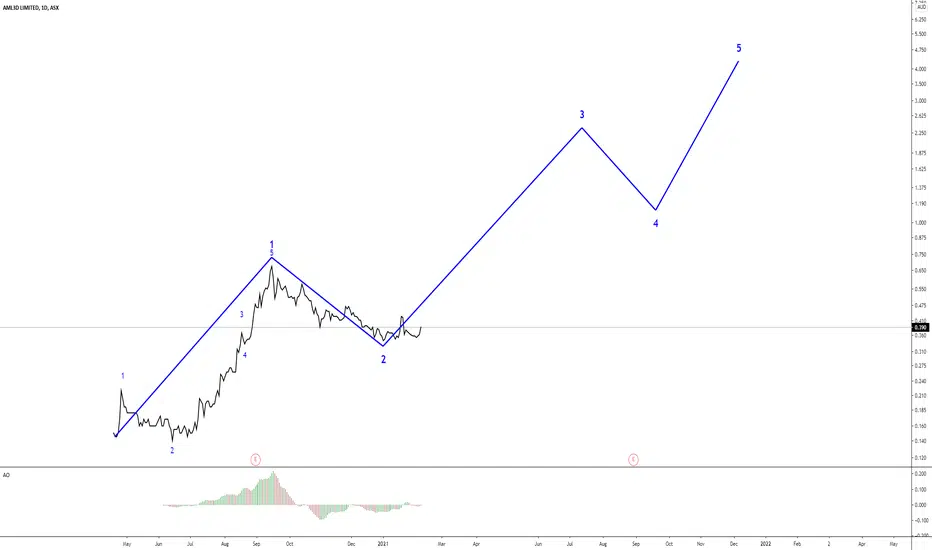

Bearish yet fundamentally bullishTechnical:

Short term: Bearish

I cannot find any bullish signal at this moment.

Here are some insights about Perennial Value Management Limited (PVM), Option Expiry Date, Tax Loss, and hedge fund liquidation rumor. I think Sell-Off is more likely finishing in June .

Recently PVM has disclosed the massive sale of 2,097,925 AL3 shares.

Their total average price is $0.254413. ((Total Cost – Total Proceeds)/number of current shareholdings = 3,939,746.08/15,485,635). At current market price of $0.18, they are making the loss of $1,152,331.78 (29.25%)

However, PVM is so far recognising the profit of $2,137,376.83 in 2021 using FIFO (First In, First Out) method. In 2020, PVM recognised the loss of $186,728.29. They have left with 1,069,994 shares which they bought below the current market price. The rest of the holding of 14,415,641 shares have an average of $0.396591 .

The recent notice confirmed that PVM was the buyer of 2.1M special cross (S3XT) on 18/03/2021 at 10:43 am.

PVM might recognise more PROFIT (not a LOSS) this June with 1,069,994 shares but they will not sell any other shares to reduce their current profit (Fund performance). I’m sure that PVM will make the SP higher for their benefit (At least to 200D SMA level) in near future after their 2021 financial year recognition.

5,279,513 options - expiry date 30/06/2021, exercise price of $0.3. Management might release something positive for their benefits before the expiry date. Recent notice for change of Director’s interests, exercised portions have been PURCHASED around IPO time . You can refer to the last financial year statements/prospectus.

Tax-loss – some OZ investors might sell for tax purposes before the end of June. Hence, selling pressure to ease from July.

According to Luke Laretive, CEO of Seneca Financial Solution stated about the hedge fund liquidation and sale of their AL3 holding ,

“… after a major shareholder, a US-based hedge fund, was put into liquidation and has been aggressively selling down the stock for months. I suspect this selling is finished and management is scaling up for growth, … If it happens how I think it will happen, the stock will see new all-time highs .”

Source: www.dmarge.com

Fundamental:

Medium to long term: Bullish

Today’s focuses are on the quality aspects of WAM.

Please refer last two posts for

- profitability and quality of AML3D (AL3) products and its possibility of successful commercialisation.

- the reason to value AL3 as a hybrid of manufacturing and software business.

If you are unsure about WAAM technology, I highly recommend downloading PAS 6012:2020 from shop.bsigroup.com for free. I was going to write about the quality aspects of WAM before finding this information, but PAS 6012 is a cheat sheet and must-read. If you read, you will understand why AML3D technology will be commercialised successfully.

If you are worried about WAM quality such as heat accumulation issues etc after watching Alex Kingsbury RMIT presentation on YouTube , AML3D overcame those issues. Otherwise, DNV or Lloyds will not certify AM3D products. Alex Kingsbury is RMIT Ph.D. Student and working with AML3D. Her positive AML3D article is linked here. Search keywords “ Alex Kingsbury, Wire AM, A new Additive technology, November 11, 2019” amhub.net.au

I’ve found an interesting person from the Rowland Metalworks Arcemy Launch photos (Available at AML3D Facebook page). Michael Smith from Naval Group Australia (Subsidiary of French naval defence group, closely related to the future submarine program). Naval Group (France) was the first 3D print (WAAM) a full-scale propeller blade for military use using robots and tools from Yaskawa Group in Japan. “Obtaining military naval quality requires rigorous development. Nearly three years of R&D”. To search the article keyword” Naval Group, WAAM, 3dprint.com, January 29, 2021”. I sense AML3D is on the table for defence works through the Rowland Metalworks and Naval Group. Great hidden evidence of AML3D technology is legitimate.

If I have opportunities and time, I will share some of my insights in technologies with AML3D such as IoT, Big Data, Topology optimisation, Digital warehouse , etc. I believe the revolution is accelerating with converging technologies. To contrary to SP action, I feel AML3D’s fundamental has been increasing in value . It’s so much more valuable than the IPO period.

“The intelligent investor never dumps a stock purely because its share price has fallen, always asks first whether the value of the company’s underlying businesses has changed” Benjamin Graham

AL3 trade ideas

$AL3 dropped a long way but, thats a fine impression of a bottom2M cross traded will help form a bottom.

35 is the obvious level to break now. will be plenty of res under 40 without news.

Lets see.

Long Legged Doji - AL3 - Still forming a bull flag?Technical:

Short term: Bearish/Bullish

Markets generally saw the today’s update as no surprise. However, it finished with the long legged doji candlestick during market sell off today. Not bad.

Current Support Level $0.35 – Strong support level so far.

Next Support Level $0.3 – option exercise price.

I still think it is forming a bull flag pattern (Long term).

Fundamental:

Medium to long term: Bullish

Today’s focuses are the profitability and quality of AML3D (AL3) products and the possibility of successful commercialisation. Please refer to my previous post that explained the reason to value AL3 as a hybrid of manufacturing and software business.

AL3 has illustrated in its presentations that the company can deliver cheaper, faster, and stronger products than typical subtractive and powder additive 3D technology companies. This led me to investigate into the technology and investment opportunity closely last year. Great technology does not guarantee the juicy return on capital. This is one of my insights about AL3’s profitability and the quality of products back then.

RAM3D is one of the largest 3D metal printing service providers in Australasia. The NZ company commercialises Selective Laser Melting (SLM) product using the Reinshaw AM250 SLM Machine. SLM technology uses metallic powders with laser beam produces relatively small to medium sized components. The CEO mentioned about its profitability at the 4th International Forum on Additive Manufacturing on 9 Sep 2020. His concern was RAM3D’s margin had been getting tight over years. Obviously, metal powders are not that cheap. He also told that the consumption of the inert gas (Argon) had been much higher than the system specification. I decided that it was not worth investing in company who use supplied machineries in 3D printing sector. The bar of entry seems incredibly low, hence, the higher competition with lower margin. Apart from the consultancy role, it does not seem to have any value-added service/product.

Meanwhile, AL3 developed its own machinery. It uses affordable metal wires instead of expensive metal powders (same alloy type). I have not done much research on these areas. I feel metal powder requires higher level of processing, so must be limited supplier (Mainly overseas?) and less availability of different materials. After the COVID, many manufactures are looking to improve their supply chain issue. Manufactures prefer easily sourced materials, then, wires seem promising. I guess that AL3 can keep much higher profit margin than RAM3D because AL3 can add value to its own innovative technology and machinery - WAM (DED system, originated from Wire Arc Additive Manufacturing - WAAM, my understanding is identical) and uses cheaper materials but same grade alloy.

AL3 focuses medium to large sized parts rather than smaller/medium parts with use of the SLM machinery.

• Renishaw AM250: Build volume 250 x 250 x 365 mm

• WAM technology: Unlimited build volume but not suited for small size parts.

Safety concerns powder Additive Manufacturing (AM) vs wire AM

• Difficulty in handling – Metal powder can be harmful to human (required breathing apparatuses and ventilation). Metal wires are easier to handle.

• Storage issue: Metal powder can be flammable (Aluminium and Titanium). I assume that wires are easier to store.

According to the Cranfield University site (www.waammat.com), WAAM performs better in cost savings, material utilisation, mechanical properties, part size and platform flexibility. On the other hand, powder bed technology (I think same as SLM, also known as Direct Metal Laser Melting – DMLM, or Laser Powder Bed Fusion – LPBF) comes with higher level of complexity and accuracy. Therefore, potential application for each technology is different. After all, I am a believer that every technology has its own use case.

By the way, Dr Paul Colegrove (Key AL3 Personnel), who is the engineering technology manager at AL3. He used to be the senior lecture at the Cranfield University. The University started up (Spin-out) the WAAM3D. You can find interesting details, key search words “WAAM, Dr Filomeno Martina, Cranfield University”.

Lastly, can AL3 succeed in commercialisation of the metal 3D printer? It is highly likely that AL3 technology will. WAAM technologies are founded based on extensive academic research (e.g., Cranfield’s University), therefore, clearly different from technology (Company) in research and development stage. WAAM technologies have been commercialised by Norsk Titanium, RAMLAB and WAAM3D. Most importantly, AL3’s management and boards are focused and experienced. AL3’s WAM has been certified by Lloyd’s Register (Great for marine industry) and well funded. I feel confident that they will engage customers and gain the commercial contracts.

AL3 targets various sectors such as marine, mining, energy, and defence. It is important to understand that it takes time to reach commercial contracts and executes through confidentiality agreement. I always recall “The stock market is a device for transferring money from the impatient to the patient – Wattern Buffett”. If I have opportunities and time, I will share some of my insights in the quality aspects of WAM such as porosity, thermal overheating, and certification etc.

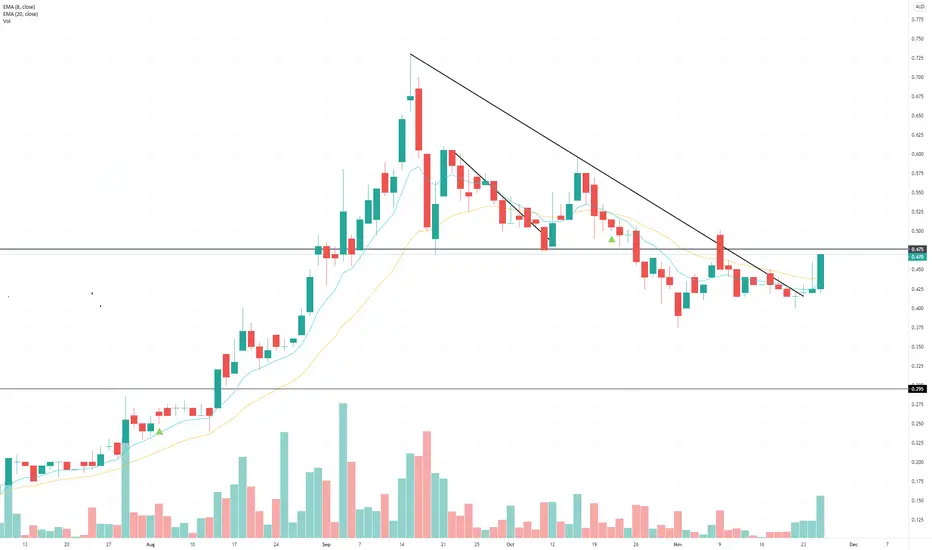

Bull Flag - Breaking Out? AL3Technical:

Bull Flag Pattern - may break out depending on any positive market news.

Fundamentals:

Some of the notable technologies in Tesla is to use cylindrical battery cells and its battery management system. Tesla achieved powerful batteries at a lower cost against peers. It was simply a revolution of combining technologies. Panasonic is one of the battery suppliers for now (Tesla plans to produce its own batteries in future, LG chem and CATL supply cells to Shanghai factory) but performance of its share price (6752) is not matched to Tesla’s one.

AML3D uses metal wires, welding robots and its 3D printing management system. Metal wires are easily available. ABB robotics appears to supply the core welding robots. AML3D combines them to make the Arcemy – Wire Additive Manufacturing (WAM) 3D metal printer. Its competitive advantage is cheaper, faster, and less wasteful than conventional metal manufacturing process.

When majority of us think about the Tesla, we would imagine the Model s/x/3 etc. We might compare its performance against Porsche Taycan/ Lamborghini Aventador etc. To enhance Prosche/Lamborghini, we probably need to take them to specialised custom car workshops. I wonder how many people would do this. On the other hand, Tesla could enhance its performance by updating software. The software update will enhance all the vehicles at the same time (Fast and scalable).

Too often, people are comparing the tangible objects only. Both Tesla and AML3D create value from converging technologies. In here, my focus is their software technology. The Arcemy can enhance its printing process and performance by software update. In not far future, factory/warehouse will have on-demand nature of 3D printer. Digital warehouse/inventory may become new trend. It will be possible to improve its printing product each time by modifying its design (with Topology optimisation, big data, machine learning etc). It is highly likely to revolutionise the manufacturing process against conventional manufacturing process (Forging, subtractive manufacturing etc). I guess that the Arcemy Software uses the algorithm to optimise the printing (Factors to considers can be wall width, wire feed speed, deposition speed, printing process etc). I sense a lot of errors and trials to develop the software and feel that it would not be that easy to copy the software capability. Hence, I think the ultimate value is created from its software.

How do you value the AML3D? As manufacturing business? Software business? I value it as hybrid.

If I have time, I might post my insights about the quality side as wells as comparison to other metal 3D printing methods. I am not here to offend Tesla; I love Tesla and respect Elon Musk. I know Tesla’s success cannot be explained in this short context.

$AL3 poor action recently needs to clear 47.5Just noting though, 3DA is a far superior chart, however

AL3 cashflow $423k for 1/4. 3DA was $63k. I think one is the real deal and one is far from proving itself. But the market is very good at discounting future growth. Lets see.

$AL3 nice bottoming pattern. 39/40 the break on volume... nice bottoming pattern here with volume pattern suggesting a pump is coming. See how it acts this week.

The business model needs proving and some chunky contracts are anticipated. Lets see.

$AL3 double bottom tl break. may not come back. reckon 50 should provide a good resistance level to buy or launch.

$AL3 - would like to see this tighen up now.Recent cap raise which would presumably have some contracts or product development releases, or both attached to it. Measured move? $0.90? Guess it all depends on how disruptive the Sales team are, pun intended.

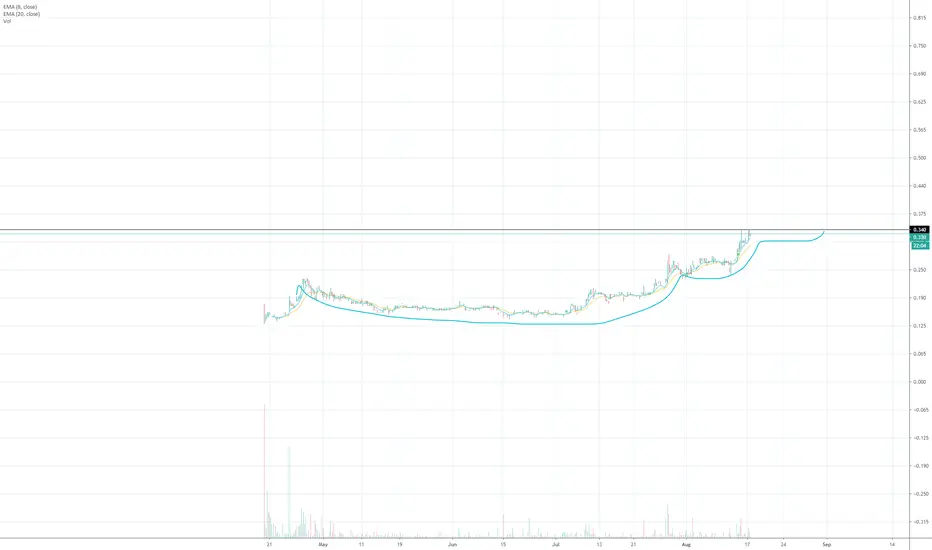

AL3:ASX - AML3D - 3D Metal Printer - Up 320% since debutAL3 was pointed out to me by @zbfairlane here on TV. Company looks interesting. I would imagine the ability to be able to 3D print metal is definitely something we are going to see more and more of as opposed to the traditional making a cast and pouring, welding and shaping. If its anything like household 3D printing it should allow for some complex shapes and approaches in industrial design and manufacturing we perhaps haven't seen before. Had a big 10% pullback today on no news so could be a good entry area if interested. Worth a watch.

$AL3 accumulation. clear res at 34.Really liking the action on this one. Hopefully it tightens up and volume drops off around this 34 level for me to add. Ideally another 14 days or so. But Im usually wrong on these guesses.

$AL3 - acting well. Nice breakin play at 28.5. Nice tight action on this one. Good volume going through the pivot. See how they close it.

$AL3 - IPO base and flag setup. Buying break of 25.Really like the setup here. Recent IPO base (8 weeks) and now flagging above all the right levels. See if they've got anything in the next few days.