Retail Pain Index (RPIx) (RPIx) Retail Pain Index (DAFE)

See the Market’s Pain. Trade the Edge.

The Retail Pain Index (RPIx) is a next-generation volatility and sentiment tool designed to reveal the hidden moments when retail traders are most likely being squeezed, stopped out, or forced to capitulate. This is not just another oscillator—it’s a behavioral market scanner that quantifies “pain” as price rips away from the average entry zone, often marking the fuel for the next big move.

Why is RPIx so Unique?

Behavioral Volatility Engine:

RPIx doesn’t just track price or volume. It measures how far price is moving away from where the crowd has recently entered (using a rolling VWAP average), then normalizes this “distance” into a Z-score. The result? You see when the market is inflicting maximum pain on the most participants.

Dynamic, Intuitive Coloring:

The main RPIx line is purple in normal conditions, but instantly turns red when pain is extreme to the upside (+2.00 or higher) and green when pain is extreme to the downside (-2.00 or lower). This makes it visually obvious when the market is entering a “max pain” regime.

Threshold Lines for Clarity:

Dashed red and green lines at +2.00 and -2.00 Z-score levels make it easy to spot rare, high-pain events at a glance.

Signature Dashboard & Info Line:

Dashboard: A compact, toggleable panel in the top right of the indicator pane shows the current Z-score, threshold, and status—perfect for desktop users who want a quick read on market stress.

Info Line: For mobile or minimalist traders, a single-line info label gives you the essentials without cluttering your screen.

Inputs & Customization

Entry Cluster Lookback: Adjusts how many bars are used to calculate the “entry zone” (VWAP average). A higher value smooths the signal, a lower value makes it more responsive.

Pain Z-Score Threshold:

Sets the sensitivity for what counts as “extreme pain.” Default is ±2.00, but you can fine-tune this to match your asset’s volatility or your own risk appetite.

Show Dashboard / Show Compact Info Label:

Toggle these features on or off to fit your workflow and screen size.

How to utilize RPIx's awesomeness:

Extreme Readings = Opportunity:

When RPIx spikes above +2.00 (red) or below -2.00 (green), the market is likely running stops, liquidating weak hands, or forcing retail traders to capitulate. These moments often precede sharp reversals, trend accelerations, or volatility expansions.

Combine with Price Action:

Use RPIx as a confirmation tool for your existing strategy, or as a standalone alert for “pain points” where the crowd is most vulnerable.

Visual Edge:

The color-coded line and threshold levels make it easy to spot regime shifts and rare events—no more squinting at numbers or guessing when the market is about to snap.

Why RPIx?

Works on Any Asset, Any Timeframe:

Stocks, futures, crypto, forex—if there’s a crowd, there’s pain, and RPIx will find it.

Behavioral Alpha:

Most indicators lag. RPIx quantifies the psychological stress in the market, giving you a real-time edge over the herd.

Customizable, Clean, and Powerful:

Designed for both power users and mobile traders, with toggles for every workflow.

See the pain. Trade the edge.

Retail Pain Index: Because the market’s next move is written in the crowd’s discomfort.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz , for DAFE Trading Systems, for DAFE Trading Systems

Volume Weighted Average Price (VWAP)

Multi VWAPsMulti VWAPs Inspired by Biran Shannon and his book:

"MAXIMUM TRADING GAINS WITH ANCHORED VWAP . The Perfect Combination of Price, Time & Volume."

(ISBN 9798986868004)

A comprehensive VWAP (Volume Weighted Average Price) indicator that combines multiple timeframes and sessions in one view. Perfect for day trading and swing trading across different markets.

Features:

• Multiple VWAP Timeframes:

- Daily VWAP

- Weekly VWAP

- Monthly VWAP

- Quarterly VWAP

- Yearly VWAP

• Session-specific VWAPs:

- London Session (3:00 AM - 11:30 AM NY time)

- New York Session (9:30 AM - 4:00 PM NY time)

• Additional Indicators:

- Midnight Price Line (Previous day's closing price)

- 5-Day Moving Average

- 50-Day Moving Average

• Customization Options:

- Toggle individual VWAPs and indicators

- Customize colors for each component

- Adjustable label positioning

- MA smoothing settings

- Option to show/hide previous day's midnight price

• Smart Features:

- Auto-adjusting calculations based on timeframe

- Clear session boundaries

- Optimized for all chart timeframes

- Clean label system

Perfect for:

• Day traders tracking multiple timeframe momentum

• Swing traders using longer-term VWAPs

• Session traders focusing on London/NY hours

• Multi-timeframe analysis

• Price action trading with VWAP support/resistance

This indicator combines essential trading tools in one clean interface, helping you make informed decisions without cluttering your chart.

Money Flow Index + VWAP Trend FilterThis indicator combines the volume-weighted momentum analysis of the Money Flow Index (MFI) with the trend-filtering capabilities of the Volume Weighted Average Price (VWAP) to generate reliable buy and sell signals. By requiring MFI overbought/oversold conditions to align with the trend direction relative to VWAP, this indicator reduces false signals, making it ideal for trading on timeframes like 5-minute to 4-hour charts.

How It Works

The indicator uses two technical components to produce signals:

Money Flow Index (MFI) for Momentum Extremes:

The MFI, calculated over a default 14-period length, measures buying and selling pressure using price and volume data. A buy signal is triggered when MFI crosses above the oversold level (default: 20), indicating potential buying pressure, while a sell signal occurs when MFI crosses below the overbought level (default: 80), suggesting selling pressure.

Volume Weighted Average Price (VWAP) for Trend Direction:

The VWAP calculates the average price of an asset, weighted by volume, resetting at the start of each trading session (e.g., daily for stocks). It acts as a dynamic support/resistance level. A bullish trend is confirmed when the price is above the VWAP, and a bearish trend when the price is below the VWAP. This ensures MFI signals are filtered to align with the broader trend direction, plotted as a purple line on the chart.

Signal Generation

Signals are generated using the previous bar’s values to prevent repainting:

Buy Signal: The MFI crosses above the oversold level, and the price is above the VWAP (bullish trend). Displayed as a green upward triangle below the bar.

Sell Signal: The MFI crosses below the overbought level, and the price is below the VWAP (bearish trend). Displayed as a red downward triangle above the bar.

TLC sessionA Professional Intraday Session Tracker with VWAP and Economic Event Integration

Description

This indicator provides visual tracking of major trading sessions (Asian, London, New York) combined with VWAP calculations and macroeconomic event zones. It's designed for intraday traders who need to monitor session overlaps, liquidity periods, and high-impact news events.

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Key Features:

Customizable Session Tracking: Visualize up to 3 trading sessions with adjustable time zones (supports IANA & GMT formats)

Dynamic VWAP Integration: Built-in Volume-Weighted Average Price calculation

Macro Event Zones: Highlights key economic announcement windows (adjustable for summer/winter time)

Price Action Visualization: Displays open/close prices, session ranges, and average price levels

Automatic DST Adjustment: Uses IANA timezone database for daylight savings awareness

How It Works

1. Trading Session Detection

Three fully configurable sessions (e.g., Asia, London, New York)

Each session displays:

Colored background zone

Opening price (dashed line)

Closing price (dashed line)

Average price (dotted line)

Optional label with session name

2. VWAP Calculation

Standard Volume-Weighted Average Price plotted as circled line

Helps identify fair value within each session

3. Macro Event Zones

Special highlighted period for economic news releases

Automatically adjusts for summer/winter time

Default set to 1000-1200 (summer) or 0900-1100 (winter) GMT-5 (US session open)

Why This Indicator is Unique

Multi-Session Awareness

Unlike simple session indicators, this tool:

Tracks price development within each session

Shows session overlaps (critical for volatility periods)

Maintains separate VWAP calculations across sessions

Professional-Grade Features

IANA timezone support (automatic DST handling)

Customizable visual elements (toggle labels, ranges, averages)

Object-based architecture (clean, efficient rendering)

News event integration (helps avoid trading during high-impact releases)

Usage Recommendations

Best Timeframes

1-minute to 1-hour charts (intraday focus)

Not recommended for daily+ timeframes

Trading Applications

1. Session Breakout Strategy: Trade breakouts when London/New York sessions open

2. VWAP Reversion: Fade moves that deviate too far from VWAP

3. News Avoidance: Reduce position sizing during macro event windows

Visual Example

Asian session (red)

London session (blue)

New York session (purple)

Macro event zone (white)

VWAP line (gold circles)

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Moving Volume-Weighted Avg Price, % Channel, BBsThis script includes:

- Moving Volume-Weighted Average Price line.

- User-defined % band above and below, very useful for "breakout" signals, and mentally adjusting to the magnitude of price swings when viewing an automatic scale on the price axis.

- Volume-Weighted Bollinger Bands, which are more sensitive to volume.

More detail:

- This is like TV's basic VWAP in concept, except the major flaw in that is that it has reset periods that you can't override, and the volume is cumulative until the next hard reset. The 'reset' is OK for securities trading, that resets every day anyway. But not for crypto - and not if/when securities trading goes 24/7. Also, the denominator accumulating over the entire period is also *not* OK, because then what is shown means something different as the day progresses - which kind of makes it useless. In other words, it starts out very sensitive to volume, and gets progressively more numb to it as they day progresses, and starts flattening out.

- This fixes both problems, by using a user-definable moving window for the average. Essentially combining SMA with volume-weighting.

- You may also find an invaluable trading aid, in the % bands above and below.

- What can optionally be shown is standard deviation bands, aka Bollinger bands. The advantage over regular BB is that it's volume-weighted. Since it is already calculated on a moving average, the period for the standard deviation has been shortened by default, and the magnitude increased, to better approximate regular Bollinger Bands - but it's still more responsive to volume.

Multi-VWAP System🚀 Multi-VWAP System — Anchored VWAP & Deviation Bands

Overview

The Multi-VWAP System provides traders with a professional-grade approach to anchored VWAP analysis. Inspired by Brian Shannon's pioneering work on Anchored VWAP, this indicator automatically calculates and plots:

Current Session VWAP

Previous Session VWAP (also known as "2-Day VWAP")

High-of-Day (HOD) Anchored VWAP

Each VWAP can also display optional Standard Deviation Bands to highlight statistically significant deviations from the volume-weighted average price.

🔍 Why Anchored VWAP Matters

Volume Weighted Average Price (VWAP) is among the most critical institutional indicators, as it represents the average price paid for a stock adjusted by trading volume. This makes VWAP crucial for identifying fair value and significant areas of institutional activity.

Institutions utilize VWAP extensively to guide their execution algorithms. For instance, if price dips below a 2-day anchored VWAP (anchored to the previous session's open), many institutions interpret this as a discounted entry, potentially triggering large-scale buy programs. Conversely, sustained movement above VWAP signals strong buying pressure and bullish sentiment.

📌 Why Multiple Anchors?

Traders commonly anchor VWAPs at critical reference points:

Current Session VWAP:

Essential for day traders as a reference for intraday sentiment. Price action above this line generally indicates bullish sentiment, while price below signals bearish sentiment.

Previous Session (2-Day) VWAP:

Heavily used by institutions and swing traders, it provides insight into multi-session sentiment. Institutions commonly activate buy or sell programs based on whether price is trading at a premium or discount relative to this VWAP.

High-of-Day (HOD) VWAP:

Frequently used by momentum traders, this anchor captures sentiment after the most recent intraday high. Price above the HOD VWAP suggests sustained bullish momentum, while price below might signal weakening momentum.

🌟 Standard Deviation Bands

Each anchored VWAP in this indicator includes optional Standard Deviation Bands, highlighting statistical extremes. Traders use these bands to:

Identify potentially overextended moves (beyond +2σ or +3σ).

Gauge momentum strength (holding above +1σ).

Spot mean-reversion setups when price returns to VWAP after extreme moves.

🎨 Dynamic Background and Momentum Colorization

To visually highlight strength or weakness in price action relative to VWAP:

Dynamic Background Fill between Current and Previous VWAPs:

Green background appears when the Current VWAP is above the Previous VWAP and the linear regression slope (adjustable length) is positive, indicating bullish sentiment.

Red background appears when the Current VWAP is below the Previous VWAP and the slope is negative, indicating bearish sentiment.

No fill when conditions are mixed or momentum is uncertain.

Gold Fill above HOD VWAP:

When price action is above the High-of-Day VWAP and momentum (linear regression slope) is positive, a subtle gold shading appears, quickly highlighting bullish momentum.

⚙ Fully Customizable Settings

Session Times: Adjust session start and end times to match your specific market hours.

Standard Deviation Bands: Enable or disable each VWAP’s deviation bands individually and select how many bands (1σ, 2σ, or 3σ) you'd like to display.

Momentum Slope Length: Adjustable lookback for linear regression slope calculation—giving you full control of trend sensitivity.

🎯 Who Should Use This Indicator?

This indicator is perfect for:

Day Traders who want quick insights into intraday sentiment shifts.

Swing Traders tracking institutional footprints and seeking optimal entry/exit points.

Momentum Traders who rely on clearly visible momentum signals from HOD anchored VWAPs.

Institutional Traders and Professionals seeking sophisticated, institutionally-inspired VWAP analysis without manual anchoring.

📈 Summary of Features

✅ Automatic VWAP Anchors (Current Session, Previous Session, High-of-Day)

✅ Optional Standard Deviation Bands for each VWAP anchor

✅ Dynamic Background Coloring based on price action and momentum conditions

✅ Gold Momentum Highlight for quick bullish momentum identification above HOD VWAP

✅ Fully Customizable Inputs for precise personalization and flexibility

📢 Conclusion

The Multi-VWAP System isn't just another VWAP indicator. It's an institutional-level, dynamic, multi-dimensional analysis tool inspired by the work of Brian Shannon and leading institutional traders. It takes the guesswork out of anchoring and analysis, leaving you free to focus on identifying and executing high-probability trade setups.

Enjoy trading smarter—not harder. Happy Trading! 🚀📊

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Volume-Weighted Pivot BandsThe Volume-Weighted Pivot Bands are meant to be a dynamic, rolling pivot system designed to provide traders with responsive support and resistance levels that adapt to both price volatility and volume participation. Unlike traditional daily pivot levels, this tool recalculates levels bar-by-bar using a rolling window of volume-weighted averages, making it highly relevant for intraday traders, scalpers, swing traders, and algorithmic systems alike.

-- What This Indicator Does --

This tool calculates a rolling VWAP-based pivot level, and surrounds that central pivot with up to five upper bands (R1–R5) and five lower bands (S1–S5). These act as dynamic zones of potential resistance (R) and support (S), adapting in real time to price and volume changes.

Rather than relying on static session or daily data, this indicator provides continually evolving levels, offering more relevant levels during sideways action, trending periods, and breakout conditions.

-- How the Bands Are Calculated --

Pivot (VWAP Pivot):

The core of this system is a rolling Volume-Weighted Average Price, calculated over a user-defined window (default 20 bars). This ensures that each bar’s price impact is weighted by its volume, giving a more accurate view of fair value during the selected lookback.

Volume-Weighted Range (VW Range):

The highest high and lowest low over the same window are used to calculate the volatility range — this acts as a spread factor.

Support & Resistance Bands (S1–S5, R1–R5):

The bands are offset above and below the pivot using multiples of the VW Range:

R1 = Pivot + (VW Range × multiplier)

R2 = R1 + (VW Range × multiplier)

R3 = R2 + (VW Range x multiplier)

...

S1 = Pivot − (VW Range × multiplier)

S2 = S1 − (VW Range × multiplier)

S3 = S2 - (VW Range x multiplier)

...

You can control the multiplier manually (default is 0.25), to widen or tighten band spacing.

Smoothing (Optional):

To prevent erratic movements, you can optionally toggle on/off a simple moving average to the pivot line (default length = 20), providing a smoother trend base for the bands.

-- How to Use It --

This indicator can be used for:

Support and resistance identification:

Price often reacts to R1/S1, and the outer bands (R4/R5 or S4/S5) act as overshoot zones or strong reversal areas.

Trend context:

If price is respecting upper bands (R2–R3), the trend is likely bullish. If price is pressing into S3 or lower, it may indicate sustained selling pressure or a breakdown.

Volatility framing:

The distance between bands adjusts based on price range over the rolling window. In tighter markets, the bands compress — in volatile moves, they expand. This makes the indicator self-adaptive.

Mean reversion trades:

A move into R4/R5 or S4/S5 without continuation can be a sign of exhaustion — potential for reversal toward the pivot.

Alerting:

Built-in alerts are available for crosses of all major bands (R1–R5, S1–S5), enabling trade automation or scalp alerts with ease.

-- Visual Features --

Fuchsia Lines: Mark all Resistance (R1–R5) levels.

Lime Lines: Mark all Support (S1–S5) levels.

Gray Circle Line: Marks the rolling pivot (VWAP-based).

-- Customizable Settings --

Rolling Length: Number of bars used to calculate VWAP and VW Range.

Multiplier: Controls how wide the bands are spaced.

Smooth Pivot: Toggle on/off to smooth the central pivot.

Pivot Smoothing Length: Controls how many bars to average when smoothing is enabled.

Offset: Visually shift all bands forward/backward in time.

-- Why Use This Over Standard Pivots? --

Traditional pivots are based on previous session data and remain fixed. That’s useful for static setups, but may become irrelevant as price action evolves. In contrast:

This system updates every bar, adjusting to current price behavior.

It includes volume — a key feature missing from most static pivots.

It shows multiple bands, giving a full view of compression, breakout potential, or trend exhaustion.

-- Who Is This For? --

This tool is ideal for:

Day traders & scalpers who need relevant intraday levels.

Swing traders looking for evolving areas of confluence.

Algorithmic/systematic traders who rely on quantifiable, volume-aware support/resistance.

Traders on all assets: works on crypto, stocks, futures, forex — any chart that has volume.

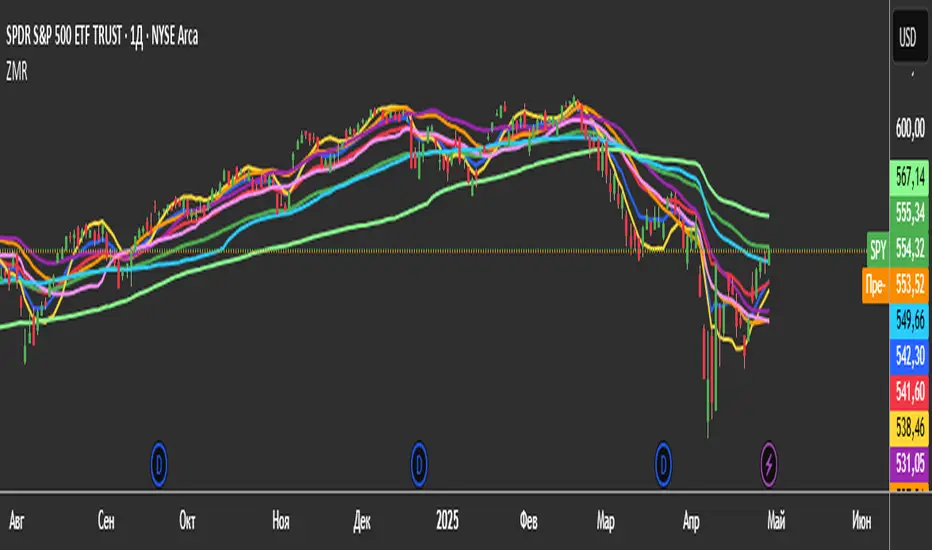

3 Zero Lag + 3 Moving Averages + 3 RVWAPThe "3 Zero Lag + 3 Moving Averages + 3 RVWAP" (ZMR) indicator combines three groups of tools for technical analysis.

1. Three Customizable Moving Averages (MAs):

Configuration for Each MA:

Choice of 7 types (SMA, EMA, WMA, HMA, VWMA, LSMA, SMMA).

Independent periods and price sources for each line.

Visualization:

MA1 (Blue), MA2 (Red), MA3 (Green).

2. Three Zero Lag EMAs (ZLEMA) with Individual Settings:

Lag Reduction: Corrects traditional EMA lag using:

Adjusted Price = 2 * Current Price - Price .

Flexibility:

Unique lengths (20, 50, 70) and individual price sources for each ZLEMA (HLC3, HL2, Close, etc.).

Colors:

ZLEMA1 (Yellow), ZLEMA2 (Orange), ZLEMA3 (Purple).

3. Three Rolling VWAPs with Custom Parameters:

Volume-Weighted Average Price (VWAP):

Calculated for three periods (20, 50, 100) with dedicated price sources for each VWAP.

Colors:

VWAP1 (Pink), VWAP2 (Light Blue), VWAP3 (Neon Green).

Stochastic and RSI2 entriesStochastic and RSI2 entries, v1.0

This indicator combines Stochastic and RSI to facilitate "RSI2" entry signals. Buy signals will be shown at the bottom.

The default configuration uses non-standard settings for the underlying indicators to tailor it for this type of entry strategy.

This is an entry strategy that tries to find entries close to "the dip".

A combination of Stochastic crossovers, VWAP, daily SMA50 and daily SMA200 are used to verify buy signals.

This indicator is written for bullish signals and aims to find the start of short trends or cheap entries for longer positions.

Like with any strategy, some signals will be false, and the user is advised to do some own research before using the buy signals for actual entries.

Happy trading!

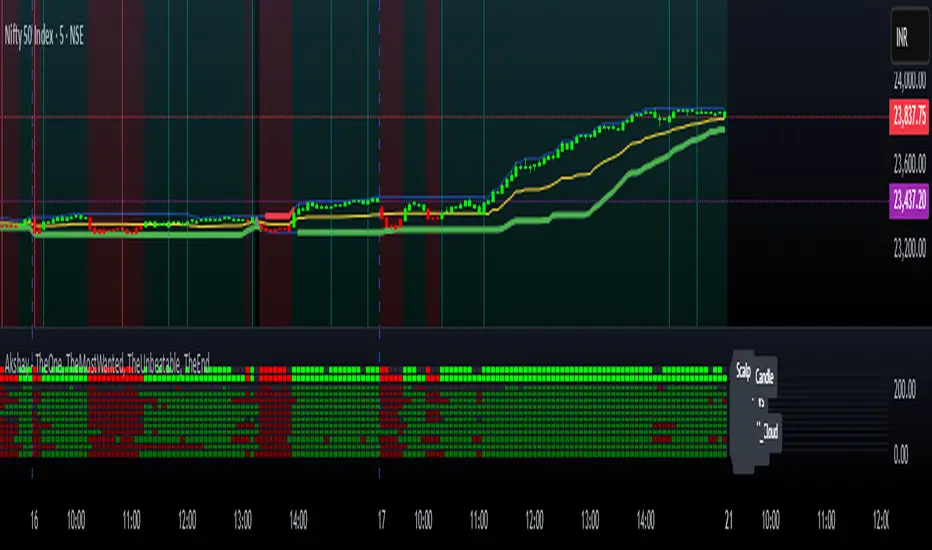

Akshay - TheOne, TheMostWanted, TheUnbeatable, TheEnd➤ All-in-One Solution (❌ No repaint):

This Technical Chart contains, MA24 Condition, Supertrend Indicator, HalfTrend Signal, Ichimoku Cloud Status, Parabolic SAR (P_SAR), First 5-Minute Candle Analysis (ORB5min), Volume-Weighted Moving Average (VWMA), Price-Volume Trend (PVT), Oscillator Composite, RSI Condition, ADX & Trend Strength.

Technicals don't lie.

🚀 Overview and Key Features

Comprehensive Multi-Indicator Approach:

The script is built to be an all-in-one technical indicator on TradingView. It integrates several well-known indicators and overlays—including Supertrend, HalfTrend, Ichimoku Cloud, various moving averages (EMA, SMA, VWMA), oscillators (Klinger, Price Oscillator, Awesome Oscillator, Chaikin Oscillator, Ultimate Oscillator, SMI Ergodic Oscillator, Chande Momentum Oscillator, Detrended Price Oscillator, Money Flow Index), ADX, and Donchian Channels—to create a composite picture of market sentiment.

Signal Generation and Alerts:

It not only calculates these indicators but also aggregates their output into “Master Candle” signals. Vertical lines are drawn on the chart with corresponding alerts to indicate potential buy or sell opportunities based on robust, combined conditions.

Visual Layering:

Through the use of colored histograms, custom candle plots, trend lines, and background color changes, the script offers a multi-layered visual representation of data, providing clarity about both short-term signals and overall market trends.

⚙️ How It Works and Functionality

MA24 Condition:

Uses the 24-period moving average as a proxy; if the price is above it, the bar is colored green, and red if below, with neutrality when conditions aren’t met.

Supertrend Indicator:

Evaluates price relative to the Supertrend level (calculated via ATR), coloring green when price is above it and red when below.

HalfTrend Signal:

Determines trend shifts by comparing the current close to a calculated trend level; green indicates an upward trend, while red suggests a downtrend.

Ichimoku Cloud Status:

Analyzes the relationship between the Conversion and Base lines; a bullish (green) signal is given when price is above both or the Conversion line is higher than the Base line.

Parabolic SAR (P_SAR):

Colors the signal based on whether the current price is above (green) or below (red) the Parabolic SAR marker, indicating stop and reverse conditions.

First 5-Minute Candle Analysis (ORB5min):

Uses key levels from the first 5-minute candle; if price exceeds the candle’s low, VWAP, and MA, it’s bullish (green), otherwise bearish (red).

Volume-Weighted Moving Average (VWMA):

Compares the current price to volume-weighted averages; a price above these levels is shown in green, below in red.

Price-Volume Trend (PVT):

Determines bullish or bearish momentum by comparing PVT to its VWAP—green when above and red when below.

Oscillator Composite:

Aggregates signals from multiple oscillators; a majority of positive results turn it green, while negative dominance results in red.

RSI Condition:

Uses a simple RSI threshold of 50, with values above signifying bullish (green) momentum and below marking bearish (red) conditions.

ADX & Trend Strength:

Reflects overall trend strength through ADX and directional movements; a combination favoring bullish conditions colors it green, with red signaling bearish pressure.

Master Candle Overall Signal:

Combines multiple indicator outputs into one “Master” signal—green for a consensus bullish trend and red for a bearish outlook.

Scalp Signal Variation:

Focused on short-term price changes, this signal adjusts quickly; green indicates improving short-term conditions, while red signals a downturn.

📊 Visualizations and 🎨 User Experience (❌ no repaint)

Dynamic Histograms & Bar Plots:

Each indicator is represented as a colored bar (with added vertical offsets) to facilitate easy comparison of their respective bullish or bearish contributions.

Clear Color-Coding & Labels:

Green (e.g., GreenFluorescent) indicates bullish sentiment.

Red (e.g., RedFluorescent) indicates bearish sentiment.

Custom labels and descriptive text accompany each bar for clarity.

Interactive Charting:

The overall background color adapts based on the “Master Candle” condition, offering an instant read on market sentiment.

The current candlestick is overlaid with color cues to reinforce the indicator’s signal, enhancing the trading experience.

Real-Time Alerts:

Vertical lines appear on signal events (buy/sell triggers), complemented by alerts that help traders stay on top of actionable market moves.

Sharp lines:

The Sharp lines are plotted based upon the EMA5 cross over with the same market trend, marks this as good time to reentry.

🔧 Settings and Customization

Flexible Timeframe Input:

Users can select their preferred timeframe for analysis, making the indicator adaptable to intraday or longer-term trading styles.

Customizable Indicator Parameters:

➤ Supertrend: Adjust ATR length and multiplier factors.

➤ HalfTrend: Tweak amplitude and channel deviation settings.

➤ Ichimoku Cloud & Oscillators: Fine-tune the conversion/base lines and oscillator lengths to match individual trading strategies.

Visual Customization:

The script’s color schemes and plotting styles can be altered as needed, giving users the freedom to tailor the interface to their taste or existing chart setups.

🌟 Uniqueness of the Concept

Integrated Multi-Indicator Synergy:

Combines a diverse range of trend, momentum, and volume-based indicators into a single cohesive system for a holistic market view.

Master Candle Aggregation:

Consolidates numerous individual signals into a "Master Candle" that filters out noise and provides a clear, consensus-based trading signal.

Layered Visual Feedback:

Uses color-coded histograms, adaptive background cues, and dynamic overlays to deliver a visually intuitive guide to market sentiment at a glance.

Customization and Flexibility:

Offers adjustable parameters for each indicator, allowing users to tailor the system to fit diverse trading styles and market conditions.

✅ Conclusion:

Robust Trading Tool & Non-Repainting Reliability:

This versatile technical analysis tool computes an extensive range of indicators, aggregates them into a stable, non-repainting “Master Candle” signal, and maintains consistent, verifiable outputs on historical data.

Holistic Market Insight & Consistent Signal Generation:

By combining trend detection, momentum oscillators, and volume analysis, the indicator delivers a comprehensive snapshot of market conditions and generates dependable signals across varying timeframes.

User-Centric Design with Rich Visual Feedback:

Customizable settings, clear color-coded outputs, adaptive backgrounds, and real-time alerts work together to provide actionable, transparent feedback—enhancing the overall trading experience.

A Unique All-in-One Solution:

The integrated approach not only simplifies complex market dynamics into an easy-to-read visual guide but also empowers systematic traders with a powerful, adaptable asset for accurate decision-making.

❤️ Credits:

Pine Script™ User Manual

Supertrend

Ichimoku Cloud

Parabolic SAR

Price Volume Trend (PVT)

Average Directional Index (ADX)

Volume Oscillator

HalfTrend

Donchian Trend

Pivot Levels with EMA Trend📌 Trend Change Levels with EMA Trend

✨ Description:

This TradingView script identifies clean trend change levels based on 1-hour structure shifts and filters them to keep only those not invalidated. It follows the "Jake Ricci" method, each level is printed at the beginning of the candle that changes the trend, on a 1 hour chart. For precision, make sure to exclude after/pre market and only use the levels on regular hours charts.

It includes dynamic EMAs (9, 50, 200), intraday VWAP, the daily open level printed, and a visual trend label based on EMA(9) slope.

Designed for intermediate traders, it helps build bias, manage entries, and avoid false setups by focusing on clean, reactive levels that the market respects.

🔧 Core Logic:

On the 1H chart, the script compares current and previous closes to detect trend direction. If the trend flips (e.g., up to down), the open of the candle that caused the flip becomes a candidate level.

Only levels that remain untouched by future candle closes are plotted — this filters out “weak” levels that price already violated (which means, a candle closes after passing through the level).

These levels become key S/R zones and often act as reaction points during pullbacks, traps, and liquidity sweeps.

The idea is to check how the price reacts to those levels. Usually there's a clean retest of the level. After that, if the price continues in that direction, it tends to reach the following level.

🔹 Included Tools:

🟣 Trend Change Levels (1H):

Fixed horizontal lines based on confirmed shifts in trend, shown only when not broken.

📉 EMAs (9 / 50 / 200):

Visibility can be set per timeframe. Use for trend context.

📍 EMA Trend Label:

Shows \"UP\", \"DOWN\", or \"RANGE\" based on EMA(9) slope.

🔵 VWAP (Intraday Reset):

Real-time volume-weighted average price that resets daily. Useful for fair value zones and reversion plays.

🟠 Daily Open Line:

Plot of the current day’s open. Used for intraday directional bias. Usually: DO NOT take longs below the Open Print, DO NOT take shorts above it.

📊 ATR Table:

Displays current ATR multiplier on the chart. It's useful to understand if the market is expanding or not.

📈 How to Use It (Strategy):

1. Start on the 1H chart to generate levels.

Only the open of candles that reversed trend are considered — and only if future candles didn’t close through them. I suggest manually adding horizontal lines to mark again the levels, so that they stick to all the timeframes.

2. Use the trend label to decide your bias — \"UP\" for long setups, \"DOWN\" for shorts. Avoid trading against the slope.

3. Switch to the 5m chart and wait for price to approach a plotted level. These are often used for manipulation, retests, or clean reversals.

4. Look for confirmation: rejection candles, break-and-retest, strong engulfing candles, or traps above/below the level. ALWAYS check the price action around the level, along with the volume.

5. Check if VWAP or an EMA is near the level. If yes, the confluence strengthens the trade idea.

6. Use the ATR value to understand if the market is expanding (candles are bigger than the ATR). You don't want to stay in a slow and ranging trade.

✅ Example Entry Flow:

1. On the 1H chart, note a trend change level printed recently.

2. Check the current trend label — if it says \"UP,\" prefer longs.

3. Wait for price to retrace toward the level.

4. On the 5m, look for a bullish engulfing candle or trap setup at the level.

5. Check if VWAP and EMA(50) are near. If yes, execute the trade.

6. Set stop just under the low of the candle prior to your entry. Ideally, a retracing candle.

To be clear: imaging to be LONG, you wait for a retracement that should touch your level. You wait for a candle that resumes the LONG trend, enter when it breaks the high of the previous candle (sill in retracement), you place your stop under the candle prior to your entry.

Notes:

No repainting — levels only show up after confirmed shifts.

Removes broken levels for chart clarity and reliability.

Helps spot high-probability pullback zones and fakeouts.

Perfect confluence tool to support price action, SMC, or EMA strategies.

Works across multiple timeframes with customizable inputs.

👤 Ideal For:

Intraday traders looking for reactive entry points and direction confirmation.

Swing traders wanting to pinpoint continuation zones or reversal pivots.

🚨 Final Note: This indicator doesn’t generate buy/sell signals. It improves your trade filtering by identifying areas the market already respected and reacting to them with price action. Combine it with your own system , test it in replay, and use screenshots to document setups.

📌 If used with discipline, this becomes a precision tool — not a signal generator.

VWAP + EMA Retracement Indicator SwiftEdgeVWAP + EMA Retracement Indicator

Overview

The VWAP + EMA Retracement Indicator is a powerful and visually engaging tool designed to help traders identify high-probability buy and sell opportunities in trending markets. By combining the Volume Weighted Average Price (VWAP) with two Exponential Moving Averages (EMAs) and a unique retracement-based signal logic, this indicator pinpoints moments when the price pulls back to a key zone before resuming its trend. Its modern, AI-inspired visuals and customizable features make it both intuitive and adaptable for traders of all levels.

What It Does

This indicator generates buy and sell signals based on a sophisticated yet straightforward strategy:

Buy Signals: Triggered when the price is above VWAP, has recently retraced to the zone between two EMAs (default 12 and 21 periods), and a strong bullish candle closes above both EMAs.

Sell Signals: Triggered when the price is below VWAP, has retraced to the EMA zone, and a strong bearish candle closes below both EMAs.

Signal Filtering: A customizable cooldown period ensures that only the first signal in a sequence is shown, reducing noise while preserving opportunities for new trends.

Confidence Scores: Each signal includes an AI-inspired confidence score (0-100%), calculated from candle strength and price distance to VWAP, helping traders gauge signal reliability.

The indicator’s visuals enhance decision-making with dynamic gradient lines, a highlighted retracement zone, and clear signal labels, all customizable to suit your preferences.

How It Works

The indicator integrates several components that work together to create a cohesive trading tool:

VWAP: Acts as a dynamic support/resistance level, reflecting the average price weighted by volume. It filters signals to ensure buys occur in uptrends (price above VWAP) and sells in downtrends (price below VWAP).

Dual EMAs: Two EMAs (default 12 and 21 periods) define a retracement zone where the price is likely to consolidate before continuing its trend. Signals are generated only after the price exits this zone with conviction.

Retracement Logic: The indicator looks for price pullbacks to the EMA zone within a user-defined lookback window (default 5 candles), ensuring signals align with trend continuation patterns.

Candle Strength: Signals require strong candles (bullish for buys, bearish for sells) with a minimum body size based on the Average True Range (ATR), filtering out weak or indecisive moves.

Cooldown Mechanism: A unique feature that prevents signal clutter by allowing only the first signal within a user-defined period (default 3 candles), balancing responsiveness with clarity.

Confidence Score: Combines candle body size and price distance to VWAP to assign a score, giving traders an at-a-glance measure of signal strength without needing external analysis.

These components are carefully combined to capture high-probability setups while minimizing false signals, making the indicator suitable for both short-term and swing trading.

How to Use It

Add to Chart: Apply the indicator to a 15-minute chart (recommended) or your preferred timeframe.

Customize Settings:

VWAP Source: Choose the price source (default: hlc3).

EMA Periods: Adjust the fast and slow EMA periods (default: 12 and 21).

Retracement Window: Set how many candles to look back for retracement (default: 5).

ATR Period & Body Size: Define candle strength requirements (default: 14 ATR period, 0.3 multiplier).

Cooldown Period: Control the minimum candles between signals (default: 3; set to 0 to disable).

Candle Requirements: Toggle whether signals require bullish/bearish candles or entire candle above/below EMAs.

Visuals: Enable/disable gradient colors, retracement zone, confidence scores, and choose a color scheme (Neon, Light, or Dark).

Interpret Signals:

Buy: A green "Buy" label with a confidence score appears below the candle when conditions are met.

Sell: A red "Sell" label with a confidence score appears above the candle.

Use the confidence score to prioritize higher-probability signals (e.g., above 80%).

Trade Management: Combine signals with your risk management strategy, such as setting stop-loss below the retracement zone and targeting a 1:2 risk-reward ratio.

Why It’s Unique

The VWAP + EMA Retracement Indicator stands out due to its thoughtful integration of classic indicators with modern enhancements:

Balanced Signal Filtering: The cooldown mechanism ensures clarity without missing key opportunities, unlike many indicators that overwhelm with frequent signals.

AI-Inspired Confidence: The confidence score simplifies decision-making by quantifying signal strength, mimicking advanced analytical tools in an accessible way.

Elegant Visuals: Dynamic gradients, a highlighted retracement zone, and customizable color schemes (Neon, Light, Dark) create a sleek, futuristic interface that’s both functional and visually appealing.

Flexibility: Extensive customization options let traders tailor the indicator to their style, from conservative swing trading to aggressive scalping.

VWAP Separation Oscillator V5 (No Arrows)Okay, here is a draft description you can adapt for your TradingView publication. It starts from the basics and explains the concepts behind the indicator and how to interpret its visual elements.

VWAP Separation Oscillator

Summary

This indicator provides a normalized view of how far the current price has deviated from its Volume-Weighted Average Price (VWAP), helping traders identify potentially overbought or oversold conditions relative to recent VWAP dynamics. It calculates the price separation from VWAP and expresses it in terms of standard deviations (a Z-score), making it easier to gauge the statistical significance of the deviation.

Core Concepts Explained

What is VWAP?

VWAP stands for Volume-Weighted Average Price. It's a trading benchmark calculated by taking the total dollar value traded for every transaction (price multiplied by volume) and dividing it by the total shares traded for the day (or other chosen period).

Unlike a simple moving average, VWAP gives more weight to price levels where more volume occurred. Many institutional traders use it as a reference point for execution quality.

This indicator allows you to choose the "Anchor Period" (Session, Week, Month, etc.) which determines when the VWAP calculation resets.

What is VWAP Separation?

P

rice doesn't always stay at the VWAP; it naturally fluctuates above and below it.

"VWAP Separation" is simply the difference between the current price (Source) and the calculated VWAP value (Separation = Price - VWAP). A positive separation means the price is above VWAP; negative means below.

How Standard Deviation is Used:

While knowing the separation is useful, its significance can vary wildly between different stocks or market conditions. A $1 separation might be huge for one stock but tiny for another.

Standard Deviation is a statistical measure of how spread out data points are from their average. In this indicator, we calculate the standard deviation of the VWAP Separation over a specified Lookback Length. This tells us how volatile or dispersed the separation has been recently.

The Oscillator Line (Z-Score):

The main purple (or Green/Red) line plotted by this indicator is the Z-score of the VWAP Separation.

Formula conceptually: Oscillator Value = (Current Separation - Average Separation) / Standard Deviation of Separation

Interpretation: It tells you how many standard deviations the current separation is away from the average separation over the lookback period.

A value of +2.0 means the current separation is 2 standard deviations higher (more extended to the upside) than the average separation.

A value of -1.5 means the current separation is 1.5 standard deviations lower (more extended to the downside) than the average separation.

This normalization makes it easier to compare readings across different assets or timeframes and to define consistent thresholds for "extreme" deviations.

Visual Elements Explained

Oscillator Line: The primary line showing the Z-score value (explained above). Can optionally be colored Green/Red based on its slope (rising/falling).

Overbought Line (Solid Red): A user-defined level (default: 2.0). When the oscillator moves above this line, it suggests the price deviation above VWAP is statistically significant compared to recent history.

Oversold Line (Solid Green): A user-defined level (default: -2.0). When the oscillator moves below this line, it suggests the price deviation below VWAP is statistically significant compared to recent history.

Overbought/Oversold Zone Fills (Transparent Red/Green): These shaded areas appear only when the oscillator line enters the respective Overbought or Oversold territory (defined by the OB/OS Lines), visually highlighting these periods.

Zero Line (Dotted Gray): Represents the point where the current VWAP separation is exactly equal to the average VWAP separation over the lookback period. Crossings indicate shifts relative to this mean.

Zero Cross Markers (Orange 'X'): Small 'x' marks plotted directly on the oscillator line whenever it crosses the Zero Line, pinpointing these moments.

Potential Usage / Interpretation

Identifying Extremes: High positive values (above OB Level) or low negative values (below OS Level) can suggest the price move relative to VWAP might be over-extended and potentially due for a pause or pullback. Look for the oscillator turning back from these extremes.

Spotting Divergences: Look for discrepancies between price action and the oscillator.

Bearish Divergence: Price makes a new high, but the oscillator makes a lower high (often in the OB zone). Suggests weakening upside momentum relative to VWAP dynamics.

Bullish Divergence: Price makes a new low, but the oscillator makes a higher low (often in the OS zone). Suggests weakening downside momentum relative to VWAP dynamics.

Context is Key: This oscillator measures deviation from a specific benchmark (VWAP). Its interpretation should always be done within the context of the overall market trend, price structure (support/resistance), volume analysis, and potentially other confirming indicators.

Disclaimer: This indicator is a tool for analysis, not a standalone trading system. It does not provide financial advice. Always use risk management.

Settings Overview

Anchor Period: Determines how often the VWAP calculation resets (Session, Week, Month, etc.).

Source: The price data used for the separation calculation (default: hlc3).

Lookback Length: The number of bars used to calculate the average and standard deviation of the separation, influencing the oscillator's responsiveness.

Overbought/Oversold Levels: User-defined thresholds for identifying extreme Z-score values.

Color Oscillator Line: Option to color the oscillator line based on whether it's rising or falling.

Anchored VWAP Pro (Final Visibility Enhanced)This is a fully customizable Anchored VWAP (Volume Weighted Average Price) indicator designed for traders who prioritize precision, clarity, and macro trend analysis.

Unlike traditional VWAPs tied to daily or session data, this version allows you to manually anchor the VWAP to any candle in history—ideal for macro swing trading, cycle lows, breakouts, and reaccumulation phases.

Features:

• Manual Anchor Date: Set the exact year, month, and day for your VWAP to begin

• Custom Price Source: Choose between HLC3, close, or any OHLC-based input

• VWAP Bands: Two standard deviation bands for identifying overextension or fair value zones

• Full Visual Control:

• Toggle each band on/off individually

• Adjust color, line width, and line style (solid, dotted, dashed)

• Built for Clarity: Designed to stand out on both light and dark charts

This script is ideal for:

• Identifying macro confluence zones

• Defining risk during trend pullbacks

• Confirming breakout legitimacy

• Layering with other tools like Market Cipher, VRVP, and Fib levels

Inspired by the work of LonesomeTheBlue, Algokid, and other pros—this is a cleaner, more flexible and updated alternative for precision trading.

Script created and published by @ImmortalEmerson

For advanced swing traders, crypto analysts, and macro trend specialists.

VWAP 2.0 with desv + Initial Balance by RiotWolftrading🌟 Overview

This powerful tool is designed for traders who want to harness the power of the Volume Weighted Average Price (VWAP) alongside session-based ranges to make informed trading decisions. Whether you're a day trader or a swing trader, this indicator provides a clean and effective way to identify support, resistance, and market trends—all in one place! 💡

✨ Key Features

Auto-Anchored VWAP 📊

Automatically calculates the VWAP based on a user-defined anchor period (e.g., Daily, Weekly, Monthly).

Resets at the start of each period (e.g., daily for a Daily anchor).

Displays a customizable VWAP line with standard deviation bands to highlight key price levels.

Standard Deviation Bands 📏

Plots up to three sets of standard deviation bands above and below the VWAP (multipliers: 1.0, 2.0, 3.0).

Includes volume percentage labels to show where trading volume is concentrated. 📉

Session High/Low Range 🕒

Identifies the high and low prices within a customizable session (default: 12:00 to 15:31).

Draws horizontal lines at the session high and low, with dotted deviation lines for additional reference points.

Perfect for spotting key levels during your trading session! 🔑

Time-Based Range Box ⏰

Highlights a specific time window (default: 15:40 to 15:50) with a colored box showing the high and low prices.

Ideal for tracking price action during high-impact events like news releases or market opens. 📅

Alerts 🚨

Set up alerts for when the price crosses above or below the VWAP—never miss a potential trading opportunity!

⚙️ Settings

Customize the indicator to fit your trading style with these easy-to-use settings:

VWAP Settings

Timezone 🌍: Select your timezone (default: GMT+2) to align calculations with your local time.

VWAP Source 📈: Choose the price source for VWAP (default: hlc3 - average of high, low, close).

Std Deviation Multipliers 📐: Adjust the multipliers for the bands (default: 1.0, 2.0, 3.0).

Line Width ✏️: Set the thickness of the VWAP and band lines (default: 1).

Session Time ⏳: Define the session window for VWAP calculations (default: 08:00-18:00, all days).

Show Upper/Lower Bands 👀: Toggle visibility for each set of bands (default: Band 1 visible, Bands 2 & 3 hidden).

Range Settings

Range Start/End Time 🕙: Set the time window for the range box (default: 15:40 to 15:50).

Box Color 🎨: Customize the border color (default: blue).

Box Background Color 🖌️: Adjust the background color (default: light aqua, 90% transparency).

I created this indicator to provide a streamlined, clutter-free tool for traders who rely on VWAP and session-based analysis. It focuses on the essentials—VWAP, standard deviation bands, session high/low, and range box—without unnecessary overlays. I hope it helps you in your trading journey! If you have feedback or suggestions, feel free to share—I’d love to hear from you! 😊

Auto Anchored VWAPs for FuturesAbout the Script

This indicator automatically plots five anchored VWAPs based on predefined starting times, offering traders key reference points across multiple timeframes. These starting points are hardcoded and cannot be customized, ensuring consistency across all time zones. Below are the anchored VWAPs and their respective starting times:

NY Session: Starts daily at 9:30 AM EST

Globex: Starts daily at 6:00 PM EST

Weekly: Resets every Sunday at 6:00 PM EST

Monthly: Anchored to the first session of the month at 6:00 PM EST

Yearly: Anchored to the first session of the year at 6:00 PM EST

How to Use the Script

1) Add the script to your chart.

2) Select the appropriate Daylight Savings Time format.

3) Customize the visual appearance to your preference.

4) Click "OK" to apply the changes.

Once configured, the VWAP levels will automatically adjust based on the predefined timeframes.

How the Script Works

The script calculates and plots anchored VWAPs at the predefined starting times listed above. As each session, week, month, and year progresses, the corresponding VWAP is recalculated and updated on the chart, providing traders with dynamic insights into market trends and volume-weighted price action.

ScalpSwing Pro SetupScript Overview

This script is a multi-tool setup designed for both scalping (1m–5m) and swing trading (1H–4H–Daily). It combines the power of trend-following , momentum , and mean-reversion tools:

What’s Included in the Script

1. EMA Indicators (20, 50, 200)

- EMA 20 (blue) : Short-term trend

- EMA 50 (orange) : Medium-term trend

- EMA 200 (red) : Long-term trend

- Use:

- EMA 20 crossing above 50 → bullish trend

- EMA 20 crossing below 50 → bearish trend

- Price above 200 EMA = uptrend bias

2. VWAP (Volume Weighted Average Price)

- Shows the average price weighted by volume

- Best used in intraday (1m to 15m timeframes)

- Use:

- Price bouncing from VWAP = reversion trade

- Price far from VWAP = likely pullback incoming

3. RSI (14) + Key Levels

- Shows momentum and overbought/oversold zones

- Levels:

- 70 = Overbought (potential sell)

- 30 = Oversold (potential buy)

- 50 = Trend confirmation

- Use:

- RSI 30–50 in uptrend = dip buying zone

- RSI 70–50 in downtrend = pullback selling zone

4. MACD Crossovers

- Standard MACD with histogram & cross alerts

- Shows trend momentum shifts

- Green triangle = Bullish MACD crossover

- Red triangle = Bearish MACD crossover

- Use:

- Confirm swing trades with MACD crossover

- Combine with RSI divergence

5. Buy & Sell Signal Logic

BUY SIGNAL triggers when:

- EMA 20 crosses above EMA 50

- RSI is between 50 and 70 (momentum bullish, not overbought)

SELL SIGNAL triggers when:

- EMA 20 crosses below EMA 50

- RSI is between 30 and 50 (bearish momentum, not oversold)

These signals appear as:

- BUY : Green label below the candle

- SELL : Red label above the candle

How to Trade with It

For Scalping (1m–5m) :

- Focus on EMA crosses near VWAP

- Confirm with RSI between 50–70 (buy) or 50–30 (sell)

- Use MACD triangle as added confluence

For Swing (1H–4H–Daily) :

- Look for EMA 20–50 cross + price above EMA 200

- Confirm trend with MACD and RSI

- Trade breakout or pullback depending on structure

NY ORB, VWAP & EMAsIndicator is designed to display key technical analysis tools on your Trading View chart. It includes:

One of the key benefits of this indicator is that it allows Basic Trading View users to set VWAP, EMAs, and ORB in a single indicator. This is particularly useful for users who are limited to a single indicator on their Basic plan, as it provides a comprehensive view of market sentiment, trend, and potential breakouts without the need for multiple indicators.

Features

New York Opening Range Breakout (ORB): Plots the high and low of the first 15 minutes (configurable) of the New York trading session.

Volume Weighted Average Price (VWAP): Displays the VWAP line, which can be toggled on or off.

Exponential Moving Averages (EMAs): Plots four EMAs (9, 21, 50, and 200 periods), which can also be toggled on or off.

Customization

ORB Length: Choose from 5 or 15 minutes for the ORB calculation.

Show VWAP and EMAs: Toggle the visibility of the VWAP and EMA lines on or off.

Usage

This indicator is designed to help traders identify key market levels, trends, and potential breakouts during the New York trading session. The ORB can be used to gauge market sentiment, while the VWAP provides a benchmark for average price action. The EMAs offer additional trend analysis and can be used to identify potential support and resistance levels.

Multi-Timeframe Anchored VWAP Valuation# Multi-Timeframe Anchored VWAP Valuation

## Overview

This indicator provides a unique perspective on potential price valuation by comparing the current price to the Volume Weighted Average Price (VWAP) anchored to the start of multiple timeframes: Weekly, Monthly, Quarterly, and Yearly. It synthesizes these comparisons into a single oscillator value, helping traders gauge if the current price is potentially extended relative to significant volume-weighted levels.

## Core Concept & Calculation

1. **Anchored VWAP:** The script calculates the VWAP separately for the current Week, Month, Quarter (3 Months), and Year (12 Months), starting the calculation from the first bar of each period.

2. **Price Deviation:** It measures how far the current `close` price is from each of these anchored VWAPs. This distance is measured in terms of standard deviations calculated *within* that specific anchor period (e.g., how many weekly standard deviations the price is away from the weekly VWAP).

3. **Deviation Score (Multiplier):** Based on this standard deviation distance, a score is assigned. The further the price is from the VWAP (in terms of standard deviations), the higher the absolute score. The indicator uses linear interpolation to determine scores between the standard deviation levels (defaulted at 1, 2, and 3 standard deviations corresponding to scores of +/-2, +/-3, +/-4, with a score of 1 at the VWAP).

4. **Timeframe Weighting:** Longer timeframes are considered more significant. The deviation scores are multiplied by fixed scalars: Weekly (x1), Monthly (x2), Quarterly (x3), Yearly (x4).

5. **Final Valuation Metric:** The weighted scores from all four timeframes are summed up to produce the final oscillator value plotted in the indicator pane.

## How to Interpret and Use

* **Histogram (Indicator Pane):**

* The main output is the histogram representing the `Final Valuation Metric`.

* **Positive Values:** Suggest the price is generally trading above its volume-weighted averages across the timeframes, potentially indicating strength or relative "overvaluation."

* **Negative Values:** Suggest the price is generally trading below its volume-weighted averages, potentially indicating weakness or relative "undervaluation."

* **Values Near Zero:** Indicate the price is relatively close to its volume-weighted averages.

* **Histogram Color:**

* The color of the histogram bars provides context based on the metric's *own recent history*.

* **Green (Positive Color):** The metric is currently *above* its recent average plus a standard deviation band (dynamic upper threshold). This highlights potentially significant "overvalued" readings relative to its normal range.

* **Red (Negative Color):** The metric is currently *below* its recent average minus a standard deviation band (dynamic lower threshold). This highlights potentially significant "undervalued" readings relative to its normal range.

* **Gray (Neutral Color):** The metric is within its typical recent range (between the dynamic upper and lower thresholds).

* **Orange Line:** Plots the moving average of the `Final Valuation Metric` itself (based on the "Threshold Lookback Period"), serving as the centerline for the dynamic thresholds.

* **On-Chart Table:**

* Provides a detailed breakdown for transparency.

* Shows the calculated VWAP, the raw deviation multiplier score, and the final weighted (adjusted) metric for each individual timeframe (W, M, Q, Y).

* Displays the current price, the final combined metric value, and a textual interpretation ("Overvalued", "Undervalued", "Neutral") based on the dynamic thresholds.

## Potential Use Cases

* Identifying potential exhaustion points when the indicator reaches statistically high (green) or low (red) levels relative to its recent history.

* Assessing whether price trends are supported by underlying volume-weighted average prices across multiple timeframes.

* Can be used alongside other technical analysis tools for confirmation.

## Settings

* **Calculation Settings:**

* `STDEV Level 1`: Adjusts the 1st standard deviation level (default 1.0).

* `STDEV Level 2`: Adjusts the 2nd standard deviation level (default 2.0).

* `STDEV Level 3`: Adjusts the 3rd standard deviation level (default 3.0).

* **Interpretation Settings:**

* `Threshold Lookback Period`: Defines the number of bars used to calculate the average and standard deviation of the final metric for dynamic thresholds (default 200).

* `Threshold StDev Multiplier`: Controls how many standard deviations above/below the metric's average are used to set the "Overvalued"/"Undervalued" thresholds (default 1.0).

* **Table Settings:** Customize the position and colors of the data table displayed on the chart.

## Important Considerations

* This indicator measures price deviation relative to *anchored* VWAPs and its *own historical range*. It is not a standalone trading system.

* The interpretation of "Overvalued" and "Undervalued" is relative to the indicator's logic and calculations; it does not guarantee future price movement.

* Like all indicators, past performance is not indicative of future results. Use this tool as part of a comprehensive analysis and risk management strategy.

* The anchored VWAP and Standard Deviation values reset at the beginning of each respective period (Week, Month, Quarter, Year).

VWAP StrategyVWAP and volatility filters for structured intraday trades.

How the Strategy Works

1. VWAP Anchored to Session

VWAP is calculated from the start of each trading day.

Standard deviations are used to create bands above/below the VWAP.

2. Entry Triggers: Al Brooks H1/H2 and L1/L2

H1/H2 (Long Entry): Opens below 2nd lower deviation, closes above it.

L1/L2 (Short Entry): Opens above 2nd upper deviation, closes below it.

3. Volatility Filter (ATR)

Skips trades when deviation bands are too tight (< 3 ATRs).

4. Stop Loss

Based on the signal bar’s high/low ± stop buffer.

Longs: signalBarLow - stopBuffer

Shorts: signalBarHigh + stopBuffer

5. Take Profit / Exit Target

Exit logic is customizable per side:

VWAP, Deviation Band, or None

6. Safety Exit

Exits early if X consecutive bars go against the trade.

Longs: X red bars

Shorts: X green bars

Explanation of Strategy Inputs

- Stop Buffer: Distance from signal bar for stop-loss.

- Long/Short Exit Rule: VWAP, Deviation Band, or None

- Long/Short Target Deviation: Standard deviation for target exit.

- Enable Safety Exit: Toggle emergency exit.

- Opposing Bars: Number of opposing candles before safety exit.

- Allow Long/Short Trades: Enable or disable entry side.

- Show VWAP/Entry Bands: Toggle visual aids.

- Highlight Low Vol Zones: Orange shading for low volatility skips.

Tuning Tips

- Stop buffer: Use 1–5 points.

- Target deviation: Start with VWAP. In strong trends use 2nd deviation and turn off the counter-trend entry.

- Safety exit: 3 bars recommended.

- Disable short/long side to focus on one type of reversal.

Backtest Setup Suggestions

- initial_capital = 2000

- default_qty_value = 1 (fixed contracts or percent-of-equity)

Multi-TF Volume & Price Analysis[BullByte]This indicator offers a comprehensive view of market dynamics by combining volume and price analysis across multiple timeframes. It calculates key metrics—such as bullish/bearish volume percentages, relative volume (RVol), cumulative volume delta (CVD), and price change percentages—for each timeframe that you choose (for example, 1, 3, 5, and 15 minutes). Here are the main features in simple terms:

- Multi-Timeframe Analysis:

The tool analyzes volume and price action from four different timeframes simultaneously. This means you get insights from short-term and slightly longer-term trends in one view.

- Volume Breakdown:

It splits the volume into bullish and bearish parts by comparing closing and opening prices. This helps you see how much of the trading volume is driving the market upward versus downward.

- Relative Volume & Spike Detection:

It calculates relative volume (current volume compared to a moving average) and flags any significant volume spikes based on a customizable multiplier. This feature helps identify unusual trading activity.

- Volume Smoothing Option:

For a cleaner signal, you can enable a smoothing option (using an exponential moving average) to reduce noise in the volume data.

- Advanced Summary:

The indicator combines volume data, price changes, and volume spikes to produce an overall market summary for each timeframe—labeling conditions as “Bullish Strong,” “Bullish Moderate,” “Bearish Strong,” “Bearish Moderate,” or “Neutral.”

- Cumulative Overview:

In addition to individual timeframe analysis, it aggregates the data to offer a cumulative view. This includes a collective bullish/bearish percentage, overall CVD, and even a simplified volume level (Low, Normal, or High).

- Customizable Dashboard:

All these metrics are neatly displayed in a dashboard on the chart. You can customize its position and text size. The dashboard uses dynamic, color-coded cells to instantly convey the market sentiment—making it easy to spot trends at a glance.

- VWAP Integration:

Finally, the dashboard includes VWAP information, providing an additional layer of context to the price action.

Overall, this indicator is designed to provide a quick yet thorough snapshot of market conditions, enabling traders to make more informed decisions with a clear visual representation of volume and price activity across different timeframes.

Multiple VWMATradingView Indicator: Multiple VWMA

This TradingView indicator allows you to display up to five separate Volume Weighted Moving Averages (VWMAs) directly on your price chart.

What it does:

Plots 5 VWMAs: It calculates and draws five distinct VWMA lines (or other styles) on the chart.

Volume Weighting: Unlike simple moving averages, a VWMA gives more weight to prices where trading volume was higher, potentially offering a clearer picture of the trend strength confirmed by volume.

Highly Customizable: Each of the five VWMAs can be configured independently through the indicator's settings panel. For each one, you can set:

Length: The lookback period (number of bars) used for the calculation.

Source: The price data to use (e.g., close, open, high, low, hl2, etc.).

Timeframe: You can calculate each VWMA based on a different timeframe than the one currently displayed on your chart (e.g., view daily VWMAs on an hourly chart). Leave blank to use the chart's timeframe.

Offset: Shift the VWMA line forwards or backwards on the chart by a specific number of bars.

Style: Choose how each VWMA is displayed (Line, Histogram, or Cross).

Overlay: The VWMAs are plotted directly over the price bars for easy comparison.

Purpose:

This indicator is useful for traders who want to analyze trends using multiple volume-weighted perspectives simultaneously. By comparing VWMAs of different lengths or based on different timeframes, you can gain insights into short-term vs. long-term trends, potential support/resistance levels, and the significance of price movements based on accompanying volume.