Value at Risk (VaR/CVaR) - Stop Loss ToolThis script calculates Value at Risk (VaR) and Conditional Value at Risk (CVaR) over a configurable T-bar forward horizon, based on historical T-bar log returns. It plots projected price thresholds that reflect the worst X% of historical return outcomes, helping set statistically grounded stop-loss levels.

A 95% 5-day VaR of −3% means: “In the worst 5% of all historical 5-day periods, losses were 3% or more.” If you're bullish, and your thesis is correct, price should not behave like one of those worst-case scenarios. So if the market starts trading below that 5-day VaR level, it may indicate that your long bias is invalidated, and a stop-loss near that level can help protect against further downside consistent with tail-risk behavior.

How it's different:

Unlike ATR or standard deviation-based methods, which measure recent volatility magnitude, VaR/CVaR incorporate both the magnitude and **likelihood** (5% chance for example) of adverse moves. This makes it better suited for risk-aware position sizing and exits grounded in actual historical return distributions.

How to use for stop placement:

- Set your holding horizon (T) and confidence level (e.g., 95%) in the inputs.

- The script plots a price level below which only the worst 5% (or chosen %) of T-bar returns have historically occurred (VaR).

- If price approaches or breaches the VaR line, your bullish/bearish thesis may be invalidated.

- CVaR gives a deeper threshold: the average loss **if** things go worse than VaR — useful for a secondary or emergency stop.

FURTHER NOTES FROM SOURCE CODE:

//======================================================================//

// If you're bullish (expecting the price to go up), then under normal circumstances, prices should not behave like they do on the worst-case days.

// If they are — you're probably wrong, or something unexpected is happening. Basically, returns shouldn't be exhibiting downside tail-like behavior if you're bullish.

// VaR(95%, T) gives the threshold below which the price falls only 5% of the time historically, over T days/bars and considering N historical samples.

// CVaR tells you the expected/average price level if that adverse move continues

// Caveats:

// For a variety of reasons, VaR underestimates volatility, despite using historical returns directly rather than making normality assumptions

// as is the case with the standard historicalvol/bollinger band/stdev/ATR approaches)

// Volatility begets volatility (volatility clustering), and VaR is not a conditional probability on recent volatility so it likely underestimates the true volatility of an adverse event

// Regieme shifts occur (bullish phase after prolonged bearish behavior), so upside/short VaR would underestimate the best-case days in the beginning of that move, depending on lookahead horizon/sampling period

// News/events happen, and maybe your sampling period doesn't contain enough event-driven returns to form reliable stats

// In general of course, this tool assumes past return distributions are reflective of forward risk (not the case in non-stationary time series)

// Thus, this tool is not predictive — it shows historical tail risk, not guaranteed outcomes.

// Also, when forming log-returns, overlapping windows of returns are used (to get more samples), but this introduces autocorrelation (if it wasn't there already). This means again, the true VaR is underestimated.

// Description:

// This script calculates and plots both Value at Risk (VaR) and

// Conditional Value at Risk (CVaR) for a given confidence level, using

// historical log returns. It computes both long-side (left tail) and

// short-side (right tail) risk, and converts them into price thresholds (red and green lines respectively).

//

// Key Concepts:

// - VaR: "There is a 95% chance the loss will be less than this value over T days. Represents the 95th-percentile worst empirical returns observed in the sampling period, over T bars.

// - CVaR: "Given that the loss exceeds the VaR, the average of those worst 5% losses is this value. (blue line)" Expected tail loss. If the worst case breached, how bad can it get on average

// - For shorts, the script computes the mirror (right-tail) equivalents.

// - Use T-day log returns if estimating risk over multiple days forward.

// - You can see instances where the VaR for time T, was surpassed historically with the "backtest" boolean

//

// Usage for Stop-Loss:

// - LONG POSITIONS:

// • 95th percentile means, 5% of the time (1 in 20 times) you'd expect to get a VaR level loss (touch the red line), over the next T bars.

// • VaR threshold = minimum price expected with (1 – confidence)% chance.

// • CVaR threshold = expected price if that worst-case zone is breached.

// → Use as potential stop-loss (VaR) or disaster stop (CVaR). If you're bullish (and you're right), price should not be exhibiting returns consistent with the worst 5% of days/T_bars historically.

//======================================================================//

Statistics

1A Monthly P&L Table - Using Library1A Monthly P&L Table: Track Your Performance Month-by-Month

Overview:

The 1A Monthly P&L Table is a straightforward yet powerful indicator designed to give you an immediate overview of your asset's (or strategy's) percentage performance on a monthly basis. Displayed conveniently in the bottom-right corner of your chart, this tool helps you quickly assess historical gains and losses, making it easier to analyze trends in performance over time.

Key Features:

Monthly Performance at a Glance: Clearly see the percentage change for each past month.

Cumulative P&L: A running total of the displayed monthly P&L is provided, giving you a quick sum of performance over the selected period.

Customizable Display:

Months to Display: Choose how many past months you want to see in the table (from 1 to 60 months).

Text Size: Adjust the text size (Tiny, Small, Normal, Large, Huge) to fit your viewing preferences.

Text Color: Customize the color of the text for better visibility against your chart background.

Intraday & Daily Compatibility: The table is optimized to display on daily and intraday timeframes, ensuring it's relevant for various trading styles. (Note: For very long-term analysis on weekly/monthly charts, you might consider other tools, as this focuses on granular monthly P&L.)

How It Works:

The indicator calculates the percentage change from the close of the previous month to the close of the current month. For the very first month displayed, it calculates the P&L from the opening price of the chart's first bar to the close of that month. This data is then neatly organized into a table, updated on the last bar of the day or session.

Ideal For:

Traders and investors who want a quick, visual summary of monthly performance.

Analyzing seasonal trends or consistent periods of profitability/drawdown.

Supplementing backtesting results with a clear month-by-month breakdown.

Settings:

Text Color: Changes the color of all text within the table.

Text Size: Controls the font size of the table content.

Months to Display: Determines the number of recent months included in the table.

MonthlyPnLTableLibrary "MonthlyPnLTable"

monthlyPnL(currentClose, initialOpenPrice, monthsToDisplay)

Parameters:

currentClose (float)

initialOpenPrice (float)

monthsToDisplay (int)

displayPnLTable(pnls, pnlMonths, pnlYears, textSizeOption, labelColor)

Parameters:

pnls (array)

pnlMonths (array)

pnlYears (array)

textSizeOption (string)

labelColor (color)

LANZ Strategy 3.0 [Backtest]🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Scalping Strategy

LANZ Strategy 3.0 is a precision-engineered backtesting tool tailored for intraday traders who rely on the Asian session range to determine directional bias. This strategy implements dynamic Fibonacci projections and strict time-window validation to simulate a clean and disciplined trading environment.

🧠 Core Components:

Asian Range Bias Definition: Direction is established between 01:15–02:15 a.m. NY time based on the candle’s close in relation to the midpoint of the Asian session range (18:00–01:15 NY).

Limit Order Execution: Only one trade is placed daily, using a limit order at the Asian range high (for sells) or low (for buys), between 01:15–08:00 a.m. NY.

Fibonacci-Based TP/SL:

Original Mode: TP = 2.25x range, SL = 0.75x range.

Optimized Mode: TP = 1.95x range, SL = 0.65x range.

No Trade After 08:00 NY: If the limit order is not executed before 08:00 a.m. NY, it is canceled.

Fallback Logic at 02:15 NY: If the market direction misaligns with the setup at 02:15 a.m., the system re-evaluates and can re-issue the order.

End-of-Day Closure: All positions are closed at 15:45 NY if still open.

📊 Backtest-Ready Design:

Entries and exits are executed using strategy.entry() and strategy.exit() functions.

Position size is fixed via capital risk allocation ($100 per trade by default).

Only one position can be active at a time, ensuring controlled risk.

📝 Notes:

This strategy is ideal for assets sensitive to the Asian/London session overlap, such as Forex pairs and indices.

Easily switch between Fibonacci versions using a single dropdown input.

Fully deterministic: all entries are based on pre-defined conditions and time constraints.

👤 Credits:

Strategy developed by rau_u_lanz using Pine Script v6. Built for traders who favor clean sessions, directional clarity, and consistent execution using time-based logic and Fibonacci projections.

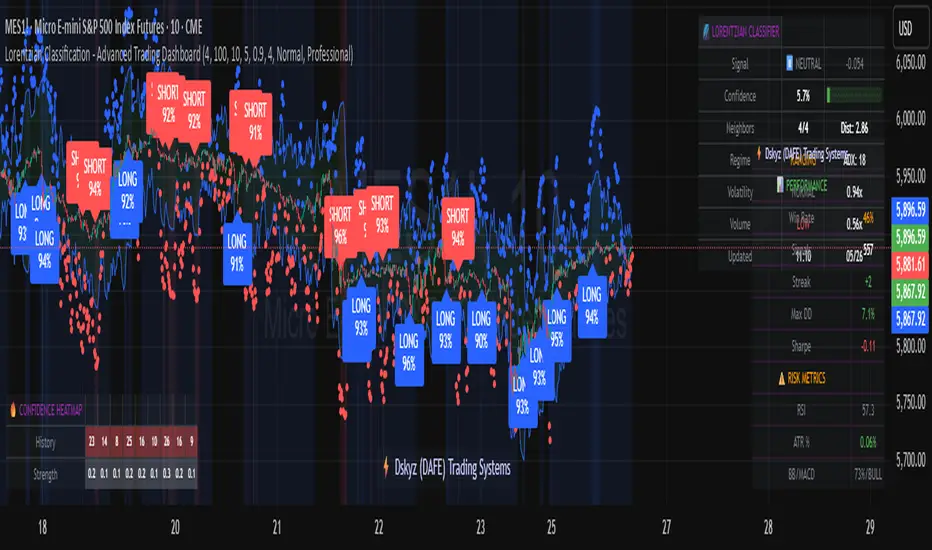

Lorentzian Classification - Advanced Trading DashboardLorentzian Classification - Relativistic Market Analysis

A Journey from Theory to Trading Reality

What began as fascination with Einstein's relativity and Lorentzian geometry has evolved into a practical trading tool that bridges theoretical physics and market dynamics. This indicator represents months of wrestling with complex mathematical concepts, debugging intricate algorithms, and transforming abstract theory into actionable trading signals.

The Theoretical Foundation

Lorentzian Distance in Market Space

Traditional Euclidean distance treats all feature differences equally, but markets don't behave uniformly. Lorentzian distance, borrowed from spacetime geometry, provides a more nuanced similarity measure:

d(x,y) = Σ ln(1 + |xi - yi|)

This logarithmic formulation naturally handles:

Scale invariance: Large price moves don't overwhelm small but significant patterns

Outlier robustness: Extreme values are dampened rather than dominating

Non-linear relationships: Captures market behavior better than linear metrics

K-Nearest Neighbors with Relativistic Weighting

The algorithm searches historical market states for patterns similar to current conditions. Each neighbor receives weight inversely proportional to its Lorentzian distance:

w = 1 / (1 + distance)

This creates a "gravitational" effect where closer patterns have stronger influence on predictions.

The Implementation Challenge

Creating meaningful market features required extensive experimentation:

Price Features: Multi-timeframe momentum (1, 2, 3, 5, 8 bar lookbacks) Volume Features: Relative volume analysis against 20-period average

Volatility Features: ATR and Bollinger Band width normalization Momentum Features: RSI deviation from neutral and MACD/price ratio

Each feature undergoes min-max normalization to ensure equal weighting in distance calculations.

The Prediction Mechanism

For each current market state:

Feature Vector Construction: 12-dimensional representation of market conditions

Historical Search: Scan lookback period for similar patterns using Lorentzian distance

Neighbor Selection: Identify K nearest historical matches

Outcome Analysis: Examine what happened N bars after each match

Weighted Prediction: Combine outcomes using distance-based weights

Confidence Calculation: Measure agreement between neighbors

Technical Hurdles Overcome

Array Management: Complex indexing to prevent look-ahead bias

Distance Calculations: Optimizing nested loops for performance

Memory Constraints: Balancing lookback depth with computational limits

Signal Filtering: Preventing clustering of identical signals

Advanced Dashboard System

Main Control Panel

The primary dashboard provides real-time market intelligence:

Signal Status: Current prediction with confidence percentage

Neighbor Analysis: How many historical patterns match current conditions

Market Regime: Trend strength, volatility, and volume analysis

Temporal Context: Real-time updates with timestamp

Performance Analytics

Comprehensive tracking system monitors:

Win Rate: Percentage of successful predictions

Signal Count: Total predictions generated

Streak Analysis: Current winning/losing sequence

Drawdown Monitoring: Maximum equity decline

Sharpe Approximation: Risk-adjusted performance estimate

Risk Assessment Panel

Multi-dimensional risk analysis:

RSI Positioning: Overbought/oversold conditions

ATR Percentage: Current volatility relative to price

Bollinger Position: Price location within volatility bands

MACD Alignment: Momentum confirmation

Confidence Heatmap

Visual representation of prediction reliability:

Historical Confidence: Last 10 periods of prediction certainty

Strength Analysis: Magnitude of prediction values over time

Pattern Recognition: Color-coded confidence levels for quick assessment

Input Parameters Deep Dive

Core Algorithm Settings

K Nearest Neighbors (1-20): More neighbors create smoother but less responsive signals. Optimal range 5-8 for most markets.

Historical Lookback (50-500): Deeper history improves pattern recognition but reduces adaptability. 100-200 bars optimal for most timeframes.

Feature Window (5-30): Longer windows capture more context but reduce sensitivity. Match to your trading timeframe.

Feature Selection

Price Changes: Essential for momentum and reversal detection Volume Profile: Critical for institutional activity recognition Volatility Measures: Key for regime change detection Momentum Indicators: Vital for trend confirmation

Signal Generation

Prediction Horizon (1-20): How far ahead to predict. Shorter horizons for scalping, longer for swing trading.

Signal Threshold (0.5-0.9): Confidence required for signal generation. Higher values reduce false signals but may miss opportunities.

Smoothing (1-10): EMA applied to raw predictions. More smoothing reduces noise but increases lag.

Visual Design Philosophy

Color Themes

Professional: Corporate blue/red for institutional environments Neon: Cyberpunk cyan/magenta for modern aesthetics

Matrix: Green/red hacker-inspired palette Classic: Traditional trading colors

Information Hierarchy

The dashboard system prioritizes information by importance:

Primary Signals: Largest, most prominent display

Confidence Metrics: Secondary but clearly visible

Supporting Data: Detailed but unobtrusive

Historical Context: Available but not distracting

Trading Applications

Signal Interpretation

Long Signals: Prediction > threshold with high confidence

Look for volume confirmation

- Check trend alignment

- Verify support levels

Short Signals: Prediction < -threshold with high confidence

Confirm with resistance levels

- Check for distribution patterns

- Verify momentum divergence

- Market Regime Adaptation

Trending Markets: Higher confidence in directional signals

Ranging Markets: Focus on reversal signals at extremes

Volatile Markets: Require higher confidence thresholds

Low Volume: Reduce position sizes, increase caution

Risk Management Integration

Confidence-Based Sizing: Larger positions for higher confidence signals

Regime-Aware Stops: Wider stops in volatile regimes

Multi-Timeframe Confirmation: Align signals across timeframes

Volume Confirmation: Require volume support for major signals

Originality and Innovation

This indicator represents genuine innovation in several areas:

Mathematical Approach

First application of Lorentzian geometry to market pattern recognition. Unlike Euclidean-based systems, this naturally handles market non-linearities.

Feature Engineering

Sophisticated multi-dimensional feature space combining price, volume, volatility, and momentum in normalized form.

Visualization System

Professional-grade dashboard system providing comprehensive market intelligence in intuitive format.

Performance Tracking

Real-time performance analytics typically found only in institutional trading systems.

Development Journey

Creating this indicator involved overcoming numerous technical challenges:

Mathematical Complexity: Translating theoretical concepts into practical code

Performance Optimization: Balancing accuracy with computational efficiency

User Interface Design: Making complex data accessible and actionable

Signal Quality: Filtering noise while maintaining responsiveness

The result is a tool that brings institutional-grade analytics to individual traders while maintaining the theoretical rigor of its mathematical foundation.

Best Practices

- Parameter Optimization

- Start with default settings and adjust based on:

Market Characteristics: Volatile vs. stable

Trading Timeframe: Scalping vs. swing trading

Risk Tolerance: Conservative vs. aggressive

Signal Confirmation

Never trade on Lorentzian signals alone:

Price Action: Confirm with support/resistance

Volume: Verify with volume analysis

Multiple Timeframes: Check higher timeframe alignment

Market Context: Consider overall market conditions

Risk Management

Position Sizing: Scale with confidence levels

Stop Losses: Adapt to market volatility

Profit Targets: Based on historical performance

Maximum Risk: Never exceed 2-3% per trade

Disclaimer

This indicator is for educational and research purposes only. It does not constitute financial advice or guarantee profitable trading results. The Lorentzian classification system reveals market patterns but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

Market dynamics are inherently uncertain, and past performance does not guarantee future results. This tool should be used as part of a comprehensive trading strategy, not as a standalone solution.

Bringing the elegance of relativistic geometry to market analysis through sophisticated pattern recognition and intuitive visualization.

Thank you for sharing the idea. You're more than a follower, you're a leader!

@vasanthgautham1221

Trade with precision. Trade with insight.

— Dskyz , for DAFE Trading Systems

Eigenvector Centrality Drift (ECD) - Market State Network What is Eigenvector Centrality Drift (ECD)?

Eigenvector Centrality Drift (ECD) is a groundbreaking indicator that applies concepts from network science to financial markets. Instead of viewing price as a simple series, ECD models the market as a dynamic network of “micro-states”—distinct combinations of price, volatility, and volume. By tracking how the influence of these states changes over time, ECD helps you spot regime shifts and transitions in market character before they become obvious in price.

This is not another moving average or momentum oscillator. ECD is inspired by eigenvector centrality—a measure of influence in network theory—and adapts it to the world of price action, volatility, and volume. It’s about understanding which market states are “in control” and when that control is about to change.

Theoretical Foundation

Network Science: In complex systems, nodes (states) and edges (transitions) form a network. Eigenvector centrality measures how influential a node is, not just by its direct connections, but by the influence of the nodes it connects to.

Market Micro-States: Each bar is classified into a “state” based on price change, volatility, and volume. The market transitions between these states, forming a network of possible regimes.

Centrality Drift: By tracking the centrality (influence) of the current state, and how it changes (drifts) over time, ECD highlights when the market’s “center of gravity” is shifting—often a precursor to major moves or regime changes.

How ECD Works

State Classification: Each bar is assigned to one of N market micro-states, based on a weighted combination of normalized price change, volatility, and volume.

Transition Matrix: Over a rolling window, ECD tracks how often the market transitions from each state to every other state, forming a transition probability matrix.

Centrality Calculation: Using a simplified eigenvector approach, ECD calculates the “influence” score for each state, reflecting how central it is to the network of recent market behavior.

Centrality Drift: The indicator tracks the Z-score of the change in centrality for the current state. Rapid increases or decreases, or a shift in the dominant state, signal a potential regime shift.

Dominant State: ECD also highlights which state currently has the highest influence, providing insight into the prevailing market character.

Inputs:

🌐 Market State Configuration

Number of Market States (n_states, default 6): Number of distinct micro-states to track.

3–4: Simple (Up/Down/Sideways)

5–6: Balanced (recommended)

7–9: Complex, more nuanced

Price Change Weight (price_weight, default 0.4):

How much price movement defines a state. Higher = more directional.

Volatility Weight (vol_weight, default 0.3):

How much volatility defines a state. Higher = more regime focus.

Volume Weight (volume_weight, default 0.3):

How much volume defines a state. Higher = more participation focus.

🔗 Network Analysis

Transition Matrix Window (transition_window, default 50): Lookback for building the state transition matrix.

Shorter: Adapts quickly

Longer: More stable

Influence Decay Factor (influence_decay, default 0.85): How much influence propagates through the network.

Higher: Distant transitions matter more

Lower: Only immediate transitions matter

Drift Detection Sensitivity (drift_sensitivity, default 1.5): Z-score threshold for significant centrality drift.

Lower: More signals

Higher: Only major shifts

🎨 Visualization

Show Network Visualization (show_network, default true): Background color and effects based on network structure.

Show Centrality Score (show_centrality, default true): Plots the current state’s centrality measure.

Show Drift Indicator (show_drift, default true): Plots the centrality drift Z-score.

Show State Map (show_state_map, default true): Dashboard showing all state centralities and which is dominant.

Color Scheme (color_scheme, default "Quantum"):

“Quantum”: Cyan/Magenta

“Neural”: Green/Blue

“Plasma”: Yellow/Pink

“Matrix”: Green/Black

Color Schemes

Dynamic gradients reflect the current state’s centrality and drift, using your chosen color palette.

Background network effect: The more central the current state, the more intense the background.

Centrality and drift lines: Color-coded for clarity and regime shift detection.

Visual Logic

Centrality Score Line: Plots the influence of the current state, with glow for emphasis.

Drift Indicator: Histogram of centrality drift Z-score, green for positive, red for negative.

Threshold Lines: Dotted lines mark the drift sensitivity threshold for regime shift alerts.

State Map Dashboard: Top-right panel shows all state centralities, highlights the current and dominant state, and visualizes influence with bars.

Information Panel: Bottom-left panel summarizes current state, centrality, dominant state, drift Z-score, and regime shift status.

How to Use ECD

Centrality Score: High = current state is highly influential; low = state is peripheral.

Drift Z-Score:

Large positive/negative = rapid change in influence, regime shift likely.

Near zero = stable network, no major shift.

Dominant State: The state with the highest centrality is “in control” of the market’s transitions.

State Map: Use to see which states are rising or falling in influence.

Tips:

Use fewer states for simple markets, more for nuanced analysis.

Watch for drift Z-score crossing the threshold—these are your regime shift signals.

Combine with your own system for confirmation.

Alerts:

ECD Regime Shift: Significant centrality drift detected—potential regime change.

ECD State Change: Market state transition occurred.

ECD Dominance Shift: Dominant market state has changed.

Originality & Usefulness

ECD is not a mashup or rehash of standard indicators. It is a novel application of network science and eigenvector centrality to market microstructure, providing a new lens for understanding regime shifts and market transitions. The state network, centrality drift, and dashboard are unique to this script. ECD is designed for anticipation, not confirmation—helping you see the market’s “center of gravity” shift before price action makes it obvious.

Chart Info

Script Name: Eigenvector Centrality Drift (ECD) – Market State Network

Recommended Use: Any asset, any timeframe. Tune parameters to your style.

Disclaimer

This script is for research and educational purposes only. It does not provide financial advice or direct buy/sell signals. Always use proper risk management and combine with your own strategy. Past performance is not indicative of future results.

See the market as a network. Anticipate the shift in influence.

— Dskyz , for DAFE Trading Systems

H4 Swing Grade Checklist English V.1✅ H4 Swing Grade Checklist – Auto Grading for Smart Money Setups

This script helps manual traders assess the quality of a Smart Money swing trade setup by checking 7 key criteria. The system assigns a grade (A+, A, A−, or B) based on how many and which checklist items are met.

📋 Checklist Items (7 total):

✅ Sweep occurs within 4 candles

✅ MSS (strong break candle)

✅ Entry is placed outside the wick of the sweep

✅ FVG is fresh (not previously used)

✅ FVG overlaps Fibonacci 0.705 level

✅ FVG lies within Premium or Discount zone

✅ Entry is placed at 0.705 Fibonacci retracement

🏅 Grading Criteria:

A+ → All 7 checklist items are satisfied

A → Only missing #5 (FVG Overlap with 0.705)

A− → Only missing #4 (FVG Fresh)

B → Only missing #2 (MSS – clear break of structure)

– → Any other combinations / fewer than 6 conditions met

⚙️ Features:

Toggle visibility with one click

Fixed display in top-right or bottom-right of the chart

Color-coded grading logic (Green, Yellow, Orange, Blue)

Clear checklist feedback for trade journaling or evaluation

🚀 Ideal For:

ICT / Smart Money traders

Prop firm evaluations

Swing trade quality control

Information Asymmetry Gradient (IAG) What is the Information Asymmetry Gradient (IAG)?

The Information Asymmetry Gradient (IAG) is a unique market regime and imbalance detector that quantifies the subtle, directional “information flow” in price and volume. Inspired by information theory and market microstructure, IAG is designed to help traders spot the early buildup of conviction or surprise—the kind of hidden imbalance that often precedes major price moves.

Unlike traditional volume or momentum indicators, IAG focuses on the efficiency and directionality of information transfer: how much “informational energy” is being revealed by up-moves versus down-moves, normalized by price movement. It’s not just about net flow, but about the quality and asymmetry of that flow.

Theoretical Foundation

Information Asymmetry: Markets move when new information is revealed. If one side (buyers or sellers) is consistently more “informationally efficient” per unit of price change, an imbalance is building—even if price hasn’t moved much yet.

Gradient: By tracking the rate of change (gradient) between fast and slow information flows, IAG highlights when a subtle imbalance is accelerating.

Volatility of Asymmetry: Sudden spikes in the volatility of information asymmetry often signal regime uncertainty or the approach of a “surprise” move.

How IAG Works

Directional Information Content: For each bar, IAG estimates the “information per unit of price change” for both up-moves and down-moves, using volume and price action.

Asymmetry Calculation: Computes the difference (or ratio) between up and down information content, revealing directional bias.

Gradient Detection: Calculates both a fast and slow EMA of the asymmetry, then measures their difference (the “gradient”), normalized as a Z-score.

Volatility of Asymmetry: Tracks the standard deviation of asymmetry over a rolling window, with Z-score normalization to spot “information shocks.”

Flow Strength: Quantifies the conviction of the current information flow on a 0–100 scale.

Regime Detection: Flags “extreme” asymmetry, “building” flow, and “high volatility” states.

Inputs:

🌌 Core Asymmetry Parameters

Fast Information Period (short_len, default 8): EMA period for detecting immediate information flow changes.

5–8: Scalping (1–5min)

8–12: Day trading (15min–1hr)

12–20: Swing trading (4hr+)

Slow Information Period (long_len, default 34): EMA period for baseline information context. Should be 3–5x fast period.

Default (34): Fibonacci number, stable for most assets.

Gradient Smoothing (gradient_smooth, default 3): Smooths the gradient calculation.

1–2: Raw, responsive

3–5: Balanced

6–10: Very smooth

📊 Asymmetry Method

Calculation Mode (calc_mode, default "Weighted"):

“Simple”: Basic volume split by direction

“Weighted”: Volume × price movement (default, most robust)

“Logarithmic”: Log-scaled for large moves

Use Ratio (show_ratio, default false):

“Difference”: UpInfo – DownInfo (additive)

“Ratio”: UpInfo / DownInfo (multiplicative, better for comparing volatility regimes)

🌊 Volatility Analysis

Volatility Window (stdev_len, default 21): Lookback for measuring asymmetry volatility.

Volatility Alert Level (vol_threshold, default 1.5): Z-score threshold for volatility alerts.

🎨 Visual Settings

Color Theme (color_theme, default "Starry Night"):

Van Gogh-inspired palettes:

“Starry Night”: Deep blues and yellows

“Sunflowers”: Warm yellows and browns

“Café Terrace”: Night blues and warm lights

“Wheat Field”: Golden and sky blue

Show Swirl Effects (show_swirls, default true): Adds swirling background to visualize information turbulence.

Show Signal Stars (show_stars, default true): Star markers at significant asymmetry points.

Show Info Dashboard (show_dashboard, default true): Top-right panel with current metrics and market state.

Show Flow Visualization (show_flow, default true): Main gradient line with artistic effects.

Color Schemes

Dynamic color gradients adapt to both the direction and intensity of the information gradient, using Van Gogh-inspired palettes for visual clarity and artistic flair.

Glow and aura effects: The main line is layered with glows for depth and to highlight strong signals.

Swirl background: Visualizes the “turbulence” of information flow, darker and more intense as flow strength and volatility rise.

Visual Logic

Main Gradient Line: Plots the normalized information gradient (Z-score), color-coded by direction and intensity.

Glow/Aura: Multiple layers for visual depth and to highlight strong signals.

Threshold Zones: Dotted lines and filled areas mark “Building” and “Extreme” asymmetry zones.

Volatility Ribbon: Area plot of volatility Z-score, highlighting information shocks.

Signal Stars: Circular markers at each “Extreme” event, color-coded for bullish/bearish; cross markers for volatility spikes.

Dashboard: Top-right panel shows current status (Extreme, Building, High Volatility, Balanced), gradient value, flow strength, information balance, and volatility status.

Trading Guide: Bottom-left panel explains all states and how to interpret them.

How to Use IAG

🌟 EXTREME: Major information imbalance—potential for explosive move or reversal.

🌙 BUILDING: Asymmetry is forming—watch for a breakout or trend acceleration.

🌪️ HIGH VOLATILITY: Information flow is unstable—expect regime uncertainty or “surprise” moves.

☁️ BALANCED: No clear bias—market is in equilibrium.

Positive Gradient: Bullish information flow (buyers have the edge).

Negative Gradient: Bearish information flow (sellers have the edge).

Flow >66%: Strong conviction—crowd is acting in unison.

Volatility Spike: Regime uncertainty—be alert for sudden moves.

Tips:

- Use lower periods for scalping, higher for swing trading.

- “Weighted” mode is most robust for most assets.

- Combine with price action or your own system for confirmation.

- Works on all assets and timeframes—tune to your style.

Alerts

IAG Extreme Asymmetry: Extreme information asymmetry detected.

IAG Building Flow: Information flow building.

IAG High Volatility: Information volatility spike.

IAG Bullish/Bearish Extreme: Directional extreme detected.

Originality & Usefulness

IAG is not a mashup of existing indicators. It is a novel approach to quantifying the “surprise” or “conviction” element in market moves, focusing on the efficiency and directionality of information transfer per unit of price change. The multi-layered color logic, artistic visual effects, and regime dashboard are unique to this script. IAG is designed for anticipation, not confirmation—helping you see subtle imbalances before they become obvious in price.

Chart Info

Script Name: Information Asymmetry Gradient (IAG) – Starry Night

Recommended Use: Any asset, any timeframe. Tune parameters to your style.

Disclaimer

This script is for research and educational purposes only. It does not provide financial advice or direct buy/sell signals. Always use proper risk management and combine with your own strategy. Past performance is not indicative of future results.

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

multi-tf standard devs [keypoems]Multi-Timeframe Standard Deviations Levels

A visual map of “how far is too far” across any three higher time-frames.

1. What it does

This script plots dynamic price “rails” built from standard deviation (StDev)—the same math that underpins the bell curve—on up to three higher-time-frames (HTFs) at once.

• It measures the volatility of intraday open-to-close increments, reaching back as far as 5000 bars (≈ 20 years on daily data).

• Each HTF can be extended to the next session or truncated at session close for tidy dashboards.

• Lines can be mirrored so you see symmetric positive/negative bands, and optional background fills shade the “probability cone.”

Because ≈ 68 % of moves live inside ±1 StDev, ≈ 95 % inside ±2, and ≈ 99.7 % inside ±3, the plot instantly shows when price is statistically stretched or compressed.

3. Key settings

Higher Time-Frame #1-3 Turn each HTF on/off, pick the interval (anything from 1 min to 1 year), and decide whether lines should extend into the next period.

Show levels for last X days Keep your chart clean by limiting how many historical sessions are displayed (1-50).

Based on last X periods Length of the StDev sample. Long look-backs (e.g. 5 000) iron-out day-to-day noise; short look-backs make the bands flex with recent volatility.

Fib Settings Toggle each multiple, line thickness/style/colour, label size, whether to print the numeric level, the live price, the HTF label, and whether to tint the background (choose your own opacity).

4. Under-the-hood notes

StDev is calculated on (close – open) / open rather than absolute prices, making the band width scale-agnostic.

Watch for tests of ±1:

Momentum traders ride the breakout with a target at the next band.

Mean-reversion traders wait for the first stall candle and trade back to zero line or VWAP.

Bottom line: Multi-Timeframe Standard-Deviations turns raw volatility math into an intuitive “price terrain map,” helping you instantly judge whether a move is ordinary, stretched, or extreme—across the time-frames that matter to you.

Original code by fadizeidan and stats by NQStats's ProbableChris.

Bullish Volume AnomalyAnomaly is designed to spot hidden bullish accumulation before price actually breaks out, by blending a trend-aware volume measure with a volatility-adjusted price channel. Here’s how it works:

First, it runs a simple ATR-based zigzag to identify the current swing direction. Volume is then signed (+ for up-trends, – for down-trends) and cumulatively summed. By converting that cumulative signed volume into a z-score over the past 480 bars, we get a sense of when buying or selling pressure is unusually strong relative to its own history.

At the same time, price itself is normalized into a z-score over the same 480-bar window, and its change over that period is also tracked. These two measures—volume z-score (s) and price z-score (p)—are compared, and the indicator looks for moments when s outpaces p by at least two standard deviations (s – p > 2), while price momentum change remains low (c < 1) and the net volume is positive (s > 0). That combination flags instances where heavy buying is taking place but price hasn’t yet reacted.

To define a dynamic trading zone, it plots a 288-bar EMA of price as the middle band (t2), and builds upper and lower bands around it using the average close-to-open range multiplied by a user-set factor. The lower band (t1) sits beneath the EMA by that volatility-based margin. A signal fires only when the bar’s high stays below t1—meaning price is still “sleeping” under the lower volatility boundary even as bullish volume builds up.

Together, these filters home in on anomalies: strong, trend-aligned volume surges that outstrip price movement, occurring while price sits below its lower volatility band. In practice, that often marks early accumulation before a breakout. You can tweak the ATR length and multiplier for the zigzag, as well as the channel period and range factor, to suit different markets or timeframes.

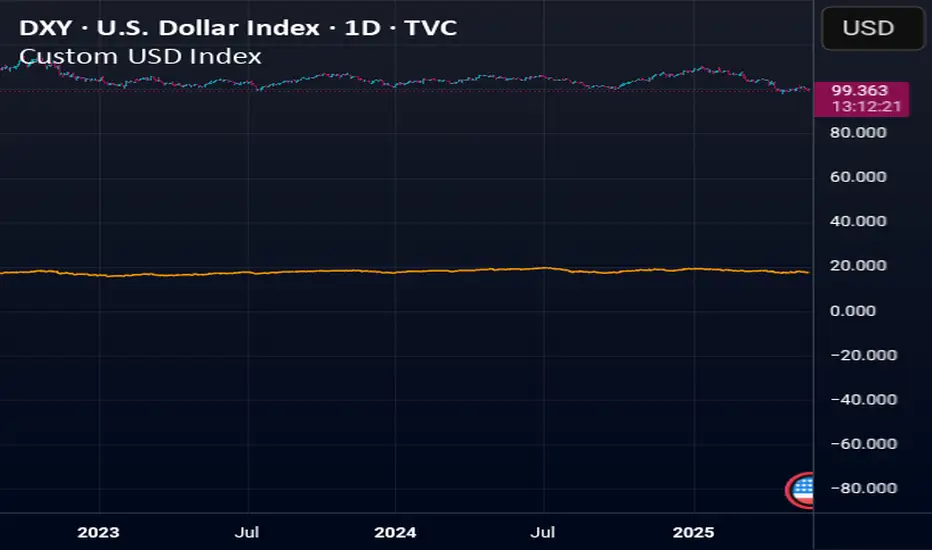

Normalized DXY+Custom USD Index (DXY+) – Normalized Dollar Strength with Bitcoin, Gold, and Yuan.

This custom USD strength index replicates the structure of the official U.S. Dollar Index (DXY), while expanding it to include modern financial assets such as Bitcoin (BTC), Ethereum (ETH), gold (XAU), and the Chinese yuan (CNY).

Weights for the core fiat currencies (EUR, JPY, GBP, CAD, SEK, CHF) follow the official ICE DXY methodology. Additional components are weighted proportionally based on their estimated global economic influence.

The index is normalized from its initial valid data point, meaning it starts at 100 on the first day all asset inputs are available. From that point forward, it tracks the relative strength of the U.S. dollar against this expanded basket.

This provides a more comprehensive and modernized view of the dollar's strength—not only against traditional fiat currencies, but also in the context of rising decentralized assets and non-Western trade power.

HGDA Hany Ghazy Digital Analytics area zone'sIndicator Name: HGDA Hany Ghazy Digital Analytics area zones

Description:

This indicator plots several key price zones based on the highest high and lowest low over a user-defined lookback period.

The plotted zones represent dynamic support and resistance levels calculated using specific ratios of the price range (High - Low), as follows:

- Zone 1 (Light Red): Represents an upper resistance zone.

- Zone 2 (Medium Green): Represents a medium support zone.

- Zone 3 (Dark Red): Represents a lower resistance zone.

- Zone 4 (Dark Green): Represents a strong support zone.

Additionally, the indicator plots a yellow "Zero" line representing the midpoint price of the selected period, serving as a balance point for price action.

This indicator is ideal for identifying the overall market trend, as prices typically move from the upper resistance zones (light red) downwards to the end of the wave in the lower zones (dark green). This helps traders better understand wave nature and direction.

Usage:

- The colored zones assist in identifying potential reversal or continuation areas.

- These zones can be used to plan entries, exits, and risk management.

- Default lookback period is 20 bars, adjustable in the settings to suit the timeframe.

Notes:

- This indicator relies on historical price data and does not guarantee market predictions.

- It is recommended to combine it with other indicators and analytical tools for improved trading decisions.

---

Developed by Hany Ghazy Digital Analytics (HGDA).

Custom USD IndexThis is a modernized, expanded version of the U.S. Dollar Index (DXY), designed to provide a more accurate representation of the dollar’s global strength in today’s diversified economy.

Unlike the traditional DXY, which excludes major players like China and entirely omits real-world stores of value, this custom index (DXY+) includes:

Fiat Currencies (78.3% total weight):

EUR, JPY, GBP, CAD, AUD, CHF, and CNY — equally weighted to reflect the global currency landscape.

Gold (17.5%):

Gold (XAUUSD) is included as a traditional reserve asset and inflation hedge, acknowledging its continued monetary relevance.

Cryptocurrencies (2.8% total weight):

Bitcoin (BTC) and Ethereum (ETH) represent the emerging digital monetary layer.

The index rises when the U.S. dollar strengthens relative to this blended basket, and falls when the dollar weakens against it. This is ideal for traders, economists, and macro analysts seeking a more inclusive and up-to-date measure of dollar performance.

Float, Daily % Change & Short %This TradingView Pine Script displays a compact table on your chart showing four key metrics for any stock:

📊 What It Shows:

Float – Number of publicly available shares, formatted in K/M/B.

Daily % Change – Price change from yesterday’s close to the current price.

Intraday % Change – Price change from today’s open to the current price.

Short Volume % – Estimated short volume as a percentage of total daily volume.

⚙️ How to Use:

Add the script to your TradingView chart.

Choose table size and screen position from the settings panel.

The values update in real-time on the latest candle only, so they stay out of the way but always visible.

Ideal for momentum traders, short float hunters, and day traders who need quick access to real-time float, price action, and short volume stats.

SOFR Spread (proxy: FEDFUNDS - US03MY)📊 SOFR Spread (Proxy: FEDFUNDS - US03MY) – Monitoring USD Money Market Liquidity

In 2008, the spread exhibits a sharp vertical spike, signaling a severe liquidity dislocation: investors rushed into short-term U.S. Treasuries, pushing their yields down dramatically, while the FEDFUNDS rate remained relatively high.

This behavior indicates extreme systemic stress in the interbank lending market, preceding massive Federal Reserve interventions such as rate cuts, emergency liquidity operations, and the launch of quantitative easing (QE).

Description:

This indicator plots the spread between the Effective Federal Funds Rate (FEDFUNDS) and the 3-Month US Treasury Bill yield (US03MY), used here as a proxy for the SOFR spread.

It serves as a simple yet powerful tool to detect liquidity dislocations and stress signals in the US short-term funding markets.

Interpretation:

🔴 Spread > 0.20% → Possible liquidity stress: elevated repo rates, cash shortage, interbank distrust.

🟡 Spread ≈ 0% → Normal market conditions, balanced liquidity.

🟢 Spread < 0% → Excess liquidity: strong demand for T-Bills, “flight to safety”, or distortion due to expansionary monetary policy.

Ideal for:

Monitoring Fed policy impact

Anticipating market-wide liquidity squeezes

Correlation with DXY, SPX, VIX, MOVE Index, and risk sentiment

🧠 Note: As SOFR is not directly available on TradingView, FEDFUNDS is used as a reliable proxy, closely tracking the same trends in most macro conditions.

LANZ Strategy 2.0 [Backtest]🔷 LANZ Strategy 2.0 — Structural Breakout Logic with Dynamic Swing Protection

LANZ Strategy 2.0 is a precision-focused backtesting system built for intraday traders who rely on structural confirmations before the London session to guide directional bias. This tool uses smart swing detection, risk-defined position sizing, and strict time-based execution to simulate real trading conditions with clarity and control.

🧠 Core Components:

Structural Confirmation (Trend & BoS): Detects trend direction and break of structure (BoS) using a three-swing logic, aligning trade entries with valid structural movement.

Time-Based Execution: Trades are triggered exclusively at 02:00 a.m. New York time, ensuring disciplined and repeatable intraday testing.

Swing-Based SL Models: Traders can select between three stop-loss protection types:

First Swing: Most recent structural level

Second Swing: Prior level

Full Coverage: All recent swing levels + configurable pip buffer

Dynamic TP Calculation: Take-Profit is projected as a risk-based multiple (RR), fully adjustable via input.

Capital-Based Risk Management: Risk is defined as a percentage of a fixed account size (e.g., $100 per trade from $10,000), and lot size is automatically calculated based on SL distance.

Fallback Entry Logic: If structural breakout is present but trend is not confirmed, a secondary entry is triggered.

End-of-Session Management: Any open trades are automatically closed at 11:45 a.m. NY time, with optional manual labeling or review.

📊 Visual Features (Optional in Indicator Version):

(Note: Visuals apply to the indicator version of LANZ 2.0, not this backtest script)

Swing level labels (1st, 2nd) and dynamic SL/TP lines.

Real-time session coloring for clarity: Pre-London, Entry Window, and NY Close.

Outcome labels: +RR, -RR, or net % at close.

Auto-cleanup of previous drawings for a clean chart per session.

⚙️ How It Works:

Detects last trend and BoS using swing logic before 02:00 a.m. NY.

At 02:00 a.m., evaluates directional bias and executes BUY or SELL if confirmed.

Applies selected SL logic (1st, 2nd, or full swing protection).

Sets TP based on the RR multiplier.

Closes the trade either on SL, TP, or at 11:45 a.m. NY manually.

🔔 Alerts:

Time-of-day alert at 02:00 a.m. NY to monitor execution.

Can be extended to cover SL/TP triggers or new BoS events.

📝 Notes:

Designed for backtesting precision and discretionary decision-making.

Ideal for Forex pairs, indices, or assets active during the London session.

Fully customizable: session timing, swing logic, SL buffer, and RR.

👤 Credits:

Strategy built by @rau_u_lanz using Pine Script v6, combining structural logic, capital-based risk control, and London-session timing in a backtest-ready framework for traders who demand accuracy and structure.

Statistical Pairs Trading IndicatorZ-Score Stat Trading — Statistical Pairs Trading Indicator

📊🔗

---

What is it?

Z-Score Stat Trading is a powerful indicator for statistical pairs trading and quantitative analysis of two correlated assets.

It calculates the Z-Score of the log-price spread between any two symbols you choose, providing both long-term and short-term Z-Score signals.

You’ll also see real-time correlation, volatility, spread, and the number of long/short signals in a handy on-chart table!

---

How to Use 🛠️

1. Add the indicator to your chart.

2. Select two assets (symbols) to analyze in the settings.

3. Watch the Z-Score plots (blue and orange lines) and threshold levels (+2, -2 by default).

4. Check the info table for:

- Correlation

- Volatility

- Spread

- Number of long (NL) and short (NS) signals in the last 1000 bars

5. Set up alerts for signal generation or threshold crossings if you want to be notified automatically.

---

Trading Strategy 💡

- This indicator is designed for statistical arbitrage (mean reversion) strategies.

- Long Signal (🟢):

When both Z-Scores drop below the negative threshold (e.g., -2), a long signal is generated.

→ Buy Symbol A, Sell Symbol B, expecting the spread to revert to the mean.

- Short Signal (🔴):

When both Z-Scores rise above the positive threshold (e.g., +2), a short signal is generated.

→ Sell Symbol A, Buy Symbol B, again expecting mean reversion.

- The info table helps you quickly assess the frequency of signals and the current statistical relationship between your chosen assets.

---

Best Practices & Warnings 🚦

- Avoid high leverage! Pairs trading can be risky, especially during periods of divergence. Use conservative position sizing.

- Check for cointegration: Before using this indicator, make sure both assets are cointegrated or have a strong historical relationship. This increases the reliability of mean reversion signals.

- Check correlation: Only use asset pairs with a high correlation (preferably 0.8–0.9 or higher) for best results. The correlation value is shown in the info table.

- Scale in and out gradually: When entering or exiting positions, consider doing so in parts rather than all at once. This helps manage slippage and risk, especially in volatile markets.

---

⚠️ Note on Performance:

This indicator may work a bit slowly, especially on large timeframes or long chart histories, because the calculation of NL and NS (number of long/short signals) is computationally intensive.

---

Disclaimer ⚠️

This script is provided for educational and informational purposes only .

It is not financial advice or a recommendation to buy or sell any asset.

Use at your own risk. The author assumes no responsibility for any trading decisions or losses.

Fibo Normalized RSI & RSI RibbonPlots both standard and Z-score normalized RSI ribbons using Fibonacci-based periods. Supports adjustable normalization, optional 0–100 scaling, and multi-line visualizations for momentum and deviation analysis.

This tool is designed for traders who want to go beyond standard RSI by adding:

Statistical normalization (Z-score)

Multi-period analysis (Fibonacci structure)

Advanced divergence and exhaustion detection

It gives you both classical momentum context and mathematically rigorous deviation insight, making it ideal for:

Swing traders

Quant-inclined discretionary traders

Multi-timeframe analysts

Trend Confirmation

When both RSI and normalized RSI across short and long periods are stacked in the same direction (e.g., above 50 or with high Z-scores), the trend is likely strong.

Disagreement between the two ribbons (e.g., RSI high but normalized RSI flat) may indicate late-stage trend or false strength.

Mean Reversion Trades

Look for normalized RSI values > +2 or < -2 (i.e., ~2 standard deviations).

Cross-check with standard RSI to see if the move aligns with a traditional overbought/oversold level.

Great for fade/reversal setups when Z-score RSI is extreme but classic RSI is just beginning to turn.

Divergence Detection

Compare the slope of RSI vs. normalized RSI over same period:

If RSI is rising but normalized RSI is falling → momentum is fading despite apparent strength.

Excellent for early warnings before reversals.

Multi-Timeframe Confluence

Use short-period ribbons (e.g., 3–13) for tactical entries/exits.

Use long-period ribbons (e.g., 55–233) for macro trend bias.

Alignment across both = high-confidence zone.

Risk Calculator PRO — manual lot size + auto lot-suggestionWhy risk management?

90 % of traders blow up because they size positions emotionally. This tool forces Risk-First Thinking: choose the amount you’re willing to lose, and the script reverse-engineers everything else.

Key features

1. Manual or Market Entry – click “Use current price” or type a custom entry.

2. Setup-based ₹-Risk – four presets (A/B/C/D). Edit to your workflow.

3. Lot-Size Input + Auto Lot Suggestion – you tell the contract size ⇒ script tells you how many lots.

4. Auto-SL (optional) – tick to push stop-loss to exactly 1-lot risk.

5. Instant Targets – 1 : 2, 1 : 3, 1 : 4, 1 : 5 plotted and alert-ready.

6. P&L Preview – table shows potential profit at each R-multiple plus real ₹ at SL.

7. Margin Column – enter per-lot margin once; script totals it for any size.

8. Clean Table UI – dark/light friendly; updates every 5 bars.

9. Alert Pack – SL, each target, plus copy-paste journal line on the chart.

How to use

1. Add to chart > “Format”.

2. Type the lot size for the symbol (e.g., 1250 for Natural Gas, 1 for cash equity).

3. Pick Side (Buy / Sell) & Setup grade.

4. ✅ If you want the script to place SL for you, tick Auto-SL (risk = 1 lot).

5. Otherwise type your own Stop-loss.

6. Read the table:

• Suggested lots = how many to trade so risk ≤ setup ₹.

• Risk (currency) = real money lost if SL hits.

7. Set TradingView alerts on the built-in conditions (T1_2, SL_hit, etc.) if you’d like push / email.

8. Copy the orange CSV label to Excel / Sheets for journalling.

Best practices

• Never raise risk to “fit” a trade. Lower size instead.

• Review win-rate vs. R multiple monthly; adjust setups A–D accordingly.

• Test Auto-SL in replay before going live.

Disclaimer

This script is educational. Past performance ≠ future results. The author isn’t responsible for trading losses.

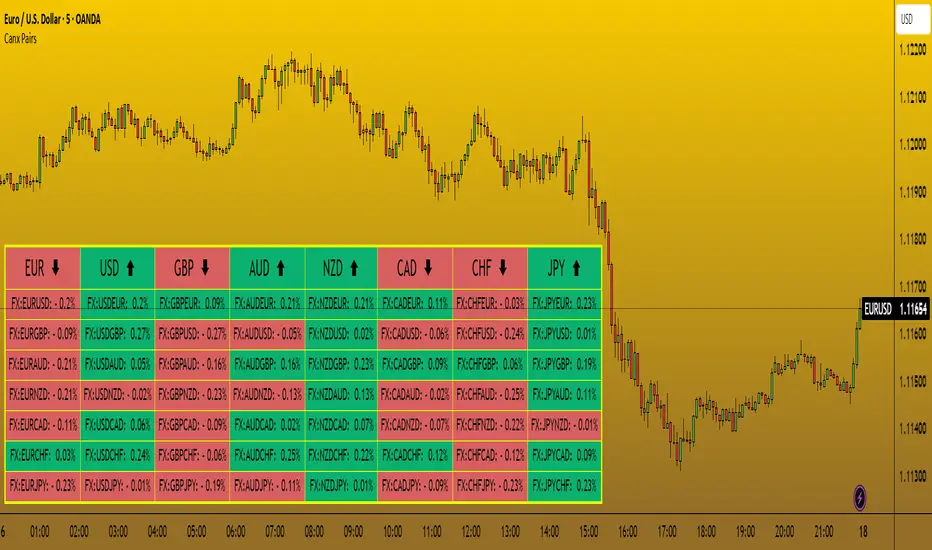

CANX Pairs Table© CanxStixTrader

This Indicator simply shows the change in movement of all the major currency pairs using custom time frames and percentage.

Customize time frame, background, text colors and indicator location to suit.

Keep it simple!

Index Futures vs Cash ArbitrageThis indicator measures the statistical spread between major stock index futures and their corresponding cash indices (e.g., ES vs SPX, NQ vs NDX) using Z-score normalization. It automatically detects commonly traded index pairs (S&P 500, Nasdaq, Dow Jones, Russell 2000) and calculates a smoothed spread between futures and spot prices. A Z-score is then derived from this spread to highlight potential overpricing or underpricing conditions.

Traders can use customizable thresholds to identify mean-reversion opportunities where the futures contract may be temporarily overvalued or undervalued relative to the index. The histogram highlights the direction of the Z-score (green = futures > index, red = futures < index), while built-in alerts notify users of key threshold breaches or zero-line crosses.

This tool is designed for discretionary traders, pairs traders, or anyone exploring statistical arbitrage strategies between futures and spot markets. It is not a buy/sell signal by itself and should be used with additional confluence or risk management techniques.

Seasonality DOW CombinedOverall Purpose

This script analyzes historical daily returns based on two specific criteria:

Month of the year (January through December)

Day of the week (Sunday through Saturday)

It summarizes and visually displays the average historical performance of the selected asset by these criteria over multiple years.

Step-by-Step Breakdown

1. Initial Settings:

Defines minimum year (i_year_start) from which data analysis will start.

Ensures the user is using a daily timeframe, otherwise prompts an error.

Sets basic display preferences like text size and color schemes.

2. Data Collection and Variables:

Initializes matrices to store and aggregate returns data:

month_data_ and month_agg_: store monthly performance.

dow_data_ and dow_agg_: store day-of-week performance.

COUNT tracks total number of occurrences, and COUNT_POSITIVE tracks positive-return occurrences.

3. Return Calculation:

Calculates daily percentage change (chg_pct_) in price:

chg_pct_ = close / close - 1

Ensures it captures this data only for the specified years (year >= i_year_start).

4. Monthly Performance Calculation:

Each daily return is grouped by month:

matrix.set updates total returns per month.

The script tracks:

Monthly cumulative returns

Number of occurrences (how many days recorded per month)

Positive occurrences (days with positive returns)

5. Day-of-Week Performance Calculation:

Similarly, daily returns are also grouped by day-of-the-week (Sunday to Saturday):

Daily return values are summed per weekday.

The script tracks:

Cumulative returns per weekday

Number of occurrences per weekday

Positive occurrences per weekday

6. Visual Display (Tables):

The script creates two visual tables:

Left Table: Monthly Performance.

Right Table: Day-of-the-Week Performance.

For each table, it shows:

Yearly data for each month/day.

Summaries at the bottom:

SUM row: Shows total accumulated returns over all selected years for each month/day.

+ive row: Shows percentage (%) of times the month/day had positive returns, along with a tooltip displaying positive occurrences vs total occurrences.

Cells are color-coded:

Green for positive returns.

Red for negative returns.

Gray for neutral/no change.

7. Interpreting the Tables:

Monthly Table (left side):

Helps identify seasonal patterns (e.g., historically bullish/bearish months).

Day-of-Week Table (right side):

Helps detect recurring weekday patterns (e.g., historically bullish Mondays or bearish Fridays).

Practical Use:

Traders use this to:

Identify patterns based on historical data.

Inform trading strategies, e.g., avoiding historically bearish days/months or leveraging historically bullish periods.

Example Interpretation:

If the table shows consistently green (positive) for March and April, historically the asset tends to perform well during spring. Similarly, if the "Friday" column is often red, historically Fridays are bearish for this asset.

Crypto_in_details_MAlibCrypto_in_details_MaLib — Advanced Moving Average Library for Pine Script

Overview:

Crypto_in_details_MaLib is a comprehensive, performance-optimized Moving Average (MA) library designed specifically for Pine Script v6 users seeking advanced technical analysis tools. Developed by Crypto_in_details, this library consolidates the most popular and sophisticated MA calculation methods — including classical, weighted, exponential, and Hull variants — into one seamless package.

Key Features:

Implements a wide range of Moving Averages: SMA, EMA, WMA, RMA, VWMA, HMA, TEMA, EHMA, THMA.

Designed for precision and flexibility — suitable for diverse trading strategies and indicator development.

Fully typed functions compatible with Pine Script v6 standards.

Simplifies your scripting workflow by providing ready-to-use MA functions via clean and easy-to-import methods.

Well-documented and maintained by an experienced Pine Script developer.

Why Use Crypto_in_details_MaLib?

Gain access to advanced MA calculations that enhance trend analysis, smoothing, and signal accuracy.

Save time on coding complex moving averages from scratch.

Easily extend or combine with your own strategies or indicators for improved performance.

Rely on a tested and community-driven solution backed by a prolific Pine Script author.

Ideal for:

Traders and developers building custom indicators or strategies requiring versatile MA techniques.

Anyone looking to improve their Pine Script efficiency and code maintainability.

Pine Script enthusiasts wanting a professional-grade MA toolkit.