Squeeze with DojiThis script indicates Bollinger band squeeze into Keltner channels to identify the contraction of price and Doji candle formation, potentially leading up to the momentum expansion in price.

Add your preferable volume or price indicators on top of this volatility contraction indicator.

Feel free to use and share your feedback.

Volatility

DAO - Directional ATR OscillatorDAO - Directional ATR Oscillator. it combines trenddirection and strength by simply splitting the Average True Range in both directions over an oscilators zeroline with two MAs to make it easier to spot the overall trenddirection together with momentum and strength but it also works great for spotting divergences and possible trendreversals early. have fun with this everything indicator !

ATR HUDThis script displays the Average True Range value for your chart's timeframe and displays it in a small tidy table. ATR is a valuable indicator for position sizing, stop placement, profit expectancy and other trade planning considerations. With this script you can keep the current ATR value visible without taking up much precious window space. You can select your preferred smoothing method, lookback period, and window position in the settings. Enjoy!

TMAD Algo Supply DemandThis Pine Script identifies supply and demand zones using volume profile analysis between pivot points or a fixed look-back period. It dynamically highlights these zones with color-coded boxes based on whether price is currently above (bullish) or below (bearish) each zone.

Liquidity Trap Zones [PhenLabs]📊 Liquidity Trap Zones

Version: PineScript™ v6

📌 Description

The goal of the Liquidity Trap Zones indicator is to try and help traders identify areas where market liquidity appears abundant but is actually thin or artificial, helping traders avoid potential fake outs and false breakouts. This advanced indicator analyzes the relationship between price wicks and volume to detect “mirage” zones where large price movements occur on low volume, indicating potential liquidity traps.

By highlighting these deceptive zones on your charts, the indicator helps traders recognize where institutional players might be creating artificial liquidity to trap retail traders. This enables more informed decision-making and better risk management when approaching key price levels.

🚀 Points of Innovation

Mirage Score Algorithm: Proprietary calculation that normalizes wick size relative to volume and average bar size

Dynamic Zone Creation: Automatically generates gradient-filled zones at trap locations with ATR-based sizing

Intelligent Zone Management: Maintains clean charts by limiting displayed zones and auto-updating existing ones

Scale-Invariant Design: Works across all assets and timeframes with intelligent normalization

Real-Time Detection: Identifies trap zones as they form, not after the fact

Volume-Adjusted Analysis: Incorporates tick volume when available for more accurate detection

🔧 Core Components

Mirage Score Calculator: Analyzes the ratio of price wicks to volume, normalized by average bar size

ATR-Based Filter: Ensures only significant price movements are considered for trap zone creation

EMA Smoothing: Reduces noise in the mirage score for clearer signals

Gradient Zone Renderer: Creates visually distinct zones with multiple opacity levels for better visibility

🔥 Key Features

Real-Time Trap Detection: Identifies liquidity mirages as they develop during live trading

Dynamic Zone Sizing: Adjusts zone height based on current market volatility (ATR)

Smart Zone Management: Automatically maintains a clean chart by limiting the number of displayed zones

Customizable Sensitivity: Fine-tune detection parameters for different market conditions

Visual Clarity: Gradient-filled zones with distinct borders for easy identification

Status Line Display: Shows current mirage score and threshold for quick reference

🎨 Visualization

Gradient Trap Zones: Purple gradient boxes with darker centers indicating trap strength

Mirage Score Line: Orange line in status area showing current liquidity quality

Threshold Reference: Gray line showing your configured detection threshold

Extended Zone Display: Zones automatically extend forward as new bars form

📖 Usage Guidelines

Detection Settings

Smoothing Length (EMA) - Default: 10 - Range: 1-50 - Description: Controls responsiveness of mirage score. Lower values make detection more sensitive to recent price action

Mirage Threshold - Default: 5.0 - Range: 0.1-20.0 - Description: Score above this level triggers trap zone creation. Higher values reduce false positives but may miss subtle traps

Filter Settings

ATR Length for Range Filter - Default: 14 - Range: 1-50 - Description: Period for volatility calculation. Standard 14 works well for most timeframes

ATR Multiplier - Default: 1.0 - Range: 0.0-5.0 - Description: Minimum bar range as multiple of ATR. Higher values filter out smaller moves

Display Settings

Zone Height Multiplier - Default: 0.5 - Range: 0.1-2.0 - Description: Controls trap zone height relative to ATR. Adjust for visual preference

Max Trap Zones - Default: 5 - Range: 1-20 - Description: Maximum zones displayed before oldest are removed. Balance clarity vs. history

✅ Best Use Cases

Identifying potential fakeout levels before entering trades

Confirming support/resistance quality by checking for liquidity traps

Avoiding stop-loss placement in trap zones where sweeps are likely

Timing entries after trap zones are cleared

Scalping opportunities when price approaches known trap zones

⚠️ Limitations

Requires volume data - less effective on instruments without reliable volume

May generate false signals during news events or genuine volume spikes

Not a standalone system - combine with price action and other indicators

Zone creation is based on historical data - future price behavior not guaranteed

💡 What Makes This Unique

First indicator to specifically target liquidity mirages using wick-to-volume analysis

Proprietary normalization ensures consistent performance across all markets

Visual gradient design makes trap zones immediately recognizable

Combines multiple volatility and volume metrics for robust detection

🔬 How It Works

1. Wick Analysis: Calculates upper and lower wicks for each bar. Normalizes by average bar size to ensure scale independence

2. Mirage Score Calculation: Divides total wick size by volume to identify thin liquidity. Applies EMA smoothing to reduce noise. Scales result for optimal visibility

3. Zone Creation: Triggers when smoothed score crosses threshold. Creates gradient boxes centered on trap bar. Sizes zones based on current ATR for market-appropriate scaling

💡 Note: Liquidity Trap Zones works best when combined with traditional support/resistance analysis and volume profile indicators. The zones highlight areas of deceptive liquidity but should not be the sole factor in trading decisions. Always use proper risk management and confirm signals with price action.

Fear Volatility Gate [by Oberlunar]The Fear Volatility Gate by Oberlunar is a filter designed to enhance operational prudence by leveraging volatility-based risk indices. Its architecture is grounded in the empirical observation that sudden shifts in implied volatility often precede instability across financial markets. By dynamically interpreting signals from globally recognized "fear indices", such as the VIX, the indicator aims to identify periods of elevated systemic uncertainty and, accordingly, restrict or flag potential trade entries.

The rationale behind the Fear Volatility Gate is rooted in the understanding that implied volatility represents a forward-looking estimate of market risk. When volatility indices rise sharply, it reflects increased demand for options and a broader perception of uncertainty. In such contexts, price movements can become less predictable, more erratic, and often decoupled from technical structures. Rather than relying on price alone, this filter provides an external perspective—derived from derivative markets—on whether current conditions justify caution.

The indicator operates in two primary modes: single-source and composite . In the single-source configuration, a user-defined volatility index is monitored individually. In composite mode, the filter can synthesize input from multiple indices simultaneously, offering a more comprehensive macro-risk assessment. The filtering logic is adaptable, allowing signals to be combined using inclusive (ANY), strict (ALL), or majority consensus logic. This allows the trader to tailor sensitivity based on the operational context or asset class.

The indices available for selection cover a broad spectrum of market sectors. In the equity domain, the filter supports the CBOE Volatility Index ( CBOE:VIX VIX) for the S&P 500, the Nasdaq-100 Volatility Index ( CBOE:VXN VXN), the Russell 2000 Volatility Index ( CBOEFTSE:RVX RVX), and the Dow Jones Volatility Index ( CBOE:VXD VXD). For commodities, it integrates the Crude Oil Volatility Index ( CBOE:OVX ), the Gold Volatility Index ( CBOE:GVZ ), and the Silver Volatility Index ( CBOE:VXSLV ). From the fixed income perspective, it includes the ICE Bank of America MOVE Index ( OKX:MOVEUSD ), the Volatility Index for the TLT ETF ( CBOE:VXTLT VXTLT), and the 5-Year Treasury Yield Index ( CBOE:FVX.P FVX). Within the cryptocurrency space, it incorporates the Bitcoin Volmex Implied Volatility Index ( VOLMEX:BVIV BVIV), the Ethereum Volmex Implied Volatility Index ( VOLMEX:EVIV EVIV), the Deribit Bitcoin Volatility Index ( DERIBIT:DVOL DVOL), and the Deribit Ethereum Volatility Index ( DERIBIT:ETHDVOL ETHDVOL). Additionally, the user may define a custom instrument for specialized tracking.

To determine whether market conditions are considered high-risk, the indicator supports three modes of evaluation.

The moving average cross mode compares a fast Hull Moving Average to a slower one, triggering a signal when short-term volatility exceeds long-term expectations.

The Z-score mode standardizes current volatility relative to historical mean and standard deviation, identifying significant deviations that may indicate abnormal market stress.

The percentile mode ranks the current value against a historical distribution, providing a relative perspective particularly useful when dealing with non-normal or skewed distributions.

When at least one selected index meets the condition defined by the chosen mode, and if the filtering logic confirms it, the indicator can mark the trading environment as “blocked”. This status is visually highlighted through background color changes and symbolic markers on the chart. An optional tabular interface provides detailed diagnostics, including raw values, fast-slow MA comparison, Z-scores, percentile levels, and binary risk status for each active index.

The Fear Volatility Gate is not a predictive tool in itself but rather a dynamic constraint layer that reinforces discipline under conditions of macro instability. It is particularly valuable when trading systems are exposed to highly leveraged or short-duration strategies, where market noise and sentiment can temporarily override structural price behavior. By synchronizing trading signals with volatility regimes, the filter promotes a more cautious, informed approach to decision-making.

This approach does not assume that all volatility spikes are harmful or that market corrections are imminent. Rather, it acknowledges that periods of elevated implied volatility statistically coincide with increased execution risk, slippage, and spread widening, all of which may erode the profitability of even the most technically accurate setups.

Therefore, the Fear Volatility Gate acts as a protective mechanism.

Oberlunar 👁️⭐

Ultimate ATR ProUltimate ATR Pro - Professional Volatility Analysis Tool

Unlock Market Turning Points with Precision Volatility Analysis

Key Features

1. Advanced ATR Calculation Engine

4 MA Types: RMA (Wilder's), SMA, EMA, WMA

Customizable Period: Adjust ATR length (default: 14)

Multi-Timeframe Compatible: Works on all chart intervals

2. Smart Volatility Extremum Detection

Low Volatility Signals: Identifies ATR contraction periods

High Volatility Signals: Detects ATR expansion phases

Custom Lookback Period: Set detection window (10-500 bars)

3. Professional Divergence System

Bullish Divergence: Price ↑ while ATR ↓ (trend continuation signal)

Bearish Divergence: Price ↓ while ATR ↑ (trend acceleration signal)

Visual Connection Lines: Dotted lines highlight price-ATR relationships

4. Visual Extreme Value Lines (NEW!)

Lowest ATR Line: Customizable dotted line showing minimum volatility level

Highest ATR Line: Customizable dotted line marking maximum volatility level

Dynamic Positioning: Auto-updates with each new bar

5. Complete Customization System

Full Color Control:

Signal markers (low/high volatility)

Divergence labels

ATR line

Extreme value lines

Background highlights

Toggle Features: Enable/disable any visual element

6. Intelligent Alert System

Dual Alert Types:

Volatility Extremes (Low/High ATR)

Divergence Signals (Bullish/Bearish)

Smart Cooldown: Prevent alert fatigue with adjustable cooldown period

Visual Alert Tags: Color-coded notifications at chart top

7. Professional Dashboard

Real-time status monitoring:

Current volatility state

Cooldown timers

Extreme ATR values

Divergence detection status

Color-coded for instant recognition

How Traders Benefit

Strategic Applications

markdown

复制

| SIGNAL | MARKET CONDITION | TRADING IMPLICATION |

|-----------------------|---------------------------|------------------------------------|

| Low Volatility | Contraction/Consolidation | Prepare for breakout strategies |

| High Volatility | Expansion/Climax | Watch for reversals or pauses |

| Bullish Divergence | Price↑ ATR↓ | Trend continuation opportunity |

| Bearish Divergence | Price↓ ATR↑ | Trend acceleration warning |

| Lowest ATR Line Break | Volatility breakout | Confirm directional movement |

Risk Management Tools

ATR-Based Position Sizing: Use extreme values to calculate optimal trade size

Dynamic Stop Loss: Adjust stops based on current volatility regime

Volatility Filtering: Avoid trading during uncertain high-volatility periods

Setup Recommendations

Parameter Guide

pine

复制

length: 14 // Standard ATR period

lookback: 50 // Optimal for swing trading

cooldownPeriod: 14// Balanced alert frequency

minLineColor: #00C853 // Bright green for low volatility

maxLineColor: #FF3D00 // Bright red for high volatility

Professional Configurations

Day Trading: Lookback=20-30, Cooldown=5-10

Swing Trading: Lookback=50-100, Cooldown=10-20

Position Trading: Lookback=100-200, Cooldown=20-50

Why Choose Ultimate ATR Pro?

"Transforms complex volatility analysis into clear, actionable visual cues - the essential tool for breakout traders and risk managers alike."

Install Now To:

Spot consolidation before big moves

Identify exhaustion at trend extremes

Automate volatility-based position sizing

Receive instant alerts at critical volatility turns

Gain professional-grade insights into market dynamics

Master market rhythms with the most advanced ATR analysis tool on TradingView!

Compatibility: Works flawlessly across stocks, forex, crypto, and commodities on all timeframes.

Version: 2.0 (Enhanced with Extreme Value Lines)

Category: Volatility Analysis | Risk Management | Professional Trading

ADX + Supertrend Persistent Entry Logicbuy condition should match below condition below

ADX DI plus should above of DI minuse

Supertrend should be bullish

ADX should be above 25

Price should not have order block resistance

Exit from buy when supertrend change trend

Sell condition should match below condition below

ADX DI plus should below of DI minuse

Supertrend should be bearish

ADX should be above 25

Price should not have order block support

Exit from Sell when supertrend change trend

ATR % of yesterday close with SMA (Bull/Bear colored)This script visualizes the Average True Range (ATR) as a percentage of a user-selected price point for a quick view of volatility.

ATR % values are plotted as a color-coded histogram. Bullish days (close > prior close) paint the bar green; bearish days (close < prior close) paint it red; unchanged days are gray.

Two simple moving average (SMA) overlays to reveal volatility trends.

Variables:

Histogram bars represent ATR as a % of one of:

- Previous Close (default option)

- Previous Open

- Today Close

- Today Open

Two SMA lines (default: blue for 20-period, orange for 5-period) shown on ATR % for trend/range regime tracking.

Optionally display the ATR % in continuous line (yellow)—hidden by default.

If you find it helpful, feel free to share any feedback and how you incorporate it into your trading strategy with the community!

Fractal Flow BandsFractal Flow Bands

A high-precision trend-following system combining HalfTrend logic with ALMA smoothing — built for clarity, speed, and smart alerts.

🔷 What is Fractal Flow Bands?

Fractal Flow Bands merges the best of both worlds:

HalfTrend for accurate trend detection

ALMA (Arnaud Legoux Moving Average) for smooth, low-lag confirmation

This unique synergy delivers clean, non-repainting Buy/Sell signals, filtering out market noise and keeping your chart crystal clear.

🔍 How It Works

Blue HalfTrend Line + Green ALMA Crossover → BUY

Red HalfTrend Line + Red ALMA Crossover → SELL

You get only ONE alert per trend change, eliminating spammy notifications. Perfect for swing traders, scalpers, and trend followers alike.

⚙️ Core Features

✅ Dual Confirmation Engine

ALMA must confirm HalfTrend — no single-line tricks here.

✅ One Alert per Trend Shift

Clean signals, no noise, no repeats.

✅ Visual Clarity

Color-coded trends. No channels, ribbons, or clutter.

✅ Customizable Settings

Tune HalfTrend amplitude and ALMA smoothness to your strategy.

🎯 Best For

Swing traders wanting confirmation before entries

Scalpers needing fast, accurate signal flow

Anyone who hates messy charts but loves sharp decisions

🛠 Settings Explained

Setting Description

HT Amplitude Controls HalfTrend sensitivity

ALMA Length / Offset / Sigma Adjusts the smoothness of ALMA

Source Choose price source (Close, Open, etc.)

Display Toggles Enable/disable arrows and ribbons

Colors Fully customizable trend color schemes

✅ Built-in Alerts — So you never miss a signal again.

⚡ Lag-free performance — Works on multiple timeframes.

📈 Real strategy-ready code — Not just another repainting overlay.

Debit Spread POMDP‑Inspired StrategyComprehensive Strategy for TradingView-Based Call and Put Debit Spread Options Using POMDP for Signal Generation

Debit spreads limit risk to the net premium paid while capping potential profit, ideal for moderate price predictions.

Pine Script in TradingView enables custom indicator integration and strategy automation for options trading.

Partially Observable Markov Decision Processes (POMDPs) optimize decision-making under market uncertainty by modeling states, actions, and observations.

Training a POMDP policy involves defining market states, actions, and observations from technical indicators, then simulating and refining the policy.

Automating the strategy via agents or TradingView alerts can execute trades when conditions align with the POMDP-generated signals.

Weighted Multi-Mode Oscillator [BackQuant]Weighted Multi‑Mode Oscillator

1. What Is It?

The Weighted Multi‑Mode Oscillator (WMMO) is a next‑generation momentum tool that turns a dynamically‑weighted moving average into a 0‑100 bounded oscillator.

It lets you decide how each bar is weighted (by volume, volatility, momentum or a hybrid blend) and how the result is normalised (Percentile, Z‑Score or Min‑Max).

The outcome is a self‑adapting gauge that delivers crystal‑clear overbought / oversold zones, divergence clues and regime shifts on any market or timeframe.

2. How It Works

• Dynamic Weight Engine

▪ Volume – emphasises bars with exceptional participation.

▪ Volatility – inverse ATR weighting filters noisy spikes.

▪ Momentum – amplifies strong directional ROC bursts.

▪ Hybrid – equal‑weight blend of the three dimensions.

• Multi‑Mode Smoothing

Choose from 8 MA types (EMA, DEMA, HMA, LINREG, TEMA, RMA, SMA, WMA) plus a secondary smoothing factor to fine‑tune lag vs. responsiveness.

• Normalization Suite

▪ Percentile – rank vs. recent history (context aware).

▪ Z‑Score – standard deviations from mean (statistical extremes).

▪ Min‑Max – scale between rolling high/low (trend friendly).

3. Reading the Oscillator

Zone Default Level Interpretation

Bull > 80 Acceleration; momentum buyers in control

Neutral 20 – 80 Consolidation / no edge

Bear < 20 Exhaustion; sellers dominate

Gradient line/area automatically shades from bright green (strong bull) to deep red (strong bear).

Optional bar‑painting colours price bars the same way for rapid chart scanning.

4. Typical Use‑Cases

Trend Confirmation – Set Weight = Hybrid, Smoothing = EMA. Enter pullbacks only when WMMO > 50 and rising.

Mean Reversion – Weight = Volatility, reduce upper / lower bands to 70 / 30 and fade extremes.

Volume Pulse – Intraday futures: Weight = Volume to catch participation surges before breakout candles.

Divergence Spotting – Compare price highs/lows to WMMO peaks for early reversal clues.

5. Inputs & Styling

Calculation: Source, MA Length, MA Type, Smoothing

Weighting: Volume period & factor, Volatility length, Momentum period

Normalisation: Method, Look‑back, Upper / Lower thresholds

Display: Gradient fills, Threshold lines, Bar‑colouring toggle, Line width & colours

All thresholds, colours and fills are fully customisable inside the settings panel.

6. Built‑In Alerts

WMMO Long – oscillator crosses up through upper threshold.

WMMO Short – oscillator crosses down through lower threshold.

Attach them once and receive push / e‑mail notifications the moment momentum flips.

7. Best Practices

Percentile mode is self‑adaptive and works well across assets; Z‑Score excels in ranges; Min‑Max shines in persistent trends.

Very short MA lengths (< 10) may produce jitter; compensate with higher “Smoothing” or longer look‑backs.

Pair WMMO with structure‑based tools (S/R, trend lines) for higher‑probability trade confluence.

Disclaimer

This script is provided for educational purposes only. It is not financial advice. Always back‑test thoroughly and manage risk before trading live capital.

Ultimate ATR Extreme DetectorUltimate ATR Extreme Detector

Professional Volatility Analysis Tool for Strategic Trading

Discover Market Turning Points with Precision

Key Features

Smart Extremum Detection: Identifies when ATR reaches its highest or lowest point in your specified lookback period

Quad Visual Alert System:

▲ Green bottom triangles for low volatility signals

▼ Red top triangles for high volatility signals

Background color highlighting for instant state recognition

Status panel showing current volatility extremes

Dual Alert Modes:

TradingView native alerts ("ATR Low/High Signal")

Visual chart alerts with period details (e.g., "Alert: ATR Low (50 bars)")

4 Calculation Methods: RMA (Wilder's), SMA, EMA, and WMA

Fully Customizable:

Adjustable ATR period (default: 14)

Variable lookback window (default: 50)

Toggle features on/off via intuitive input settings

How It Works

The indicator scans volatility extremes using proprietary logic:

Calculates True Range using selected method (RMA/SMA/EMA/WMA)

Compares current ATR value against historical data

Flags critical moments when:

Volatility contracts to N-period lows (prepare for breakouts)

Volatility expands to N-period highs (watch for trend exhaustion)

Strategic Applications

markdown

复制

| SIGNAL | MARKET CONDITION | TRADING IMPLICATION |

|------------------|-----------------------|--------------------------------|

| Low Volatility | Contraction/Consolidation | Anticipate breakout moves |

| High Volatility | Expansion/Climax | Prepare for reversals or pauses |

Position Sizing: Use ATR values to determine optimal stop distances

Entry Timing: Combine with price action at key support/resistance

Risk Management: Adjust stops dynamically based on volatility regime

Optimization Guide

Day Trading: Short lookback (20-30 periods)

Swing Trading: Medium lookback (50-100 periods)

Position Trading: Long lookback (100-200 periods)

Volatility Analysis: Compare multiple timeframes simultaneously

Professional Setup Recommendations

Combine with:

Breakout Confirmation: Volume spikes, chart patterns

Reversal Signals: RSI divergence, candlestick reversals

Volatility Filters: Bollinger Band contraction, Keltner Channel breakout

Compatibility: Works flawlessly across FX, stocks, crypto, and commodities on all timeframes.

Why Traders Choose This Indicator

"Transforms complex volatility analysis into clear, actionable visual cues – the essential tool for breakout traders and risk managers alike."

Install Now to:

Spot consolidation before big moves

Identify exhaustion at trend extremes

Automate volatility-based position sizing

Receive instant alerts at critical volatility turns

Master market rhythms with professional-grade volatility intelligence!

Qossai Stock Info### Qossai Stock Info Indicator

This indicator provides a concise overlay of essential stock information directly on your chart, presented in a clean, organized table. Designed for quick glances, it helps traders and investors stay informed about key fundamental and volatility metrics of the currently viewed symbol.

**Key Features:**

* **Symbol/Ticker Display:** Clearly shows the ticker of the asset you are currently viewing.

* **Dynamic Market Capitalization (Market Cap):** Automatically calculates and displays the market capitalization in a readable format (Millions, Billions, or Trillions), providing instant insight into the company's size.

* **Average True Range (ATR) as Percentage:** Shows the 14-day Average True Range (a measure of volatility) as a percentage of the closing price, helping you gauge the typical price movement. The ATR period is customizable.

* **Earnings Countdown:** Keep track of upcoming events with a precise countdown displaying the number of days remaining until the next earnings announcement. This feature can be toggled on or off via the indicator's settings.

* **Clean Table Format:** All information is presented neatly in a table with a subtle black background, ensuring readability without cluttering your main chart view.

**How to Use:**

Simply add the "Qossai Stock Info" indicator to your chart. You can adjust the ATR length and toggle the earnings countdown visibility from the indicator's settings.

**Purpose:**

This tool aims to simplify access to critical stock data, empowering users to make quicker, more informed decisions by having vital information readily available on their screen.

---

[Top] LHAMA Consolidation DetectorIntroducing the Low-High Adaptive Moving Average (LHAMA 🦙), a powerful tool designed to help traders visually distinguish between trending and consolidating market phases. Unlike traditional moving averages that can produce false signals in choppy markets, the LHAMA is engineered to flatten out during periods of consolidation and become more responsive when a clear trend emerges.

This indicator's primary function is to act as a "Consolidation Detector." When the LHAMA line goes flat and adopts its "Flat Color," it serves as a clear visual cue that the market is range-bound. Conversely, when the line begins to slope and changes to its Bullish or Bearish color, it signals a potential breakout or the start of a new trend.

How It Works

The LHAMA is a type of adaptive moving average. Its adaptiveness is derived from a unique calculation that measures market "trendiness." It does this by tracking whether new highs or new lows are being made within a specified lookback period.

In a Trending Market: When the price consistently makes new highs or lows, the indicator's responsiveness increases, causing the LHAMA to track the price much more closely and responsively.

In a Consolidating Market: When the price is range-bound and fails to make new highs or lows, the responsiveness decreases significantly. This causes the LHAMA to flatten out and become less sensitive to minor price fluctuations, effectively filtering out market noise.

Key Features

Adaptive Calculation: The core engine of the indicator, which automatically adjusts its smoothing based on trend strength.

Slope-Based Coloring: The line's color dynamically changes based on its slope, providing an at-a-glance view of market conditions: bullish, bearish, or flat.

Multi-Line & Multi-Timeframe (MTF): You can enable up to six fully customizable LHAMA lines. Each line can be configured with its own length, colors, and can even be set to a different timeframe, allowing for comprehensive multi-timeframe analysis on a single chart.

Volatility Clouds: Each LHAMA can display an optional cloud around it. The cloud's width is based on your choice of either the Average True Range (ATR) or Standard Deviation (StdDev), offering a visual representation of volatility.

Volume Weighting: An option to incorporate volume into the adaptive calculation, making the LHAMA even more responsive during high-volume price movements.

How to Use

Identify Consolidation: The primary use case. A flat and consistently colored LHAMA line is a strong indication of a sideways or consolidating market. This can help traders avoid taking trend-following trades in choppy conditions.

Confirm Trends: When the LHAMA begins to slope upwards or downwards and changes to its trend color, it can be used to confirm the direction and strength of a new trend. The steeper the slope, the stronger the momentum, and more solid the directional color.

Dynamic Support & Resistance: Like other moving averages, the LHAMA can act as a dynamic level of support in an uptrend or resistance in a downtrend. The optional cloud can further define these zones.

Multi-MA Ribbon Strategy: By enabling multiple LHAMAs with different lengths (e.g., Fibonacci sequence like 14, 21, 34, 55), you can create a ribbon. The expansion of the ribbon indicates a strong trend, while its contraction signals a weakening trend or consolidation.

Settings Explained

Enable 🦙 Line: A simple checkbox to turn each of the six LHAMA lines on or off.

Length: The lookback period for the LHAMA calculation. Shorter lengths are more responsive, while longer lengths are smoother.

Timeframe: Set a specific timeframe for each LHAMA. Leave blank to use the chart's current timeframe.

Volume Weight: If checked, adds volume weighting to make the LHAMA more responsive to high-volume moves.

Colors (Bullish, Bearish, Flat): Customize the colors for each market state. To only see the line during consolidation, set the Bullish and Bearish colors to 100% transparency. To hide the line during consolidation, set the Flat color to 100% transparency.

Color Sensitivity: This is a crucial setting. Because price scales (tick sizes) vary widely between symbols, this setting allows you to adjust the sensitivity of the slope detection. A lower value requires a steeper slope to trigger a trend color, while a higher value is more sensitive.

Recommended settings are provided in the input tooltip as a starting point:

$5 Tick: 0.25 Sensitivity

$1 Tick: 0.75 Sensitivity

$0.25 Tick: 3 Sensitivity

$0.01 Tick: 50 Sensitivity

$0.005 Tick: 100 Sensitivity

Cloud Settings:

Show Cloud: Toggles the visibility of the volatility cloud around the LHAMA.

Width Based On: Choose between "ATR" or "StdDev" to calculate the cloud's width.

Cloud Length & Width: Set the lookback period and multiplier for the ATR/StdDev calculation to control the size of the cloud.

Risk Context + Position SizingWhat This Indicator Does (And Doesn't Do)

This is NOT a buy/sell signal indicator. Instead, it's a risk management tool that helps you understand two critical things:

How volatile the market is right now (compared to recent history)

How much you should risk on your next trade based on that volatility

The Core Problem It Solves

Imagine you always risk the same amount on every trade - say $100. But sometimes the market is calm and predictable, other times it's wild and unpredictable. This indicator says: "Hey, the market is going crazy right now - maybe only risk $70 instead of your usual $100."

How It Works

Measures Market "Nervousness"

Uses ATR (Average True Range) to measure how much prices typically move each day

Compares today's volatility to the past 100 days

Shows you a percentile (0-100%) - higher = more volatile

Categorizes Risk Environment

LOW (green): Market is calm, you can size up slightly

NORMAL: Standard conditions, use your normal position size

HIGH (red): Market is jumpy, reduce your position size

EXTREME (dark red): Market is in chaos, significantly reduce size

Important Disclaimers

This doesn't predict price direction - it only measures current market stress

You still need a trading strategy - this just helps you size it properly

Past volatility doesn't guarantee future volatility

Always combine with proper stop losses and risk management

Indian Stocks Daily, Weekly, Monthly, All-Time High-LowDaily high, low, last week high low, current week high low, current month high low.

ATR Dynamic Stop (Table + Plot + ATR %)📊 This script displays dynamic stop levels based on ATR, designed for active traders.

Features:

- Shows long and short stop levels (price ± ATR × multiplier).

- Displays values as a floating table on the top-right corner.

- Optional plot lines directly on the chart.

- Option to calculate based on realtime price or last close.

- Displays the ATR value both in price units and as a percentage of the selected price.

- Fully customizable table: text size, text color, background color.

Inputs:

- ATR Multiplier and Length.

- Show/hide stop lines on the chart.

- Select price source (realtime or last close).

- Table appearance options.

Ideal for:

- Traders who want a clear visual stop guide.

- Combining volatility with risk management.

Fat Tails Analyzer🧠 Fat Tails Analyzer — Analysis of Anomalous ("Fat-Tailed") Movements

📌 Description

Fat Tails Analyzer is a tool for analyzing "fat tails" in the distribution of returns. Unlike normal distribution, financial markets often exhibit frequent extreme movements. This indicator identifies and visualizes such events by analyzing logarithmic returns, deviations from normal distribution, and excess kurtosis.

🔬 Methodology

Logarithmic returns (ln(Close / Close )) are calculated for accurate aggregation and symmetry.

Moving average and standard deviation of returns are computed over a specified period.

"Fat-tailed" events are identified when returns exceed μ ± k·σ, where k is user-defined.

Normal distribution bands (±2σ) and kurtosis (a measure of tail "heaviness") are displayed for clarity.

📊 What It Displays

📈 Histogram of Returns: Green for positive, red for negative.

🟣 Fat Tail Threshold Lines: Marking extreme events.

⚪ Silver Normal Distribution Bands: ±2σ boundaries.

🔵 Kurtosis Line: If enabled.

📋 Table with Key Metrics: Mean, σ, kurtosis.

⚙️ Parameters

Lookback Period (Bars): Analysis period (default: 252).

Fat Tail Threshold (Std Devs): Deviation for extreme events (k, default: 2.5).

Show Normal Distribution Bands: Toggle ±2σ boundaries.

Show Kurtosis: Enable kurtosis analysis mode.

📌 Interpretation

Excess Kurtosis > 0: More extreme events than predicted by normal distribution.

Returns beyond fat-tail thresholds: Potential signals of panic, shock, or exceptional news.

Consistently high kurtosis: Unstable or speculative asset.

🧪 Applications

📉 Identify extreme risks in assets (especially cryptocurrencies and derivatives).

🧠 Study market behavior and dispersion.

🛡 Support risk analysis, stop-loss settings, and systemic risk assessment.

🔎 Compare assets by the "normality" of their behavior.

🧭 Live Metrics Table

Displayed in the bottom-right corner:

Mean return

Standard deviation

Excess kurtosis (color-coded by value)

🧠 Good to Know

Normal distribution has kurtosis = 0.

> 0: "Fat tails" (more extreme values).

< 0: "Thin tails" (values close to the mean).

Volume Peak LineA fully configurable “Volume Peak Line” indicator that draws a horizontal threshold at the highest volume over the last X candles (default 5).

Custom lookback (X volume candles)

Optional alert when current volume exceeds that peak

Separate up/down volume bars (green/red) or hide them to use your own volume overlays

Use it to spot surges in trading activity on any timeframe—ideal for intraday or swing setups where a barn-burner volume bar can signal a reversal or the start of a new trend.

TREV Candles - Range-Based Trend ReversalTREV Candles - Range-Based Trend Reversal Chart Implementation

What is a Trend Reversal (TREV) Chart?

A Trend Reversal chart, also known as a Point & Figure chart variation, is a unique charting method that focuses on price movement thresholds rather than time intervals. Unlike traditional candlestick charts where each candle represents a fixed time period, TREV candles form only when price moves by predefined amounts in ticks.

TREV charts eliminate time-based noise and focus purely on significant price movements, making them ideal for identifying genuine trend changes and continuation patterns.

How TREV Candles Work

This indicator implements true TREV logic with two critical thresholds:

Trend Size: The number of ticks price must move in the current direction to form a trend continuation candle

Reversal Size: The number of ticks price must move against the current direction to form a reversal candle and change the overall trend direction

Key TREV Rules Enforced:

Direction Changes Only Through Reversals: You cannot go from bullish trend directly to bearish trend - a reversal candle must occur first

Threshold-Based Formation: Candles form only when price thresholds are breached, not on time

Logical Wick Placement: Wicks only appear on the "open" side of candles where price temporarily moved against the formation direction

Multiple Candles Per Bar: When price moves significantly, several TREV candles can form within a single time-based bar

Four Distinct Candle Types

Bullish Trend (Green): Continues upward movement when trend threshold is hit

Bearish Trend (Red): Continues downward movement when trend threshold is hit

Bullish Reversal (Blue): Changes from bearish to bullish direction when reversal threshold is breached

Bearish Reversal (Orange): Changes from bullish to bearish direction when reversal threshold is breached

Practical Trading Applications

Trend Identification: Clear visual representation of when trends are continuing vs. reversing

Noise Reduction: Filters out insignificant price movements that don't meet threshold requirements

Support/Resistance: TREV levels often act as significant support and resistance zones

Breakout Confirmation: When price forms multiple trend candles in succession, it confirms strong directional movement

Reversal Signals: Reversal candles provide early warning of potential trend changes

Technical Implementation Features

Intelligent Price Path Processing: Analyzes the assumed price path within each bar (Low→High→Close for bullish bars, High→Low→Close for bearish bars)

Automatic Tick Size Detection: Works with any instrument by automatically detecting the correct tick size

Manual Override Option: Allows manual tick size specification for custom analysis

Impossible Scenario Prevention: Built-in logic prevents impossible wick configurations and direction changes

PineScript Optimization: Efficient state management and drawing limits handling for smooth performance

Comprehensive Styling Options

Each of the four candle types offers complete visual customization:

Body Colors: Independent color settings for each candle type's body

Border Colors: Separate border color customization

Border Styles: Choose from solid, dashed, or dotted borders

Wick Colors: Individual wick color settings for each candle type

Default Color Scheme:

🟢 Bullish Trend: Green body and wicks

🔵 Bullish Reversal: Blue body and wicks

🔴 Bearish Trend: Red body and wicks

🟠 Bearish Reversal: Orange body and wicks

Configuration Guidelines

Trend Size: Larger values create fewer, more significant trend candles. Smaller values increase sensitivity

Reversal Size: Should typically be smaller than trend size. Controls how easily the trend direction can change

Tick Size: Use "auto" for most instruments. Manual override useful for custom point values or backtesting

Ideal Use Cases

Swing Trading: Identify major trend changes and continuation patterns

Scalping: Use smaller thresholds to catch quick reversals and momentum shifts

Position Trading: Use larger thresholds to filter noise and focus on major trend moves

Multi-Timeframe Analysis: Compare TREV patterns across different threshold settings

Support/Resistance Trading: TREV close levels often become significant price zones

Why This Implementation is Superior

True TREV Logic: Enforces proper trend reversal rules that many implementations ignore

No Impossible Scenarios: Prevents wicks on both sides of candles and impossible direction changes

Professional Visualization: Clean, customizable appearance suitable for serious analysis

Performance Optimized: Handles large datasets without lag or drawing limit issues

Educational Value: Helps traders understand the difference between time-based and threshold-based charting

Perfect for traders who want to see beyond time-based noise and focus on what price is actually doing - moving in significant, measurable amounts that matter for trading decisions.

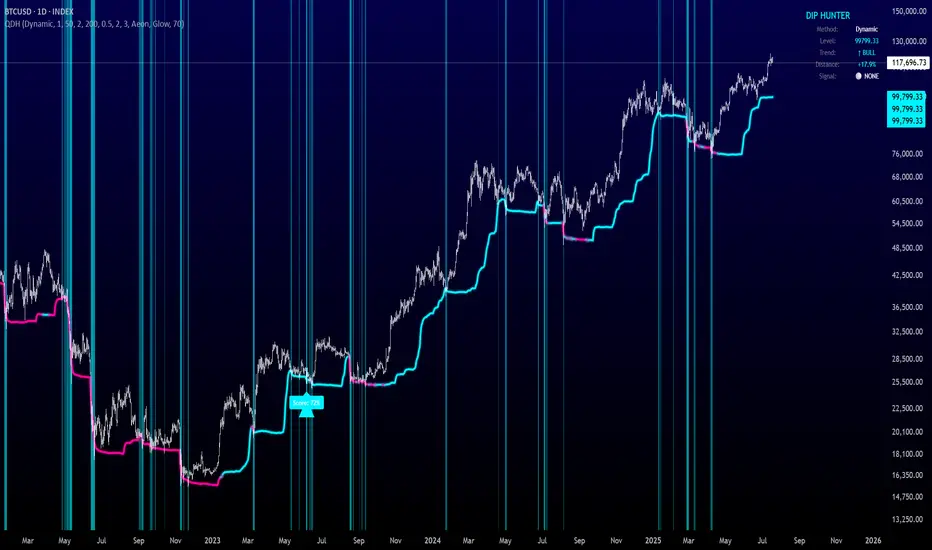

Quantum Dip Hunter | AlphaNattQuantum Dip Hunter | AlphaNatt

🎯 Overview

The Quantum Dip Hunter is an advanced technical indicator designed to identify high-probability buying opportunities when price temporarily dips below dynamic support levels. Unlike simple oversold indicators, this system uses a sophisticated quality scoring algorithm to filter out low-quality dips and highlight only the best entry points.

"Buy the dip" - but only the right dips. Not all dips are created equal.

⚡ Key Features

5 Detection Methods: Choose from Dynamic, Fibonacci, Volatility, Volume Profile, or Hybrid modes

Quality Scoring System: Each dip is scored from 0-100% based on multiple factors

Smart Filtering: Only signals above your quality threshold are displayed

Visual Effects: Glow, Pulse, and Wave animations for the support line

Risk Management: Automatic stop-loss and take-profit calculations

Real-time Statistics: Live dashboard showing current market conditions

📊 How It Works

The indicator calculates a dynamic support line using your selected method

When price dips below this line, it evaluates the dip quality

Quality score is calculated based on: trend alignment (30%), volume (20%), RSI (20%), momentum (15%), and dip depth (15%)

If the score exceeds your minimum threshold, a buy signal arrow appears

Stop-loss and take-profit levels are automatically calculated and displayed

🚀 Detection Methods Explained

Dynamic Support

Adapts to recent price action

Best for: Trending markets

Uses ATR-adjusted lowest points

Fibonacci Support

Based on 61.8% and 78.6% retracement levels

Best for: Pullbacks in strong trends

Automatically switches between fib levels

Volatility Support

Uses Bollinger Band methodology

Best for: Range-bound markets

Adapts to changing volatility

Volume Profile Support

Finds high-volume price levels

Best for: Identifying institutional support

Updates dynamically as volume accumulates

Hybrid Mode

Combines all methods for maximum accuracy

Best for: All market conditions

Takes the most conservative support level

⚙️ Key Settings

Dip Detection Engine

Detection Method: Choose your preferred support calculation

Sensitivity: Higher = more sensitive to price movements (0.5-3.0)

Lookback Period: How far back to analyze (20-200 bars)

Dip Depth %: Minimum dip size to consider (0.5-10%)

Quality Filters

Trend Filter: Only buy dips in uptrends when enabled

Minimum Dip Score: Quality threshold for signals (0-100%)

Trend Strength: Required trend score when filter is on

📈 Trading Strategies

Conservative Approach

Use Dynamic method with Trend Filter ON

Set minimum score to 80%

Risk:Reward ratio of 2:1 or higher

Best for: Swing trading

Aggressive Approach

Use Hybrid method with Trend Filter OFF

Set minimum score to 60%

Risk:Reward ratio of 1:1

Best for: Day trading

Scalping Setup

Use Volatility method

Set sensitivity to 2.0+

Focus on Target 1 only

Best for: Quick trades

🎨 Visual Customization

Color Themes:

Neon: Bright cyan/magenta for dark backgrounds

Ocean: Cool blues and teals

Solar: Warm yellows and oranges

Matrix: Classic green terminal look

Gradient: Smooth color transitions

Line Styles:

Solid: Clean, simple line

Glow: Adds depth with glow effect

Pulse: Animated breathing effect

Wave: Oscillating wave pattern

💡 Pro Tips

Start with the Trend Filter ON to avoid catching falling knives

Higher quality scores (80%+) have better win rates but fewer signals

Use Volume Profile method near major support/resistance levels

Combine with your favorite momentum indicator for confirmation

The pulse animation can help draw attention to key levels

⚠️ Important Notes

This indicator identifies potential entries, not guaranteed profits

Always use proper risk management

Works best on liquid instruments with good volume

Backtest your settings before live trading

Not financial advice - use at your own risk

📊 Statistics Panel

The live statistics panel shows:

Current detection method

Support level value

Trend direction

Distance from support

Current signal status

🤝 Support

Created by AlphaNatt

For questions or suggestions, please comment below!

Happy dip hunting! 🎯

Not financial advice, always do your own research

Trimmed ATR🧠 **Brief Description**:

Trimmed ATR is a modified volatility indicator that removes extreme values from the ATR calculation. This makes it more reliable for analyzing market conditions and filters out "noise" spikes. It is particularly useful for setting stop-losses and in strategies sensitive to false volatility.

🧾 **How Does Trimmed ATR Work?**

📌 For each bar:

- True Range (TR) is calculated.

- A sliding window of the last N TR values (where N = length) is stored.

- The TR list is sorted, and trimPercent % is cut off from each side:

- The smallest and largest values are removed.

- The remaining values are averaged → Trimmed ATR.

🔍 **Why Is This Important?**

Regular ATR can be distorted by outliers:

- A single spike can sharply inflate the ATR.

- This creates a false impression of market volatility.

🎯 Trimmed ATR solves this by eliminating the impact of anomalies, providing a more stable and accurate volatility measure.

📈 **What Does It Mean If Trimmed ATR Is Higher or Lower Than Regular ATR?**

🔵 **Trimmed ATR is lower than ATR** — this is normal:

- There are isolated TR spikes (high volatility on 1–2 bars).

- ATR increases, including these outliers.

- Trimmed ATR discards them → reflects the true average market background.

🧠 This is the most common case, indicating: a spike occurred, but the market is generally calm.

🟠 **Trimmed ATR is higher than ATR** — a rare but important signal:

- There were artificially low TR values (very small movements).

- ATR becomes too low.

- Trimmed ATR discards these "quiet" periods → provides a more realistic volatility estimate.

⚠️ This may indicate:

- Hidden pressure.

- Preparation for a breakout from a tight range.

- Underestimated volatility.

💡 **Applications**:

- **Trailing Stop**: Trimmed ATR helps avoid stop triggers due to noise.

- **Trend Filter**: Better reflects the "true" market dynamics.

- **Strategy Backtesting**: Eliminates distortions in volatility calculations.