Linear % ST | QuantEdgeB🚀 Introducing Linear Percentile SuperTrend (Linear % ST) by QuantEdgeB

🛠️ Overview

Linear % SuperTrend (Linear % ST) by QuantEdgeB is a hybrid trend-following indicator that combines Linear Regression, Percentile Filters, and Volatility-Based SuperTrend Logic into one dynamic tool. This system is designed to identify trend shifts early while filtering out noise during choppy market conditions.

By utilizing percentile-based median smoothing and customized ATR multipliers, this tool captures both breakout momentum and pullback opportunities with precision.

✨ Key Features

🔹 Percentile-Based Median Filtering

Removes outliers and normalizes price movement for cleaner trend detection using the 50th percentile (median) of recent price action.

🔹 Linear Regression Smoothing

A smoothed baseline is computed with Linear Regression to detect the underlying trend while minimizing lag.

🔹 SuperTrend Structure with Adaptive Bands

The indicator implements an enhanced SuperTrend engine with custom ATR bands that adapt to trend direction. Bands tighten or loosen based on volatility and trend strength.

🔹 Dynamic Long/Short Conditions

Long and short signals are derived from the relationship between price and the SuperTrend threshold zones, clearly showing trend direction with optional "Long"/"Short" labels on the chart.

🔹 Multiple Visual Themes

Select from 6 built-in color palettes including Strategy, Solar, Warm, Cool, Classic, and Magic to match your personal style or strategy layout.

📊 How It Works

1️⃣ Percentile Filtering

The source price (default: close) is filtered using a nearest-rank 50th percentile over a custom lookback. This normalizes data to reflect the central tendency and removes noisy extremes.

2️⃣ Linear Regression Trend Base

A Linear Regression Moving Average (LSMA) is applied to the filtered median, forming the core trend line. This dynamic trendline provides a low-lag yet smooth view of market direction.

3️⃣ SuperTrend Engine

ATR is applied with custom multipliers (different for long and short) to create dynamic bands. The bands react to price movement and only shift direction after confirmation, preventing false flips.

4️⃣ Trend Signal Logic

• When price stays above the dynamic lower band → Bullish trend

• When price breaks below the upper band → Bearish trend

• Trend direction remains stable until violated by price.

⚙️ Custom Settings

• Percentile Length → Lookback for percentile smoothing (default: 35)

• LSMA Length → Determines the base trend via linear regression (default: 24)

• ATR Length → ATR period used in dynamic bands (default: 14)

• Long Multiplier → ATR multiplier for bullish thresholds (default: 0.8)

• Short Multiplier → ATR multiplier for bearish thresholds (default: 1.9)

✅ How to Use

1️⃣ Trend-Following Strategy

✔️ Go Long when price breaks above the lower ATR band, initiating an upward trend

✔️ Go Short when price falls below the upper ATR band, confirming bearish conditions

✔️ Remain in trend direction until the SuperTrend flips

2️⃣ Visual Confirmation

✔️ Use bar coloring and the dynamic bands to stay aligned with trend direction

✔️ Optional Long/Short labels highlight key signal flips

👥 Who Should Use Linear % ST?

✅ Swing & Position Traders → To ride trends confidently

✅ Trend Followers → As a primary directional filter

✅ Breakout Traders → For clean signal generation post-range break

✅ Quant/Systematic Traders → Integrate clean trend logic into algorithmic setups

📌 Conclusion

Linear % ST by QuantEdgeB blends percentile smoothing with linear regression and volatility bands to deliver a powerful, adaptive trend-following engine. Whether you're a discretionary trader seeking cleaner entries or a systems-based trader building logic for automation, Linear % ST offers clarity, adaptability, and precision in trend detection.

🔹 Key Takeaways:

1️⃣ Percentile + Regression = Noise-Reduced Core Trend

2️⃣ ATR-Based SuperTrend = Reliable Breakout Confirmation

3️⃣ Flexible Parameters + Color Modes = Custom Fit for Any Strategy

📈 Use it to spot emerging trends, filter false signals, and stay confidently aligned with market momentum.

📌 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

📌 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Volatility

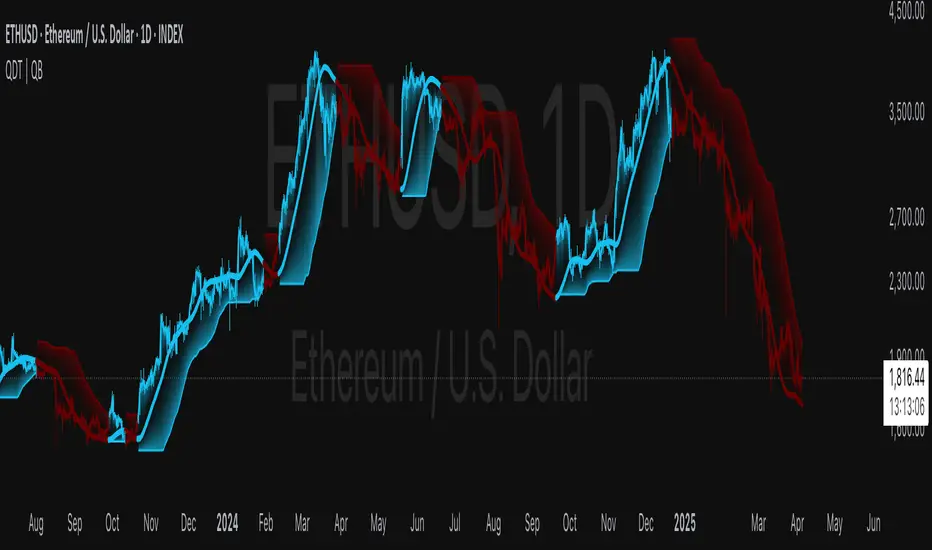

Quantile DEMA Trend | QuantEdgeB🚀 Introducing Quantile DEMA Trend (QDT) by QuantEdgeB

🛠️ Overview

Quantile DEMA Trend (QDT) is an advanced trend-following and momentum detection indicator designed to capture price trends with superior accuracy. Combining DEMA (Double Exponential Moving Average) with SuperTrend and Quantile Filtering, QDT identifies strong trends while maintaining the ability to adapt to various market conditions.

Unlike traditional trend indicators, QDT uses percentile filtering to adjust for volatility and provides dynamic thresholds, ensuring consistent signal performance across different assets and timeframes.

✨ Key Features

🔹 Trend Following with Adaptive Sensitivity

The DEMA component ensures quicker responses to price changes while reducing lag, offering a real-time reflection of market momentum.

🔹 Volatility-Adjusted Filtering

The SuperTrend logic incorporates quantile percentile filters and ATR (Average True Range) multipliers, allowing QDT to adapt to fluctuating market volatility.

🔹 Clear Signal Generation

QDT generates clear Long and Short signals using percentile thresholds, effectively identifying trend changes and market reversals.

🔹 Customizable Visual & Signal Settings

With multiple color modes and customizable settings, you can easily align the QDT indicator with your trading strategy, whether you're focused on trend-following or volatility adjustments.

📊 How It Works

1️⃣ DEMA Calculation

DEMA is used to reduce lag compared to traditional moving averages. It is calculated by applying a Double Exponential Moving Average to price data. This smoother trend-following mechanism ensures responsiveness to market movements without introducing excessive noise.

2️⃣ SuperTrend with Percentile Filtering

The SuperTrend component adapts the trend-following signal by incorporating quantile percentile filters. It identifies dynamic support and resistance levels based on historical price data:

• Upper Band: Calculated using the 75th percentile + ATR (adjusted with multiplier)

• Lower Band: Calculated using the 25th percentile - ATR (adjusted with multiplier)

These dynamic bands adjust to market conditions, filtering out noise while identifying the true direction.

3️⃣ Signal Generation

• Long Signal: Triggered when price crosses below the SuperTrend Lower Band

• Short Signal: Triggered when price crosses above the SuperTrend Upper Band

The indicator provides signals with corresponding trend direction based on these crossovers.

👁 Visual & Custom Features

• 🎨 Multiple Color Modes: Choose from "Strategy", "Solar", "Warm", "Cool", "Classic", and "Magic" color palettes to match your charting style.

• 🏷️ Long/Short Signal Labels: Optional labels for visual cueing when a long or short trend is triggered.

• 📉 Bar Color Customization: Bar colors dynamically adjust based on trend direction to visually distinguish the market bias.

👥 Who Should Use QDT?

✅ Trend Followers: Use QDT as a dynamic tool to confirm trends and capture profits in trending markets.

✅ Swing Traders: Use QDT to time entries based on confirmed breakouts or breakdowns.

✅ Volatility Traders: Identify market exhaustion or expansion points, especially during volatile periods.

✅ Systematic & Quant Traders: Integrate QDT into algorithmic strategies to enhance market detection with adaptive filtering.

⚙️ Customization & Default Settings

- DEMA Length(30): Controls the lookback period for DEMA calculation

- Percentile Length(10): Sets the lookback period for percentile filtering

- ATR Length(14): Defines the length for calculating ATR (used in SuperTrend)

- ATR Multiplier(1.2 ): Multiplier for ATR in SuperTrend calculation

- SuperTrend Length(30):Defines the length for SuperTrend calculations

📌 How to Use QDT in Trading

1️⃣ Trend-Following Strategy

✔ Enter Long positions when QDT signals a bullish breakout (price crosses below the SuperTrend lower band).

✔ Enter Short positions when QDT signals a bearish breakdown (price crosses above the SuperTrend upper band).

✔ Hold positions as long as QDT continues to provide the same direction.

2️⃣ Reversal Strategy

✔ Take profits when price reaches extreme levels (upper or lower percentile zones) that may indicate trend exhaustion or reversion.

3️⃣ Volatility-Driven Entries

✔ Use the percentile filtering to enter positions based on mean-reversion logic or breakout setups in volatile markets.

🧠 Why It Works

QDT combines the DEMA’s quick response to price changes with SuperTrend's volatility-adjusted thresholds, ensuring a responsive and adaptive indicator. The use of percentile filters and ATR multipliers helps adjust to varying market conditions, making QDT suitable for both trending and range-bound environments.

🔹 Conclusion

The Quantile DEMA Trend (QDT) by QuantEdgeB is a powerful, adaptive trend-following and momentum detection system. By integrating DEMA, SuperTrend, and quantile percentile filtering, it provides accurate and timely signals while adjusting to market volatility. Whether you are a trend follower or volatility trader, QDT offers a robust solution to identify high-probability entry and exit points.

🔹 Key Takeaways:

1️⃣ Trend Confirmation – Uses DEMA and SuperTrend for dynamic trend detection

2️⃣ Volatility Filtering – Adjusts to varying market conditions using percentile logic

3️⃣ Clear Signal Generation – Easy-to-read signals and visual cues for strategy implementation

📌 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

📌 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Z-Score Normalized Volatility IndicesVolatility is one of the most important measures in financial markets, reflecting the extent of variation in asset prices over time. It is commonly viewed as a risk indicator, with higher volatility signifying greater uncertainty and potential for price swings, which can affect investment decisions. Understanding volatility and its dynamics is crucial for risk management and forecasting in both traditional and alternative asset classes.

Z-Score Normalization in Volatility Analysis

The Z-score is a statistical tool that quantifies how many standard deviations a given data point is from the mean of the dataset. It is calculated as:

Z = \frac{X - \mu}{\sigma}

Where X is the value of the data point, \mu is the mean of the dataset, and \sigma is the standard deviation of the dataset. In the context of volatility indices, the Z-score allows for the normalization of these values, enabling their comparison regardless of the original scale. This is particularly useful when analyzing volatility across multiple assets or asset classes.

This script utilizes the Z-score to normalize various volatility indices:

1. VIX (CBOE Volatility Index): A widely used indicator that measures the implied volatility of S&P 500 options. It is considered a barometer of market fear and uncertainty (Whaley, 2000).

2. VIX3M: Represents the 3-month implied volatility of the S&P 500 options, providing insight into medium-term volatility expectations.

3. VIX9D: The implied volatility for a 9-day S&P 500 options contract, which reflects short-term volatility expectations.

4. VVIX: The volatility of the VIX itself, which measures the uncertainty in the expectations of future volatility.

5. VXN: The Nasdaq-100 volatility index, representing implied volatility in the Nasdaq-100 options.

6. RVX: The Russell 2000 volatility index, tracking the implied volatility of options on the Russell 2000 Index.

7. VXD: Volatility for the Dow Jones Industrial Average.

8. MOVE: The implied volatility index for U.S. Treasury bonds, offering insight into expectations for interest rate volatility.

9. BVIX: Volatility of Bitcoin options, a useful indicator for understanding the risk in the cryptocurrency market.

10. GVZ: Volatility index for gold futures, reflecting the risk perception of gold prices.

11. OVX: Measures implied volatility for crude oil futures.

Volatility Clustering and Z-Score

The concept of volatility clustering—where high volatility tends to be followed by more high volatility—is well documented in financial literature. This phenomenon is fundamental in volatility modeling and highlights the persistence of periods of heightened market uncertainty (Bollerslev, 1986).

Moreover, studies by Andersen et al. (2012) explore how implied volatility indices, like the VIX, serve as predictors for future realized volatility, underlining the relationship between expected volatility and actual market behavior. The Z-score normalization process helps in making volatility data comparable across different asset classes, enabling more effective decision-making in volatility-based strategies.

Applications in Trading and Risk Management

By using Z-score normalization, traders can more easily assess deviations from the mean in volatility, helping to identify periods when volatility is unusually high or low. This can be used to adjust risk exposure or to implement volatility-based trading strategies, such as mean reversion strategies. Research suggests that volatility mean-reversion is a reliable pattern that can be exploited for profit (Christensen & Prabhala, 1998).

References:

• Andersen, T. G., Bollerslev, T., Diebold, F. X., & Vega, C. (2012). Realized volatility and correlation dynamics: A long-run approach. Journal of Financial Economics, 104(3), 385-406.

• Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

• Christensen, B. J., & Prabhala, N. R. (1998). The relation between implied and realized volatility. Journal of Financial Economics, 50(2), 125-150.

• Whaley, R. E. (2000). Derivatives on market volatility and the VIX index. Journal of Derivatives, 8(1), 71-84.

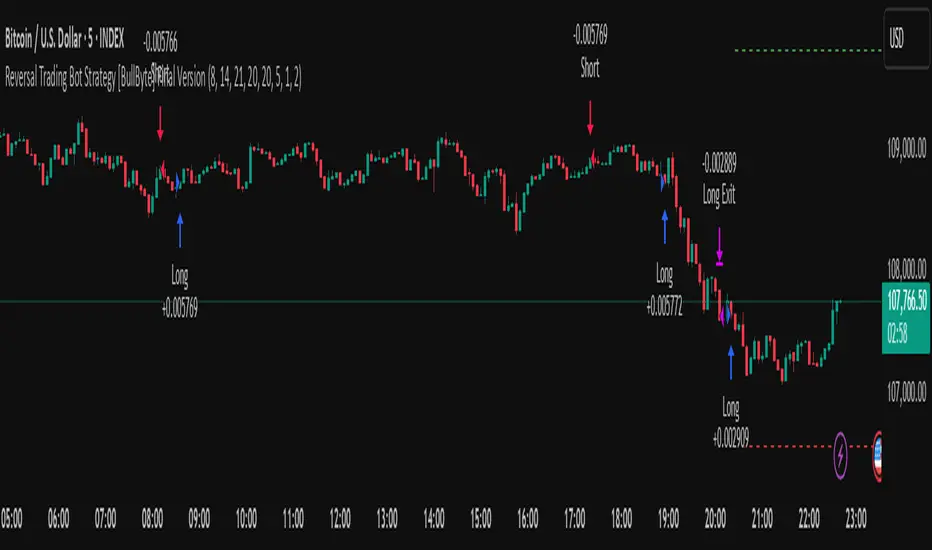

Reversal Trading Bot Strategy[BullByte]Overview :

The indicator Reversal Trading Bot Strategy is crafted to capture potential market reversal points by combining momentum, volatility, and trend alignment filters. It uses a blend of technical indicators to identify both bullish and bearish reversal setups, ensuring that multiple market conditions are met before entering a trade.

Core Components :

Technical Indicators Used :

RSI (Relative Strength Index) :

Purpose : Detects divergence conditions by comparing recent lows/highs in price with the RSI.

Parameter : Length of 8.

Bollinger Bands (BB) :

Purpose : Measures volatility and identifies price levels that are statistically extreme.

Parameter : Length of 20 and a 2-standard deviation multiplier.

ADX (Average Directional Index) & DMI (Directional Movement Index) :

Purpose : Quantifies the strength of the trend. The ADX threshold is set at 20, and additional filters check for the alignment of the directional indicators (DI+ and DI–).

ATR (Average True Range) :

Purpose : Provides a volatility measure used to set stop levels and determine risk through trailing stops.

Volume SMA (Simple Moving Average of Volume ):

Purpose : Helps confirm strength by comparing the current volume against a 20-period average, with an optional filter to ensure volume is at least twice the SMA.

User-Defined Toggle Filters :

Volume Filter : Confirms that the volume is above average (or twice the SMA) before taking trades.

ADX Trend Alignment Filter : Checks that the ADX’s directional indicators support the trade direction.

BB Close Confirmation : Optionally refines the entry by requiring price to be beyond the upper or lower Bollinger Band rather than just above or below.

RSI Divergence Exit : Allows the script to close positions if RSI divergence is detected.

BB Mean Reversion Exit : Closes positions if the price reverts to the Bollinger Bands’ middle line.

Risk/Reward Filter : Ensures that the potential reward is at least twice the risk by comparing the distance to the Bollinger Band with the ATR.

Candle Movement Filter : Optional filter to require a minimum percentage move in the candle to confirm momentum.

ADX Trend Exit : Closes positions if the ADX falls below the threshold and the directional indicators reverse.

Entry Conditions :

Bullish Entry :

RSI Divergence : Checks if the current close is lower than a previous low while the RSI is above the previous low, suggesting bullish divergence.

Bollinger Confirmation : Requires that the price is above the lower (or upper if confirmation is toggled) Bollinger Band.

Volume & Trend Filters : Combines volume condition, ADX strength, and an optional candle momentum condition.

Risk/Reward Check : Validates that the trade meets a favorable risk-to-reward ratio.

Bearish Entry :

Uses a mirror logic of the bullish entry by checking for bearish divergence, ensuring the price is below the appropriate Bollinger level, and confirming volume, trend strength, candle pattern, and risk/reward criteria.

Trade Execution and Exit Strateg y:

Trade Execution :

Upon meeting the entry conditions, the strategy initiates a long or short position.

Stop Loss & Trailing Stops :

A stop-loss is dynamically set using the ATR value, and trailing stops are implemented as a percentage of the close price.

Exit Conditions :

Additional exit filters can trigger early closures based on RSI divergence, mean reversion (via the middle Bollinger Band), or a weakening trend as signaled by ADX falling below its threshold.

This multi-layered exit strategy is designed to lock in gains or minimize losses if the market begins to reverse unexpectedly.

How the Strategy Works in Different Market Conditions :

Trending Markets :

The ADX filter ensures that trades are only taken when the trend is strong. When the market is trending, the directional movement indicators help confirm the momentum, making the reversal signal more reliable.

Ranging Markets :

In choppy markets, the Bollinger Bands expand and contract, while the RSI divergence can highlight potential turning points. The optional filters can be adjusted to avoid false signals in low-volume or low-volatility conditions.

Volatility Management :

With ATR-based stop-losses and a risk/reward filter, the strategy adapts to current market volatility, ensuring that risk is managed consistently.

Recommendation on using this Strategy with a Trading Bot :

This strategy is well-suited for high-frequency trading (HFT) due to its ability to quickly identify reversal setups and execute trades dynamically with automated stop-loss and trailing exits. By integrating this script with a TradingView webhook-based bot or an API-driven execution system, traders can automate trade entries and exits in real-time, reducing manual execution delays and capitalizing on fast market movements.

Disclaimer :

This script is provided for educational and informational purposes only. It is not intended as investment advice. Trading involves significant risk, and you should always conduct your own research and analysis before making any trading decisions. The author is not responsible for any losses incurred while using this script.

Chonky ATR Levels 2.0Show ATR based high/low projections.

Choose a custom ATR calculation in the indicator's settings.

The default is a 20day RMA based ATR.

----------How projections are calculated----------

To project the ATR High, the ATR value is added to the low of the current candle that matches the ATR's timeframe.

To project the ATR Low, the ATR value is subtracted from the high of the current candle that matches the ATR's timeframe.

Example:

If a 20day RMA ATR is used:

- the ATR High will be the current day's low + the ATR value.

- the ATR Low will be the current day's high - the ATR value.

*However*, if the price action exceeds either ATR projection, the opposite ATR level will be fixed to the extreme of the period.

See the AUDUSD screenshot above for an example.

The ATR Low was exceeded, so the ATR High projection is capped at the high of day.

If the ATR High is exceeded, the ATR Low would be capped at the low of day.

Rachas ATR AssistHey Traders!

This indicator is a simple, it uses Average True Range (ATR) data from the daily chart and the current timeframe to estimate potential range and volatility.

This indicator compares the daily ATR to the current daily wick range (from low to high), helping you gauge how much "room" might be left for price movement within the day. Alongside that, it shows the ATR over the last 14 candles and 5 candles on your current chart for intraday volatility awareness—ideal for setting stops, targets, or position sizing.

Gauge Daily Potential Movement:

The "Day Range Difference" cell shows how much of the expected daily range (based on ATR) is still unfilled. If the market has moved less than the average, there's still potential for expansion. If it's close to or above the ATR, expect a slowdown or reversal.

Position Sizing & Stop Losses:

Use the 14-period ATR and 5-period ATR on your current timeframe to understand recent volatility. This helps in choosing logical stop loss levels and adjusting position sizes based on market conditions.

Volatility Awareness:

Knowing the average daily range and how much of it has been used lets you avoid entering trades too late in the move or placing stops in overly tight spots.

Table Position & Font:

You can adjust the table location (top/bottom left/right) and font size to best fit your chart layout.

Smart Dynamic Levels [ATR-Based]Smart Dynamic Levels

Automated Support & Resistance Levels Based on Market Volatility

Overview:

This advanced indicator automatically plots dynamic support and resistance levels based on the Average True Range (ATR), creating meaningful price zones that adapt to changing market conditions. Unlike static round-number levels, these volatility-adjusted zones provide more relevant technical reference points.

Key Features:

Volatility-Responsive: Levels automatically adjust based on the asset's ATR

Smart Visualization:

Color gradient shows strength of each level (darker = stronger)

Bullish (green) levels below price, bearish (red) levels above

Customizable Settings:

Adjust ATR length (14-period default)

Modify level sensitivity with ATR multiplier (1.5x default)

Choose number of levels to display (5 above/below default)

Toggle labels and line extensions

How It Works:

Calculates the asset's true volatility using ATR

Rounds to significant price intervals based on current volatility

Plots equidistant levels above and below current price

Colors levels based on their position relative to price

Automatically updates as market conditions change

Recommended Use:

Day Trading: Identify intraday support/resistance zones

Swing Trading: Spot potential reversal areas

Breakout Trading: Watch for moves beyond key levels

Works on all markets: Stocks, Forex, Crypto, Futures

Settings Guide:

ATR Length: Higher values for smoother levels (14-20)

Multiplier: Increase for wider levels (1.5-3x)

Levels Count: More levels for higher timeframes (3-10)

Pro Tips:

Combine with trend analysis - levels are more significant when aligned with trend

Watch for price reactions at these levels for confirmation

Use wider levels (higher multiplier) for volatile assets

Rolling ATR Momentum

Rolling ATR Momentum Indicator – User Manual

---

🔍 Overview

The Rolling ATR Momentum Indicator is a simple yet powerful tool designed to detect shifts in market volatility. It compares the current Average True Range (ATR) with the ATR from a previous point in time to measure how market volatility is changing.

This indicator is especially useful for:

- Spotting the beginning or fading of a momentum phase

- Filtering out low-volatility market conditions

- Enhancing timing for entries and exits in trending or breakout trades

---

📊 Key Components

✅ ATR Delta (Rolling)

- Definition: `ATR Delta = Current ATR - Past ATR`

- Inputs:

- ATR Period (default: 14): The base ATR calculation window

- Lookback Period (default: 5): How many bars ago to compare ATR

- Interpretation:

- Positive ATR Delta (Green Line): Market volatility is increasing

- Negative ATR Delta (Red Line): Market volatility is decreasing

📈 Zero Line

- A horizontal baseline at zero helps you easily see when ATR momentum shifts from negative to positive (or vice versa).

🟩/🟥 Background Color

- Green Background: ATR Delta is positive (rising volatility)

- Red Background: ATR Delta is negative (falling volatility)

🔵 Optional: ATR Reference Lines

- You can optionally display raw Current ATR and Past ATR by changing their visibility settings.

---

✅ How to Use It

Entry Timing (Futures/Options)

- Use ATR Delta as a filter:

- Only take trades when ATR Delta is positive → confirms momentum is building

- Avoid trades when ATR Delta is negative → market might be slow, sideways, or losing steam

Breakout Anticipation

- A rising ATR Delta after a tight range or consolidation can suggest that a breakout is underway

Stop-loss Strategy

- Use high ATR periods for wider stops (to avoid noise)

- Use low ATR periods for tighter stops or skip trading

---

🧠 Pro Tips

- This indicator doesn’t predict direction—combine with trend or price structure tools (like EMA, PPMA, candlesticks)

- Works best in trending or breakout environments

- Add it to multi-timeframe layouts to see volatility buildup on higher timeframes

---

⚙️ Settings

| Parameter | Description |

|----------|-------------|

| ATR Period | Length of the ATR calculation (default 14) |

| Lookback Period | How many bars back to compare ATR values |

---

🧭 Best For:

- Index futures (Nifty, BankNifty)

- Option buyers needing volatility confirmation

- Intraday & swing traders looking to trade momentum setups

---

Use the Rolling ATR Momentum indicator as your volatility radar—simple, clean, and highly effective for staying on the right side of market energy.

End of Manual

Rolling ATR Momentum - EnhancedATR Rolling Momentum Indicator – User Manual

---

🔍 Overview

The ATR Rolling Momentum Indicator is a dynamic volatility tool built on the Average True Range (ATR). It not only tracks increasing or decreasing momentum but also provides early warnings and confirmation signals for potential breakout moves. It’s especially powerful for futures and options traders looking to align with expanding price action.

---

📊 Core Components

✅ ATR Delta (Rolling ATR)

- Definition: Difference between current ATR and past ATR (user-defined lookback).

- Use: Tells whether volatility is expanding (positive delta) or contracting (negative delta).

- Visual: Green line for rising momentum, red for declining.

🟣 ATR Delta Slope

- Definition: Measures acceleration in momentum.

- Use: Helps identify early signs of breakout buildup.

- Visual: Purple line. Watch for slope turning up from below.

🟡 Volatility Squeeze (Yellow Dot)

- Definition: Current ATR is significantly lower than its 20-period average.

- Use: Indicates the market is coiling—possible breakout ahead.

🔼 Momentum Start (Green Triangle)

- Definition: ATR Delta slope turns from negative to positive.

- Use: Early warning to prepare for volatility expansion.

🔷 Breakout Confirmation (Blue Label Up)

- Definition: ATR Delta exceeds its high of the last 10 candles.

- Use: Confirms volatility breakout—trade opportunity if direction aligns.

🟩/🟥 Background Color

- Green Background: Momentum rising (positive ATR delta)

- Red Background: Momentum falling (negative ATR delta)

- Yellow Tint: Active squeeze zone

---

✅ How to Use It (Futures/Options Focus)

Step-by-Step:

1. Squeeze Detected (Yellow Dot) → Stay alert. Market is coiling.

2. Green Triangle Appears → Momentum is starting to rise.

3. Background Turns Green → Confirmed rising momentum.

4. Blue Label Appears → Confirmed breakout (enter trade if trend aligns).

Directional Bias:

- Use your main chart setup (price action, EMAs, trendlines, etc.) to decide direction (Call or Put, Long or Short).

- ATR Momentum only tells you how strong the move is—not which way.

---

⚙️ Inputs & Settings

- ATR Period: Default 14 (core volatility measure)

- Rolling Lookback: Used to calculate delta (default 5)

- Slope Length: Used to measure acceleration (default 3)

- Squeeze Factor: Default 0.8 — lower = more sensitive squeeze detection

- Breakout Lookback: Checks ATR delta against last X bars (default 10)

---

🧠 Pro Tips

- Works great when paired with EMA stacks, price structure, or breakout patterns.

- Avoid taking trades based only on squeeze or momentum—combine with chart confirmation.

- If background turns red after a breakout, it may be losing momentum—book partials or tighten stops.

---

🧭 Ideal For:

- Nifty/BankNifty Futures

- Option directional trades (call/put buying)

- Index scalping and momentum swing setups

---

Use this tool as your volatility compass—it won't tell you where to go, but it'll tell you when the wind is strong enough to move fast.

End of Manual

Smart Mean Reversion DashboardThis indicator is designed to help traders identify potential mean reversion opportunities using a combination of Bollinger Bands, RSI, and deviation from the moving average. It provides a clean, visually appealing dashboard that displays key metrics and signals in real-time.

How to Read and Use:

Deviation from Mean:

Displays the percentage deviation of the current price from the moving average.

A high positive or negative deviation may indicate overextension and a potential mean reversion opportunity.

Bollinger Band Status:

Indicates whether the price is inside or outside the Bollinger Bands.

"Outside Upper" suggests overbought conditions, while "Outside Lower" suggests oversold conditions.

RSI Status:

Shows whether the RSI is in overbought (>70), oversold (<30), or neutral conditions.

Overbought and oversold levels can confirm potential reversal zones.

Signal:

BUY: Triggered when the price is outside the lower Bollinger Band and RSI is in the oversold zone.

SELL: Triggered when the price is outside the upper Bollinger Band and RSI is in the overbought zone.

WAIT: No clear signal; wait for better conditions.

Important Notes:

This is NOT a buy or sell recommendation. This indicator is a tool to assist in identifying potential trading opportunities. Always use it in conjunction with your own analysis and risk management.

The signals generated by this indicator are based on historical data and do not guarantee future performance.

It is recommended to use this indicator alongside other technical analysis tools and confirm signals with price action or other strategies.

Features:

Dashboard: Displays deviation, Bollinger Band status, RSI status, and signals in a clean, movable interface.

Customizable Settings: Adjust Bollinger Band length, RSI length, and moving average length to suit your trading style.

Visual Enhancements: Color-coded signals and metrics for easy interpretation in both light and dark modes.

Disclaimer:

Trading involves significant risk, and past performance is not indicative of future results. This indicator is for educational purposes only and should not be considered financial advice. Always consult with a financial advisor before making trading decisions.

CME Price LimitCalculates the CME Price Limit

The reference price is obtained from the previous day's closing settlement price

(data pulled from the asset's daily chart with settlement enabled)

Percentage limit can be modified in settings

Buffer can be enabled (for example, 2% buffer on a 7% limit, so a line gets drawn at 5% too)

Alert can be enabled for price crossing a certain percentage from reference on the day

You can choose to plot the historical lines on every day, or the current day only

The reference price output can be found in the data window, or in the indicator status line if enabled in the settings.

Before placing real trades with this, you should compare the indicator's reference price to what's shown on CME's website, to double check that TradingView's data matches for your contract.

www.cmegroup.com

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :

- The script first calculates the ATR-based grid levels and ensures price action has sufficient volatility before allowing trades.

- An additional RSI filter is used to ensure trades are taken at ideal market conditions.

- Once a trade is executed, the script implements a trailing stop and predefined take profit to maximize gains while reducing risks.

---

Disclaimer :

Risk Warning :

This strategy is provided for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Users are advised to conduct their own due diligence and risk management before using this strategy in live trading.

The developer and publisher of this script are not responsible for any financial losses incurred by the use of this strategy. Market conditions, slippage, and execution quality can affect real-world trading outcomes.

Use this script at your own discretion and always trade responsibly.

TTM Squeeze Momentum MTF [Cometreon]TTM Squeeze Momentum MTF combines the core logic of both the Squeeze Momentum by LazyBear and the TTM Squeeze by John Carter into a single, unified indicator. It offers a complete system to analyze the phase, direction, and strength of market movements.

Unlike the original versions, this indicator allows you to choose how to calculate the trend, select from 15 different types of moving averages, customize every parameter, and adapt the visual style to your trading preferences.

If you are looking for a powerful, flexible and highly configurable tool, this is the perfect choice for you.

🔷 New Features and Improvements

🟩 Unified System: Trend Detection + Visual Style

You can decide which logic to use for the trend via the "Show TTM Squeeze Trend" input:

✅ Enabled → Trend calculated using TTM Squeeze

❌ Disabled → Trend based on Squeeze Momentum

You can also customize the visual style of the indicator:

✅ Enable "Show Histogram" for a visual mode using Histogram, Area, or Column

❌ Disable it to display the classic LazyBear-style line

Everything updates automatically and dynamically based on your selection.

🟩 Full Customization

Every base parameter of the original indicator is now fully configurable: lengths, sources, moving average types, and more.

You can finally adapt the squeeze logic to your strategy — not the other way around.

🟩 Multi-MA Engine

Choose from 15 different Moving Averages for each part of the calculation:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

🟩 Dynamic Signal Line

Apply a moving average to the momentum for real-time cross signals, with full control over its length and type.

🟩 Multi-Timeframe & Multi-Ticker Support

You're no longer limited to the chart's current timeframe or ticker. Apply the squeeze to any symbol or timeframe without repainting.

🔷 Technical Details and Customizable Inputs

This indicator offers a fully modular structure with configurable parameters for every component:

1️⃣ Squeeze Momentum Settings – Choose the source, length, and type of moving average used to calculate the base momentum.

2️⃣ Trend Mode Selector – Toggle "Show TTM Squeeze Trend" to select the trend logic displayed on the chart:

✅ Enabled – Shows the trend based on TTM Squeeze (Bollinger Bands inside/outside Keltner Channel)

❌ Disabled – Displays the trend based on Squeeze Momentum logic

🔁 The moving average type for the Keltner Channel is handled automatically, so you don't need to select it manually, even if the custom input is disabled.

3️⃣ Signal Line – Toggle the Signal Line on the Squeeze Momentum. Select its length and MA type to generate visual cross signals.

4️⃣ Bollinger Bands – Configure the length, multiplier, source, and MA type used in the bands.

5️⃣ Keltner Channel – Adjust the length, multiplier, source, and MA type. You can also enable or disable the True Range option.

6️⃣ Advanced MA Parameters – Customize the parameters for advanced MAs (JMA, ALMA, FRAMA, VIDYA), including Phase, Power, Offset, Sigma, and Shift values.

7️⃣ Ticker & Input Source – Select the ticker and manage inputs for alternative chart types like Renko, Kagi, Line Break, and Point & Figure.

8️⃣ Style Settings – Choose how the squeeze is displayed:

Enable "Show Histogram" for Histogram, Area, or Column style

Disable it to show the classic LazyBear-style line

Use Reverse Color to invert line colors

Toggle Show Label to highlight Signal Line cross signals

Customize trend colors to suit your preferences

9️⃣ Multi-Timeframe Options - Timeframe – Use the squeeze on higher timeframes for stronger confirmation

🔟 Wait for Timeframe Closes -

✅ Enabled – Prevents multiple signals within the same candle

❌ Disabled – Displays the indicator smoothly without delay

🔧 Default Settings Reference

To replicate the default settings of the original indicators as they appear when first applied to the chart, use the following configurations:

🟩 TTM Squeeze (John Carter Style)

Squeeze

Length: 20

MA Type: SMA

Show TTM Squeeze Trend: Enabled

Bollinger Bands

Length: 20

Multiplier: 2.0

MA Type: SMA

Keltner Channel

Length: 20

Multiplier: 1.0

Use True Range: ON

MA Type: EMA

Style

Show Histogram: Enabled

Reverse Color: Enabled

🟩 Squeeze Momentum (LazyBear Style)

Squeeze

Length: 10

MA Type: SMA

Show TTM Squeeze Trend: Disabled

Bollinger Bands

Length: 20

Multiplier: 1.5

MA Type: SMA

Keltner Channel

Length: 10

Multiplier: 1.5

Use True Range: ON

MA Type: SMA

Style

Show Histogram: Disabled

Reverse Color: Disabled

⚠️ These values are intended as a starting point. The Cometreon indicator lets you fully customize every input to fit your trading style.

🔷 How to Use Squeeze Momentum Pro

🔍 Identifying Trends

Squeeze Momentum Pro supports two different methods for identifying the trend visually, each based on a distinct logic:

Squeeze Momentum Trend (LazyBear-style):

Displays 3 states based on the position of the Bollinger Bands relative to the Keltner Channel:

🔵 Blue = No Squeeze (BB outside KC and KC outside BB)

⚪️ White = Squeeze Active (BB fully inside KC)

⚫️ Gray = Neutral state (none of the above)

TTM Squeeze Trend (John Carter-style):

Calculates the difference in width between the Bollinger Bands and the Keltner Channel:

🟩 Green = BB width is greater than KC → potential expansion phase

🟥 Red = BB are tighter than KC → possible compression or pre-breakout

📈 Interpreting Signals

Depending on the active configuration, the indicator can provide various signals, including:

Trend color → Reflects the current compression/expansion state (based on selected mode)

Momentum value (above or below 0) → May indicate directional pressure

Signal Line cross → Can highlight momentum shifts

Color change in the momentum → May suggest a potential trend reversal

🛠 Integration with Other Tools

Squeeze Momentum Pro works well alongside other indicators to strengthen market context:

✅ Volume Profile / OBV – Helps confirm accumulation or distribution during squeezes

✅ RSI – Useful to detect divergence between momentum and price

✅ Moving Averages – Ideal for defining primary trend direction and filtering signals

☄️ If you find this indicator useful, leave a Boost to support its development!

Every piece of feedback helps improve the tool and deliver an even better trading experience.

🔥 Share your ideas or feature requests in the comments!

EMA Price Range by tuanduongEMA Price Range Indicator – Dynamic Range Analysis with Custom EMA (tuanduong2511)

Overview

The EMA Price Range Indicator is designed to help traders visualize the distance between price action and a key Exponential Moving Average (EMA). This indicator dynamically calculates the range from each candle to a user-defined EMA and displays it in a real-time table. By understanding the relationship between price and the EMA, traders can better gauge potential support, resistance, and overextension in the market.

Key Features

✅ Customizable EMA – Allows users to choose the EMA period that best suits their strategy (default: 144).

✅ Real-Time Range Calculation – Computes the absolute difference between the EMA and the price (using the high or low, depending on whether the candle is above or below the EMA).

✅ Minimalist UI – The EMA is plotted directly on the chart, while a small table in the bottom-right corner provides numerical insights, reducing chart clutter.

✅ Versatile Use Cases – Suitable for trend-following traders (identifying pullbacks to EMA) and mean-reversion traders (spotting extended price movements).

How It Works

User-Defined EMA:

The script calculates an Exponential Moving Average (EMA) based on the selected period.

EMA adapts dynamically, giving more weight to recent price movements.

Range Calculation:

If the price is above the EMA, the range is measured from the high point of the candle to the EMA.

If the price is below the EMA, the range is measured from the low point of the candle to the EMA.

This approach ensures that we’re measuring the most relevant distance for price interaction.

Live Table Display:

The current EMA value and the distance (range) from the price are displayed in a small table in the bottom-right corner of the chart.

How to Use It

📌 Trend Traders: Use the indicator to track pullbacks to key EMAs (e.g., EMA 50, 144, or 200). When the price is far from the EMA, it may indicate an overextended trend or potential retracement zone.

📌 Mean Reversion Traders: Look for extreme deviations between price and the EMA. Large distances can signal potential price snapbacks to the mean.

📌 Scalping & Day Trading: Short-term traders can use it with fast EMAs (e.g., EMA 21 or 34) to measure quick price movements relative to short-term momentum.

Why This Indicator?

Unlike traditional EMA indicators, which only plot a moving average, this script provides quantifiable price distance to the EMA, helping traders make data-driven decisions. It allows traders to answer:

✅ Is the price stretched too far from the EMA?

✅ Should I wait for a pullback before entering?

✅ Is the trend strong, or is the price losing momentum?

By integrating EMA-based range analysis, traders gain a clearer understanding of market conditions and can improve their entry, exit, and risk management strategies.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

Body Percentage of Range (Colored)Short Description:

This indicator measures the dominance of the candle's body relative to its total range (High - Low), providing a visual gauge of intra-candle strength versus indecision. Columns are colored based on whether the body constitutes more or less than a defined percentage (default 50%) of the candle's total height.

Detailed Description:

What it Does:

The "Body Percentage of Range" indicator calculates, for each candle, what percentage of the total price range (High minus Low) is occupied by the candle's body (absolute difference between Open and Close).

A value of 100% means the candle has no wicks (a Marubozu), indicating strong conviction during that period.

A value of 0% means the candle has no body (a Doji), indicating perfect indecision.

Values in between show the relative balance between the directional move (body) and the price exploration/rejection (wicks).

How to Interpret:

The indicator plots this percentage as columns:

Column Height: Represents the percentage of the body relative to the total range. Higher columns indicate a larger body dominance.

Column Color:

Green Columns: Appear when the body percentage is above the user-defined threshold (default 50%). This suggests that the directional move within the candle was stronger than the indecision (wicks). Often seen during trending moves or strong momentum candles.

Red Columns: Appear when the body percentage is at or below the user-defined threshold (default 50%). This suggests that wicks dominate the candle (body is 50% or less of the range), indicating significant indecision, struggle between buyers and sellers, or potential reversals. These are common in choppy, consolidating, or reversal market conditions.

Orange Line (Optional MA): A Simple Moving Average (SMA) of the body percentages is plotted to help smooth the readings and identify broader periods where candle structure indicates more trending (high MA) vs. ranging/indecisive (low MA) characteristics.

Potential Use Cases:

Identifying Choppy vs. Trending Markets: Sustained periods of low, predominantly red columns (and often a low/declining MA) can signal a choppy, range-bound market where trend-following strategies might underperform. Conversely, periods with frequent high, green columns suggest a more trending environment.

Confirming Breakouts/Momentum: High green columns appearing alongside increased volume during a breakout can add conviction to the move's strength.

Spotting Potential Exhaustion/Reversals: A very tall green column after a strong trend, followed immediately by a low red column (like a Doji or Spinning Top pattern appearing on the price chart), might signal potential exhaustion or a pending reversal, indicating indecision has suddenly entered the market.

Filtering Entries: Traders might avoid taking entries (especially trend-following ones) when the indicator shows a consistent pattern of low red columns, suggesting high market indecision.

Settings:

Color Threshold %: Allows you to set the percentage level above which columns turn green (default is 50%).

Smoothing MA Length: Adjusts the lookback period for the Simple Moving Average.

Disclaimer:

This indicator is a tool for technical analysis and should be used in conjunction with other methods (like price action, volume analysis, other indicators) and robust risk management. It does not provide direct buy/sell signals and past performance is not indicative of future results.

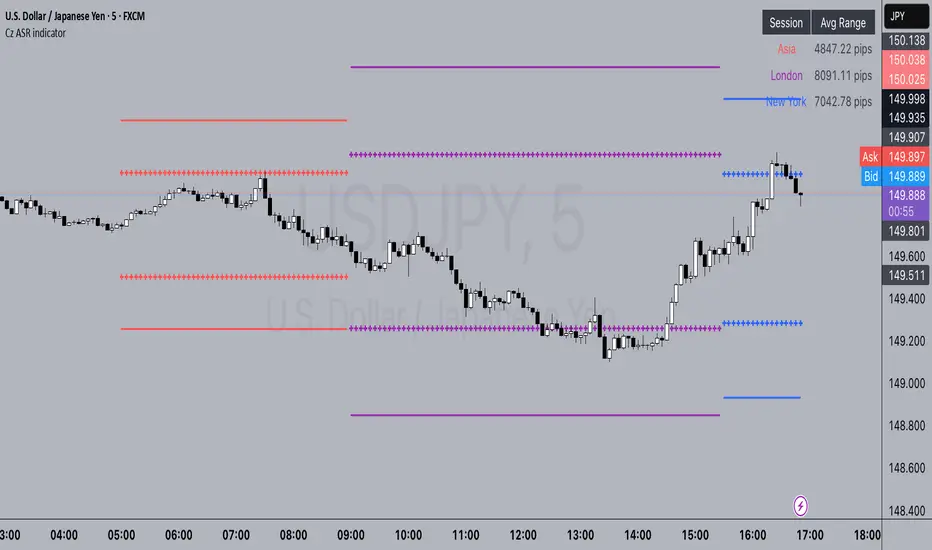

Cz ASR indicatorAverage session range indicator built by me. Great tool to gauge volatility and intraday reversal zones. Great for FX as there is an included table that shows range in pips; however, this can be applied across all assets as a volatility measure.

How it works:

The script measures the range of sessions, including Asia, London, and New York. The lookback period could be adjusted so you can find what length works best and is most accurate. This is then averaged out to provide the ASR. This provides us with an upper and lower bound of which the price could potentially fluctuate in based on the past session ranges. I have also added the 50% ASR, which is also a super useful metric for reversals or continuations.

There is also a configurable UTC so that you can adjust the indicator so it can accurately measure the range within certain sessions.

Note - different session start and stop times vary from market to market. I have set the code to the standard forex market opens however, if you wish to change the time ,you are able to do so by editing the variables in the script

Enjoy :)

Relative Volume Indicator (RVOL)Relative Volume Indicator (RVOL)

The Relative Volume Indicator (RVOL) helps traders identify unusual volume activity by comparing the current volume to the average historical volume. This makes it easier to spot potential breakouts, reversals, or significant market events that are accompanied by volume confirmation.

What This Indicator Shows

This indicator displays volume as a multiple of average volume, where:

- 1.0x means 100% of average volume

- 2.0x means 200% of average volume (twice the average)

- 0.5x means 50% of average volume (half the average)

Color Coding

The volume bars are color-coded based on configurable thresholds:

- Red: Below average volume (< Average Volume Threshold)

- Yellow: Average volume (between Average Volume and Above Average thresholds)

- Green: Above average volume (between Above Average and Extreme thresholds)

- Magenta: Extreme volume (> Extreme Volume Threshold)

Horizontal Reference Lines

Three dotted horizontal reference lines help you visualize the thresholds:

- Lower gray line: Average Volume Threshold (default: 0.8x)

- Upper gray line: Above Average Threshold (default: 1.25x)

- Magenta line: Extreme Volume Threshold (default: 4.0x)

How To Use This Indicator

1. Volume Confirmation: Use green bars to confirm breakouts or trend changes - stronger moves often come with above-average volume.

2. Low Volume Warning: Red bars during price movements may indicate weak conviction and potential reversals.

3. Extreme Volume Events: Magenta bars (extreme volume) often signal major market events or potential exhaustion points that could lead to reversals.

4. Volume Divergence: Look for divergences between price and volume - for example, if price makes new highs but volume is decreasing (more yellow/red bars), the move may be losing strength.

Settings Configuration

- Average Volume Lookback Period: Number of bars used to calculate the average volume (default: 20)

- Average Volume Threshold: Volume below this level is considered below average (default: 0.8x)

- Above Average Threshold: Volume above this level is considered above average (default: 1.25x)

- Extreme Volume Threshold: Volume above this level is considered extreme (default: 4.0x)

- Colors: Customize colors for each volume category

Important Note: Adjust threshold values only through the indicator settings (not in the Style tab). Changing values in the Style tab will not adjust the coloring of the volume bars.

Adjust these settings based on the specific asset being analyzed and your trading timeframe. More volatile assets may require higher thresholds, while less volatile ones might need lower thresholds.

SUPeR TReND 2.718An evolved version of the classic Supertrend, SUPeR TReND 2.718 is built to deliver elegant, high-precision trend detection using Euler's constant (e = 2.718) as its default multiplier. Designed for clarity and visual flow, this indicator brings together smooth line work, intelligent color logic, and a minimalistic tally system that tracks trend persistence — all in a highly customizable, overlay-ready format.

Unlike traditional implementations, this version maintains line visibility regardless of fill opacity, ensuring crisp tracking even in complex environments. Ideal for traders who value both aesthetics and actionable structure.

__________________________________________________________

🔑 Key Features:

- 📐 ATR-based Supertrend with default multiplier = e (2.718)

- 📉 Dynamic trend line with optional fill beneath price

- ⏳ Trend duration tally label (count-only or full format)

- ⬆️ Higher-timeframe Supertrend overlay (optional)

- 🟢 Directional candle coloring for clarity

- 🟡 Subtle anchor line to guide perception without clutter

- ⚙️ PineScript v6 compliant, efficient and modular

__________________________________________________________

🧠 Interpretation Guide:

- The Supertrend line tracks trend support or resistance — beneath price in uptrends, above in downtrends.

- The shaded fill reflects direction with 70% transparency.

- The trend tally label counts how long the current trend has lasted.

- Candle colors confirm direction without overtaking price action.

- The optional HTF line shows higher-timeframe context.

- A soft yellow anchor line stabilizes the fill relationship without distraction.

__________________________________________________________

⚙️ Inputs & Controls:

- ✏️ ATR Length – Volatility lookback

- 🧮 Multiplier – Default = 2.718 (Euler's number)

- 🕰️ Higher Timeframe – Choose your bias frame

- 👁️ Show HTF / Main – Toggle each trend layer

- 🧾 Show Label / Simplify – Show trend duration, with or without arrows

- 🎨 Color Candles – Turn directional bar coloring on or off

- 🪄 Show Fill – Toggle the shaded visual rhythm

- 🎛️ All visuals use tuned colors and transparencies for clarity

__________________________________________________________

🚀 Best Practices:

- ✅ Works on any time frame; shines on 1h v. 1D

- 🔁 Use the HTF line for macro bias filtering

- 📊 Combine with volume or liquidity overlays for edge

- 🧱 Use as a structural base layer with minimalist stacks

__________________________________________________________

📈 Strategy Tips:

- 🧭 MTF Trend Alignment: Enable the HTF line to filter trades. If the HTF trend is up, only take longs on the lower frame, and vice versa.

- 🔁 Pullback Entries: During a strong trend, consider short-term dips below the Supertrend line as possible re-entry zones — only if HTF remains aligned.

- ⏳ Tally for Exhaustion: When the bar count exceeds 15+, look for confluence (volume divergence, key levels, reversal signals).

- ⚠️ HTF Flip + Extended Trend: When the HTF trend reverses while the main trend is extended, that may be a macro exit or fade signal.

- 🚫 Solo Mode: Disable HTF and use the main trend + tally as a standalone signal layer.

- 🧠 Swing Setup Friendly: Especially powerful on 1D or 1h in swing systems or trend-based grid strategies.

ATR - Asymmetric Turbulence Ribbon🧭 Asymmetric Turbulence Ribbon (ATR)

The Asymmetric Turbulence Ribbon (ATR) is an enhanced and reimagined version of the standard Average True Range (ATR) indicator. It visualizes not just raw volatility, but the structure, momentum, and efficiency of volatility through a multi-layered visual approach.

It contains two distinct visual systems:

1. A zero-centered histogram that expresses how current volatility compares to its historical average, with intensity and color showing speed and conviction

2. A braided ribbon made of dual ATR-based moving averages that highlight transitions in volatility behavior—whether volatility is expanding or contracting

The name reflects its purpose: to capture asymmetric, evolving turbulence in market behavior, through structure-aware volatility tracking.

_______________________________________________________________

🔧 Inputs (Fibonacci defaults)

ATR Length

Lookback period for ATR calculation (default: 13)

ATR Base Avg. Length

Moving average period used as the zero baseline for histogram (default: 55)

ATR ROC Lookback

Number of bars to measure rate of change for histogram color mapping (default: 8)

Timeframe Override

Optionally calculate ATR values from a higher or fixed timeframe (e.g., 1D) for macro-volatility overlay

Show Ribbon Fill

Toggles colored fill between ATR EMA and HMA lines

Show ATR MAs

Toggles visibility of ATR EMA and HMA lines

Show Crossover Markers

Shows directional triangle markers where ATR EMA and HMA cross

Show Histogram

Toggles the entire histogram display

_______________________________________________________________

📊 Histogram Component: Volatility Energy Profile

The histogram shows how far the current ATR is from its moving average baseline, centered around zero. This lets you interpret volatility pressure—whether it's expanding, contracting, or preparing to reverse.

To complement this, the indicator also plots the raw ATR line in aqua. This is the actual average true range value—used internally in both the histogram and ribbon calculations. By default, it appears as a slightly thicker line, providing a clear reference point for comparing historical volatility trends and absolute levels.

Use the baseline ATR to:

- Compare real-time volatility to previous peaks or troughs

- Monitor how ATR behaves near histogram flips or ribbon crossovers

- Evaluate volatility phases in absolute terms alongside relative momentum

The ATR line is particularly helpful for users who want to keep tabs on raw volatility values while still benefiting from the enhanced visual storytelling of the histogram and ribbon systems.

Each histogram bar is colored based on the rate of change (ROC) in ATR: The faster ATR rises or falls, the more intense the color. Meanwhile, the opacity of each bar is adjusted by the effort/result ratio of the price candle (body vs. range), showing how much price movement was achieved with conviction.

Color Interpretation:

🔴 Red

Strong volatility expansion

Market entering or deepening into a volatility burst

Seen during breakouts, panic moves, or macro shock events

Often accompanied by large real candle bodies

🟠 Orange

Moderate volatility expansion

Heating up phase, often precedes breakouts

Common in strong trending environments

Signals tightening before acceleration

🟡 Yellow

Mild volatility increase

Transitional state—energy building, not yet exploding

Appears in early trend development or pullbacks

🟢 Green

Mild volatility contraction

ATR cooling off

Seen during consolidation, reversion, or range balance

Good time to assess upcoming directional setups

🔵 Aqua

Moderate compression

Volatility is clearly declining

Signals consolidation within larger structure

Pre-breakout zones often form here

🔵 Deep Blue

Strong volatility compression

Market is coiling or dormant

Can signal upcoming squeeze or fade environment

Often followed by sharp expansion

Opacity scaling:

Brighter bars = efficient, directional price action (strong bodies)

Faded bars = indecision, chop, absorption, or wick-heavy structure

Together, color and opacity give a 2D view of market volatility: Hue = the type and direction of volatility

Opacity = the quality and structure behind it

Use this to gauge whether volatility is rising with conviction, fading into neutrality, or compressing toward breakout potential.

_______________________________________________________________

🪡 Ribbon Component: Volatility Rhythm Structure

The ribbon overlays two moving averages of ATR:

EMA (yellow) – faster, more reactive

HMA (orange) – smoother, more rhythmic

Their relationship creates the ribbon logic:

Yellow fill (EMA > HMA)

Short-term volatility is increasing faster than the longer-term rhythm

Signals active expansion and engagement

Orange fill (HMA > EMA)

Volatility is decaying or leveling off

Suggests possible exhaustion, pullback, or range

Crossover triangle markers (optional, off by default to avoid clutter) identify the moment of shift in volatility phase.

The ribbon reflects the shape of volatility over time—ideal for mapping cyclical energy shifts, transitional states, and alignment between current and average volatility.

_______________________________________________________________

📐 Strategy Application

Use the Asymmetric Turbulence Ribbon to:

- Detect volatility expansions before breakouts or directional runs

- Spot compression zones that precede structural ruptures

- Visually separate efficient moves from noisy market activity

- Confirm or fade trade setups based on underlying energy state

- Track the volatility environment across multiple timeframes using the override

_______________________________________________________________

🎯 Ideal Timeframes

Designed to function across all timeframes, but particularly powerful on intraday to daily ranges (1H to 1D)

Use the timeframe override to anchor your chart in higher-timeframe volatility context, like daily ATR behavior influencing a 1H setup.

_______________________________________________________________

🧬 Customization Tips

- Increase ATR ROC Lookback for smoother color transitions

- Extend ATR Base Avg Length for more macro-driven histogram centering

- Disable the histogram for ribbon-only rhythm view

- Use opacity and color shifts in the histogram to detect stealth energy builds

- Align ATR phases with structure or order flow tools for high-quality setups

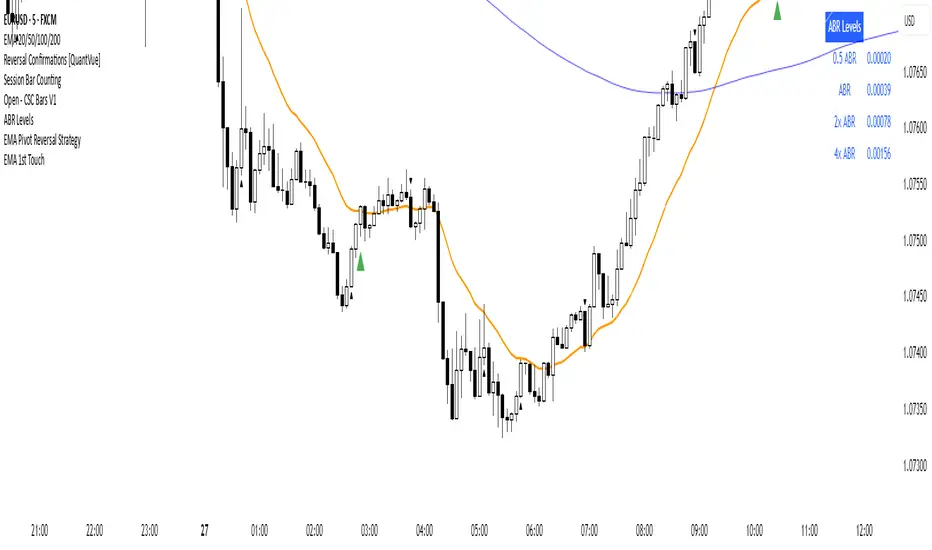

First EMA Touch (Last N Bars)Okay, here's a description of the "First EMA Touch (Last N Bars)" TradingView indicator:

Indicator Name: First EMA Touch (Last N Bars)

Core Purpose:

This indicator is designed to visually highlight on the chart the exact moment when the price (specifically, the high/low range of a price bar) makes contact with a specified Exponential Moving Average (EMA) for the first time within a defined recent lookback period (e.g., the last 20 bars).

How it Works:

EMA Calculation: It first calculates a standard Exponential Moving Average (EMA) based on the user-defined EMA Length and EMA Source (e.g., close price). This EMA line is plotted on the chart, often serving as a dynamic level of potential support or resistance.

"Touch" Detection: For every price bar, the indicator checks if the bar's range (from its low to its high) overlaps with or crosses the calculated EMA value for that bar. If low <= EMA <= high, it's considered a "touch".

"First Touch" Logic: This is the key feature. The indicator looks back over a specified number of preceding bars (defined by the Lookback Period). If a "touch" occurs on the current bar, and no "touch" occurred on any of the bars within that preceding lookback window, then the current touch is marked as the "first touch".

Visual Signal: When a "first touch" condition is met, the indicator plots a distinct shape (by default, a small green triangle) below the corresponding price bar. This makes it easy to spot these specific events.

Key Components & Settings:

EMA Line: The calculated EMA itself is plotted (typically as an orange line) for visual reference.

First Touch Signal: A shape (e.g., green triangle) appears below bars meeting the "first touch" criteria.

EMA Length (Input): Determines the period used for the EMA calculation. Shorter lengths make the EMA more reactive to recent price changes; longer lengths make it smoother and slower.

Lookback Period (Input): Defines how many bars (including the current one) the indicator checks backwards to determine if the current touch is the first one. A lookback of 20 means it checks if there was a touch in the previous 19 bars before signalling the current one as the first.

EMA Source (Input): Specifies which price point (close, open, high, low, hl2, etc.) is used to calculate the EMA.

Interpretation & Potential Uses:

Identifying Re-tests: The signal highlights when price returns to test the EMA after having stayed away from it for the duration of the lookback period. This can be significant as the market re-evaluates the EMA level.

Potential Reversal/Continuation Points: A first touch might indicate:

A potential area where a trend might resume after a pullback (if price bounces off the EMA).

A potential area where a reversal might begin (if price strongly rejects the EMA).

A point of interest if price consolidates around the EMA after the first touch.

Filtering Noise: By focusing only on the first touch within a period, it can help filter out repeated touches that might occur during choppy or consolidating price action around the EMA.

Confluence: Traders might use this signal in conjunction with other forms of analysis (e.g., horizontal support/resistance, trendlines, candlestick patterns, other indicators) to strengthen trade setups.

Limitations:

Lagging: Like all moving averages, the EMA is a lagging indicator.

Not Predictive: The signal indicates a specific past event (the first touch) occurred; it doesn't guarantee a future price movement.

Parameter Dependent: The effectiveness and frequency of signals heavily depend on the chosen EMA Length and Lookback Period. These may need tuning for different assets and timeframes.

Requires Confirmation: It's generally recommended to use this indicator as part of a broader trading strategy and not rely solely on its signals for trade decisions.

In essence, the "First EMA Touch (Last N Bars)" indicator provides a specific, refined signal related to price interaction with a moving average, helping traders focus on potentially significant initial tests of the EMA after a period of separation.

Litecoin Trailing-Stop StrategyAltcoins Trailing-Stop Strategy

This strategy is based on a momentum breakout approach using PKAMA (Powered Kaufman Adaptive Moving Average) as a trend filter, and a delayed trailing stop mechanism to manage risk effectively.

It has been designed and fine-tuned Altcoins, which historically shows consistent volatility patterns and clean trend structures, especially on intraday timeframes like 15m and 30m.

Strategy Logic:

Entry Conditions:

Long when PKAMA indicates an upward move

Short when PKAMA detects a downward trend

Minimum spacing of 30 bars between trades to avoid overtrading

Trailing Stop:

Activated only after a customizable delay (delayBars)

User can set trailing stop % and delay independently

Helps avoid premature exits due to short-term volatility

Customizable Parameters:

This strategy uses a custom implementation of PKAMA (Powered Kaufman Adaptive Moving Average), inspired by the work of alexgrover

PKAMA is a volatility-aware moving average that adjusts dynamically to market conditions, making it ideal for altcoins where trend strength and direction change frequently.

This script is for educational and experimental purposes only. It is not financial advice. Please test thoroughly before using it in live conditions, and always adapt parameters to your specific asset and time frame.

Feedback is welcome! Feel free to clone and adapt it for your own trading style.

02 SMC + BB Breakout (Improved)This strategy combines Smart Money Concepts (SMC) with Bollinger Band breakouts to identify potential trading opportunities. SMC focuses on identifying key price levels and market structure shifts, while Bollinger Bands help pinpoint overbought/oversold conditions and potential breakout points. The strategy also incorporates higher timeframe trend confirmation to filter out trades that go against the prevailing trend.

Key Components:

Bollinger Bands:

Calculated using a Simple Moving Average (SMA) of the closing price and a standard deviation multiplier.

The strategy uses the upper and lower bands to identify potential breakout points.

The SMA (basis) acts as a centerline and potential support/resistance level.

The fill between the upper and lower bands can be toggled by the user.

Higher Timeframe Trend Confirmation:

The strategy allows for optional confirmation of the current trend using a higher timeframe (e.g., daily).

It calculates the SMA of the higher timeframe's closing prices.

A bullish trend is confirmed if the higher timeframe's closing price is above its SMA.

This helps filter out trades that go against the prevailing long-term trend.

Smart Money Concepts (SMC):

Order Blocks:

Simplified as recent price clusters, identified by the highest high and lowest low over a specified lookback period.

These levels are considered potential areas of support or resistance.

Liquidity Zones (Swing Highs/Lows):

Identified by recent swing highs and lows, indicating areas where liquidity may be present.

The Swing highs and lows are calculated based on user defined lookback periods.

Market Structure Shift (MSS):

Identifies potential changes in market structure.

A bullish MSS occurs when the closing price breaks above a previous swing high.

A bearish MSS occurs when the closing price breaks below a previous swing low.

The swing high and low values used for the MSS are calculated based on the user defined swing length.

Entry Conditions:

Long Entry:

The closing price crosses above the upper Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bullish.

A bullish MSS must have occurred.

Short Entry:

The closing price crosses below the lower Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bearish.

A bearish MSS must have occurred.

Exit Conditions:

Long Exit:

The closing price crosses below the Bollinger Band basis.

Or the Closing price falls below 99% of the order block low.

Short Exit:

The closing price crosses above the Bollinger Band basis.

Or the closing price rises above 101% of the order block high.

Position Sizing:

The strategy calculates the position size based on a fixed percentage (5%) of the strategy's equity.

This helps manage risk by limiting the potential loss per trade.

Visualizations:

Bollinger Bands (upper, lower, and basis) are plotted on the chart.

SMC elements (order blocks, swing highs/lows) are plotted as lines, with user-adjustable visibility.

Entry and exit signals are plotted as shapes on the chart.

The Bollinger band fill opacity is adjustable by the user.

Trading Logic:

The strategy aims to capitalize on Bollinger Band breakouts that are confirmed by SMC signals and higher timeframe trend. It looks for breakouts that align with potential market structure shifts and key price levels (order blocks, swing highs/lows). The higher timeframe filter helps avoid trades that go against the overall trend.

In essence, the strategy attempts to identify high-probability breakout trades by combining momentum (Bollinger Bands) with structural analysis (SMC) and trend confirmation.

Key User-Adjustable Parameters:

Bollinger Bands Length

Standard Deviation Multiplier

Higher Timeframe

Higher Timeframe Confirmation (on/off)

SMC Elements Visibility (on/off)

Order block lookback length.

Swing lookback length.

Bollinger band fill opacity.

This detailed description should provide a comprehensive understanding of the strategy's logic and components.