Mutanabby_AI | Ultimate Algo | Remastered+Overview

The Mutanabby_AI Ultimate Algo Remastered+ represents a sophisticated trend-following system that combines Supertrend analysis with multiple moving average confirmations. This comprehensive indicator is designed specifically for identifying high-probability trend continuation and reversal opportunities across various market conditions.

Core Algorithm Components

**Supertrend Foundation**: The primary signal generation relies on a customizable Supertrend indicator with adjustable sensitivity (1-20 range). This adaptive trend-following tool uses Average True Range calculations to establish dynamic support and resistance levels that respond to market volatility.

**SMA Confirmation Matrix**: Multiple Simple Moving Averages (SMA 4, 5, 9, 13) provide layered confirmation for signal strength. The algorithm distinguishes between regular signals and "Strong" signals based on SMA 4 vs SMA 5 relationship, offering traders different conviction levels for position sizing.

**Trend Ribbon Visualization**: SMA 21 and SMA 34 create a visual trend ribbon that changes color based on their relationship. Green ribbon indicates bullish momentum while red signals bearish conditions, providing immediate visual trend context.

**RSI-Based Candle Coloring**: Advanced 61-tier RSI system colors candles with gradient precision from deep red (RSI ≤20) through purple transitions to bright green (RSI ≥79). This visual enhancement helps traders instantly assess momentum strength and overbought/oversold conditions.

Signal Generation Logic

**Buy Signal Criteria**:

- Price crosses above Supertrend line

- Close price must be above SMA 9 (trend confirmation)

- Signal strength determined by SMA 4 vs SMA 5 relationship

- "Strong Buy" when SMA 4 ≥ SMA 5

- Regular "Buy" when SMA 4 < SMA 5

**Sell Signal Criteria**:

- Price crosses below Supertrend line

- Close price must be below SMA 9 (trend confirmation)

- Signal strength based on SMA relationship

- "Strong Sell" when SMA 4 ≤ SMA 5

- Regular "Sell" when SMA 4 > SMA 5

Advanced Risk Management System

**Automated TP/SL Calculation**: The indicator automatically calculates stop loss and take profit levels using ATR-based measurements. Risk percentage and ATR length are fully customizable, allowing traders to adapt to different market conditions and personal risk tolerance.

**Multiple Take Profit Targets**:

- 1:1 Risk-Reward ratio for conservative profit taking

- 2:1 Risk-Reward for balanced trade management

- 3:1 Risk-Reward for maximum profit potential

**Visual Risk Display**: All risk management levels appear as both labels and optional trend lines on the chart. Customizable line styles (solid, dashed, dotted) and positioning ensure clear visualization without chart clutter.

**Dynamic Level Updates**: Risk levels automatically recalculate with each new signal, maintaining current market relevance throughout position lifecycles.

Visual Enhancement Features

**Customizable Display Options**: Toggle trend ribbon, TP/SL levels, and risk lines independently. Decimal precision adjustments (1-8 decimal places) accommodate different instrument price formats and personal preferences.

**Professional Label System**: Clean, informative labels show entry points, stop losses, and take profit targets with precise price levels. Labels automatically position themselves for optimal chart readability.

**Color-Coded Momentum**: The gradient RSI candle coloring system provides instant visual feedback on momentum strength, helping traders assess market energy and potential reversal zones.

Implementation Strategy

**Timeframe Optimization**: The algorithm performs effectively across multiple timeframes, with higher timeframes (4H, Daily) providing more reliable signals for swing trading. Lower timeframes work well for day trading with appropriate risk adjustments.

**Sensitivity Adjustment**: Lower sensitivity values (1-5) generate fewer but higher-quality signals, ideal for conservative approaches. Higher sensitivity (15-20) increases signal frequency for active trading styles.

**Risk Management Integration**: Use the automated risk calculations as baseline parameters, adjusting risk percentage based on account size and market conditions. The 1:1, 2:1, 3:1 targets enable systematic profit-taking strategies.

Market Application

**Trend Following Excellence**: Primary strength lies in capturing significant trend movements through the Supertrend foundation with SMA confirmation. The dual-layer approach reduces false signals common in single-indicator systems.

**Momentum Assessment**: RSI-based candle coloring provides immediate momentum context, helping traders assess signal strength and potential continuation probability.

**Range Detection**: The trend ribbon helps identify ranging conditions when SMA 21 and SMA 34 converge, alerting traders to potential breakout opportunities.

Performance Optimization

**Signal Quality**: The requirement for both Supertrend crossover AND SMA 9 confirmation significantly improves signal reliability compared to basic trend-following approaches.

**Visual Clarity**: The comprehensive visual system enables rapid market assessment without complex calculations, ideal for traders managing multiple instruments.

**Adaptability**: Extensive customization options allow fine-tuning for specific markets, trading styles, and risk preferences while maintaining the core algorithm integrity.

## Non-Repainting Design

**Educational Note**: This indicator uses standard TradingView functions (Supertrend, SMA, RSI) with normal behavior patterns. Real-time updates on current candles are expected and standard across all technical indicators. Historical signals on closed candles remain fixed and unchanged, ensuring reliable backtesting and analysis.

**Signal Confirmation**: Final signals are confirmed only when candles close, following standard technical analysis principles. The algorithm provides clear distinction between developing signals and confirmed entries.

Technical Specifications

**Supertrend Parameters**: Default sensitivity of 4 with ATR length of 11 provides balanced signal generation. Sensitivity range from 1-20 allows adaptation to different market volatilities and trading preferences.

**Moving Average Configuration**: SMA periods of 8, 9, and 13 create multi-layered trend confirmation, while SMA 21 and 34 form the visual trend ribbon for broader market context.

**Risk Management**: ATR-based calculations with customizable risk percentage ensure dynamic adaptation to market volatility while maintaining consistent risk exposure principles.

Recommended Settings

**Conservative Approach**: Sensitivity 4-5, RSI length 14, higher timeframes (4H, Daily) for swing trading with maximum signal reliability.

**Active Trading**: Sensitivity 6-8, RSI length 8-10, intermediate timeframes (1H) for balanced signal frequency and quality.

**Scalping Setup**: Sensitivity 10-15, RSI length 5-8, lower timeframes (15-30min) with enhanced risk management protocols.

## Conclusion

The Mutanabby_AI Ultimate Algo Remastered+ combines proven trend-following principles with modern visual enhancements and comprehensive risk management. The algorithm's strength lies in its multi-layered confirmation approach and automated risk calculations, providing both novice and experienced traders with clear signals and systematic trade management.

Success with this system requires understanding the relationship between signal strength indicators and adapting sensitivity settings to match current market conditions. The comprehensive visual feedback system enables rapid decision-making while the automated risk management ensures consistent trade parameters.

Practice with different sensitivity settings and timeframes to optimize performance for your specific trading style and risk tolerance. The algorithm's systematic approach provides an excellent framework for disciplined trend-following strategies across various market environments.

Volatility

Mutanabby_AI __ OSC+ST+SQZMOMMutanabby_AI OSC+ST+SQZMOM: Multi-Component Trading Analysis Tool

Overview

The Mutanabby_AI OSC+ST+SQZMOM indicator combines three proven technical analysis components into a unified trading system, providing comprehensive market analysis through integrated oscillator signals, trend identification, and volatility assessment.

Core Components

Wave Trend Oscillator (OSC): Identifies overbought and oversold market conditions using exponential moving average calculations. Key threshold levels include overbought zones at 60 and 53, with oversold areas marked at -60 and -53. Crossover signals between the two oscillator lines generate entry opportunities, displayed as colored circles on the chart for easy identification.

Supertrend Indicator (ST): Determines overall market direction using Average True Range calculations with a 2.5 factor and 10-period ATR configuration. Green lines indicate confirmed uptrends while red lines signal downtrend conditions. The indicator automatically adapts to market volatility changes, providing reliable trend identification across different market environments.

Squeeze Momentum (SQZMOM): Compares Bollinger Bands with Keltner Channels to identify consolidation periods and potential breakout scenarios. Black squares indicate squeeze conditions representing low volatility periods, green triangles signal confirmed upward breakouts, and red triangles mark downward breakout confirmations.

Signal Generation Logic

Long Entry Conditions:

Green triangles from Squeeze Momentum component

Supertrend line transitioning to green

Bullish crossovers in Wave Trend Oscillator from oversold territory

Short Entry Conditions:

Red triangles from Squeeze Momentum component

Supertrend line transitioning to red

Bearish crossovers in Wave Trend Oscillator from overbought territory

Automated Risk Management

The indicator incorporates comprehensive risk management through ATR-based calculations. Stop losses are automatically positioned at 3x ATR distance from entry points, while three progressive take profit targets are established at 1x, 2x, and 3x ATR multiples respectively. All risk management levels are clearly displayed on the chart using colored lines and informative labels.

When trend direction changes, the system automatically clears previous risk levels and generates new calculations, ensuring all risk parameters remain current and relevant to existing market conditions.

Alert and Notification System

Comprehensive alert framework includes trend change notifications with complete trade setup details, squeeze release alerts for breakout opportunity identification, and trend weakness warnings for active position management. Alert messages contain specific trading pair information, timeframe specifications, and all relevant entry and exit level data.

Implementation Guidelines

Timeframe Selection: Higher timeframes including 4-hour and daily charts provide the most reliable signals for position trading strategies. One-hour charts demonstrate good performance for day trading applications, while 15-30 minute timeframes enable scalping approaches with enhanced risk management requirements.

Risk Management Integration: Limit individual trade risk to 1-2% of total capital using the automatically calculated stop loss levels for precise position sizing. Implement systematic profit-taking at each target level while adjusting stop loss positions to protect accumulated gains.

Market Volatility Adaptation: The indicator's ATR-based calculations automatically adjust to changing market volatility conditions. During high volatility periods, risk management levels appropriately widen, while low volatility conditions result in tighter risk parameters.

Optimization Techniques

Combine indicator signals with fundamental support and resistance level analysis for enhanced signal validation. Monitor volume patterns to confirm breakout strength, particularly when Squeeze Momentum signals develop. Maintain awareness of scheduled economic events that may influence market behavior independent of technical indicator signals.

The multi-component design provides internal signal confirmation through multiple alignment requirements, significantly reducing false signal occurrence while maintaining reasonable trade frequency for active trading strategies.

Technical Specifications

The Wave Trend Oscillator utilizes customizable channel length (default 10) and average length (default 21) parameters for optimal market sensitivity. Supertrend calculations employ ATR period of 10 with factor multiplier of 2.5 for balanced signal quality. Squeeze Momentum analysis uses Bollinger Band length of 20 periods with 2.0 multiplication factor, combined with Keltner Channel length of 20 periods and 1.5 multiplication factor.

Conclusion

The Mutanabby_AI OSC+ST+SQZMOM indicator provides a systematic approach to technical market analysis through the integration of proven oscillator, trend, and momentum components. Success requires thorough understanding of each element's functionality and disciplined implementation of proper risk management principles.

Practice with demo trading accounts before live implementation to develop familiarity with signal interpretation and trade management procedures. The indicator's systematic approach effectively reduces emotional decision-making while providing clear, objective guidelines for trade entry, management, and exit strategies across various market conditions.

GOLD SCALPER SESSIONS - By The Homerun SeriesThis zones should be used to turn on/off your gold scalper, for access to our gold scalper please dm the author or @_theindiantrader_ on instagram

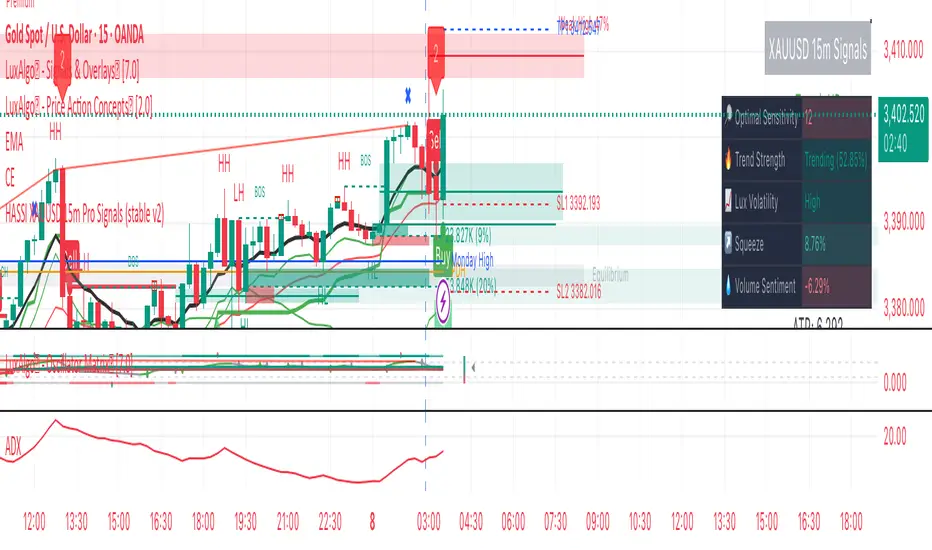

Hassi XAUUSD STRATEGY BOTGold (XAUUSD) 15m trend+momentum based signals with EMA(9/21/200), RSI, custom ADX, ATR-based SL/TP & alerts

Works on XAUUSD 15m.

Entry: EMA9/21 cross + price relative to EMA200 + RSI filter + custom ADX trend strength.

Risk: default SL=1.5×ATR, TP=2×ATR (editable).

Notes: No financial advice. Backtest before live use. Avoid high-impact news whipsaws.

Regime KaleidoscopeWhat is Regime Kaleidoscope?

Regime Kaleidoscope is an advanced market regime visualizer and adaptive signal generator.

It helps traders instantly understand whether current market conditions are best for mean-reversion (fading price back to the mean) or breakout/trend-following (riding strong moves), using a data-driven, non-repainting approach.

How It Works

1. Regime Detection & Background Colors

The indicator analyzes both volatility (ATR) and the shape of each candle (body size vs. range) over a rolling window.

Each bar is classified into one of three regimes, and the chart’s background color changes accordingly:

Regime Background Color What It Means How to Use

Low Vol Balanced Green background Market is calm, compressed. More likely to revert back to mean. Look for mean-reversion signals only (fade moves).

High Vol Directional Red background Market is in a high-volatility, trending, or “breakout” state.

Red does NOT mean bearish. It simply means conditions are ripe for strong directional moves—either up or down. Look for breakout signals only (ride strong moves after structure break).

Chop Gray background Market is indecisive or transitioning between states. Signals are minimized or blocked. Best to wait or trade with extra caution.

→ Red background means high volatility/trending regime, not a signal direction!

Green means “mean-revert environment,” not always bullish!

Gray means “chop/transition”—usually best avoided.

2. Signals — How to Read and Trade Them

Mean-Reversion Signals (Green Regime Only):

Appear when price is stretched away from a rolling mean (SMA) by a configurable ATR-based threshold.

Optional: Only allowed in the direction of the higher-timeframe trend, if enabled.

Long signals: Fade extreme dips (look for triangle-up shapes & green labels).

Short signals: Fade extreme spikes (triangle-down shapes & red labels).

Labels show signal strength (distance from mean in ATR units).

Breakout Signals (Red Regime Only):

Only triggered when price breaks above or below a confirmed swing high or low (pivot), with a strong candle and optional trend confirmation.

Long signals: Breakout above last swing high (regardless of background color).

Short signals: Breakout below last swing low.

Labels show signal strength (distance from pivot in ATR units).

Red background does NOT mean sell— it means “trend environment”—so both long and short signals are possible, depending on which direction price is breaking out.

Signal Controls & Filtering:

Signals only fire at bar close (non-repainting), never intrabar or on future data.

ATR “floor” blocks signals when volatility is too low for meaningful moves.

Cooldown: Signals are limited to one per regime per direction for a minimum number of bars (user input).

Optional confirmation candles: Only strong reversals or breakouts count, reducing noise and whipsaws.

All signals are visible as triangle shapes below/above bars, and labeled with strength.

3. Visual Guide

Background color: Maps the regime, not buy/sell direction.

Transition label: Appears only when the regime changes, so you can see state shifts at a glance.

Triangle shapes & labels: Mark entry points; label gives strength.

Info table (optional): Shows regime and ATR at transitions.

Why is Regime Kaleidoscope Unique?

Uses rolling statistical percentiles of ATR and candle body shape for dynamic market state detection—not just a moving average or volatility band.

Separates regime from signal direction, so you always know “what mode the market is in” and when signals actually have a higher probability.

No repainting. All logic is strictly bar-close, confirmed pivots, and non-future-leaking.

Highly customizable—all thresholds, filters, trend confirmation, and cooldown are user inputs.

How To Use

Add to any chart.

Use the background color to identify if you’re in a mean-revert, breakout, or chop regime.

Take only the signals that match the regime:

Green = fade extremes, Red = ride breakouts, Gray = wait.

Tune settings for your asset and timeframe.

All signals are educational—always test before live use!

Past performance is not necessarily indicative of future results.

Test the indicator on your assets and timeframes. All signals are for educational use only.

Bollinger Heatmap [Quantitative]Overview

The Bollinger Heatmap is a composite indicator that synthesizes data derived from 30 Bollinger bands distributed over multiple time horizons, offering a high-dimensional characterization of the underlying asset.

Algorithm

The algorithm quantifies the current price’s relative position within each Bollinger band ensemble, generating a normalized position ratio. This ratio is subsequently transformed into a scalar heat value, which is then rendered on a continuous color gradient from red to blue. Red hues correspond to price proximity to or extension below the lower band, while blue hues denote price proximity to or extension above the upper band.

Using default parameters, the indicator maps bands over timeframes increasing in a pattern approximating exponential growth, constrained to multiples of seven days. The lower region encodes relationships with shorter-term bands spanning between 1 and 14 weeks, whereas the upper region portrays interactions with longer-term bands ranging from 15 to 52 weeks.

Conclusion

By integrating Bollinger bands across a diverse array of time horizons, the heatmap indicator aims to mitigate the model risk inherent in selecting a single band length, capturing exposure across a richer parameter space.

Squeeze Momentum Regression Clouds [SciQua]╭──────────────────────────────────────────────╮

☁️ Squeeze Momentum Regression Clouds

╰──────────────────────────────────────────────╯

🔍 Overview

The Squeeze Momentum Regression Clouds (SMRC) indicator is a powerful visual tool for identifying price compression , trend strength , and slope momentum using multiple layers of linear regression Clouds. Designed to extend the classic squeeze framework, this indicator captures the behavior of price through dynamic slope detection, percentile-based spread analytics, and an optional UI for trend inspection — across up to four customizable regression Clouds .

────────────────────────────────────────────────────────────

╭────────────────╮

⚙️ Core Features

╰────────────────╯

Up to 4 Regression Clouds – Each Cloud is created from a top and bottom linear regression line over a configurable lookback window.

Slope Detection Engine – Identifies whether each band is rising, falling, or flat based on slope-to-ATR thresholds.

Spread Compression Heatmap – Highlights compressed zones using yellow intensity, derived from historical spread analysis.

Composite Trend Scoring – Aggregates directional signals from each Cloud using your chosen weighting model.

Color-Coded Candles – Optional candle coloring reflects the real-time composite score.

UI Table – A toggleable info table shows slopes, compression levels, percentile ranks, and direction scores for each Cloud.

Gradient Cloud Styling – Apply gradient coloring from Cloud 1 to Cloud 4 for visual slope intensity.

Weight Aggregation Options – Use equal weighting, inverse-length weighting, or max pooling across Clouds to determine composite trend strength.

────────────────────────────────────────────────────────────

╭──────────────────────────────────────────╮

🧪 How to Use the Indicator

1. Understand Trend Bias with Cloud Colors

╰──────────────────────────────────────────╯

Each Cloud changes color based on its current slope:

Green indicates a rising trend.

Red indicates a falling trend.

Gray indicates a flat slope — often seen during chop or transitions.

Cloud 1 typically reflects short-term structure, while Cloud 4 represents long-term directional bias. Watch for multi-Cloud alignment — when all Clouds are green or red, the trend is strong. Divergence among Clouds often signals a potential shift.

────────────────────────────────────────────────────────────

╭───────────────────────────────────────────────╮

2. Use Compression Heat to Anticipate Breakouts

╰───────────────────────────────────────────────╯

The space between each Cloud’s top and bottom regression lines is measured, normalized, and analyzed over time. When this spread tightens relative to its history, the script highlights the band with a yellow compression glow .

This visual cue helps identify squeeze zones before volatility expands. If you see compression paired with a changing slope color (e.g., gray to green), this may indicate an impending breakout.

────────────────────────────────────────────────────────────

╭─────────────────────────────────╮

3. Leverage the Optional Table UI

╰─────────────────────────────────╯

The indicator includes a dynamic, floating table that displays real-time metrics per Cloud. These include:

Slope direction and value , with historical Min/Max reference.

Top and Bottom percentile ranks , showing how price sits within the Cloud range.

Current spread width , compared to its historical norms.

Composite score , which blends trend, slope, and compression for that Cloud.

You can customize the table’s position, theme, transparency, and whether to show a combined summary score in the header.

────────────────────────────────────────────────────────────

╭─────────────────────────────────────────────╮

4. Analyze Candle Color for Composite Signals

╰─────────────────────────────────────────────╯

When enabled, the indicator colors candles based on a weighted composite score. This score factors in:

The signed slope of each Cloud (up, down, or flat)

The percentile pressure from the top and bottom bands

The degree of spread compression

Expect green candles in bullish trend phases, red candles during bearish regimes, and gray candles in mixed or low-conviction zones.

Candle coloring provides a visual shorthand for market conditions , useful for intraday scanning or historical backtesting.

────────────────────────────────────────────────────────────

╭────────────────────────╮

🧰 Configuration Guidance

╰────────────────────────╯

To tailor the indicator to your strategy:

Use Cloud lengths like 21, 34, 55, and 89 for a balanced multi-timeframe view.

Adjust the slope threshold (default 0.05) to control how sensitive the trend coloring is.

Set the spread floor (e.g., 0.15) to tune when compression is detected and visualized.

Choose your weighting style : Inverse Length (favor faster bands), Equal, or Max Pooling (most aggressive).

Set composite weights to emphasize trend slope, percentile bias, or compression—depending on your market edge.

────────────────────────────────────────────────────────────

╭────────────────╮

✅ Best Practices

╰────────────────╯

Use aligned Cloud colors across all bands to confirm trend conviction.

Combine slope direction with compression glow for early breakout entry setups.

In choppy markets, watch for Clouds 1 and 2 turning flat while Clouds 3 and 4 remain directional — a sign of potential trend exhaustion or consolidation.

Keep the table enabled during backtesting to manually evaluate how each Cloud behaved during price turns and consolidations.

────────────────────────────────────────────────────────────

╭───────────────────────╮

📌 License & Usage Terms

╰───────────────────────╯

This script is provided under the Creative Commons Attribution-NonCommercial 4.0 International License .

✅ You are allowed to:

Use this script for personal or educational purposes

Study, learn, and adapt it for your own non-commercial strategies

❌ You are not allowed to:

Resell or redistribute the script without permission

Use it inside any paid product or service

Republish without giving clear attribution to the original author

For commercial licensing , private customization, or collaborations, please contact Joshua Danford directly.

Filtro Antirumore Ottimizzato by G.I.N.e TradingNoise Filter – Adaptive Version for Bund & DAX by G.I.N.e Trading

The Noise Filter is a market condition tool designed to help traders avoid false signals by identifying sideways or low-quality trading phases. This version has been specifically optimized to work effectively with both Bund and DAX price action behaviors.

⚙️ How It Works

The indicator analyzes four key components to determine if the market is in a "noise zone" (sideways, low volatility, or weak trend):

Bollinger Band Width – Detects price compression.

ADX – Measures the strength of the trend.

ATR – Captures recent volatility.

HMA Slope – Evaluates directional movement (trend or no trend).

A noise zone is triggered if at least two out of three core conditions are met:

Narrow Bollinger Bands

ADX below threshold

ATR below threshold

And it is confirmed only if there is no clear directional slope in price.

A strong directional slope overrides the noise signal, allowing valid trends with low volatility (common in instruments like the Bund).

🎯 Visual Output

Gray column → Noise zone: avoid signals in this phase (low quality environment).

Yellow column → Operational zone: conditions are more favorable for trend-following systems.

🛠️ Fully Customizable

You can adjust:

Bollinger Band period & width threshold

ADX length & threshold

ATR period & threshold

HMA slope sensitivity

💡 Best For

Filtering false signals in automated or manual trading strategies

Enhancing trend-following accuracy

Adapting behavior to both high-volatility instruments (DAX) and low-volatility instruments (Bund)

Energy Advanced Policy StrategyThis trading strategy emphasizes both technical trading as well as sentiment trading. Using news and government policy decisions, it can determine either positive or negative sentiment in the energy sector.

How the Strategy Works

This strategy has two main parts that work together to find good trades:

1. The "Policy & Sentiment Engine "

Policy Event Detection : The script spots potential big news or policy changes by looking for big, sudden price moves and huge trading volume. You can play with the Policy Event Volume Threshold and Policy Event Price Threshold (%) settings to make it more or less sensitive.

Sentiment Score : When the script finds a positive or negative event, it adds to a sentiment score. This score isn't forever, though; it fades over time, so the newest events matter the most.

Manual Override : The Manual News Sentiment setting lets you tell the script exactly what the market's mood is for a set time, which is perfect for when you already know about a big upcoming announcement.

The strategy only looks for a trade if the overall feeling is bullish enough. This makes sure you're trading with the big, fundamental forces of the market, not against them.

2. Technical Confirmation & Precision

After the policy and sentiment part gives a green light, the strategy uses a variety of technical indicators to confirm the trend and ideal entry positions.

Long-Term Trend : The script makes sure the market is in a strong uptrend by checking if the fast and medium-speed moving averages are going up, and if the price is above a long-term moving average.

Momentum : The MACD is used to make sure the price's upward momentum is getting stronger, not weaker.

Oscillator : It also uses the RSI to check if the market has gone up too much, too fast, which could mean it's about to turn around.

How to Use the Script

You can customize this strategy to fit your trading style and how much risk you're comfortable with. The inputs are grouped into logical sections for easy adjustment.

News & Policy Analysis : You can play with the Policy Event thresholds to make the script more or less sensitive to market shocks. And you can always use the Manual News Sentiment to take over when you're watching a specific news event.

Technical Analysis : Feel free to change the settings for things like the moving averages, RSI, and MACD to match what you like to trade and on what timeframe.

Multi-Length Quad Bollinger BandsHere is a Pine Script code for TradingView that plots four separate Bollinger Bands on your chart. The lengths are preset to 14, 50, 100, and 200, but every aspect—including lengths, standard deviations, colors, and the source price—is fully customizable through the script's settings menu.

The 14 and 50-period bands are enabled by default, while the 100 and 200-period bands are disabled to keep the chart clean initially. You can easily toggle any of them on or off.

VWAP-RSI Scalper FINAL v1Description

This script implements a robust, battle-tested intraday scalping strategy designed for prop firm challenges, funded trader programs, and serious futures scalpers.

It combines VWAP, RSI, EMA trend, and ATR-based risk management to capture high-probability mean reversion and momentum moves during the most liquid hours of the trading day.

Core Logic

RSI (Relative Strength Index):

Trades are triggered when the RSI is either oversold or overbought using a short lookback (default: 3). This ensures only the strongest intraday reversals or exhaustion moves are considered.

VWAP Filter:

Longs are only taken above VWAP, shorts only below VWAP, aligning trades with the session’s dominant bias.

EMA Filter:

Additional trend quality filter—longs require price above EMA, shorts below EMA.

Session Control:

Only trades between user-defined session hours (default: US cash session), eliminating overnight/illiquid action.

ATR-based Dynamic Stops & Targets:

Every trade uses a stop loss at 1x ATR and a take profit at 2x ATR for a positive risk/reward ratio.

Max Trades Per Day:

Prevents overtrading and controls risk exposure (default: 3).

Performance (Sample Backtest)

Profit Factor: 1.37+ (prop-firm quality)

Drawdown: <1% (very conservative risk)

Win Rate: 37–48% (RR > 1, so high edge)

Consistency: Smooth, steady equity curve over hundreds of trades.

Best For:

ES/NQ/CL/GC intraday traders

Prop firm evaluation challenges (Tradeify, Topstep, Apex, etc.)

Anyone needing robust, no-nonsense systematic edge for futures or indices.

How to Use & Tune

Apply to 3min, 5min, or 15min charts of liquid futures or indices.

Change parameters in the settings panel to suit your asset, volatility, or session hours.

Use “Strategy Tester” to validate P&L, win rate, and drawdown.

How to Optimize

Raise/lower RSI length or bands to make signals more/less frequent.

Adjust stop/target multiples for your preferred risk/reward profile.

Change session hours to match your broker or market.

Disclaimer

This is not financial advice. Use on a demo or sim account first. Results will vary by market, slippage, and execution speed. Past performance does not guarantee future results.

If you find this useful, please give it a like, follow for more strategies, and comment your results or questions!

Good luck and safe trading!

ATR%指標概要 / Overview

ATR Percentage (MTF):把 ATR 轉為百分比(ATR%)或保留為絕對值,並在該「波動序列」上套用布林帶。支援多週期(MTF)計算:例如在 5 分圖顯示 4H / D1 的 ATR%。內建白色點狀水平線作為固定門檻(預設 1%)。

ATR Percentage (MTF): Converts ATR to a percentage of price (ATR%) or keeps it as absolute ATR, then applies Bollinger Bands on this volatility series. Supports multi-timeframe (MTF) calculation (e.g., show 4H/D1 ATR% on a 5-min chart). Includes a configurable white dotted horizontal threshold line (default 1%).

⸻

設計目的 / Purpose

• 以 ATR% 衡量相對波動,利於跨品種比較。

Use ATR% for relative volatility to compare across markets.

• 以 布林帶 標示「高/低波動區」,觀察擴張與壓縮。

Use Bollinger Bands on volatility to highlight expansion/squeeze.

• 提供 固定閾值(1%) 作為策略濾網或告警門檻。

Provide a fixed threshold (1%) for filters/alerts.

• 以 MTF 方式,讓低週期策略用高週期波動做濾網。

MTF lets lower-TF strategies filter by higher-TF volatility.

⸻

參數說明 / Inputs

• Use ATR as % of Close:切換 ATR(絕對值)/ ATR%(建議)。

Toggle between absolute ATR and ATR% (recommended).

• ATR Periods:ATR 計算長度(預設 22)。

ATR lookback (default 22).

• Show Bollinger Bands / BB Periods / StdDev:布林帶開關、長度與倍數(預設 20 / 2)。

Bollinger Bands on/off, length, and deviation (default 20 / 2).

• Source Timeframe:計算用週期(如 60、240、D、W;留空/Chart = 跟隨圖表)。

Timeframe used for calculations (e.g., 60, 240, D, W; empty/“Chart” = current).

• Threshold Line (%):白色點線門檻,預設 1.0(即 1%)。

White dotted threshold line, default 1.0 (1%).

提醒:當 非 ATR% 模式時,Threshold 值代表「價格單位」而非百分比。

Note: In non-ATR% mode, the threshold is in price units, not percent.

⸻

訊號解讀 / How to Read

• ATR% > 上軌:波動顯著擴張(趨勢啟動或加速常見)。

ATR% above upper band: significant expansion; often trend ignition/acceleration.

• ATR% < 下軌:波動明顯壓縮(常見於突破前)。

ATR% below lower band: volatility squeeze; often precedes breakouts.

• ATR% 穿越 Threshold(1%):達到固定波動標準,可作策略開關或風控分水嶺。

ATR% crossing the 1% threshold: fixed volatility bar for filters/risk gates.

⸻

內建告警 / Built-in Alerts

• Volatility Breakout (MTF):ATR/ATR% 向上穿越上軌。

Triggers when ATR/ATR% crosses above the upper band.

• Volatility Squeeze (MTF):ATR/ATR% 向下穿越下軌。

Triggers when ATR/ATR% crosses below the lower band.

⸻

使用建議 / Suggested Uses

• 當沖濾網:於 1–5 分圖選擇 4H / D1 作為 Source Timeframe;僅在 ATR% > 1% 且位於中線以上時允許趨勢進場。

Intraday filter: on 1–5m charts, set 4H/D1 as source TF; allow trend entries only when ATR% > 1% and above the midline.

• 突破前偵測:ATR% 長時間貼近下軌 → 留意可能的波動擴張。

Pre-breakout scan: prolonged ATR% near lower band can foreshadow expansion.

• 跨品種比較:用 ATR% 統一指數、外匯、商品的波動刻度。

Cross-asset comparison: ATR% normalizes volatility across indices/FX/commodities.

⸻

已知限制 / Notes

• MTF 對齊:使用 request.security() 對映高週期資料到當前圖表;在歷史回補與即時邊界棒可能略有差異。

MTF alignment: request.security() maps higher-TF data; boundary bars may differ slightly between historical and realtime.

• 百分比分母:ATR% 的分母為同一週期的 close;若需更平滑可改 ATR / SMA(close, N) × 100。

Denominator: ATR% uses same-TF close; for smoother values consider ATR / SMA(close, N) × 100.

• 風險聲明:僅供研究/教育用途,非投資建議,請自行控管風險。

Disclaimer: For research/education only. Not investment advice.

⸻

版本與更新 / Version & Updates

• v1.0:ATR/ATR% + BB(MTF)、1% 白色點線、兩組告警。

v1.0: ATR/ATR% + BB (MTF), 1% white dotted line, two alert conditions.

Filtro Universale Antirumore by G.I.N.e TradingNoise Filter Indicator by G.I.N.e Trading

The Noise Filter Indicator is designed to detect market conditions where price action is likely to generate false signals due to low volatility or lack of trend. These are typically sideways or congested phases that trend-following systems should avoid.

⚙️ How it works:

The indicator analyzes the current market structure using three components:

Bollinger Band Width

Measures price compression.

Narrow bands indicate a potential sideways phase.

Average Directional Index (ADX)

Measures the strength of the trend.

Low ADX values suggest absence of directional momentum.

Average True Range (ATR)

Measures recent price volatility.

When ATR is below its moving average, the market is likely ranging or losing energy.

A noise zone is identified when at least 2 out of 3 conditions are true:

Low volatility (Bollinger Band Width)

Weak trend (ADX < threshold)

ATR below reference value

🎯 Visual Output:

🟨 Yellow bar: Trend conditions favorable — signals are more reliable.

⬜️ Gray bar: Noise zone — high risk of false signals, avoid trading.

ACR(Average Candle Range) With TargetsWhat is ACR?

The Average Candle Range (ACR) is a custom volatility metric that calculates the mean distance between the high and low of a set number of past candles. ACR focuses only on the actual candle range (high - low) of specific past candles on a chosen timeframe.

This script calculates and visualizes the Average Candle Range (ACR) over a user-defined number of candles on a custom timeframe. It displays a table of recent range values, plots dynamic bullish and bearish target levels, and marks the start of each new candle with a vertical line. All calculations update in real time as price action develops. This script was inspired by the “ICT ADR Levels - Judas x Daily Range Meter°” by toodegrees.

Key Features

Custom Timeframe Selection: Choose any timeframe (e.g., 1D, 4H, 15m) for analysis.

User-Defined Lookback: Calculate the average range across 1 to 10 previous candles.

Dynamic Targets:

Bullish Target: Current candle low + ACR.

Bearish Target: Current candle high – ACR.

Live Updates: Targets adjust intrabar as highs or lows change during the current candle.

Candle Start Markers: Vertical lines denote the open of each new candle on the selected timeframe.

Floating Range Table:

Displays the current ACR value.

Lists individual ranges for the previous five candles.

Extend Target Lines: Choose to extend bullish and bearish target levels fully across the screen.

Global Visibility Controls: Toggle on/off all visual elements (targets, vertical lines, and table) for a cleaner view.

How It Works

At each new candle on the user-selected timeframe, the script:

Draws a vertical line at the candle’s open.

Recalculates the ACR based on the inputted previous number of candles.

Plots target levels using the current candle's developing high and low values.

Limitation

Once the price has already moved a full ACR in the opposite direction from your intended trade, the associated target loses its practical value. For example, if you intended to trade long but the bearish ACR target is hit first, the bullish target is no longer a reliable reference for that session.

Use Case

This tool is designed for traders who:

Want to visualize the average movement range of candles over time.

Use higher or lower timeframe candles as structural anchors.

Require real-time range-based price levels for intraday or swing decision-making.

This script does not generate entry or exit signals. Instead, it supports range awareness and target projection based on historical candle behavior.

Key Difference from Similar Tools

While this script was inspired by “ICT ADR Levels - Judas x Daily Range Meter°” by toodegrees, it introduces a major enhancement: the ability to customize the timeframe used for calculating the range. Most ADR or candle-range tools are locked to a single timeframe (e.g., daily), but this version gives traders full control over the analysis window. This makes it adaptable to a wide range of strategies, including intraday and swing trading, across any market or asset.

EMA 9/21 Crossover Alert (BerryRight)This indicator gives entry signals through EMA crossover and the gives the opportunity to set up alerts. I will update this indicator with exits in the future. it's written in Pinesctipt v5

OPTIONS GREEKS PROFESSIONAL DASHBOARD ANALYZEROPTIONS GREEKS’ PROFESSIONAL DASHBOARD ANALYZER

(Study Material & Script Description)

Overview

The "Professional Options Greeks Analyzer" by aiTrendview.com is a comprehensive analytical tool developed using the Black-Scholes Option Pricing Model. It is designed to help traders, investors, and financial analysts measure and visualize the most important first-order Greeks — Delta, Gamma, Theta, Vega, and Rho — along with key metrics like option pricing, implied volatility (IV), break-even points, moneyness, expected move, and risk level. This dashboard is highly configurable and supports various expiry durations, volatility assumptions, and strike price selection modes, providing a deeply customizable yet intuitive user interface.

________________________________________

Core Logic and Calculation Model

The tool is based on the Black-Scholes model, a well-known pricing method for European-style options. The model computes Call and Put prices using parameters such as current spot price (S), strike price (K), time to expiry (T), implied volatility (σ), and risk-free interest rate (r). The d1 and d2 components — central to Black-Scholes — are derived from logarithmic price ratios and volatility-adjusted time decay.

From these, all major Greeks are calculated:

• Delta: Measures the sensitivity of the option's price to the underlying asset's price.

• Gamma: Indicates the rate of change in Delta relative to changes in the underlying.

• Vega: Captures the sensitivity of the option's price to changes in implied volatility.

• Theta: Reflects the rate at which the option loses value due to time decay.

• Rho: Indicates the sensitivity to interest rate changes.

These values are updated in real time and displayed in a tabular format with visual progress bars to help traders interpret values more effectively.

________________________________________

Customization & User Inputs

The indicator allows users to adjust several key parameters to fit different trading scenarios:

• Implied Volatility (IV) can be manually input (default 25%), allowing traders to model expected outcomes under their assumptions.

• Strike Price Mode offers flexibility with "ATM" (At-the-Money) or "Custom" strike selection.

• Expiry Selection includes 7D, 14D, 30D, 60D, and 90D periods, making the Greeks adaptive to different option durations.

• Risk-Free Rate is configurable (default 4.5%) to reflect current economic conditions.

The tool also computes realized volatility from price action over 30 bars, which is compared with implied volatility to calculate IV Rank, categorized as HIGH, MEDIUM, or LOW. This helps traders decide whether options are relatively expensive or cheap.

________________________________________

Visual Dashboard and Interpretation

The dashboard is structured into five key rows:

1. Market Metrics: Asset name, spot price, selected strike, days to expiry, IV, IV Rank, trend over 1-day period, and moneyness (ITM/ATM/OTM).

2. Option Pricing: Call and Put prices, breakeven levels, time value components, expected move, and realized volatility.

3. Greeks: Displays Delta (with progress bar), Gamma, Vega, Theta (Call and Put), and visual interpretation.

4. Risk & Recommendation: Based on IV Rank and short-term trend, the script generates real-time suggestions (e.g., "BUY STRADDLES", "SELL CALL SPREADS").

5. Visual Encoding: Each data point is color-coded — green for positive, red for negative, and gray for neutral — enhancing visual clarity.

This layout not only provides transparency but also helps both novice and professional traders make quick and informed decisions.

________________________________________

Strategy Suggestions and Interpretation

The script provides a status-based recommendation engine that suggests strategic action based on market conditions:

• High IV & Rising Market: Suggests "SELL CALL SPREADS"

• High IV & Falling Market: Suggests "SELL PUT SPREADS"

• Low IV & Sideways Market: Suggests "BUY STRADDLES"

• Unclear Condition: Suggests "MONITOR"

Additionally, the risk level is determined by the Gamma value, which serves as a proxy for position sensitivity — categorized into HIGH, MEDIUM, or LOW.

________________________________________

Use Case and Trader Benefits

This tool is especially beneficial for:

• Options Traders analyzing multiple Greeks in real-time.

• Volatility Strategists comparing implied and realized volatility.

• Retail Investors evaluating premium pricing and moneyness quickly.

• Portfolio Managers visualizing risk and hedging exposures.

The real-time alert system, progress bars, and recommendation logic make it suitable for both manual trading and integration into automated strategies or alerts via webhook/notifications.

________________________________________

Practical Steps for Use

1. Load the script in TradingView’s Pine Script editor and apply it to your desired chart.

2. Choose your expiry duration and configure IV and strike price based on your trade thesis.

3. Observe the Greeks, pricing, IV Rank, and generated recommendations.

4. Use the dashboard to plan spreads, straddles, directional trades, or hedges accordingly.

5. Optionally, create alerts when IV Rank hits HIGH/LOW or when recommended strategies change.

________________________________________

Disclaimer by aiTrendview

The "Professional Options Greeks Analyzer" and all tools or materials provided by aiTrendview.com are strictly intended for educational and informational purposes only. They are not investment advice, financial recommendations, or trading signals. Options trading involves substantial risk and may not be suitable for all investors. Past performance does not guarantee future returns. Users are solely responsible for their decisions and are advised to test strategies in simulation environments before applying them to live trading. Please consult a certified financial advisor or legal counsel before making any financial decisions.

VRP Zones with Strategy Labels & TooltipsThis script marries the core concept of Volatility Risk Premium—how far implied vol sits above or below realized vol—with practical, on-chart signals that guide you toward specific options trades. By seeing “High VRP” in orange or “Negative VRP” in red right on your price bars (with hover-for-tooltip strategy tips), you get both the quantitative measure and the qualitative trade idea in one glance.

Target in ATR by G.I.N.e TradingTarget in ATR (Bar View)

🧭 Purpose:

This indicator visualizes the target level for a trade as a percentage of the ATR (Average True Range). It is designed to help traders adapt their profit-taking logic to current market volatility.

Features:

ATR-based dynamic target: Automatically adjusts to market volatility

Color-coded bars to visually represent volatility regimes:

🟢 Green → High volatility (Target > ATR) → Ideal for trailing stops

🟠 Orange → Moderate volatility (Target between 0.5×ATR and ATR) → Good for fixed targets

🔴 Red → Low volatility (Target < 0.5×ATR) → Consider avoiding trades

Optional line plot to show current target value as a continuous line

Quantum Range Filter by MRKcoin### Quantum Range Filter by MRKcoin

**Overview**

This indicator is a sophisticated range detection tool designed based on the principles of quantitative multi-factor models. Instead of relying on a single condition, it assesses the market from three different dimensions to provide a more robust and reliable identification of range-bound (sideways) markets.

When the background is highlighted in red, it indicates that the market is likely in a range phase, suggesting that trend-following strategies may be less effective, and mean-reversion (range trading) strategies could be more suitable.

---

**Core Logic: A Multi-Factor Approach**

The filter evaluates the market state using the following three independent factors:

1. **Momentum Volatility (RSI Bollinger Bandwidth):**

* **Question:** Is the momentum of the market contracting?

* **Method:** It measures the width of the Bollinger Bands applied to the RSI. A narrow bandwidth suggests that momentum is consolidating, which is a common characteristic of a range market.

2. **Price Volatility (ATR Ratio):**

* **Question:** Is the actual price movement shrinking?

* **Method:** It calculates the Average True Range (ATR) as a percentage of the closing price. A low ratio indicates that the price volatility itself is low, reinforcing the case for a range environment.

3. **Absence of Trend (ADX):**

* **Question:** Is there a lack of a clear directional trend?

* **Method:** It uses the Average Directional Index (ADX), a standard tool for measuring trend strength. A low ADX value provides active confirmation that the market is not in a trending phase.

---

**How to Use**

1. **Range Detection:** The primary use is to identify ranging markets. The red highlighted background serves as a visual cue.

2. **Strategy Selection:**

* **Inside the Red Zone:** Consider using range-trading strategies (e.g., buying at support, selling at resistance, using oscillators like RSI or Stochastics for overbought/oversold signals). Avoid using trend-following indicators like moving average crossovers, as they are prone to generating false signals in these conditions.

* **Outside the Red Zone:** The market is likely trending. Trend-following strategies are more appropriate.

3. **Parameter Tuning (In Settings):**

* **This is the key to adapting the filter to any market or timeframe.** Different assets (like BTC vs. ETH) and different timeframes have unique volatility characteristics. Don't hesitate to adjust the parameters to fit the specific chart you are analyzing.

* **Range Detection Score:** This is the most important setting. It determines how many of the three factors must agree to classify the market as a range. The default is `2`, which provides a good balance.

* If the filter seems **too sensitive** (highlighting too often), increase the score to `3`.

* If the filter seems **not sensitive enough** (missing obvious ranges), decrease the score to `1`.

* **Factor Thresholds:** For fine-tuning, adjust the thresholds for each factor.

* **`RSI BB Width Threshold`:** If you want to detect even tighter momentum consolidations, *decrease* this value.

* **`ATR Ratio Threshold`:** If you want to be stricter about price volatility, *decrease* this value.

* **`ADX Threshold`:** To be more lenient on what constitutes a "trendless" market, *increase* this value (e.g., to 30). To be stricter, *decrease* it (e.g., to 20).

* **Pro Tip:** Use the Debug Table (uncomment it in the script's code) to see the live values of each factor. This will give you a clear idea of how to set the thresholds for the specific asset you are trading.

**Disclaimer**

This indicator is a tool to assist in market analysis and should not be used as a standalone signal for making financial decisions. Always use it in conjunction with your own trading strategy, risk management, and analysis. Past performance is not indicative of future results.

**Credits**

* **Concept & Vision:** MRKcoin

EMA Channel with ATR Offset + 2 Custom EMAsJust an alternative channel indicator to Bollinger Bands or Ketner channels that uses ATR offsets as the corridor of possible movements, which I recommend changing to fit various tickers.

Also thrown in is EMA, default is 100 and 50 periods for trend direction and potential confirmation

Mutanabby_AI | Fresh Algo V24Mutanabby_AI | Fresh Algo V24: Advanced Multi-Mode Trading System

Overview

The Mutanabby_AI Fresh Algo V24 represents a sophisticated evolution of multi-component trading systems that adapts to various market conditions through advanced operational configurations and enhanced analytical capabilities. This comprehensive indicator provides traders with multiple signal generation approaches, specialized assistant functions, and dynamic risk management tools designed for professional market analysis across diverse trading environments.

Primary Signal Generation Framework

The Fresh Algo V24 operates through two fundamental signal generation approaches that accommodate different market perspectives and trading philosophies. The Trending Signals Mode serves as the primary trend-following mechanism, combining Wave Trend Oscillator analysis with Supertrend directional signals and Squeeze Momentum breakout detection. This mode incorporates ADX filtering that requires values exceeding 20 to ensure sufficient trend strength exists before signal activation, making it particularly effective during sustained directional market movements where momentum persistence creates profitable trading opportunities.

The Contrarian Signals Mode provides an alternative approach targeting reversal opportunities through extreme market condition identification. This mode activates when the Wave Trend Oscillator reaches critical threshold levels, specifically when readings surpass 65 indicating potential bearish reversal conditions or drop below 35 suggesting bullish reversal opportunities. This methodology proves valuable during overextended market phases where mean reversion becomes statistically probable.

Advanced Filtering Mechanisms

The system incorporates multiple sophisticated filtering mechanisms designed to enhance signal quality and reduce false positive occurrences. The High Volume Filter requires volume expansion confirmation before signal activation, utilizing exponential moving average calculations to ensure institutional participation accompanies price movements. This filter substantially improves signal reliability by eliminating low-conviction breakouts that lack adequate volume support from professional market participants.

The Strong Filter provides additional trend confirmation through 200-period exponential moving average analysis. Long position signals require price action above this benchmark level, while short position signals necessitate price action below it. This ensures strategic alignment with longer-term trend direction and reduces the probability of trading against major market movements that could invalidate shorter-term signals.

Cloud Filter Configuration System

The Fresh Algo V24 offers four distinct cloud filter configurations, each optimized for specific trading timeframes and market approaches. The Smooth Cloud Filter utilizes the mathematical relationship between 150-period and 250-period exponential moving averages, providing stable trend identification suitable for position trading strategies. This configuration generates signals exclusively when price action aligns with cloud direction, creating a more deliberate but highly reliable signal generation process.

The Swing Cloud Filter employs modified Supertrend calculations with parameters specifically optimized for swing trading timeframes. This filter achieves optimal balance between responsiveness and stability, adapting effectively to medium-term price movements while filtering excessive market noise that typically affects shorter-term analytical systems.

For active intraday traders, the Scalping Cloud Filter utilizes accelerated Supertrend calculations designed to capture rapid trend changes effectively. This configuration provides enhanced signal generation frequency suitable for compressed timeframe strategies. The advanced Scalping+ Cloud Filter incorporates Hull Moving Average confirmation, delivering maximum responsiveness for ultra-short-term trading while maintaining signal quality through additional momentum validation processes.

Specialized Assistant Functionality

The system includes two distinct assistant modes that provide supplementary market analysis capabilities. The Trend Assistant Mode activates advanced cloud analysis overlays that display dynamic support and resistance zones calculated through adaptive volatility algorithms. These levels automatically adjust to current market conditions, providing visual guidance for identifying trend continuation patterns and potential reversal areas with mathematical precision.

The Trend Tracker Mode concentrates on long-term trend identification by displaying major exponential moving averages with color-coded fill areas that clarify directional bias. This mode maintains visual simplicity while providing comprehensive trend context evaluation, enabling traders to quickly assess broader market direction and align shorter-term strategies accordingly.

Dynamic Risk Management System

The integrated risk management system automatically adapts across all operational modes, calculating stop loss and take profit targets using Average True Range multiples that adjust to current market volatility. This approach ensures consistent risk parameters regardless of selected operational mode while maintaining relevance to prevailing market conditions.

Stop loss placement occurs at dynamically calculated distances from entry points, while three progressive take profit targets establish at customizable ATR multiples respectively. The system automatically updates these levels upon trend direction changes, ensuring current market volatility influences all risk calculations and maintains appropriate risk-reward ratios throughout trade management.

Comprehensive Market Analysis Dashboard

The sophisticated dashboard provides real-time market analysis including volatility measurements, institutional activity assessment, and multi-timeframe trend evaluation across five-minute through four-hour periods. This comprehensive market context assists traders in selecting appropriate operational modes based on current market characteristics rather than relying exclusively on historical performance data.

The multi-timeframe analysis ensures mode selection considers broader market context beyond the primary trading timeframe, improving overall strategic alignment and reducing conflicts between different temporal market perspectives. The dashboard displays market state classification, volatility percentages, institutional activity levels, current trading session information, and trend pressure indicators with professional formatting and clear visual hierarchy.

Enhanced Trading Assistants

The Fresh Algo V24 includes specialized trading assistant features that complement the primary signal generation system. The Reversal Dot functionality identifies potential reversal points through Wave Trend Oscillator analysis, displaying visual indicators when crossover conditions occur at extreme levels. These reversal indicators provide early warning signals for potential trend changes before they appear in the primary signal system.

The Dynamic Take Profit Labels feature automatically identifies optimal profit-taking opportunities through RSI threshold analysis, marking potential exit points at multiple levels for long positions and corresponding levels for short positions. This automated profit management system helps traders optimize exit timing without requiring constant manual monitoring of technical indicators.

Advanced Alert System

The comprehensive alert system accommodates all operational modes while providing granular notification control for various signal types and risk management events. Traders can configure separate alerts for normal buy signals, strong buy signals, normal sell signals, strong sell signals, stop loss triggers, and individual take profit target achievements.

Cloud crossover alerts notify traders when trend direction changes occur, providing early indication of potential strategy adjustments. The alert system includes detailed trade setup information, timeframe data, and relevant entry and exit levels, ensuring traders receive complete context for informed decision-making without requiring constant chart monitoring.

Technical Foundation Architecture

The Fresh Algo V24 combines multiple proven technical analysis components including Wave Trend Oscillator for momentum assessment, Supertrend for directional bias determination, Squeeze Momentum for volatility analysis, and various exponential moving averages for trend confirmation. Each component contributes specific market insights while the unified system provides comprehensive market evaluation through their mathematical integration.

The multi-component approach reduces dependency on individual indicator limitations while leveraging the analytical strengths of each technical tool. This creates a robust analytical framework capable of adapting to diverse market conditions through appropriate mode selection and parameter optimization, ensuring consistent performance across varying market environments.

Market State Classification

The indicator incorporates advanced market state classification through ADX analysis, distinguishing between trending, ranging, and transitional market conditions. This classification system automatically adjusts signal sensitivity and filtering parameters based on current market characteristics, optimizing performance for prevailing conditions rather than applying static analytical approaches.

The volatility measurement system calculates current market activity levels as percentages, providing quantitative assessment of market energy and helping traders select appropriate operational modes. Institutional activity detection through volume analysis ensures signal generation aligns with professional market participation patterns.

Implementation Strategy Considerations

Successful implementation requires careful matching of operational modes to prevailing market conditions and individual trading objectives. Trending modes demonstrate optimal performance during directional markets with sustained momentum characteristics, while contrarian modes excel during range-bound or overextended market conditions where reversal probability increases.

The cloud filter configurations provide varying degrees of confirmation strength, with smoother settings reducing false signal occurrence at the expense of some responsiveness to price changes. Traders must balance signal quality against signal frequency based on their risk tolerance and available trading time, utilizing the comprehensive customization options to optimize performance for their specific requirements.

Multi-Timeframe Integration

The system provides seamless multi-timeframe analysis through the integrated dashboard, displaying trend alignment across multiple time horizons from five-minute through four-hour periods. This analysis helps traders understand broader market context and avoid conflicts between different temporal perspectives that could compromise trade outcomes.

Session analysis identifies current trading session characteristics, providing context for expected market behavior patterns and helping traders adjust their approach based on typical session volatility and participation levels. This geographic market awareness enhances strategic decision-making and improves timing for trade execution.

Advanced Visualization Features

The indicator includes sophisticated visualization capabilities through gradient candle coloring based on MACD analysis, providing immediate visual feedback on momentum strength and direction. This enhancement allows rapid market assessment without requiring detailed indicator analysis, improving efficiency for traders managing multiple instruments simultaneously.

The cloud visualization system uses color-coded fill areas to clearly indicate trend direction and strength, with automatic adaptation to selected operational modes. This visual clarity reduces analytical complexity while maintaining comprehensive market information display through professional chart presentation.

Performance Optimization Framework

The Fresh Algo V24 incorporates performance optimization features including signal strength classification, automatic parameter adjustment based on market conditions, and dynamic filtering that adapts to current volatility levels. These optimizations ensure consistent performance across varying market environments while maintaining signal quality standards.

The system automatically adjusts sensitivity levels based on selected operational modes, ensuring appropriate responsiveness for different trading approaches. This adaptive framework reduces the need for manual parameter adjustments while maintaining optimal performance characteristics for each operational configuration.

Conclusion

The Mutanabby_AI Fresh Algo V24 represents a comprehensive solution for professional trading analysis, combining multiple analytical approaches with advanced visualization and risk management capabilities. The system's strength lies in its adaptive multi-mode design and sophisticated filtering mechanisms, providing traders with versatile tools for various market conditions and trading styles.

Success with this system requires understanding the relationship between different operational modes and their optimal application scenarios. The comprehensive dashboard and alert system provide essential market context and trade management support, enabling systematic approach to market analysis while maintaining flexibility for individual trading preferences.

The indicator's sophisticated architecture and extensive customization options make it suitable for traders at all experience levels, from those seeking systematic signal generation to advanced practitioners requiring comprehensive market analysis tools. The multi-timeframe integration and adaptive filtering ensure consistent performance across diverse market conditions while providing clear guidelines for strategic implementation.

Average VolatilityThis script offers a unique and practical approach to visualizing average volatility by calculating a simple moving average of the daily high-low ranges, directly reflecting price fluctuations over a user-defined period. Unlike standard volatility indicators, it provides customizable options such as adjustable period length, display of absolute and percentage volatility values, and flexible text formatting for clear and tailored insights. This makes it a valuable tool for traders seeking to better understand market volatility trends and manage risk more effectively. Its straightforward visualization supports informed decision-making across various instruments and timeframes.

The indicator displays the average volatility over a configurable period as a bar chart (originally designed for daily intervals). It visualizes the price range (difference between high and low) across a selectable number of periods, as well as its ratio to the closing price, offering various customization options.

For many traders, assets with daily moves of 1% or more may offer greater profit opportunities, especially for short-term trading strategies. Instruments with lower volatility are generally less favored and often not recommended in such approaches due to reduced trading potential. Please note that higher volatility also implies increased risk, and potential losses can be significant. Always use proper risk management.

Detailed description:

The script calculates average volatility as a simple moving average of the high-low ranges (default: 5 periods, intended for daily timeframes). Volatility can be shown as either a bar or line chart. Users can choose to display the absolute volatility values and/or the volatility expressed as a percentage of the closing price. Text size and spacing between labels are adjustable to ensure readability across different instruments. Additionally, the last (unconfirmed) bar can be shown or hidden, since its value depends on the current price. Overall, the script provides a flexible and clear visualization of an instrument’s volatility.

---

Russian:

Индикатор отображает среднюю волатильность как простое скользящее среднее диапазонов «максимум-минимум» (по умолчанию 5 периодов, предназначено для дневных таймфреймов). Волатильность может отображаться в виде столбчатой или линейной диаграммы. Пользователи могут выбрать отображение абсолютных значений волатильности и/или волатильности, выраженной в процентах от цены закрытия. Размер текста и расстояния между надписями регулируются для удобочитаемости на разных инструментах. Кроме того, последний (неподтверждённый) столбец можно показать или скрыть, так как его значение зависит от текущей цены. В общем, скрипт обеспечивает гибкое и наглядное отображение волатильности инструмента.

Активы с волатильностью от 1% и выше дают больше возможностей для краткосрочной торговли, но риск также выше. Инструменты с низкой волатильностью не рекомендуются для таких подходов из-за ограниченного торгового потенциала и сложности в реализации прибыльных сделок. Всегда применяйте риск-менеджмент.

---

Spanish:

El script calcula la volatilidad promedio como un promedio móvil simple de las diferencias entre máximos y mínimos (por defecto 5 periodos, pensado para intervalos diarios). La volatilidad puede mostrarse como gráfico de barras o de líneas. El usuario puede elegir mostrar los valores absolutos de la volatilidad y/o los valores expresados en porcentaje respecto al precio de cierre. El tamaño del texto y el espacio entre las etiquetas son ajustables para garantizar la legibilidad en diferentes instrumentos. Además, se puede mostrar u ocultar la última barra (no confirmada), ya que su valor depende del precio actual. En conjunto, el script proporciona una visualización flexible y clara de la volatilidad del instrumento.

Los activos con una volatilidad del 1% o más ofrecen mayores oportunidades para el trading a corto plazo, pero también conllevan un mayor riesgo. Los instrumentos con baja volatilidad no se recomiendan para este tipo de estrategias debido a su limitado potencial de trading y la dificultad para obtener ganancias. Siempre utilice una gestión de riesgos adecuada.