (CC)

This indicator measures the statistical correlation between two selected securities over a defined period, scaled from -100 to +100.

It helps you quickly assess whether assets are moving:

Together (positive correlation)

Opposite (negative correlation)

Independently (zero correlation)

🔧 Features:

Select any two symbols (default: NIFTY & BANKNIFTY)

Adjustable length parameter for short-term or long-term correlation analysis

Clean, color-coded plot with horizontal levels to easily identify key correlation zones

📈 Useful For:

Pair trading setups

Hedging strategies

Detecting market regime shifts or intermarket divergences

⚠️ Disclaimer: This is not trading or investment advice.

This indicator is intended for informational purposes only and is not recommended for making

direct trading decisions.

Ergodic Market Divergence (EMD)Ergodic Market Divergence (EMD)

Bridging Statistical Physics and Market Dynamics Through Ensemble Analysis

The Revolutionary Concept: When Physics Meets Trading

After months of research into ergodic theory—a fundamental principle in statistical mechanics—I've developed a trading system that identifies when markets transition between predictable and unpredictable states. This indicator doesn't just follow price; it analyzes whether current market behavior will persist or revert, giving traders a scientific edge in timing entries and exits.

The Core Innovation: Ergodic Theory Applied to Markets

What Makes Markets Ergodic or Non-Ergodic?

In statistical physics, ergodicity determines whether a system's future resembles its past. Applied to trading:

Ergodic Markets (Mean-Reverting)

- Time averages equal ensemble averages

- Historical patterns repeat reliably

- Price oscillates around equilibrium

- Traditional indicators work well

Non-Ergodic Markets (Trending)

- Path dependency dominates

- History doesn't predict future

- Price creates new equilibrium levels

- Momentum strategies excel

The Mathematical Framework

The Ergodic Score combines three critical divergences:

Ergodic Score = (Price Divergence × Market Stress + Return Divergence × 1000 + Volatility Divergence × 50) / 3

Where:

Price Divergence: How far current price deviates from market consensus

Return Divergence: Momentum differential between instrument and market

Volatility Divergence: Volatility regime misalignment

Market Stress: Adaptive multiplier based on current conditions

The Ensemble Analysis Revolution

Beyond Single-Instrument Analysis

Traditional indicators analyze one chart in isolation. EMD monitors multiple correlated markets simultaneously (SPY, QQQ, IWM, DIA) to detect systemic regime changes. This ensemble approach:

Reveals Hidden Divergences: Individual stocks may diverge from market consensus before major moves

Filters False Signals: Requires broader market confirmation

Identifies Regime Shifts: Detects when entire market structure changes

Provides Context: Shows if moves are isolated or systemic

Dynamic Threshold Adaptation

Unlike fixed-threshold systems, EMD's boundaries evolve with market conditions:

Base Threshold = SMA(Ergodic Score, Lookback × 3)

Adaptive Component = StDev(Ergodic Score, Lookback × 2) × Sensitivity

Final Threshold = Smoothed(Base + Adaptive)

This creates context-aware signals that remain effective across different market environments.

The Confidence Engine: Know Your Signal Quality

Multi-Factor Confidence Scoring

Every signal receives a confidence score based on:

Signal Clarity (0-35%): How decisively the ergodic threshold is crossed

Momentum Strength (0-25%): Rate of ergodic change

Volatility Alignment (0-20%): Whether volatility supports the signal

Market Quality (0-20%): Price convergence and path dependency factors

Real-Time Confidence Updates

The Live Confidence metric continuously updates, showing:

- Current opportunity quality

- Market state clarity

- Historical performance influence

- Signal recency boost

- Visual Intelligence System

Adaptive Ergodic Field Bands

Dynamic bands that expand and contract based on market state:

Primary Color: Ergodic state (mean-reverting)

Danger Color: Non-ergodic state (trending)

Band Width: Expected price movement range

Squeeze Indicators: Volatility compression warnings

Quantum Wave Ribbons

Triple EMA system (8, 21, 55) revealing market flow:

Compressed Ribbons: Consolidation imminent

Expanding Ribbons: Directional move developing

Color Coding: Matches current ergodic state

Phase Transition Signals

Clear entry/exit markers at regime changes:

Bull Signals: Ergodic restoration (mean reversion opportunity)

Bear Signals: Ergodic break (trend following opportunity)

Confidence Labels: Percentage showing signal quality

Visual Intensity: Stronger signals = deeper colors

Professional Dashboard Suite

Main Analytics Panel (Top Right)

Market State Monitor

- Current regime (Ergodic/Non-Ergodic)

- Ergodic score with threshold

- Path dependency strength

- Quantum coherence percentage

Divergence Metrics

- Price divergence with severity

- Volatility regime classification

- Strategy mode recommendation

- Signal strength indicator

Live Intelligence

- Real-time confidence score

- Color-coded risk levels

- Dynamic strategy suggestions

Performance Tracking (Left Panel)