VIX-Price Covariance MonitorThe VIX-Price Covariance Monitor is a statistical tool that measures the evolving relationship between a security's price and volatility indices such as the VIX (or VVIX).

It can give indication of potential market reversal, as typically, volatility and the VIX increase before markets turn red,

This indicator calculates the Pearson correlation coefficient using the formula:

ρ(X,Y) = cov(X,Y) / (σₓ × σᵧ)

Where:

ρ is the correlation coefficient

cov(X,Y) is the covariance between price and the volatility index

σₓ and σᵧ are the standard deviations of price and the volatility index

Enjoy!

Features

Dual Correlation Periods: Analyze both short-term and long-term correlation trends simultaneously

Adaptive Color Coding: Correlation strength is visually represented through color intensity

Market Condition Assessment: Automatic interpretation of correlation values into actionable market insights

Leading/Lagging Analysis: Optional time-shift analysis to detect predictive relationships

Detailed Information Panel: Real-time statistics including current correlation values, historical averages, and trading implications

Interpretation

Positive Correlation (Red): Typically bearish for price, as rising VIX correlates with falling markets. This is what traders should be looking for.

Negative Correlation (Green): Typically bullish for price, as falling VIX correlates with rising markets

How to use it

Apply the indicator to any chart to see its correlation with the default VIX index

Adjust the correlation length to match your trading timeframe (shorter for day trading, longer for swing trading)

Enable the secondary correlation period to compare different timeframes simultaneously

For advanced analysis, enable the Leading/Lagging feature to detect if VIX changes precede or follow price movements

Use the information panel to quickly assess the current market condition and potential trading implications

Volatilityindicator

EVaR Indicator and Position SizingThe Problem:

Financial markets consistently show "fat-tailed" distributions where extreme events occur with higher frequency than predicted by normal distributions (Gaussian or even log-normal). These fat tails manifest in sudden price crashes, volatility spikes, and black swan events that traditional risk measures like volatility can underestimate. Standard deviation and conventional VaR calculations assume normally distributed returns, leaving traders vulnerable to severe drawdowns during market stress.

Cryptocurrencies and volatile instruments display particularly pronounced fat-tailed behavior, with extreme moves occurring 5-10 times more frequently than normal distribution models would predict. This reality demands a more sophisticated approach to risk measurement and position sizing.

The Solution: Entropic Value at Risk (EVAR)

EVaR addresses these limitations by incorporating principles from statistical mechanics and information theory through Tsallis entropy. This advanced approach captures the non-linear dependencies and power-law distributions characteristic of real financial markets.

Entropy is more adaptive than standard deviations and volatility measures.

I was inspired to create this indicator after reading the paper " The End of Mean-Variance? Tsallis Entropy Revolutionises Portfolio Optimisation in Cryptocurrencies " by by Sana Gaied Chortane and Kamel Naoui.

Key advantages of EVAR over traditional risk measures:

Superior tail risk capture: More accurately quantifies the probability of extreme market moves

Adaptability to market regimes: Self-calibrates to changing volatility environments

Non-parametric flexibility: Makes less assumptions about the underlying return distribution

Forward-looking risk assessment: Better anticipates potential market changes (just look at the charts :)

Mathematically, EVAR is defined as:

EVAR_α(X) = inf_{z>0} {z * log(1/α * M_X(1/z))}

Where the moment-generating function is calculated using q-exponentials rather than conventional exponentials, allowing precise modeling of fat-tailed behavior.

Technical Implementation

This indicator implements EVAR through a q-exponential approach from Tsallis statistics:

Returns Calculation: Price returns are calculated over the lookback period

Moment Generating Function: Approximated using q-exponentials to account for fat tails

EVAR Computation: Derived from the MGF and confidence parameter

Normalization: Scaled to for intuitive visualization

Position Sizing: Inversely modulated based on normalized EVAR

The q-parameter controls tail sensitivity—higher values (1.5-2.0) increase the weighting of extreme events in the calculation, making the model more conservative during potentially turbulent conditions.

Indicator Components

1. EVAR Risk Visualization

Dynamic EVAR Plot: Color-coded from red to green normalized risk measurement (0-1)

Risk Thresholds: Reference lines at 0.3, 0.5, and 0.7 delineating risk zones

2. Position Sizing Matrix

Risk Assessment: Current risk level and raw EVAR value

Position Recommendations: Percentage allocation, dollar value, and quantity

Stop Parameters: Mathematically derived stop price with percentage distance

Drawdown Projection: Maximum theoretical loss if stop is triggered

Interpretation and Application

The normalized EVAR reading provides a probabilistic risk assessment:

< 0.3: Low risk environment with minimal tail concerns

0.3-0.5: Moderate risk with standard tail behavior

0.5-0.7: Elevated risk with increased probability of significant moves

> 0.7: High risk environment with substantial tail risk present

Position sizing is automatically calculated using an inverse relationship to EVAR, contracting during high-risk periods and expanding during low-risk conditions. This is a counter-cyclical approach that ensures consistent risk exposure across varying market regimes, especially when the market is hyped or overheated.

Parameter Optimization

For optimal risk assessment across market conditions:

Lookback Period: Determines the historical window for risk calculation

Q Parameter: Controls tail sensitivity (higher values increase conservatism)

Confidence Level: Sets the statistical threshold for risk assessment

For cryptocurrencies and highly volatile instruments, a q-parameter between 1.5-2.0 typically provides the most accurate risk assessment because it helps capturing the fat-tailed behavior characteristic of these markets. You can also increase the q-parameter for more conservative approaches.

Practical Applications

Adaptive Risk Management: Quantify and respond to changing tail risk conditions

Volatility-Normalized Positioning: Maintain consistent exposure across market regimes

Black Swan Detection: Early identification of potential extreme market conditions

Portfolio Construction: Apply consistent risk-based sizing across diverse instruments

This indicator is my own approach to entropy-based risk measures as an alterative to volatility and standard deviations and it helps with fat-tailed markets.

Enjoy!

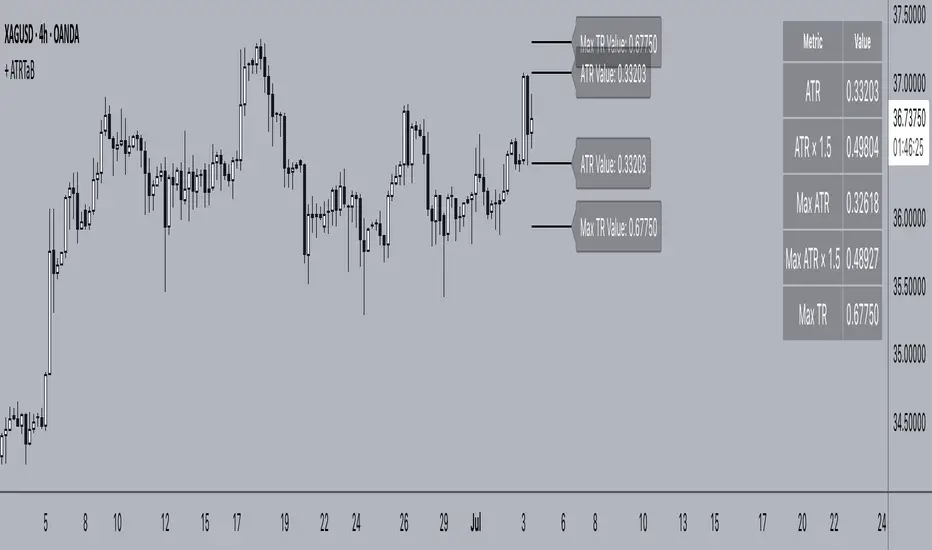

+ ATR Table and BracketsHi, all. I'm back with a new indicator—one I firmly believe could be one of the most valuable indicators you keep in your indicator toolshed—based around true range.

This is a simple, streamlined indicator utilizing true range and average true range that will help any trader with stoploss, trailing stoploss, and take-profit placement—things that I know many traders use average true range for. It could also be useful for trade entries as well, depending on the trader's style.

Typically, most traders (or at least what I've seen recommended across websites, video tutorials on YouTube, etc.) are taught to simply take the ATR number and use that, and possibly some sort of multiplier, as your stoploss and take-profit. This is fine, but I thought that it might be possible to dive a bit deeper into these values. Because an average is a combination of values, some higher, some lower, and we often see ATR spikes during periods of high volatility, I thought wouldn't it be useful to know what value those ATR spikes are, and how do they relate to the ATR? Then I thought to myself, well, what about the most volatile candle within that ATR (the candle with the greatest true range)? Couldn't knowing that value be useful to a trader? So then the idea of a table displaying these values, along with the ATR and the ATR times some multiplier number, would be a useful, simple way to display this information. That's what we have here.

The table is made up of two columns, one with the name of the metric being measured, and the other with its value. That's it. Simple.

As nice as this was, I thought an additional, great, and perhaps better, way to visualize this information would be in the form of brackets extending from the current bar. These are simply lines/labels plotted at the price values of the ATR, ATR times X, highest ATR, highest ATR times X, and highest TR value. These labels supply the actual values of the ATR, etc., but may also display the price if you should choose (both of these values are toggleable in the 'Inputs' section of the indicator.). Additionally, you can choose to display none of these labels, or all five if you wish (leaves the chart a bit cluttered, as shown in the image below), though I suspect you'll determine your preferences for which information you'd like to see and which not.

Chart with all five lines/labels displayed. I adjusted the ATRX value to 3 just to make the screenshot as legible as possible. Default is set to 1.5. As you can see, the label doesn't show the multiplier number, but the table does.

Here's a screenshot of the labels showing the price in addition to the value of the ATR, set to "Previous Closing Price," (see next paragraph for what that means) and highest TR. Personally, I don't see the value in the displaying the price, but I thought some people might want that. It's not available in the table as of now, but perhaps if I get enough requests for it I will add it.

That's basically it, but one last detail I need to go over is the dropdown box labeled "Bar Value ATR Levels are Oriented To." Firstly, this has no effect on Highest ATR, Highest ATRX, and Highest TR levels. Those are based on the ATR up to the last closed candle, meaning they aren't including the value of the currently open candle (this would be useless). However, knowing that different traders trade different ways it seemed to me prudent to allow for traders to select which opening or closing value the trader wishes to have the ATR brackets based on. For example, as someone who has consumed much No Nonsense Forex content I know that traders are urged to enter their trades in the last fifteen minutes of the trading day because the ATR is unlikely to change significantly in that period (ATR being the centerpiece of NNFX money management), so one of three selections here is to plot the brackets based on the ATR's inclusion of this value (this of course means the brackets will move while the candle is still open). The other options are to set the brackets to the current opening price, or the previous closing price. Depending on what you're trading many times these prices are virtually identical, but sometimes price gaps (stocks in particular), so, wanting your brackets placed relative to the previous close as opposed to the current open might be preferable for some traders.

And that's it. I really hope you guys like this indicator. I haven't seen anything closely similar to it on TradingView, and I think it will be something you all will find incredibly handy.

Please enjoy!

Volatility Zones (STDEV %)This indicator displays the relative volatility of an asset as a percentage, based on the standard deviation of price over a custom length.

🔍 Key features:

• Uses standard deviation (%) to reflect recent price volatility

• Classifies volatility into three zones:

Low volatility (≤2%) — highlighted in blue

Medium volatility (2–4%) — highlighted in orange

High volatility (>4%) — highlighted in red

• Supports visual background shading and colored line output

• Works on any timeframe and asset

📊 This tool is useful for identifying low-risk entry zones, periods of expansion or contraction in price behavior, and dynamic market regime changes.

You can adjust the STDEV length to suit your strategy or timeframe. Best used in combination with your entry logic or trend filters.

EWMA Volatility EstimatorThis script calculates EWMA Volatility (Exponentially Weighted Moving Average Volatility).

Commonly used model in financial risk management.

It estimates recent price volatility by applying more weight to the most recent returns, capturing volatility clustering while remaining responsive to fast market shifts.

The method uses a decay factor (λ) of 0.94, the standard value used in models like RiskMetrics, and converts the variance estimate into annualized volatility in percentage terms.

This is not a forecasting tool. It’s an estimator that reflects the magnitude of recent price moves in a statistically robust way.

It can be helpful for:

Understanding regime shifts in market behavior

Designing position sizing rules based on recent volatility

Filtering entries during high or low volatility phases

How It Works

Computes log returns of the closing price.

Squares the returns to get a proxy for variance.

Applies an exponential moving average to the squared returns using an equivalent EMA period based on λ = 0.94.

Converts the result to volatility by taking the square root and scaling to a percentage.

Key Characteristics

Backward-looking estimator

Reacts faster than standard rolling-window volatility

Smooths noise while still being sensitive to recent spikes

This script is educational and informational. It is not financial advice or a guarantee of performance. Always test any tool as part of a broader strategy before using it in live markets.

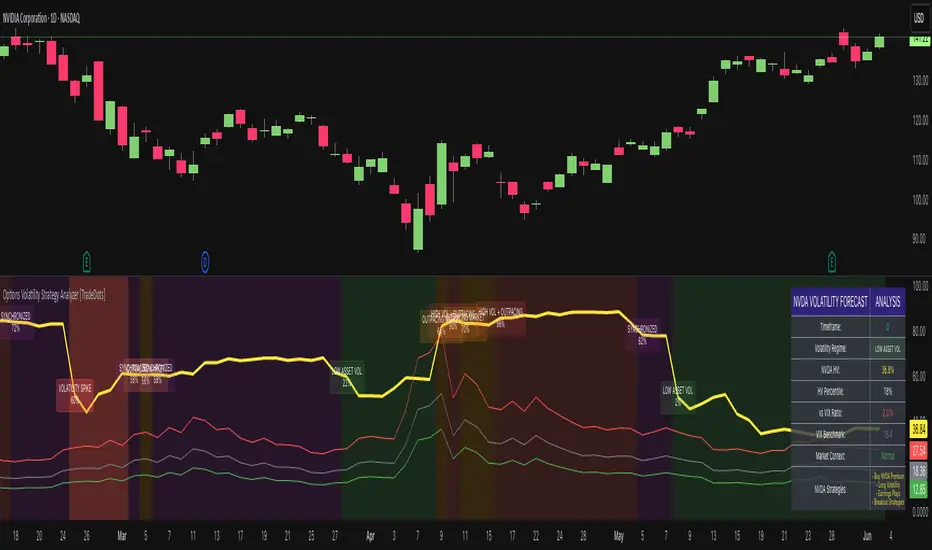

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Exponential Trend [AlgoAlpha]OVERVIEW

This script plots an adaptive exponential trend system that initiates from a dynamic anchor and accelerates based on time and direction. Unlike standard moving averages or trailing stops, the trend line here doesn't follow price directly—it expands exponentially from a pivot determined by a modified Supertrend logic. The result is a non-linear trend curve that starts at a specific price level and accelerates outward, allowing traders to visually assess trend strength, persistence, and early-stage reversal points through both base and volatility-adjusted extensions.

CONCEPTS

This indicator builds on the idea that trend-following tools often need dynamic, non-static expansion to reflect real market behavior. It uses a simplified Supertrend mechanism to define directional context and anchor levels, then applies an exponential growth function to simulate trend acceleration over time. The exponential growth is unidirectional and resets only when the direction flips, preserving trend memory. This method helps avoid whipsaws and adds time-weighted confirmation to trends. A volatility buffer—derived from ATR and modifiable by a width multiplier—adds a second layer to indicate zones of risk around the main trend path.

FEATURES

Exponential Trend Logic : Once a directional anchor is set, the base trend line accelerates using an exponential formula tied to elapsed bars, making the trend stronger the longer it persists.

Volatility-Adjusted Extension : A secondary band is plotted above or below the base trend line, widened by ATR to visualize volatility zones, act as soft stop regions or as a better entry point (Dynamic Support/Resistance).

Color-Coded Visualization : Clear green/red base and extension lines with shaded fills indicate trend direction and confidence levels.

Signal Markers & Alerts : Triangle markers indicate confirmed trend reversals. Built-in alerts notify users of bullish or bearish direction changes in real-time.

USAGE

Use this script to identify strong trends early, visually measure their momentum over time, and determine safe areas for entries or exits. Start by adjusting the *Exponential Rate* to control how quickly the trend expands—the higher the rate, the more aggressive the curve. The *Initial Distance* sets how far the anchor band is placed from price initially, helping filter out noise. Increase the *Width Multiplier* to widen the volatility zone for more conservative entries or exits. When the price crosses above or below the base line, a new trend is assumed and the exponential projection restarts from the new anchor. The base trend and its extension both shift over time, but only reset on a confirmed reversal. This makes the tool especially useful for momentum continuation setups or trailing stop logic in trending markets.

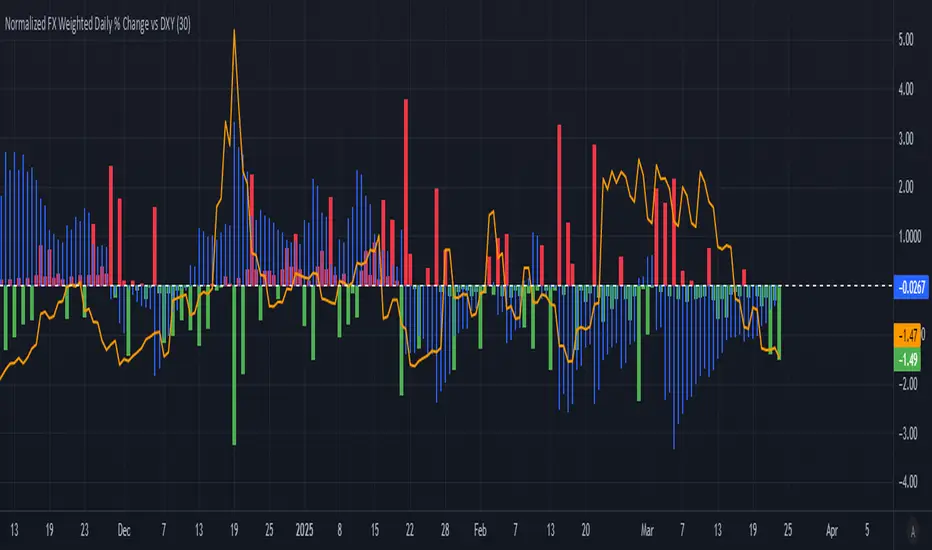

Normalized FX Weighted Daily % Change vs DXYThis indicator tracks international liquidity flows by measuring the USD’s relative strength against major currencies—EUR, CNY, JPY, GBP, and CAD. It calculates the weighted percentage change of each pair over a specified interval. A positive reading means the USD is weakening (liquidity flowing out of the US), while a negative reading indicates the USD is strengthening (liquidity flowing in). Additionally, the indicator incorporates the DXY index and VIX, with all components normalized using Z-scores for clear, comparable insights into market dynamics.

Hourly Volatility Explorer📊 Hourly Volatility Explorer: Master The Market's Pulse

Unlock the hidden rhythms of price action with this sophisticated volatility analysis tool. The Hourly Volatility Explorer reveals the most potent trading hours across multiple time zones, giving you a strategic edge in timing your trades.

🌟 Key Features:

⏰ Multi-Timezone Analysis

• GMT (UTC+0)

• EST (UTC-5) - New York

• BST (UTC+1) - London

• JST (UTC+9) - Tokyo

• AEST (UTC+10) - Sydney

Perfect for tracking major market sessions and their overlaps!

📈 Dynamic Visualization

• Color-gradient hourly bars for instant pattern recognition

• Real-time volatility comparison

• Interactive data table with comprehensive statistics

• Automatic highlighting of peak volatility periods

🎯 Strategic Applications:

Day Trading:

• Identify optimal trading windows

• Avoid low-liquidity periods

• Capitalize on session overlaps

• Fine-tune entry/exit timing

Risk Management:

• Set appropriate stop losses based on hourly volatility

• Adjust position sizes for different market hours

• Optimize risk-reward ratios

• Plan around high-impact hours

Global Market Analysis:

• Track volatility across all major sessions

• Spot institutional trading patterns

• Identify quiet vs. active periods

• Monitor 24/7 market dynamics

💡 Perfect For:

• Forex traders navigating global sessions

• Crypto traders in 24/7 markets

• Day traders optimizing execution times

• Algorithmic traders fine-tuning strategies

• Risk managers calibrating exposure

📊 Advanced Features:

• Rolling 3-month analysis for reliable patterns

• Precise pip movement calculations

• Sample size tracking for statistical validity

• Real-time current hour comparison

• Color-coded visual system for instant insights

⚡ Pro Trading Tips:

• Use during major session overlaps for maximum opportunity

• Compare patterns across different instruments

• Combine with volume analysis for deeper insights

• Track seasonal variations in hourly patterns

• Build trading schedules around peak hours

🎓 Educational Value:

• Understand market microstructure

• Learn global market dynamics

• Master timezone relationships

• Develop timing intuition

🛠️ Customization:

• Adjustable lookback period

• Flexible pip multiplier

• Multiple timezone options

• Visual preference settings

Whether you're scalping the 1-minute chart or managing longer-term positions, the Hourly Volatility Explorer provides the precise timing intelligence needed for today's global markets.

Transform your trading schedule from guesswork to science. Know exactly when markets move, why they move, and how to position yourself for maximum opportunity.

#TechnicalAnalysis #Trading #Volatility #MarketTiming #DayTrading #Forex #Crypto #TradingView #PineScript #MarketAnalysis #TradingStrategy #RiskManagement #GlobalMarkets #FinancialMarkets #TradingTools #MarketStructure #PriceAction #Scalping #SwingTrading #AlgoTrading

BTC-USDT Liquidity Trend [Ajit Pandit]his script helps traders visualize trend direction and identify liquidity zones where price might react due to past pivot levels. The color-coded candles and extended pivot lines make it easier to spot support/resistance levels and potential breakout points.

Key Features:

1. Trend Detection Using EMA

Uses two EMA calculations to determine the trend:

emaValue: Standard EMA based on length1

correction: Adjusted price movement relative to EMA

Trend: Another EMA of the corrected value

Determines bullish (signalUp) and bearish (signalDn) signals when Trend crosses emaValue.

2. Candlestick Coloring Based on Trend

Candlesticks are colored:

Uptrend → Blue (up color)

Downtrend → Pink (dn color)

Neutral → No color

3. Liquidity Zones (Pivot Highs & Lows)

Identifies pivot highs and lows using a customizable pivot length.

Draws liquidity lines:

High pivot lines (Blue, adjustable width)

Low pivot lines (Pink, adjustable width)

Extends lines indefinitely until price breaks above/below the level.

Removes broken pivot levels dynamically.

Trendchange Zones Indicator | iSolani

Spotting Reversals Before They Happen: The iSolani Trendshift System

Where RSI Meets Smart Volume Analysis - Your Visual Guide to Market Turns

Core Methodology

RSI-Powered Zones

Identifies critical levels using:

14-period RSI (default) with 70/30 thresholds

Semi-transparent boxes marking overbought (red) and oversold (green) territories

Zone persistence until RSI returns to neutral range

Dynamic Level Tracking

Plots evolving support/resistance using:

Pivot highs/lows with 15-bar lookback (default)

Auto-extending lines that adapt to new price extremes

Volume-Confirmed Breakouts

Flags significant moves with:

5/10 EMA volume oscillator

20% volume threshold (default) for confirmation

Technical Innovation

Three-Layer Confirmation

Unique combination of:

Classic RSI extremes

Price structure through pivot points

Volume-fueled momentum shifts

Adaptive Visualization

Zones maintain historical context at 33% transparency

Dynamic lines extend indefinitely until invalidated

Discreet labels for breakout events

System Workflow

Calculates RSI values in real-time

Draws colored zones when RSI crosses 70/30

Marks pivot points every 15 bars (default)

Updates support/resistance lines on new pivots

Triggers alerts when price breaks levels with volume confirmation

Standard Configuration

RSI Settings : 14-period length

Pivot Detection : 15-bar left/right lookback

Visuals : 33% transparency zones with thin borders

Volume Threshold : 20% oscillator difference

Alerts : Breakout signals with "B" labels

This system transforms the classic RSI into a spatial analysis tool - not just showing when markets are overextended, but where they're likely to reverse. The dynamic lines act as moving barriers that adapt to market structure, while the volume filter ensures only high-conviction breaks get flagged. By layering momentum, price action, and volume dynamics, it creates a multi-spectrum view of potential trend changes.

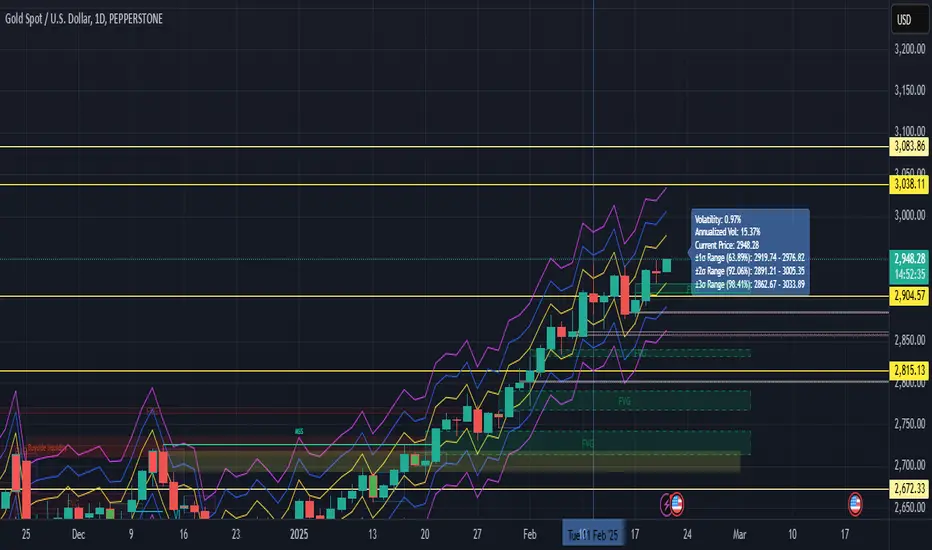

Volatility with Sigma BandsOverview

The Volatility Analysis with Sigma Bands indicator is a powerful and flexible tool designed for traders who want to gain deeper insights into market price fluctuations. It calculates historical volatility within a user-defined time range and displays ±1σ, ±2σ, and ±3σ standard deviation bands, helping traders identify potential support, resistance levels, and extreme price behaviors.

Key Features

Multiple Volatility Band Displays:

±1σ Range (Yellow line): Covers approximately 68% of price fluctuations.

±2σ Range (Blue line): Covers approximately 95% of price fluctuations.

±3σ Range (Fuchsia line): Covers approximately 99% of price fluctuations.

Dynamic Probability Mode:

Toggle between standard normal distribution probabilities (68.2%, 95.4%, 99.7%) and actual historical probability calculations, allowing for more accurate analysis tailored to varying market conditions.

Highly Customizable Label Display:

The label shows:

Real-time volatility

Annualized volatility

Current price

Price ranges for each σ level

Users can adjust the label’s position and horizontal offset to prevent it from overlapping key price areas.

Real-Time Calculation & Visualization:

The indicator updates in real-time based on the selected time range and current market data, making it suitable for day trading, swing trading, and long-term trend analysis.

Use Cases

Risk Management:

Understand the distribution probabilities of price within different standard deviation bands to set more effective stop-loss and take-profit levels.

Trend Confirmation:

Determine trend strength or spot potential reversals by observing whether the price breaks above or below ±1σ or ±2σ ranges.

Market Sentiment Analysis:

Price movement beyond the ±3σ range often indicates extreme market sentiment, providing potential reversal opportunities.

Backtesting and Historical Analysis:

Utilize the customizable time range feature to backtest volatility during various periods, providing valuable insights for strategy refinement.

The Volatility Analysis with Sigma Bands indicator is an essential tool for traders seeking to understand market volatility patterns. Whether you're a day trader looking for precise entry and exit points or a long-term investor analyzing market behavior, this indicator provides deep insights into volatility dynamics, helping you make more confident trading decisions.

Position resetThe "Position Reset" indicator

The Position Reset indicator is a sophisticated technical analysis tool designed to identify possible entry points into short positions based on an analysis of market volatility and the behavior of various groups of bidders. The main purpose of this indicator is to provide traders with information about the current state of the market and help them decide whether to open short positions depending on the level of volatility and the mood of the main players.

The main components of the indicator:

1. Parameters for the RSI (Relative Strength Index):

The indicator uses two sets of parameters to calculate the RSI: one for bankers ("Banker"), the other for hot money ("Hot Money").

RSI for Bankers:

RSIBaseBanker: The baseline for calculating bankers' RSI. The default value is 50.

RSIPeriodBanker: The period for calculating the RSI for bankers. The default period is 14.

RSI for hot money:

RSIBaseHotMoney: The baseline for calculating the RSI of hot money. The default value is 30.

RSIPeriodHotMoney: The period for calculating the RSI for hot money. The default period is 21.

These parameters allow you to adjust the sensitivity of the indicator to the actions of different groups of market participants.

2. Sensitivity:

Sensitivity determines how strongly changes in the RSI will affect the final result of calculations. It is configured separately for bankers and hot money:

SensitivityBanker: Sensitivity for bankers' RSI. It is set to 2.0 by default.

SensitivityHotMoney: Sensitivity for hot money RSI. It is set to 1.0 by default.

Changing these parameters allows you to adapt the indicator to different market conditions and trader preferences.

3. Volatility Analysis:

Volatility is measured based on the length of the period, which is set by the volLength parameter. The default length is 30 candles. The indicator calculates the difference between the highest and lowest value for the specified period and divides this difference by the lowest value, thus obtaining the volatility coefficient.

Based on this coefficient, four levels of volatility are distinguished.:

Extreme volatility: The coefficient is greater than or equal to 0.25.

High volatility: The coefficient ranges from 0.125 to 0.2499.

Normal volatility: The coefficient ranges from 0.05 to 0.1249.

Low volatility: The coefficient is less than 0.0499.

Each level of volatility has its own significance for making decisions about entering a position.

4. Calculation functions:

The indicator uses several functions to process the RSI and volatility data.:

rsi_function: This function applies to every type of RSI (bankers and hot money). It adjusts the RSI value according to the set sensitivity and baseline, limiting the range of values from 0 to 20.

Moving Averages: Simple moving averages (SMA), exponential moving averages (EMA), and weighted moving averages (RMA) are used to smooth fluctuations. They are applied to different time intervals to obtain the average values of the RSI.

Thus, the indicator creates a comprehensive picture of market behavior, taking into account both short-term and long-term dynamics.

5. Bearish signals:

Bearish signals are considered situations when the RSI crosses certain levels simultaneously with a drop in indicators for both types of market participants (bankers and hot money).:

The bankers' RSI crossing is below the level of 8.5.

The current hot money RSI is less than 18.

The moving averages for banks and hot money are below their signal lines.

The RSI values for bankers are less than 5.

These conditions indicate a possible beginning of a downtrend.

6. Signal generation:

Depending on the current level of volatility and the presence of bearish signals, the indicator generates three types of signals:

Orange circle: Extremely high volatility and the presence of a bearish signal.

Yellow circle: High volatility and the presence of a bearish signal.

Green circle: Low volatility and the presence of a bearish signal.

These visual markers help the trader to quickly understand what level of risk accompanies each specific signal.

7. Notifications:

The indicator supports the function of sending notifications when one of the three types of signals occurs. The notification contains a brief description of the conditions under which the signal was generated, which allows the trader to respond promptly to a change in the market situation.

Advantages of using the "Position Reset" indicator:

Multi-level analysis: The indicator combines technical analysis (RSI) and volatility assessment, providing a comprehensive view of the current market situation.

Flexibility of settings: The ability to adjust the sensitivity parameters and the RSI baselines allows you to adapt the indicator to any market conditions and personal preferences of the trader.

Clear visualization: The use of colored labels on the chart simplifies the perception of information and helps to quickly identify key points for entering a trade.

Notification support: The notification sending feature makes it much easier to monitor the market, allowing you to respond to important events in time.

Choppiness IndexThis Pine Script v6 indicator calculates the Choppiness Index over a user-defined length and segments it based on user-defined thresholds for choppy and trending market conditions. The indicator allows users to toggle the visibility of choppy, trending, and neutral segments using checkboxes.

Here's how it works:

Inputs: Users can set the length for the Choppiness Index calculation and thresholds for choppy and trending conditions. They can also choose which segments to display.

Choppiness Index Calculation: The script calculates the Choppiness Index using the ATR and the highest-high and lowest-low over the specified length.

Segment Determination: The script determines which segment the current Choppiness Index value falls into based on the thresholds. The color changes exactly at the threshold values.

Dynamic Plotting: The Choppiness Index is plotted with a color that changes based on the segment. The plot is only visible if the segment is "turned on" by the user.

Threshold Lines: Dashed horizontal lines are plotted at the choppy and trending thresholds for reference.

This indicator helps traders visualize market conditions and identify potential transitions between choppy and trending phases, with precise color changes at the threshold values.

RSI Volatility Suppression Zones [BigBeluga]RSI Volatility Suppression Zones is an advanced indicator that identifies periods of suppressed RSI volatility and visualizes these suppression zones on the main chart. It also highlights breakout dynamics, giving traders actionable insights into potential market momentum.

🔵 Key Features:

Detection of Suppression Zones:

Identifies periods where RSI volatility is suppressed and marks these zones on the main price chart.

Breakout Visualization:

When the price breaks above the suppression zone, the box turns aqua, and an upward label is drawn to indicate a bullish breakout.

If the price breaks below the zone, the box turns purple, and a downward label is drawn for a bearish breakout.

Breakouts accompanied by a "+" label represent strong moves caused by short-lived, tight zones, signaling significant momentum.

Wave Labels for Consolidation:

If the suppression zone remains unbroken, a "wave" label is displayed within the gray box, signifying continued price stability within the range.

Gradient Intensity Below RSI:

A gradient strip below the RSI line increases in intensity based on the duration of the suppressed RSI volatility period.

This visual aid helps traders gauge how extended the low volatility phase is.

🔵 Usage:

Identify Breakouts: Use color-coded boxes and labels to detect breakouts and their direction, confirming potential trend continuation or reversals.

Evaluate Market Momentum: Leverage "+" labels for strong breakout signals caused by short suppression phases, indicating significant market moves.

Monitor Price Consolidation: Observe gray boxes and wave labels to understand ongoing consolidation phases.

Analyze RSI Behavior: Utilize the gradient strip to measure the longevity of suppressed volatility phases and anticipate breakout potential.

RSI Volatility Suppression Zones provides a powerful visual representation of RSI volatility suppression, breakout signals, and price consolidation, making it a must-have tool for traders seeking to anticipate market movements effectively.

HV-RV Oscillator by DINVESTORQ(PRABIR DAS)Description:

The HV-RV Oscillator is a powerful tool designed to help traders track and compare two types of volatility measures: Historical Volatility (HV) and Realized Volatility (RV). This indicator is useful for identifying periods of market volatility and can be employed in various trading strategies. It plots both volatility measures on a normalized scale (0 to 100) to allow easy comparison and analysis.

How It Works:

Historical Volatility (HV):

HV is calculated by taking the log returns of the closing prices and finding the standard deviation over a specified period (default is 14 periods).

The value is then annualized assuming 252 trading days in a year.

Realized Volatility (RV):

RV is based on the True Range, which is the maximum of the current high-low range, the difference between the high and the previous close, and the difference between the low and the previous close.

Like HV, the standard deviation of the True Range over a specified period is calculated and annualized.

Normalization:

Both HV and RV values are normalized to a 0-100 scale, making it easy to see their relative magnitude over time.

The highest and lowest values within the period are used to normalize the data, which smooths out short-term volatility spikes.

Smoothing:

The normalized values of both HV and RV are then smoothed using a Simple Moving Average (SMA) to reduce noise and provide a clearer trend.

Crossover Signals:

Buy Signal : When the Normalized HV crosses above the Normalized RV, it indicates that the historical volatility is increasing relative to the realized volatility, which could be interpreted as a buy signal.

Sell Signal : When the Normalized HV crosses below the Normalized RV, it suggests that the historical volatility is decreasing relative to the realized volatility, which could be seen as a sell signal.

Features:

Two Volatility Lines: The blue line represents Normalized HV, and the orange line represents Normalized RV.

Neutral Line: A gray dashed line at the 50 level indicates a neutral state between the two volatility measures.

Buy/Sell Markers: Green upward arrows are shown when the Normalized HV crosses above the Normalized RV, and red downward arrows appear when the Normalized HV crosses below the Normalized RV.

Inputs:

HV Period: The number of periods used to calculate Historical Volatility (default = 14).

RV Period: The number of periods used to calculate Realized Volatility (default = 14).

Smoothing Period: The number of periods used for smoothing the normalized values (default = 3).

How to Use:

This oscillator is designed for traders who want to track the relationship between Historical Volatility and Realized Volatility.

Buy signals occur when HV increases relative to RV, which can indicate increased market movement or potential breakout conditions.

Sell signals occur when RV is greater than HV, signaling reduced volatility or potential trend exhaustion.

Example Use Cases:

Breakout/Trend Strategy: Use the oscillator to identify potential periods of increased volatility (when HV crosses above RV) for breakout trades.

Mean Reversion: Use the oscillator to detect periods of low volatility (when RV crosses above HV) that might signal a return to the mean or consolidation.

This tool can be used on any asset class such as stocks, forex, commodities, or indices to help you make informed decisions based on the comparison of volatility measures.

NOTE: FOR INTRDAY PURPOSE USE 30/7/9 AS SETTING AND FOR DAY TRADE USE 14/7/9

Profitability Visualization with Bid-Ask Spread ApproximationOverview

The " Profitability Visualization with Bid-Ask Spread Approximation " indicator is designed to assist traders in assessing potential profit and loss targets in relation to the current market price or a simulated entry price. It provides flexibility by allowing users to choose between two methods for calculating the offset from the current price:

Bid-Ask Spread Approximation: The indicator attempts to estimate the bid-ask spread by using the highest (high) and lowest (low) prices within a given period (typically the current bar or a user-defined timeframe) as proxies for the ask and bid prices, respectively. This method provides a dynamic offset that adapts to market volatility.

Percentage Offset: Alternatively, users can specify a fixed percentage offset from the current price. This method offers a consistent offset regardless of market conditions.

Key Features

Dual Offset Calculation Methods: Choose between a dynamic bid-ask spread approximation or a fixed percentage offset to tailor the indicator to your trading style and market analysis.

Entry Price Consideration: The indicator can simulate an entry price at the beginning of each trading session (or the first bar on the chart if no sessions are defined). This feature enables a more realistic visualization of potential profit and loss levels based on a hypothetical entry point.

Profit and Loss Targets: When the entry price consideration is enabled, the indicator plots profit target (green) and loss target (red) lines. These lines represent the price levels at which a trade entered at the simulated entry price would achieve a profit or incur a loss equivalent to the calculated offset amount.

Offset Visualization: Regardless of whether the entry price is considered, the indicator always displays upper (aqua) and lower (fuchsia) offset lines. These lines represent the calculated offset levels based on the chosen method (bid-ask approximation or percentage offset).

Customization: Users can adjust the percentage offset, toggle the bid-ask approximation and entry price consideration, and customize the appearance of the lines through the indicator's settings.

Inputs

useBidAskApproximation A boolean (checkbox) input that determines whether to use the bid-ask spread approximation (true) or the percentage offset (false). Default is false.

percentageOffset A float input that allows users to specify the percentage offset to be used when useBidAskApproximation is false. The default value is 0.63.

considerEntryPrice A boolean input that enables the consideration of a simulated entry price for calculating and displaying profit and loss targets. Default is true.

Calculations

Bid-Ask Approximation (if enabled): bidApprox = request.security(syminfo.tickerid, timeframe.period, low) Approximates the bid price using the lowest price (low) of the current period. askApprox = request.security(syminfo.tickerid, timeframe.period, high) Approximates the ask price using the highest price (high) of the current period. spreadApprox = askApprox - bidApprox Calculates the approximate spread.

Offset Amount: offsetAmount = useBidAskApproximation ? spreadApprox / 2 : close * (percentageOffset / 100) Determines the offset amount based on the selected method. If useBidAskApproximation is true, the offset is half of the approximated spread; otherwise, it's the current closing price (close) multiplied by the percentageOffset.

Entry Price (if enabled): var entryPrice = 0.0 Initializes a variable to store the entry price. if considerEntryPrice Checks if entry price consideration is enabled. if barstate.isnew Checks if the current bar is the first bar of a new session. entryPrice := close Sets the entryPrice to the closing price of the first bar of the session.

Profit and Loss Targets (if entry price is considered): profitTarget = entryPrice + offsetAmount Calculates the profit target price level. lossTarget = entryPrice - offsetAmount Calculates the loss target price level.

Plotting

Profit Target Line: Plotted in green (color.green) with a dashed line style (plot.style_linebr) and increased linewidth (linewidth=2) when considerEntryPrice is true.

Loss Target Line: Plotted in red (color.red) with a dashed line style (plot.style_linebr) and increased linewidth (linewidth=2) when considerEntryPrice is true.

Upper Offset Line: Always plotted in aqua (color.aqua) to show the offset level above the current price.

Lower Offset Line: Always plotted in fuchsia (color.fuchsia) to show the offset level below the current price.

Limitations

Approximation: The bid-ask spread approximation is based on high and low prices and may not perfectly reflect the actual bid-ask spread of a specific broker, especially during periods of high volatility or low liquidity.

Simplified Entry: The entry price simulation is basic and assumes entry at the beginning of each session. It does not account for specific entry signals or order types.

No Order Execution: This indicator is purely for visualization and does not execute any trades.

Data Discrepancies: The high and low values used for approximation might not always align with real-time bid and ask prices due to differences in data aggregation and timing between TradingView and various brokers.

Disclaimer

This indicator is for educational and informational purposes only and should not be considered financial advice. Trading involves substantial risk, and past performance is not indicative of future results. Always conduct thorough research and consider your own risk tolerance before making any trading decisions. It is recommended to combine this indicator with other technical analysis tools and a well-defined trading strategy.

Adaptive Volatility-Scaled Oscillator [AVSO] (Zeiierman)█ Overview

The Adaptive Volatility-Scaled Oscillator (AVSO) is a dynamic trading indicator that measures and visualizes volatility-adjusted market behavior. By scaling various metrics (such as volume, price changes, standard deviation, ATR, and Yang-Zhang volatility) and applying adaptive smoothing, AVSO helps traders identify market conditions where volatility deviates significantly from the norm.

This indicator uses standardized scaling (Z-Score logic) to highlight periods of abnormally high or low volatility relative to recent history. With gradient coloring and clear volatility zones, AVSO provides a visually intuitive way to analyze market volatility and adapt trading strategies accordingly.

█ How It Works

⚪ Scaling Metrics: The indicator scales user-selected metrics (e.g., volume, ATR, standard deviation) relative to the market and price, providing a standardized volatility measure.

⚪ Z-Score Standardization: The scaled metric is normalized using a Z-Score to measure how far current volatility deviates from its recent mean.

Positive Z-Score: Above-average volatility.

Negative Z-Score: Below-average volatility.

⚪ Adaptive Smoothing: An Adaptive EMA smooths the Z-Score, dynamically adjusting its length based on the strength of the volatility. Stronger deviations result in shorter smoothing, increasing responsiveness.

█ Unique Feature: Yang-Zhang Volatility

The Yang-Zhang volatility estimator sets this indicator apart by providing a more robust and accurate measure of volatility compared to traditional methods like ATR or standard deviation.

⚪ What Makes Yang-Zhang Volatility Unique?

Comprehensive Calculation: It combines overnight price gaps (log returns from the previous close to the current open) and intraday price movements (high, low, and close).

Accurate for Gapped Markets: Traditional volatility measures can misrepresent price movement when significant gaps occur between sessions. Yang-Zhang accounts for these gaps, making it highly reliable for assets prone to overnight price jumps, such as stocks, cryptocurrencies, and futures.

Adaptable to Real Market Conditions : By including both close-to-open returns and intraday volatility, it provides a balanced and adaptive measure that captures the full volatility picture.

⚪ Why This Matters to Traders

Better Volatility Insights: Yang-Zhang offers a clearer view of true market volatility, especially in markets with price gaps or uneven trading sessions.

Improved Trade Timing: By identifying volatility spikes and calm periods more effectively, traders can time their entries and exits with greater confidence.

█ How to Use

Identify High and Low Volatility

A high Z-Score (>2) indicates significant market volatility. This can signal momentum-driven moves, breakouts, or areas of increased risk.

A low Z-Score (<-2) suggests low volatility or a calm market environment. This often occurs before a potential breakout or reversal.

Trade Signals

High Volatility Zones (background highlight): Monitor for potential breakouts, trend continuations, or reversals.

Low Volatility Zones: Anticipate range-bound conditions or upcoming volatility spikes.

█ Settings

Source: Select the price source for scaling calculations (close, high, low, open).

Metric Measure: Choose the volatility measure:

Volume: Scales raw volume.

Close: Uses closing price changes.

Standard Deviation: Price dispersion.

ATR: Average True Range.

Yang: Yang-Zhang volatility estimate.

Bars to Analyze: Number of historical bars used to calculate the mean and standard deviation of the scaled metric.

ATR / Standard Deviation Period: Lookback period for ATR or Standard Deviation calculation.

Yang Volatility Period: Period for the Yang-Zhang volatility estimator.

Smoothing Period: Base smoothing length for the adaptive smoothing line.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Volatility % (Standard Deviation of Returns)This script takes closing prices of candles to measure the Standard Deviation (σ) which is then used to calculate the volatility by taking the stdev of the last 30 candles and multiplying it by the root of the trading days in a year, month and week. It then multiplies that number by 100 to show a percentage.

Default settings are annual volatility (252 candles, red), monthly volatility (30 candles, blue) and weekly volatility (5 candles, green) if you use daily candles. It is open source so you can increase the number of candles with which the stdev is calculated, and change the number of the root that multiplies the stdev.

Rainbow EMA Areas with Volatility HighlightThe indicator provides traders with an enhanced visual tool to observe price movements, trend strength, and market volatility on their charts. It combines multiple EMAs (Exponential Moving Averages) with color-coded areas to indicate the market’s directional bias and a high-volatility highlight for detecting times of increased market activity.

Explanation of Key Components

Multiple EMAs (Exponential Moving Averages):

Six different EMAs are calculated for various periods (15, 45, 100, 150, 200, 300).

Each EMA period represents a different timeframe, from short-term to long-term trends, providing a well-rounded view of price behavior across different market cycles.

The EMAs are color-coded for easy differentiation:

Green shades indicate bullish trends when prices are above the EMAs.

Red shades indicate bearish trends when prices are below the EMAs.

The space between each EMA is filled with a gradient color, creating a "wave" effect that helps identify the market’s overall direction.

ATR-Based Volatility Detection:

The ATR (Average True Range), a measure of market volatility, is used to assess how much the price is fluctuating. When volatility is high, price movements are typically more significant, indicating potential trading opportunities or times to exercise caution.

The indicator calculates ATR and uses a customizable multiplier to set a high-volatility threshold.

When the ATR exceeds this threshold, it signals that the market is experiencing high volatility.

Visual High Volatility Highlight:

A yellow background appears on the chart during periods of high volatility, giving a subtle but clear visual indication that the market is active.

This highlight helps traders spot potential breakout areas or increased activity zones without obstructing the EMA areas.

Volatility Signal Markers:

Small, red triangular markers are plotted above price bars when high volatility is detected, marking these areas for additional emphasis.

These signals serve as alerts to help traders quickly recognize high volatility moments where price moves may be stronger.

How to Use This Indicator

Identify Trends Using EMA Areas:

Bullish Trend: When the price is above most or all EMAs, and the EMA areas are colored in shades of green, it indicates a strong bullish trend. Traders might look for buy opportunities in this scenario.

Bearish Trend: When the price is below most or all EMAs, and the EMA areas are colored in shades of red, it signals a bearish trend. This condition can suggest potential sell opportunities.

Consolidation or Neutral Trend: If the price is moving within the EMA bands without a clear green or red dominance, the market may be in a consolidation phase. This period often precedes a breakout in either direction.

Volatility-Based Entries and Exits:

High Volatility Areas: The yellow background and red triangular markers signal high-volatility areas. This information can be valuable for identifying potential breakout points or strong moves.

Trading in High Volatility: During high-volatility phases, the market may experience rapid price changes, which can be ideal for breakout trades. However, high volatility also involves higher risk, so traders may adjust their strategies accordingly (e.g., setting wider stops or adjusting position sizes).

Trading in Low Volatility: When the yellow background and markers are absent, volatility is lower, indicating a calmer market. In these times, traders may choose to look for range-bound trading opportunities or wait for the next trend to develop.

Combining with Other Indicators:

This indicator works well in combination with momentum or oscillating indicators like RSI or MACD, providing a well-rounded view of the market.

For example, if the indicator shows a bullish EMA area with high volatility, and an RSI is trending up, it could be a stronger buy signal. Conversely, if the indicator shows a bearish EMA area with high volatility and RSI is trending down, this could be a stronger sell signal.

Practical Trading Examples

Bullish Trend in High Volatility:

Price is above the EMAs, showing green EMA areas, and the high volatility background is active.

This indicates a strong bullish trend with significant price movement potential.

A trader could look for breakout or continuation entries in the direction of the trend.

Bearish Reversal Signal:

Price crosses below the EMAs, showing red EMA areas, while high volatility is also detected.

This suggests that the market may be reversing to a bearish trend with increased price movement.

Traders could consider taking short positions or setting stops on existing long trades.

This indicator is designed to provide a rich visual experience, making it easy to spot trends, consolidations, and volatility zones at a glance. It is best used by traders who benefit from visual cues and who seek a quick understanding of both trend direction and market activity. Let me know if you'd like further customization or additional functionalities!

Machine Learning Adaptive SuperTrend [AlgoAlpha]📈🤖 Machine Learning Adaptive SuperTrend - Take Your Trading to the Next Level! 🚀✨

Introducing the Machine Learning Adaptive SuperTrend , an advanced trading indicator designed to adapt to market volatility dynamically using machine learning techniques. This indicator employs k-means clustering to categorize market volatility into high, medium, and low levels, enhancing the traditional SuperTrend strategy. Perfect for traders who want an edge in identifying trend shifts and market conditions.

What is K-Means Clustering and How It Works

K-means clustering is a machine learning algorithm that partitions data into distinct groups based on similarity. In this indicator, the algorithm analyzes ATR (Average True Range) values to classify volatility into three clusters: high, medium, and low. The algorithm iterates to optimize the centroids of these clusters, ensuring accurate volatility classification.

Key Features

🎨 Customizable Appearance: Adjust colors for bullish and bearish trends.

🔧 Flexible Settings: Configure ATR length, SuperTrend factor, and initial volatility guesses.

📊 Volatility Classification: Uses k-means clustering to adapt to market conditions.

📈 Dynamic SuperTrend Calculation: Applies the classified volatility level to the SuperTrend calculation.

🔔 Alerts: Set alerts for trend shifts and volatility changes.

📋 Data Table Display: View cluster details and current volatility on the chart.

Quick Guide to Using the Machine Learning Adaptive SuperTrend Indicator

🛠 Add the Indicator: Add the indicator to favorites by pressing the star icon. Customize settings like ATR length, SuperTrend factor, and volatility percentiles to fit your trading style.

📊 Market Analysis: Observe the color changes and SuperTrend line for trend reversals. Use the data table to monitor volatility clusters.

🔔 Alerts: Enable notifications for trend shifts and volatility changes to seize trading opportunities without constant chart monitoring.

How It Works

The indicator begins by calculating the ATR values over a specified training period to assess market volatility. Initial guesses for high, medium, and low volatility percentiles are inputted. The k-means clustering algorithm then iterates to classify the ATR values into three clusters. This classification helps in determining the appropriate volatility level to apply to the SuperTrend calculation. As the market evolves, the indicator dynamically adjusts, providing real-time trend and volatility insights. The indicator also incorporates a data table displaying cluster centroids, sizes, and the current volatility level, aiding traders in making informed decisions.

Add the Machine Learning Adaptive SuperTrend to your TradingView charts today and experience a smarter way to trade! 🌟📊

[Pandora] Vast Volatility Treasure TroveINTRODUCTION:

Volatility enthusiasts, prepare for VICTORY on this day of July 4th, 2024! This is my "Vast Volatility Treasure Trove," intended mostly for educational purposes, yet these functions will also exhibit versatility when combined with other algorithms to garner statistical excellence. Once again, I am now ripping the lid off of Pandora's box... of volatility. Inside this script is a 'vast' collection of volatility estimators, reflecting the indicators name. Whether you are a seasoned trader destined to navigate financial strife or an eagerly curious learner, this script offers a comprehensive toolkit for a broad spectrum of volatility analysis. Enjoy your journey through the realm of market volatility with this code!

WHAT IS MARKET VOLATILITY?:

Market volatility refers to various fluctuations in the value of a financial market or asset over a period of time, often characterized by occasional rapid and significant deviations in price. During periods of greater market volatility, evolving conditions of prices can move rapidly in either direction, creating uncertainty for investors with results of sharp declines as well as rapid gains. However, market volatility is a typical aspect expected in financial markets that can also present opportunities for informed decision-making and potential benefits from the price flux.

SCRIPT INTENTION:

Volatility is assuredly omnipresent, waxing and waning in magnitude, and some readers have every intention of studying and/or measuring it. This script serves as an all-in-one armada of volatility estimators for TradingView members. I set out to provide a diverse set of tools to analyze and interpret market volatility, offering volatile insights, and aid with the development of robust trading indicators and strategies.

In today's fast-paced financial markets, understanding and quantifying volatility is informative for both seasoned traders and novice investors. This script is designed to empower users by equipping them with a comprehensive suite of volatility estimators. Each function within this script has been meticulously crafted to address various aspects of volatility, from traditional methods like Garman-Klass and Parkinson to more advanced techniques like Yang-Zhang and my custom experimental algorithms.

Ultimately, this script is more than just a collection of functions. It is a gateway to a deeper understanding of market volatility and a valuable resource for anyone committed to mastering the complexities of financial markets.

SCRIPT CONTENTS:

This script includes a variety of functions designed to measure and analyze market volatility. Where applicable, an input checkbox option provides an unbiased/biased estimate. Below is a brief description of each function in the original order they appear as code upon first publish:

Parkinson Volatility - Estimates volatility emphasizing the high and low range movements.

Alternate Parkinson Volatility - Simpler version of the original Parkinson Volatility that I realized.

Garman-Klass Volatility - Estimates volatility based on high, low, open, and close prices using a formula that adjusts for biases in price dynamics.

Rogers-Satchell-Yoon Volatility #1 - Estimates volatility based on logarithmic differences between high, low, open, and close values.

Rogers-Satchell-Yoon Volatility #2 - Similar estimate to Rogers-Satchell with the same result via an alternate formulation of volatility.

Yang-Zhang Volatility - An advanced volatility estimate combining both strengths of the Garman-Klass and Rogers-Satchell estimators, with weights determined by an alpha parameter.

Yang-Zhang (Modified) Volatility - My experimental modification slightly different from the Yang-Zhang formula with improved computational efficiency.

Selectable Volatility - Basic customizable volatility calculation based on the logarithmic difference between selected numerator and denominator prices (e.g., open, high, low, close).

Close-to-Close Volatility - Estimates volatility using the logarithmic difference between consecutive closing prices. Specifically applicable to data sources without open, high, and low prices.

Open-to-Close Volatility - (Overnight Volatility): Estimates volatility based on the logarithmic difference between the opening price and the last closing price emphasizing overnight gaps.

Hilo Volatility - Estimates volatility using a method similar to Parkinson's method, which considers the logarithm of the high and low prices.

Vantage Volatility - My experimental custom 'vantage' method to estimate volatility similar to Yang-Zhang, which incorporates various factors (Alpha, Beta, Gamma) to generate a weighted logarithmic calculation. This may be a volatility advantage or disadvantage, hence it's name.

Schwert Volatility - Estimates volatility based on arithmetic returns.

Historical Volatility - Estimates volatility considering logarithmic returns.

Annualized Historical Volatility - Estimates annualized volatility using logarithmic returns, adjusted for the number of trading days in a year.

If I omitted any other known varieties, detailed requests for future consideration can be made below for their inclusion into this script within future versions...

BONUS ALGORITHMS:

This script also includes several experimental and bonus functions that push the boundaries of volatility analysis as I understand it. These functions are designed to provide additional insights and also are my ideal notions for traders looking to explore other methods of volatility measurement.

VOLATILITY APPLICATIONS:

Volatility estimators serve a common role across various facets of trading and financial analysis, offering insights into market behavior. These tools are already in instrumental with enhancing risk management practices by providing a deeper understanding of market dynamics and the inherent uncertainty in asset prices. With volatility estimators, traders can effectively quantifying market risk and adjust their strategies accordingly, optimizing portfolio performance and mitigating potential losses. Additionally, volatility estimations may serve as indication for detecting overbought or oversold market conditions, offering probabilistic insights that could inform strategic decisions at turning points. This script

distinctly offers a variety of volatility estimators to navigate intricate financial terrains with informed judgment to address challenges of strategic planning.

CODE REUSE:

You don't have to ask for my permission to use/reuse these functions in your published scripts, simply because I have better things to do than answer requests for the reuse of these functions.

Notice: Unfortunately, I will not provide any integration support into member's projects at all. I have my own projects that require way too much of my day already.

Realized volatility differentialAbout

This is a simple indicator that takes into account two types of realized volatility: Close-Close and High-Low (the latter is more useful for intraday trading).

The output of the indicator is two values / plots:

an average of High-Low volatility minus Close-Close volatility (10day period is used as a default)

the current value of the indicator

When the current value is:

lower / below the average, then it means that High-Low volatility should increase.

higher / above then obviously the opposite is true.

How to use it

It might be used as a timing tool for mean reversion strategies = when your primary strategy says a market is in mean reversion mode, you could use it as a signal for opening a position.

For example: let's say a security is in uptrend and approaching an important level (important to you).

If the current value is:

above the average, a short position can be opened, as High-Low volatility should decrease;

below the average, a trend should continue.

Intended securities

Futures contracts