Key Indicators Dashboard (KID)📌 Overview

Key Indicators Dashboard (KID) is a comprehensive all-in-one technical analysis tool designed for discretionary, systematic, and quantitative traders. It brings together multiple essential trading metrics into a highly customizable, interactive dashboard that overlays directly on your TradingView chart.

🎯 What Does KID Do?

KID consolidates all vital market metrics into a single, glanceable dashboard—saving screen space and analysis time. Whether you are screening equities or monitoring open positions, the KID panel updates dynamically, highlighting actionable signals and market conditions based on your own thresholds and trading style.

🛠 Key Features

⦿ Volatility and Range Metrics

ADR (Average Daily Range, % and Value): Quantifies average price movement over a defined period, with threshold-based color highlights.

ATR (Average True Range, % and Value): Measures volatility as both value and percentage of price.

⦿ Relative Strength and Trend Metrics

Relative Strength (RS) vs. Benchmark: Dynamically calculated using a customizable comparative symbol (default: NSE:NIFTYMIDSML400).

IBD-style RS Rating: Weighted average of price changes over several periods (3, 6, 9, and 12 months).

Trend Detection: Uses Supertrend indicator to visually identify up/down market trends.

⦿ Liquidity and Volume Analysis

Relative Volume (RVol): Comparison of current volume to moving average volume.

Turnover (in Cr): Average turnover calculation to assess liquidity.

Market Cap & Free Float: Real-time computation using price and outstanding/floating shares.

⦿ Trend Strength and Structure

MA Extensions: Compares price extension from a selected moving average, depicted as ATR multiples and percentages.

Moving Averages (MAs): Choice of EMA/SMA with customizable lengths, including up to four plotted MAs and detection of MA crossovers.

⦿ Breakout and Tightness Detectors

52-Week High/Low: Calculates and optionally marks the highest and lowest prices over 252 trading days, including percentage distance from current price.

Minervini Trend Template: The Trend Template is a set of technical criteria designed to identify stocks in strong uptrends.

• Price > 50-DMA > 150-DMA > 200-DMA

• 200-DMA is trending up for at least 1 month

• Price ≥ 52-week high proximity

• Price is at least 30% above its 52-week low.

• Price is within at least 25 percent of its 52-week high

• Table highlights when a stock meets all above criteria.

Tightness Indicator: Highlights periods with compressed price action relative to historical ranges.

⦿ Candlestick Patterns and Power Bars

Inside Bar Detection: Color- and shape-based highlighting of "inside bars" for pattern traders.

PowerBar (Purple Dot): Flags bars with strong price movement paired with high volume, using ROC and volume thresholds.

⦿ Sector/Industry

Automatically reflects symbol sector and industry if available from trading platform data.

⚙️ Customizable Visualization

Switchable between vertical or horizontal layout.

Works in dark/light mode

User-configurable to toggle any indicator ON or OFF.

User-configurable Moving (EMA/SMA), Period/Lengths and thresholds.

🔔 Built-in Alerts

Supports automatic alert creation for:

ADR%, ATR/ATR %, RS, RS Rating, Turnover

Moving Average Crossover (Bullish/Bearish)

52-Week High/Low

Inside Bars (Bullish/Bearish)

Tightness

Minervini Trend Template

⏳PineScreener Capabilities

The indicator’s alert conditions act as filters for PineScreener.

Available Screener Filters & Alerts:

Price Filters: Minimum and maximum price cutoffs.

Daily Change Filters: Minimum and maximum daily percent move.

Volatility Filters: ADR% and ATR% thresholds met or exceeded.

Liquidity Filters: Minimum average turnover and relative volume cutoffs.

Momentum/Trend Filters:

• Strong RS/RS Rating

• Uptrend/Downtrend state (Supertrend-based)

• Price extensions (detect overbought/oversold situations quickly)

• Breakout proximity via 52-week high/low alerts

Pattern and Setup Detection:

• Minervini Trend Template

• Inside Bar

• Tightness (compressed/volatility contraction setups)

• PowerBar (High ROC + high volume bars)

• MA crossover or above/below specific MAs

⦿ (Optional) : For horizontal table orientation increase Top Margin to 16% in Chart (Canvas) settings to avoid chart overlapping with table.

⚡ Add this script to your chart and start making smarter trade decisions today! 🚀

Volatility

WT + Stoch RSI Reversal Combo📊MR.Z RSI : WT + Stochastic RSI Reversal Combo

This custom indicator combines WaveTrend oscillator and Stochastic RSI to detect high-confidence market reversal points, filtering signals so they only appear when both indicators align.

🔍 Core Components:

✅ WaveTrend Oscillator

Based on smoothed deviation from EMA (similar to TCI logic)

Plots:

WT1 (main line)

WT2 (signal line = SMA of WT1)

Uses overbought/oversold thresholds (default: ±53) to filter signals

✅ Stochastic RSI

Momentum oscillator based on RSI's stochastic value

Plots:

%K: smoothed Stoch of RSI

%D: smoothed version of %K

Adjustable oversold/overbought thresholds (default: 20/80)

🔁 Combined Reversal Signal Logic:

🔼 Buy Signal

WT1 crosses above WT2 below WT oversold level (e.g., -53)

%K crosses above %D below Stoch RSI oversold level (e.g., 20)

🔽 Sell Signal

WT1 crosses below WT2 above WT overbought level (e.g., 53)

%K crosses below %D above Stoch RSI overbought level (e.g., 80)

🔔 Signals are only plotted and alerted if both conditions are true.

📌 Features:

Toggle on/off:

WaveTrend lines and histogram

Stochastic RSI

Combined Buy/Sell signals

Horizontal reference lines (±100, OB/OS)

Fully customizable smoothing lengths and thresholds

Signal plots:

✅ Green up-triangle = Combo Buy

✅ Red down-triangle = Combo Sell

Optional: Circle/cross markers for WT-only and Stoch-only signals

🔔 Built-in alerts for Buy/Sell signals

📈 Use Cases:

Reversal Trading: Wait for both indicators to confirm momentum shift

Entry Filter: Use in combination with trend indicators (like EMA)

Scalping or Swing: Works on intraday and higher timeframes

RV Indicator This Pine Script defines a custom Relative Volatility (RV) Indicator, which measures the ratio of directional price movement to volatility over a specified number of bars. Below is a full explanation of what this script does.

Title:

RV Indicator — Relative Volatility Oscillator

Purpose:

This indicator measures how aggressively price is moving compared to recent volatility, and smooths the result with a signal line. It can be used to gauge momentum shifts and trend strength.

How It Works – Step by Step

1. Measuring Price Momentum (v1)

It calculates the difference between the close and open prices of the last 4 candles.

A weighted average is applied:

The current candle and the one 3 bars ago get weight 1.

The two middle candles (1 and 2 bars ago) get weight 2.

This creates a smoothed momentum measure:

If close > open (bullish), v1 is positive.

If close < open (bearish), v1 is negative.

2. Measuring Volatility (v2)

Similarly, it calculates the high-low range for the last 4 candles.

The same weighting (1, 2, 2, 1) is applied.

This gives a smoothed volatility measure.

3. Combining Momentum and Volatility (RV Ratio)

For the past ti bars (default: 10), it sums up:

All v1 values (momentum sum)

All v2 values (volatility sum)

Then it divides them:

𝑅𝑉= sum of price momentum % sum of volatility

This produces the RV value:

RV > 0: Momentum is bullish (price is generally moving up relative to its volatility).

RV < 0: Momentum is bearish (price is moving down relative to its volatility).

4. Smoothed Signal Line (rvsig)

A smoothed version of the RV is created using a weighted average of the latest 4 RV values.

This acts like a signal line, similar to how MACD uses a signal line.

Crossovers between RV and this signal line can be used to detect shifts in momentum.

5. Visual Output

Orange Line (RV): Shows the raw momentum/volatility ratio.

Blue Line (Signal): A smoother line that follows RV more slowly.

Zero Line: Divides bullish vs. bearish momentum.

How to Use It in Trading

1. Look for Crossovers:

If RV crosses above its signal line → Possible buy signal (momentum turning bullish).

If RV crosses below its signal line → Possible sell signal (momentum turning bearish).

2. Check the Zero Line:

If both RV and Signal are above zero, momentum is bullish.

If both are below zero, momentum is bearish.

3. Filter False Signals:

Combine RV with a trend filter (like a 50 or 200 EMA) to avoid trading against the main trend.

Disclaimer: This script is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading decisions are solely your responsibility. Use at your own risk.

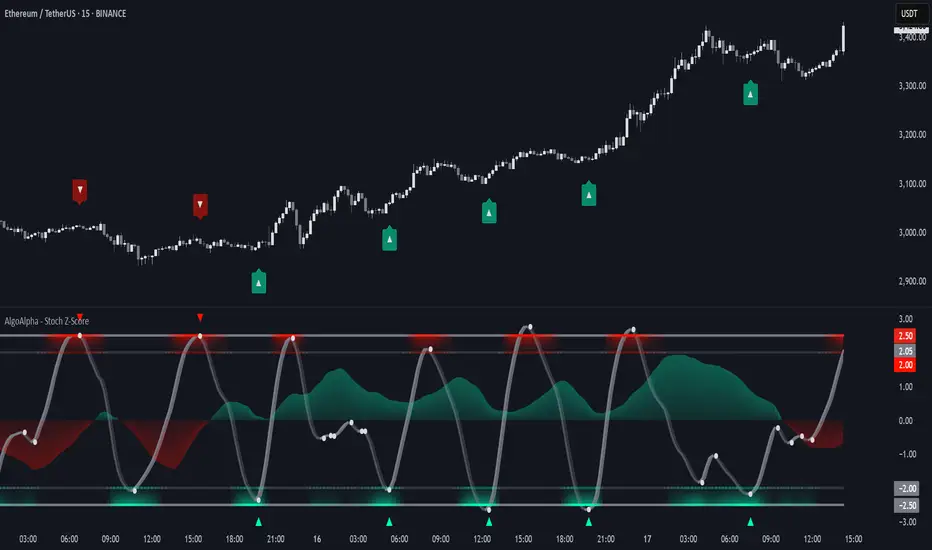

Stochastic Z-Score [AlgoAlpha]🟠 OVERVIEW

This indicator is a custom-built oscillator called the Stochastic Z-Score , which blends a volatility-normalized Z-Score with stochastic principles and smooths it using a Hull Moving Average (HMA). It transforms raw price deviations into a normalized momentum structure, then processes that through a stochastic function to better identify extreme moves. A secondary long-term momentum component is also included using an ALMA smoother. The result is a responsive oscillator that reacts to sharp imbalances while remaining stable in sideways conditions. Colored histograms, dynamic oscillator bands, and reversal labels help users visually assess shifts in momentum and identify potential turning points.

🟠 CONCEPTS

The Z-Score is calculated by comparing price to its mean and dividing by its standard deviation—this normalizes movement and highlights how far current price has stretched from typical values. This Z-Score is then passed through a stochastic function, which further refines the signal into a bounded range for easier interpretation. To reduce noise, a Hull Moving Average is applied. A separate long-term trend filter based on the ALMA of the Z-Score helps determine broader context, filtering out short-term traps. Zones are mapped with thresholds at ±2 and ±2.5 to distinguish regular momentum from extreme exhaustion. The tool is built to adapt across timeframes and assets.

🟠 FEATURES

Z-Score histogram with gradient color to visualize deviation intensity (optional toggle).

Primary oscillator line (smoothed stochastic Z-Score) with adaptive coloring based on momentum direction.

Dynamic bands at ±2 and ±2.5 to represent regular vs extreme momentum zones.

Long-term momentum line (ALMA) with contextual coloring to separate trend phases.

Automatic reversal markers when short-term crosses occur at extremes with supporting long-term momentum.

Built-in alerts for oscillator direction changes, zero-line crosses, overbought/oversold entries, and trend confirmation.

🟠 USAGE

Use this script to track momentum shifts and identify potential reversal areas. When the oscillator is rising and crosses above the previous value—especially from deeply negative zones (below -2)—and the ALMA is also above zero, this suggests bullish reversal conditions. The opposite holds for bearish setups. Reversal labels ("▲" and "▼") appear only when both short- and long-term conditions align. The ±2 and ±2.5 thresholds act as momentum warning zones; values inside are typical trends, while those beyond suggest exhaustion or extremes. Adjust the length input to match the asset’s volatility. Enable the histogram to explore underlying raw Z-Score movements. Alerts can be configured to notify key changes in momentum or zone entries.

Supertrend with ADX & MTF MA Filter# **Supertrend with ADX & MTF MA Filter - Comprehensive Explanation**

---

## **1. Purpose of This Indicator**

This indicator combines three powerful technical analysis tools to create a robust trading system:

✅ **Supertrend** (Trend-following)

✅ **ADX Filter** (Trend strength confirmation)

✅ **MTF MA Filter** (Multi-timeframe trend direction confirmation)

**Primary Goals:**

✔ **Identify high-probability trend reversals** with confirmation from multiple indicators

✔ **Filter out weak trends** using ADX (Average Directional Index)

✔ **Add higher timeframe context** with MTF (Multi-TimeFrame) Moving Average

✔ **Reduce false signals** by requiring confluence between all three components

---

## **2. Core Logic & Components**

### **A. Supertrend (Base Indicator)**

- **Calculation:**

```pine

up = hl2 - (Multiplier * ATR(Periods))

dn = hl2 + (Multiplier * ATR(Periods))

```

- **Bullish trend** when price > `up` (green line)

- **Bearish trend** when price < `dn` (red line)

- **Why Supertrend?**

- Simple yet effective trend-following system

- Adapts to volatility via ATR (Average True Range)

---

### **B. ADX Filter (Trend Strength Confirmation)**

- **ADX Calculation:**

```pine

= calcADX(adxLength, adxSmoothing)

strongTrend = adxVal >= adxThreshold

```

- **ADX > Threshold (Default: 20)** = Strong trend

- **DI+ > DI-** = Bullish momentum

- **DI- > DI+** = Bearish momentum

- **Why ADX?**

- Avoids trading in choppy markets (low ADX = weak trend)

- Confirms if Supertrend signals occur in a strong trend

---

### **C. MTF MA Filter (Higher Timeframe Trend Alignment)**

- **Moving Average Calculation:**

```pine

= getMA(maSource, maLength, maType, maTF)

```

- **MA Type:** SMA, EMA, WMA, or DEMA

- **Timeframe:** Any (1m, 5m, 1H, 4H, D, W, M)

- **Trend Direction:**

- **Buy Signal:** MA must be **rising**

- **Sell Signal:** MA must be **falling**

- **Why MTF MA?**

- Aligns trades with the **higher timeframe trend**

- Reduces counter-trend entries

---

## **3. How to Use This Indicator**

### **A. Buy Conditions (All Must Be True)**

1. **Supertrend turns bullish** (price crosses above `up` line)

2. **ADX ≥ Threshold** (trend is strong)

3. **Higher timeframe MA is rising** (confirms bullish bias)

### **B. Sell Conditions (All Must Be True)**

1. **Supertrend turns bearish** (price crosses below `dn` line)

2. **ADX ≥ Threshold** (trend is strong)

3. **Higher timeframe MA is falling** (confirms bearish bias)

### **C. Recommended Settings**

| Parameter | Recommended Value | Description |

|-----------|------------------|-------------|

| **ATR Period** | 14 | Sensitivity of Supertrend |

| **Multiplier** | 1.5-3.0 | Adjust for volatility |

| **ADX Threshold** | 20-25 | Higher = stricter trend filter |

| **MA Length** | 20-50 | Smoothness of trend filter |

| **MA Timeframe** | 1H/D | Align with trading style |

---

## **4. Trading Strategies**

### **A. Trend-Following Strategy**

- **Enter:** When all 3 conditions align (Supertrend + ADX + MA)

- **Exit:** When Supertrend flips or ADX drops below threshold

### **B. Pullback Strategy**

- **Wait for:**

- Supertrend in trend direction

- ADX remains strong

- MA still aligned

- **Enter:** On pullback to Supertrend line

### **C. Multi-Timeframe Confirmation**

- **Intraday traders:** Use 4H/D MA for trend bias

- **Swing traders:** Use D/W MA for trend bias

---

## **5. Advantages Over Standard Supertrend**

✔ **Fewer false signals** (ADX filters weak trends)

✔ **Higher timeframe alignment** (avoids trading against larger trends)

✔ **Customizable MA types** (SMA, EMA, WMA, DEMA)

✔ **Works on all markets** (stocks, forex, crypto)

---

### **Final Thoughts**

This indicator is designed for traders who want **high-confidence trend signals** by combining:

🔹 **Supertrend** (entry trigger)

🔹 **ADX** (trend strength filter)

🔹 **MTF MA** (higher timeframe trend alignment)

By requiring all three components to align, it significantly improves signal quality compared to standalone Supertrend systems.

**→ Best for:** Swing trading, trend-following, and avoiding choppy markets.

Lorentzian Theory Classifier🧮 Lorentzian Theory Classifier: An Observatory for Market Spacetime

Transcend the flat plane of traditional charting. Enter the curved, dynamic reality of market spacetime. The Lorentzian Theory Classifier (LTC) is not an indicator; it is a computational observatory. It is an instrument engineered to decode the geometry of market behavior, revealing the hidden curvatures and resonant frequencies that precede significant turning points.

We discard the outdated tools of Euclidean simplicity and embrace a more profound truth: financial markets, much like the cosmos described by general relativity, are governed by a fabric that is warped by the mass of participation and the energy of volatility. The LTC is your lens to perceive this fabric, to move beyond predicting lines on a chart and begin reading the very architecture of probability.

The Resonance Manifold: Standard Euclidean models search for historical analogues within a rigid sphere, missing the crucial outliers that define market extremes. The LTC's Lorentzian Resonance engine operates in a curved, non-Euclidean space, allowing it to connect with these "fat-tail" events—the true genesis points of major reversals.

🌌 THE THEORETICAL FRAMEWORK: A new Grand Unified Theory of Market Analysis

The LTC is built upon a revolutionary synthesis of concepts from special relativity, quantum mechanics, and information theory. It reframes market analysis not as a problem of forecasting, but as a problem of state recognition in a non-Euclidean manifold.

1. The Lorentzian Kernel: The Mathematics of Reality

Financial markets are not Gaussian. Their reality is one of "fat tails"—sudden, high-impact events that standard models dismiss as anomalies. The LTC acknowledges this reality by using the mathematically pure and robust Lorentzian kernel as its core engine:

Similarity(x, y) = 1 / (1 + (||x − y||² / γ²))

||x − y||²: The squared distance between the current market state (x) and a historical state (y) in our 8-dimensional feature space.

γ (Gamma): A dynamic bandwidth parameter, our "Lorentz factor," which adapts to market entropy (chaos). In calm markets, gamma is small, demanding precise resonance. In chaotic markets, gamma expands, intelligently seeking broader patterns.

This heavy-tailed function is revolutionary. It correctly assigns profound significance to the rare, extreme events that truly define market structure, while gracefully tuning out the noise of mundane price action. It doesn't just calculate; it understands context.

2. The 8-Dimensional State Vector: The Market's Quantum Fingerprint

To achieve a holistic view, the LTC projects the market onto an 8-dimensional Hilbert space, where each dimension represents a critical "observable":

Momentum & Acceleration (f_rsi, f_roc): The market's velocity and its rate of change.

Cyclical Position (f_stoch, f_cci): The market's location within its recent oscillation cycles.

Energy & Participation (f_vol, f_cor): The force of capital flow and its harmony with price.

Chaos & Uncertainty (f_ent, f_mom): The degree of randomness and the standardized force of price changes.

These are not eight separate indicators. They are entangled properties of a single "market wavefunction." The LTC's genius lies in measuring the geometric distance between these complete quantum states.

3. The k-NN Oracle: A Council of Past Universes

The LTC employs a k-Nearest Neighbors algorithm, but in our curved Lorentzian spacetime. It poses a constant, profound question: " Which moments in history are most geometrically congruent to the present moment across all eight dimensions? "

It then summons a "council" of these historical neighbors. Each neighbor's future outcome (did price ascend or descend?) casts a vote, weighted by its resonant similarity. The result is a probabilistic forecast of stunning clarity:

Prognosis: The final weighted consensus on future direction.

Assurance: The degree of unanimity within the council—a direct measure of the prediction's confidence.

The Funnel of Conviction: The LTC's process is a rigorous distillation of information. Raw, chaotic market data is resolved into a clean 8-dimensional state vector. The Lorentzian Kernel filters these states for resonance, which are then passed to the k-NN Oracle for a vote. Noise is eliminated at each stage, resulting in a single, validated, high-conviction signal.

⚙️ THE COMMAND CONSOLE: A Guide to Calibrating Your Observatory

Mastering the LTC's inputs is to become an architect of your own analytical universe. Each parameter is a dial that tunes the observatory's focus, from galactic structures to subatomic fluctuations. The tooltips in-script—over 6,000 words of documentation—provide immediate reference; this guide provides the philosophy.

A summarized guide to the Core, Signal, Supreme, and Visual controls is included directly in the indicator's code and tooltips. We encourage all users to explore these settings to tune the LTC to their unique analytical style.

🏆 THE SUPREME DASHBOARD: Your Mission Control

The dashboard is not a data table; it is your command interface with market reality. It translates the intricate dance of probabilities and vectors into clear, actionable intelligence.

⚡ ORACLE STATUS

Prognosis: The primary directional vector. Its color, magnitude, and emoji (⚡) reveal the strength and conviction of the Oracle's forward guidance.

Assurance: A real-time gauge of prediction quality, from "LOW" (high uncertainty) to "ELITE" (overwhelming statistical consensus). Interpret this as your core risk metric: trade with conviction when Assurance is ELITE; trade with caution when it is LOW.

🔮 RESONANCE ANALYSIS

Chaos: A direct measurement of market entropy. "LOW CHAOS" signifies a predictable, orderly regime. "HIGH CHAOS" is a warning of randomness and unpredictability, where trend-following logic may fail.

Turbulence: A measure of raw volatility. When the market is "TURBULENT," expect wider price swings and increased risk. Use this metric to adjust stop-loss distances and profit targets dynamically.

🏆 PERFORMANCE & ⚔️ GUARD METRICS

These sections provide illustrative statistics on the script's recent historical behavior. Metrics like Yield Ratio and Guard Index offer a quick heuristic on the prevailing risk-reward environment. Crucially, these are for observational context only and are not a substitute for your own rigorous testing and analysis.

🎨 THE VISUAL MANIFESTATION: Charting the Unseen

The LTC's visuals are designed to transform your chart from a 2D price graph into a 4D informational battlespace.

The Dynamic Aura (Background Color): This is the ambient energy field of the market. A luminous green (Ascend) signifies a bullish resonance field; a deep red (Descend) indicates bearish pressure.

The Assurance Shroud (Blue Bands): A visualization of confidence. When the shroud is wide and expansive , the Oracle's vision is clear and its predictions are robust.

The Prognosis Arc (Curved Line): A geodesic projection of the market's most likely path, based on the current Prognosis.

The Turbulence Cloud (Orange Mist): A visual warning system for market chaos. When this entropic mist expands , it is a clear sign that you are navigating a nebula of high unpredictability.

Oracle Markers (▲▼): The final, validated signals. These are not merely pivot points. They are moments in spacetime where a structural pivot has been confirmed and then ratified by a high-conviction vote from the Lorentzian Oracle. They are the pinnacles of confluence.

The Analyst's Observatory: The LTC transforms your chart into a command center for market analysis, providing a complete, at-a-glance view of market state, risk, and probabilistic trajectory.

🔧 THE ARCHITECT'S VISION: From a Blank Slate to a New Cosmos

The LTC was not assembled; it was derived. It began not with code, but with first principles, asking: "If we were to build an instrument to measure the market today, unbound by the technical dogmas of the 20th century, what would it look like?" The answer was clear: it must be multi-dimensional, it must be adaptive, and it must be built on a mathematical framework that respects the "fat-tailed" nature of reality.

The decision to use a pure Lorentzian kernel was non-negotiable. It represented a commitment to intellectual honesty over computational ease. The development of the Supreme Dashboard was driven by the philosophy of the "glass cockpit"—a belief that a trader's greatest asset is not a black box signal, but a transparent and intuitive flow of high-quality information. This script is the result of that unwavering vision: to create not just another indicator, but a new lens through which to perceive the market.

⚠️ RISK DISCLOSURE & PHILOSOPHY OF USE

The Lorentzian Theory Classifier is an instrument of profound analytical power, intended for the serious, discerning trader. It does not generate infallible signals. It generates high-probability, data-driven hypotheses based on a rigorous and transparent methodology. All trading involves substantial risk, and the future is fundamentally unknowable. Past performance, whether real or simulated, is no guarantee of future results. Use this tool to augment your own skill, to confirm your own analysis, and to manage your own risk within a well-defined trading plan.

"The effort to understand the universe is one of the very few things that lifts human life a little above the level of farce, and gives it some of the grace of tragedy."

— Steven Weinberg, Nobel Laureate in Physics

Trade with rigor. Trade with perspective. Trade with enlightenment. Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

Synthetic VX3! & VX4! continuous /VX futuresTradingView is missing continuous 3rd and 4th month VIX (/VX) futures, so I decided to try to make a synthetic one that emulates what continuous maturity futures would look like. This is useful for backtesting/historical purposes as it enables traders to see how their further out VX contracts would've performed vs the front month contract.

The indicator pulls actual realtime data (if you subscribe to the CBOE data package) or 15 minute delayed data for the VIX spot (the actual non-tradeable VIX index), the continuous front month (VX1!), and the continuous second month (VX2!) continually rolled contracts. Then the indicator's script applies a formula to fairly closely estimate how 3rd and 4th month continuous contracts would've moved.

It uses an exponential mean‑reversion to a long‑run level formula using:

σ(T) = θ+(σ0−θ)e−kT

You can expect it to be off by ~5% or so (in times of backwardation it might be less accurate).

Beta calculatorCalculates the market beta for the stock that is on your screen. You may change the parameters by changing the symbol you are using as benchmark to calculate market beta in the settings. This will affect the market beta you get. VTI is used since it has a theoretical market beta of 1.

Squeeze Pro Momentum BAR color - KLTDescription:

The Squeeze Pro Momentum indicator is a powerful tool designed to detect volatility compression ("squeeze" zones) and visualize momentum shifts using a refined color-based system. This script blends the well-known concepts of Bollinger Bands and Keltner Channels with an optimized momentum engine that uses dynamic color gradients to reflect trend strength, direction, and volatility.

It’s built for traders who want early warning of potential breakouts and clearer insight into underlying market momentum.

🔍 How It Works:

📉 Squeeze Detection:

This indicator identifies "squeeze" conditions by comparing Bollinger Bands and Keltner Channels:

When Bollinger Bands are inside Keltner Channels → Squeeze is ON

When Bollinger Bands expand outside Keltner Channels → Squeeze is OFF

You’ll see squeeze zones classified as:

Wide

Normal

Narrow

Each represents varying levels of compression and breakout potential.

⚡ Momentum Engine:

Momentum is calculated using linear regression of the price's deviation from a dynamic average of highs, lows, and closes. This gives a more accurate representation of directional pressure in the market.

🧠 Smart Candle Coloring (Optimized):

The momentum color logic is inspired by machine learning principles (no hardcoded thresholds):

EMA smoothing and rate of change (ROC) are used to detect momentum acceleration.

ATR-based filters help remove noise and false signals.

Colors are dynamically assigned based on both direction and trend strength.

🧪 How to Use It:

Look for Squeeze Conditions — especially narrow squeezes, which tend to precede high-momentum breakouts.

Confirm with Momentum Color — strong colors often indicate trend continuation; fading colors may signal exhaustion.

Combine with Price Action — use this tool with support/resistance or patterns for higher probability setups.

Recommended For:

Trend Traders

Breakout Traders

Volatility Strategy Users

Anyone who wants visual clarity on trend strength

📌 Tip: This indicator works great when layered with volume and price action patterns. It is fully non-repainting and supports overlay on price charts.

Fair Value Gap [Dova Lazarus]Fair Value Gap (FVG) indicator detects and visualizes price inefficiencies between three consecutive candles:

* Bullish FVG: current candle’s low > high of two candles ago

* Bearish FVG: current candle’s high < low of two candles ago

Includes automatic detection of mitigations:

* Partial mitigation: price enters but doesn’t fully fill the gap

* Full mitigation: price completely fills the gap

* Optional **50% mitigation** based on midpoint reach

**Display styles**:

* Box (filled rectangle)

* High & Low lines only

* Midpoint lines (optional, with customizable style and color)

Multi-timeframe support:

* Up to 5 higher timeframes (HTF), each with individual color, label, and visibility settings

* HTF gaps help identify key support/resistance and price magnet zones

Customization options:

* Separate colors for unmitigated and mitigated gaps

* Adjustable width and extension of boxes

* Optional deletion of mitigated gaps

* Label positioning, size, and visibility

All settings are grouped for clarity:

* FVG Appearance

* HTF FVGs

* Mitigation

* General Settings

BB with Heikin Ashi + Reversal CheckThis indicator combines Bollinger Bands (BB) with Heikin Ashi candles to detect potential reversal points after price breaks the BB boundaries. It works on any symbol and timeframe, retrieving Heikin Ashi data via request.security().

Core Features

Heikin Ashi Candle Plot

Smooths price action by using Heikin Ashi candles instead of regular candles.

Candles are plotted directly on the chart with green (bullish) and red (bearish) colors.

Bollinger Bands (BB)

Calculated from Heikin Ashi close price.

Includes Basis (MA), Upper Band, and Lower Band, with customizable MA type, length, and standard deviation multiplier.

Break & Reversal Detection

The indicator tracks whether the price has broken above the Upper Band (p1) or below the Lower Band (p2).

It remembers the last breakout direction until the opposite breakout occurs (mutually exclusive logic).

Signal Logic

Long Signal (▲):

Price was previously below the Lower Band and then reversed upward (BB Lower rising + Heikin Ashi candle rising).

Short Signal (▼):

Price was previously above the Upper Band and then reversed downward (BB Upper falling + Heikin Ashi candle falling).

Alerts

Custom alert conditions trigger when Long or Short signals occur, allowing automated notifications or bot integration.

Use Cases

✅ Swing Trading / Trend Reversal – Identify potential bottom/top reversals after BB breakouts.

✅ Mean Reversion Strategies – Enter trades when the price reverts to the BB mean after an extreme breakout.

✅ Multi-Timeframe Analysis – Works with any timeframe and symbol via request.security().

Customization

MA Type: SMA, EMA, RMA, WMA, VWMA

BB Length & StdDev Multiplier

Timeframe & Symbol Selection

Days Since ±1% Move on CloseInterpretation & Use‑Case

The “Days Since ±1% Move” indicator simply tells you how many trading days have passed since the last daily close that moved at least 1% in either direction. Here’s how to put it to work:

Complacency Gauge

A long stretch without a ≥1% move often signals that realized volatility has collapsed and market participants may be under‑positioned for a sudden swing.

Positioning Insight

When institutional hedges and systematic strategies see low recent volatility, they tend to scale back protection (fewer options hedges, tighter risk limits), which can amplify the impact of any eventual volatility pickup.

Mean‑Reversion Signal

After an extended streak (e.g. 20–30 days), a fresh ≥1% move is more likely—and often more violent—because pent‑up positioning flows rush to adjust.

Trend Confirmation

Conversely, a reset in the count (i.e., a new ≥1% move) that coincides with strong volume and follow‑through suggests genuine directional conviction rather than just a volatility “blip.”

Buyer/Seller Zone (Simplified Version)📌 Indicator: Buyer/Seller Zone (Simplified Version)

This indicator is designed to highlight potential areas of strong buyer or seller activity based on advanced volume and volatility analysis. It identifies key candles that exhibit anomalous behavior — those standing out from typical market noise — and marks them as potential interest zones.

🔍 What it does:

Detects candles with unusually high volume (anomalies).

Filters them further based on strong price movement (volatility).

Marks bullish and bearish zones using customizable visuals: area, circle, or diamond.

Provides optional alerts when a buyer/seller signal is detected.

💡 How to use:

Use this tool to identify potential reversal or continuation zones.

Zones may act as strong support/resistance areas.

Some levels are more significant than others — do not trade every level blindly. Combine with your own analysis or wait for a retest/confirmation before entry.

⚙️ Customization:

Volume filter threshold

Volatility sensitivity

Visualization type, size, and transparency

🚨 Alerts: Set alerts for bullish, bearish, or any signal type.

Minimalist Trend & Risk For 5-Min Timeframe

Of course. Here is a professionally written TradingView description for your indicator, following the specified formatting and incorporating the strategy you outlined.

Minimalist Trend & Risk For 5-Min Timeframe

Overview

This is a clean, on-chart visual tool designed to identify high-probability entries and manage risk, specifically tailored for a 5-minute scalping or day trading strategy. It combines a higher-timeframe trend anchor with a current-timeframe trigger line and a volatility-based stop loss level, keeping your chart uncluttered and your decisions clear.

Visual Components

Trend EMA (50-period, 15-min): This is your main trend guide. The thick, colored line represents the 50 EMA from the 15-minute chart.

Green: Confirmed uptrend.

Red: Confirmed downtrend.

Gray: Neutral or consolidating market.

Price EMA (21-period, 5-min): The thin white line is the 21 EMA based on your current chart (5-minute). This acts as a dynamic trigger line that price must reclaim after a pullback.

Stop Loss Zone (ATR-based): The thin red line provides a suggested stop loss level based on current market volatility (ATR). It automatically appears below price in an uptrend and above price in a downtrend, helping you define your risk on every trade.

How To Use for a Long Entry Strategy

The strategy is to trade pullbacks in the direction of the higher-timeframe trend. This indicator helps you visualize each step of the setup.

1. Identify the Trend: Wait for the main Trend EMA (the thick line) to be green. This confirms you are in an established uptrend on the 15-minute timeframe and should only be looking for long entries.

2. Wait for a Pullback: The core of the strategy is patience. Wait for a 5-minute candlestick to pull back and close below the 15-minute Trend EMA. This confirms a temporary dip within the larger uptrend, offering a better entry price.

3. Spot the Entry Trigger: After the pullback, the entry signal occurs when a 5-minute candlestick closes back above the faster, white Price EMA (21-period). This signals that momentum is returning in the direction of the main trend.

4. Manage Your Risk: Use the red Stop Loss Zone line that appears below your entry as a guide to set your initial stop loss. This helps ensure your risk is managed dynamically based on current volatility.

This indicator simplifies a powerful pullback strategy by plotting all the necessary components directly on your chart, allowing for quick and disciplined trade execution.

Multi-Timeframe 200 SMA OverlayMulti Timeframe 200 SMAs

Indicator Displays and labels on anytime frame:

2 minute 200 SMA

5 minute 200 SMA

10 minute 200 SMA

15 minute 200 SMA

1 Hour 200 SMA

4 Hour 200 SMA

1 Day 200 SMA

Reversal Point Dynamics⇋ Reversal Point Dynamics (RPD)

This is not an indicator; it is a complete system for deconstructing the mechanics of a market reversal. Reversal Point Dynamics (RPD) moves far beyond simplistic pattern recognition, venturing into a deep analysis of the underlying forces that cause trends to exhaust, pause, and turn. It is engineered from the ground up to identify high-probability reversal points by quantifying the confluence of market dynamics in real-time.

Where other tools provide a static signal, RPD delivers a dynamic probability. It understands that a true market turning point is not a single event, but a cascade of failing momentum, structural breakdown, and a shift in market order. RPD's core engine meticulously analyzes each of these dynamic components—the market's underlying state, its velocity and acceleration, its degree of chaos (entropy), and its structural framework. These forces are synthesized into a single, unified Probability Score, offering you an unprecedented, transparent view into the conviction behind every potential reversal.

This is not a "black box" system. It is an open-architecture engine designed to empower the discerning trader. Featuring real-time signal projection, an integrated Fibonacci R2R Target Engine, and a comprehensive dashboard that acts as your Dynamics Control Center , RPD gives you a complete, holistic view of the market's state.

The Theoretical Core: Deconstructing Market Dynamics

RPD's analytical power is born from the intelligent synthesis of multiple, distinct theoretical models. Each pillar of the engine analyzes a different facet of market behavior. The convergence of these analyses—the "Singularity" event referenced in the dashboard—is what generates the final, high-conviction probability score.

1. Pillar One: Quantum State Analysis (QSA)

This is the foundational analysis of the market's current state within its recent context. Instead of treating price as a random walk, QSA quantizes it into a finite number of discrete "states."

Formulaic Concept: The engine establishes a price range using the highest high and lowest low over the Adaptive Analysis Period. This range is then divided into a user-defined number of Analysis Levels. The current price is mapped to one of these states (e.g., in a 9-level system, State 0 is the absolute low, and State 8 is the absolute high).

Analytical Edge: This acts as a powerful foundational filter. The engine will only begin searching for reversal signals when the market has reached a statistically stretched, extreme state (e.g., State 0 or 8). The Edge Sensitivity input allows you to control exactly how close to this extreme edge the price must be, ensuring you are trading from points of maximum potential exhaustion.

2. Pillar Two: Price State Roc (PSR) - The Dynamics of Momentum

This pillar analyzes the kinetic forces of the market: its velocity and acceleration. It understands that it’s not just where the price is, but how it got there that matters.

Formulaic Concept: The psr function calculates two derivatives of price.

Velocity: (price - price ). This measures the speed and direction of the current move.

Acceleration: (velocity - velocity ). This measures the rate of change in that speed. A negative acceleration (deceleration) during a strong rally is a critical pre-reversal warning, indicating momentum is fading even as price may be pushing higher.

Analytical Edge: The engine specifically hunts for exhaustion patterns where momentum is clearly decelerating as price reaches an extreme state. This is the mechanical signature of a weakening trend.

3. Pillar Three: Market Entropy Analysis - The Dynamics of Order & Chaos

This is RPD's chaos filter, a concept borrowed from information theory. Entropy measures the degree of randomness or disorder in the market's price action.

Formulaic Concept: The calculateEntropy function analyzes recent price changes. A market moving directionally and smoothly has low entropy (high order). A market chopping back and forth without direction has high entropy (high chaos). The value is normalized between 0 and 1.

Analytical Edge: The most reliable trades occur in low-entropy, ordered environments. RPD uses the Entropy Threshold to disqualify signals that attempt to form in chaotic, unpredictable conditions, providing a powerful shield against whipsaw markets.

4. Pillar Four: The Synthesis Engine & Probability Calculation

This is where all the dynamic forces converge. The final probability score is a weighted calculation that heavily rewards confluence.

Formulaic Concept: The calculateProbability function intelligently assembles the final score:

A Base Score is established from trend strength and entropy.

An Entropy Score adds points for low entropy (order) and subtracts for high entropy (chaos).

A significant Divergence Bonus is awarded for a classic momentum divergence.

RSI & Volume Bonuses are added if momentum oscillators are in extreme territory or a volume spike confirms institutional interest.

MTF & Adaptive Bonuses add further weight for alignment with higher timeframe structure.

Analytical Edge: A signal backed by multiple dynamic forces (e.g., extreme state + decelerating momentum + low entropy + volume spike) will receive an exponentially higher probability score. This is the very essence of analyzing reversal point dynamics.

The Command Center: Mastering the Inputs

Every input is a precise lever of control, allowing you to fine-tune the RPD engine to your exact trading style, market, and timeframe.

🧠 Core Algorithm

Predictive Mode (Early Detection):

What It Is: Enables the engine to search for potential reversals on the current, unclosed bar.

How It Works: Analyzes intra-bar acceleration and state to identify developing exhaustion. These signals are marked with a ' ? ' and are tentative.

How To Use It: Enable for scalping or very aggressive day trading to get the earliest possible indication. Disable for swing trading or a more conservative approach that waits for full bar confirmation.

Live Signal Mode (Current Bar):

What It Is: A highly aggressive mode that plots tentative signals with a ' ! ' on the live bar based on projected price and momentum. These signals repaint intra-bar.

How It Works: Uses a linear regression projection of the close to anticipate a reversal.

How To Use It: For advanced users who use intra-bar dynamics for execution and understand the nature of repainting signals.

Adaptive Analysis Period:

What It Is: The main lookback period for the QSA, PSR, and Entropy calculations. This is the engine's "memory."

How It Works: A shorter period makes the engine highly sensitive to local price swings. A longer period makes it focus only on major, significant market structure.

How To Use It: Scalping (1-5m): 15-25. Day Trading (15m-1H): 25-40. Swing Trading (4H+): 40-60.

Fractal Strength (Bars):

What It Is: Defines the strength of the pivot detection used for confirming reversal events.

How It Works: A value of '2' requires a candle's high/low to be more extreme than the two bars to its left and right.

How To Use It: '2' is a robust standard. Increase to '3' for an even stricter definition of a structural pivot, which will result in fewer signals.

MTF Multiplier:

What It Is: Integrates pivot data from a higher timeframe for confluence.

How It Works: A multiplier of '4' on a 15-minute chart will pull pivot data from the 1-hour chart (15 * 4 = 60m).

How To Use It: Set to a multiple that corresponds to your preferred higher timeframe for contextual analysis.

🎯 Signal Settings

Min Probability %:

What It Is: Your master quality filter. A signal is only plotted if its score exceeds this threshold.

How It Works: Directly filters the output of the final probability calculation.

How To Use It: High-Quality (80-95): For A+ setups only. Balanced (65-75): For day trading. Aggressive (50-60): For scalping.

Min Signal Distance (Bars):

What It Is: A noise filter that prevents signals from clustering in choppy conditions.

How It Works: Enforces a "cooldown" period of N bars after a signal.

How To Use It: Increase in ranging markets to focus on major swings. Decrease on lower timeframes.

Entropy Threshold:

What It Is: Your "chaos shield." Sets the maximum allowable market randomness for a signal.

How It Works: If calculated entropy is above this value, the signal is invalidated.

How To Use It: Lower values (0.1-0.5): Extremely strict. Higher values (0.7-1.0): More lenient. 0.85 is a good balance.

Adaptive Entropy & Aggressive Mode:

What It Is: Toggles for dynamically adjusting the engine's core parameters.

How It Works: Adaptive Entropy can slightly lower the required probability in strong trends. Aggressive Mode uses more lenient settings across the board.

How To Use It: Keep Adaptive on. Use Aggressive Mode sparingly, primarily for scalping highly volatile assets.

📊 State Analysis

Analysis Levels:

What It Is: The number of discrete "states" for the QSA.

How It Works: More levels create a finer-grained analysis of price location.

How To Use It: 6-7 levels are ideal. Increasing to 9 can provide more precision on very volatile assets.

Edge Sensitivity:

What It Is: Defines how close to the absolute top/bottom of the range price must be.

How It Works: '0' means price must be in the absolute highest/lowest state. '3' allows a signal within the top/bottom 3 states.

How To Use It: '3' provides a good balance. Lower it to '1' or '0' if you only want to trade extreme exhaustion.

The Dashboard: Your Dynamics Control Center

The dashboard provides a transparent, real-time view into the engine's brain. Use it to understand the context behind every signal and to gauge the current market environment at a glance.

🎯 UNIFIED PROB SCORE

TOTAL SCORE: The highest probability score (either Peak or Valley) the engine is currently calculating. This is your main at-a-glance conviction metric. The "Singularity" header refers to the event where market dynamics align—the event RPD is built to detect.

Quality: A human-readable interpretation of the Total Score. "EXCEPTIONAL" (🌟) is a rare, A+ confluence event. "STRONG" (💪) is a high-quality, tradable setup.

📊 ORDER FLOW & COMPONENT ANALYSIS

Volume Spike: Shows if the current volume is significantly higher than average (YES/NO). A 'YES' adds major confirmation.

Peak/Valley Conf: This breaks down the probability score into its directional components, showing you the separate confidence levels for a potential top (Peak) versus a bottom (Valley).

🌌 MARKET STRUCTURE

HTF Trend: Shows the direction of the underlying trend based on a Supertrend calculation.

Entropy: The current market chaos reading. "🔥 LOW" is an ideal, ordered state for trading. "😴 HIGH" is a warning of choppy, unpredictable conditions.

🔮 FIB & R2R ZONE (Large Dashboard)

This section gives you the status of the Fibonacci Target Engine. It shows if an Active Channel (entry zone) or Stop Zone (invalidation zone) is active and displays the precise price levels for the static entry, target, and stop calculated at the time of the signal.

🛡️ FILTERS & PREDICTIVES (Large Dashboard)

This panel provides a status check on all the bonus filters. It shows the current RSI Status, whether a Divergence is present, and if a Live Pending signal is forming.

The Visual Interface: A Symphony of Data

Every visual element is designed for instant, intuitive interpretation of market dynamics.

Signal Markers: These are the primary outputs of the engine.

▼/▲ b: A fully confirmed signal that has passed all filters.

? b: A tentative signal generated in Predictive Mode, indicating developing dynamics.

◈ b: This diamond icon replaces the standard triangle when the signal is confirmed by a strong momentum divergence, highlighting it as a superior setup where dynamics are misaligned with price.

Harmonic Wave: The flowing, colored wave around the price.

What It Represents: The market's "flow dynamic" and volatility.

How to Interpret It: Expanding waves show increasing volatility. The color is tied to the "Quantum Color" in your theme, representing the underlying energy field of the market.

Entropy Particles: The small dots appearing above/below price.

What They Represent: A direct visualization of the "order dynamic."

How to Interpret Them: Their presence signifies a low-entropy, ordered state ideal for trading. Their color indicates the direction of momentum (PSR velocity). Their absence means the market is too chaotic (high entropy).

The Fibonacci Target Engine: The dynamic R2R system appearing post-signal.

Static Fib Levels: Colored horizontal lines representing the market's "structural dynamic."

The Green "Active Channel" Box: Your zone of consideration. An area to manage a potential entry.

Development Philosophy

Reversal Point Dynamics was engineered to answer a fundamental question: can we objectively measure the forces behind a market turn? It is a synthesis of concepts from market microstructure, statistics, and information theory. The objective was never to create a "perfect" system, but to build a robust decision-support tool that provides a measurable, statistical edge by focusing on the principle of confluence.

By demanding that multiple, independent market dynamics align simultaneously, RPD filters out the vast majority of market noise. It is designed for the trader who thinks in terms of probability and risk management, not in terms of certainties. It is a tool to help you discount the obvious and bet on the unexpected alignment of market forces.

"Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected."

— George Soros

Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

xGhozt Percentage Price ChangeDisplays two dynamic horizontal lines at ±X% from the current price, with customizable colors and labels. Useful for visualizing profit targets, stop loss zones, or expected volatility ranges. Labels show both the percentage and the corresponding price.

WaveTrend with CrossesWaveTrend with Crosses — Spot Golden & Dead Crosses with Precision!

WaveTrend with Crosses is a customized version of the classic WaveTrend oscillator, enhanced with clean visual signals to help you pinpoint momentum shifts through golden and dead crosses.

✅ Key Features

Momentum analysis based on WaveTrend (WT1 & WT2)

Detects Golden Cross (WT1 crosses above WT2) and

Dead Cross (WT1 crosses below WT2)

Customizable Overbought/Oversold zones (defaults: ±60, ±53)

Visual circle markers on valid crossovers for easy recognition

Built-in alert system to notify you of real-time cross signals

📊 How to Use

Add the indicator to your chart and choose your desired symbol & timeframe.

The blue shaded area shows the divergence between WT1 and WT2 — a visual cue for momentum buildup.

Circle markers:

Red circle: Dead cross — potential bearish momentum

Green circle: Golden cross — potential bullish reversal

Customize the settings to fit your personal trading strategy if needed.

🛠 User Inputs

n1, n2: Channel lengths (default: 10 and 21)

obLevel, osLevel: Overbought/Oversold thresholds (default: ±60 / ±53)

standardValue: Threshold used to validate significant crossovers (default: 60)

🔔 Alert System

Get notified with alerts like "Golden Cross" or "Dead Cross" when key crossovers occur,

helping you react quickly and confidently.

⚠️ Notes

Past performance is not indicative of future results — always backtest and use in conjunction with other tools.

Low timeframes may generate frequent signals; filtering or confirmation is recommended.

💡 Author's Note

Simple and effective — this tool is designed to focus solely on cross-based entries.

Ideal for momentum-based scalping or swing trading strategies.

Feel free to customize and tweak as needed! 😄

Trend Range Detector (Zeiierman)█ Overview

Trend Range Detector (Zeiierman) is a market structure tool that identifies and tracks periods of price compression by forming adaptive range boxes based on volatility and price movement. When prices remain stable within a defined band, the script dynamically draws a range box; when prices break out of that structure, the box highlights the breakout in real-time.

By combining a volatility-based envelope with a custom weighted centerline, this tool filters out noise and isolates truly stable zones — providing a clean framework for traders who focus on accumulation, distribution, breakout anticipation, and reversion opportunities.

Whether you're range trading, spotting trend consolidations, or looking for volatility contractions before major moves, the Trend Range Detector gives you a mathematically adaptive, visually intuitive structure that maps the heartbeat of the market.

█ How It Works

⚪ Range Formation Engine

The core of this indicator revolves around two conditions:

Distance Filter: The maximum distance between all recent closes and a dynamic centerline must remain within a volatility envelope.

Volatility Envelope: Based on an ATR(2000) multiplied by a user-defined factor to account for broader market volatility trends.

If both conditions are satisfied over the most recent length bars, a range box is drawn to visually anchor the zone.

⚪ Dynamic Breakout Coloring

When price breaks out of the top or bottom of the active range box, the box color shifts in real-time:

Blue Boxes represent areas where price has remained within a defined volatility envelope over a sustained number of bars. These zones reflect stable, low-volatility periods, often associated with consolidation, equilibrium, or market indecision.

Green Boxes for bullish breakouts.

Red Boxes for bearish breakdowns.

This allows traders to visually spot transitions from consolidation to expansion phases without relying on lagging signals.

█ Why Use a Weighted Close Instead of SMA?

A standard Simple Moving Average (SMA) treats all past closes equally, which works well in theory, but not in dynamic, fast-shifting markets. In this script, we replace the traditional SMA with a speed-weighted average that reflects how aggressively the market has moved bar-to-bar.

⚪ Here's why it matters:

Bars with higher momentum (larger price differences between closes) are given more weight.

Slow, sideways candles (typical in noise or low volume) contribute less to the calculated centerline.

This method creates a more accurate snapshot of market behavior, especially during volatile phases. As a result, the indicator adapts to market conditions more effectively, helping traders identify real consolidation zones, not just average lines distorted by flat bars or noise.

█ How to Use

⚪ Range Detection

Boxes form only when price remains consistently close to the speed-weighted mean.

Helps identify sideways zones, consolidations, and low-volatility structures where price is “charging up.”

⚪ Breakout Confirmation

Once price exits the top or bottom boundary, the box immediately highlights the direction of the break.

Use this signal in conjunction with your own momentum, volume, or trend filters for higher-confidence trades.

█ Settings

Minimum Range Length: Number of candles required for a valid range to form.

Range Width Multiplier: Adjusts the envelope around the weighted average using ATR(2000).

Highlight Box Breaks: Enables real-time coloring of breakouts and breakdowns for immediate visual feedback.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

ATR Circle PlotTitle: ATR Circle Plot

Short Title: ATR Circle Plot

Description:

ATR Circle Plot is a dynamic overlay indicator that visualizes volatility-based levels around the open price of each bar, using the Average True Range (ATR). It plots two customizable levels—Upper and Lower ATR—calculated by multiplying the ATR by a user-defined factor (default: 1.0) and adding/subtracting it from the open price. These levels are displayed as colored circles on the chart, ideal for identifying potential breakout or stop-loss zones. A movable table summarizes the ATR value, Upper Level, and Lower Level with tick precision, and a new toggleable label feature displays these values directly on the chart for quick reference.

Perfect for traders in volatile markets like forex, futures, or stocks, this indicator helps set risk parameters or spot key price levels. Users can adjust the ATR timeframe, length, multiplier, table position, and circle colors to suit their strategy. The optional chart labels enhance usability by overlaying ATR metrics at the latest price levels, reducing the need to check the table during fast-moving markets.

Key Features:

Plots Upper and Lower ATR levels as colored circles around the open price.

Toggleable table (top/bottom, left/right) showing ATR and level values in ticks.

Optional chart labels for ATR, Upper, and Lower levels, toggleable via input.

Customizable ATR length, multiplier, timeframe, and colors for flexibility.

Lightweight and compatible with any chart timeframe.

How to Use:

Add the indicator to your chart and adjust the ATR length, multiplier, and timeframe as needed. Enable/disable the table or labels based on your preference. Use the Upper and Lower ATR levels as dynamic support/resistance or stop-loss guides. For example, place stops beyond the Upper/Lower levels or target breakouts when price crosses them. Combine with trend or momentum indicators for a robust setup.

Note: Leave the ATR Timeframe input empty to use the chart’s timeframe, or specify a higher timeframe (e.g., “D” for daily) for broader volatility context. Ensure your chart’s tick size aligns with the asset for accurate table values.

Tags: ATR, volatility, support resistance, stop loss, table, labels, breakout

Category: Volatility

Extreme Zone Volume ProfileExtreme Zone Volume Profile (EZVP) is a high-resolution, percentile-based volume profile tool designed for intuitive market structure analysis. Unlike standard profiles, EZVP emphasizes extreme zones — highlighting potential value rejection or accumulation areas using user-defined percentile thresholds.

Key Features:

Custom Lookback: Profiles volume over a defined number of bars (no rolling memory creep).

Zoned Percentiles: Segment volume by zones:

Zone B = extreme tails (e.g. 2.5% for one wing of ~2 Standard Deviations)

Zone A = outer wings (e.g. 14% for one wing of ~1 Standard Deviations)

Center = remaining bulk of traded volume

Rightward-Growing Bars: Clean, forward-facing display — avoids clutter in historical areas.

Colored Volume Bars: Each zone gets a distinct tone, helping spot high-interest levels fast.

Optional Lines: Toggle POC, Median, Mean, and zone boundary lines for cleaner setups.

This is built for clarity and control — a great fit for traders who want a visually expressive profile without overcomplication. Tweak the zoning percentages to match your strategy or instrument volatility.

TBMC CloudsTBMC Clouds translates the Triple Banded Momentum Cloud (TBMC) into a normalized, non-overlay format, plotting the relationship between your base, trend, and signal moving averages in units of standard deviations. This reveals how far each element diverges from its context — not just in price, but in volatility-adjusted terms.

Trend Cloud: (Trend MA − Base MA) / stdev of Base

Signal Cloud: (Signal MA − Trend MA) / stdev of Trend

Close Line: (Price − Signal MA) / stdev of Signal

Each component is normalized by its own timeframe’s standard deviation, making this chart ideal for comparing momentum intensity and trend distance across multiple horizons. Horizontal bands at configurable thresholds (e.g., ±1, ±2, ±3 stdev) act as reference levels for extension, mean reversion, or volatility breakout logic.

Momentum BandsMomentum Bands indicator-->technical tool that measures the rate of price change and surrounds this momentum with adaptive bands to highlight overbought and oversold zones. Unlike Bollinger Bands, which track price, these bands track momentum itself, offering a unique view of market strength and exhaustion points. At its core, it features a blue momentum line that calculates the rate of change over a set period, an upper red band marking dynamic resistance created by adding standard deviations to the momentum average, a lower green band marking dynamic support by subtracting standard deviations, and a gray middle line representing the average of momentum as a central anchor. When the momentum line touches or moves beyond the upper red band, it often signals that the market may be overbought and a pullback or reversal could follow; traders might lock in profits or watch for short setups. Conversely, when it drops below the lower green band, it can suggest an oversold market primed for a bounce, prompting traders to look for buying opportunities. If momentum remains between the bands, it typically indicates balanced conditions where waiting for stronger signals at the extremes is wise. The indicator can be used in contrarian strategies—buying near the lower band and selling near the upper—or in trend-following setups by waiting for momentum to return toward the centerline before entering trades. For stronger confirmation, traders often combine it with volume spikes, support and resistance analysis, or other trend tools, and it’s useful to check multiple timeframes to spot consistent patterns. Recommended settings vary: short-term traders might use a 7–10 period momentum with 14-period bands; medium-term traders might keep the default 14-period momentum and 20-period bands; while long-term analysis might use 21-period momentum and 50-period bands. Visually, background colors help spot extremes: red for strong overbought, green for strong oversold, and no color for normal markets, alongside reference lines at 70, 30, and 0 to guide traditional overbought, oversold, and neutral zones. Typical bullish signals include momentum rebounding from the lower band, crossing back above the middle after being oversold, or showing divergence where price makes new lows but momentum doesn’t. Bearish signals might appear when momentum hits the upper band and weakens, drops below the middle after being overbought, or price makes new highs while momentum fails to follow. The indicator tends to work best in mean-reverting or sideways markets rather than strong trends, where overbought and oversold conditions tend to repeat.