AUDUSD LONGPrice entered a 15min Demand zone, gave a fake choch and a real choch

Entered on a extreme demand on the 1min timeframe

When price hits 5rr i secure 50% and stop to breakeven.

AUDUSD trade ideas

AUD/USD continue with the UptrendOn AUD/USD , it's nice to see a strong buying reaction at the price of 0.64470 .

There's a significant accumulation of contracts in this area, indicating strong buyer interest. I believe that buyers who entered at this level will defend their long positions. If the price returns to this area, strong buyers will likely push the market up again.

Strong S/R zone from the past + Uptrend and high volume cluster are the main reasons for my decision to go long on this trade.

Happy trading

Dale

AUDUSD has submitted breakoutAUDUSD has submitted breakout on one hour time frame price is in uptrend,good chance for buying once price show some correction buy limit order is recommended.

GBP/JPY Short, GBP/USD Short, AUD/CAD Short and AUD/USD ShortGBP/JPY Short

Minimum entry requirements:

• If structured 1H continuation forms, 1H risk entry within it.

GBP/USD Short

Minimum entry requirements:

• Corrective tap into area of value.

• 4H risk entry or 1H risk entry after 2 x 1H rejection candles.

Minimum entry requirements:

• Tap into area of value.

• 1H impulse down below area of value.

• If tight non-structured 5 min continuation follows, reduced risk entry on the break of it.

• If tight structured 5 min continuation follows, reduced risk entry on the break of it or 5 min risk entry within it.

• If tight non-structured 15 min continuation follows, 5 min risk entry within it if the continuation is structured on the 5 min chart or reduced risk entry on the break of it.

• If tight structured 15 min continuation follows, reduced risk entry on the break of it or 15 min risk entry within it.

AUD/CAD Short

Minimum entry requirements:

• 1H impulse down below area of value.

• If tight non-structured 15 min continuation follows, 5 min risk entry within it if the continuation is structured on the 5 min chart or reduced risk entry on the break of it.

• If tight structured 15 min continuation follows, reduced risk entry on the break of it or 15 min risk entry within it.

AUD/USD Short

Minimum entry requirements:

• 1H impulse down below area of interest.

• If tight non-structured 15 min continuation follows, 5 min risk entry within it if the continuation is structured on the 5 min chart or reduced risk entry on the break of it.

• If tight structured 15 min continuation follows, reduced risk entry on the break of it or 15 min risk entry within it.

AUDUSD Short PotentialTechnical Analysis

The AUDUSD pair is currently trending upwards due to USD weakness. The pair seems overbought based on stochastics > 80%

Fundamental Analysis

The RBA is widely expected to cut interest rates at its upcoming 20th May meeting. Inflation has fallen substantially based on previous RBA meeting minutes which warrants a current 25 basis points rate cut with more expected in the future.

Trade Setup

Short positions are preferred based on the current AUDUSD strength with a potential entry around .6547 which is near the 61.8% Fib level with a S/L at .6562 and T/P at the 50% Fib level around .6437.

AUDUSD LONG FORECAST Q2 W19 D5 Y25

AUDUSD LONG FORECAST Q2 W19 D5 Y25

Professional Risk Managers👋

Welcome back to another FRGNT chart update📈

Diving into some Forex setups using predominantly higher time frame order blocks alongside confirmation breaks of structure.

Let’s see what price action is telling us today!

💡Here are some trade confluences📝

✅Weekly 50 EMA

✅Intraday 15' order block

✅Tokyo ranges to be filled

✅Intraday bullish breaks of structure to be confirmed

🔑 Remember, to participate in trading comes always with a degree of risk, therefore as professional risk managers it remains vital that we stick to our risk management plan as well as our trading strategies.

📈The rest, we leave to the balance of probabilities.

💡Fail to plan. Plan to fail.

🏆It has always been that simple.

❤️Good luck with your trading journey, I shall see you at the very top.

🎯Trade consistent, FRGNT X

AudUsd Expanding TriangleAudUsd is making a bullish structure in the more recent timeframes. Based of specific patterns, I'd say this inclines to be an expanding triangle, which price just broke above, and it seems to stay above, after failing to go lower lows near the top. Price broke above, made a retest and I think it is more wise to buy after it made a positive reaction to this well known expanding triangle pattern.

Aussie Perks Up As Asia NapsAUD/USD closed last week at the highest level of 2025 and has extended the move today, pushing above the key 200-day moving average. The rally coincides with further strength in the offshore-traded Chinese yuan, which also finished last week at 2025 highs against the U.S. dollar.

While the price action is undeniably bullish—mirrored by strengthening momentum indicators—light turnover due to holidays across much of Asia warrants caution. The European open may offer a clearer read on whether this break above the 200DMA will stick.

If there’s no immediate reversal during European trade, traders may consider establishing longs with a tight stop below the 200DMA, targeting resistance near .6550. Alternatively, a move back beneath the 200DMA—echoing Friday’s reversal—could open the door for shorts, with uptrend support around .6370 and the 50DMA below that as possible downside targets.

Good luck!

DS

Potential bullish rise?The Aussie (AUD/USD) has bounced off the pivot which is a pullback support and could rise to the 1st resistance which has been identified as an overlap resistance.

Pivot: 0.6391

1st Support: 0.6258

1st Resistance: 0.6647

Risk Warning:

Trading Forex and CFDs carries a high level of risk to your capital and you should only trade with money you can afford to lose. Trading Forex and CFDs may not be suitable for all investors, so please ensure that you fully understand the risks involved and seek independent advice if necessary.

Disclaimer:

The above opinions given constitute general market commentary, and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended only to be informative, is not an advice nor a recommendation, nor research, or a record of our trading prices, or an offer of, or solicitation for a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation and needs of any specific person who may receive it. Please be aware, that past performance is not a reliable indicator of future performance and/or results. Past Performance or Forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or any information supplied by any third-party.

Week of 5/4/25: AUDUSD AnalysisAfter a hellish week of consolidation, price has made its move higher (finally) and we're back to a trendy chart.

My analysis the beginning of the week shows 2 POIs that I am interested in for longs, and if it breaks the level that I pointed out bearish, I will look for shorts.

Thanks for tuning in!

Major News:

FOMC - Wed

Unemployment - Thurs

AudUsd Trade IdeaAU is showing a clear range between 64350 and 63600. With last weeks higher time frame closing below the previous high at 64500 I would want to see smaller frames shifting bearish below 64350 to confirm our move to the downside where 63600 could potentially get smacked again in the range continuation.

AUDUSD looking Bullish?!!Hello traders I hope you are having a wonderful week!!!

We have this wonderful resistance which we broke out of and now we might be looking at buys.

This resistance has also been a market high for a few days now.

That white line there is my Pivot for next week and it serves as a great spot to put my SL.

Falling towards 50% Fibonacci support?AUD/USD is falling towards a support level, which is a pullback support that aligns with the 50% Fibonacci retracement, and could bounce from this level toward our take-profit target.

Entry: 0.6418

Why we like it:

There is a pullback support level that lines up with the 50% Fibonacci retracement.

Stop loss: 0.6394

Why we like it:

There is a pullback support level that is slightly above the 78.6% Fibonacci retracement.

Take profit: 0.6466

Why we like it:

There is a pullback resistance level.

Enjoying your TradingView experience? Review us!

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Everest Fortune Group’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Everest Fortune Group.

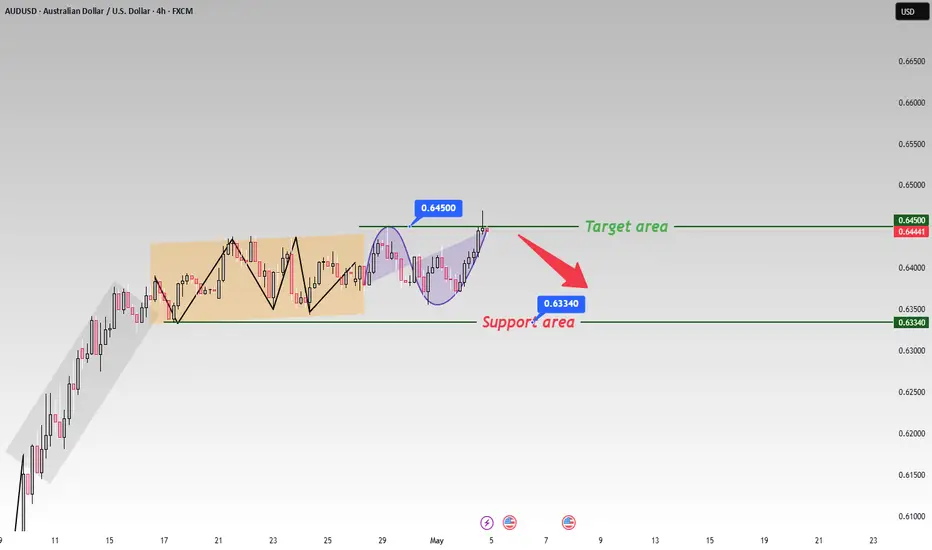

The trend next weekJudging from the price trend presented in the chart, the current market is clearly in a bearish state 📉. Previously, after the price reached the key resistance level of 0.64500, it failed to break through effectively and continue the upward trend. Instead, it entered a consolidation pattern 📊. This indicates that the bullish forces encountered strong resistance near this price level and found it difficult to push the price higher 👎.

It is expected that in the coming period, without significant positive news stimuli, the price is highly likely to continue its downward trend 📉. Investors should closely monitor whether the support level of 0.63340 holds 👀. If this support level is broken, they may consider selling short on rallies ⏬.

⚡⚡⚡ AUDUSD ⚡⚡⚡

🚀 Sell@0.6500 - 0.6450

🚀 TP 0.6350 - 0.6300

Accurate signals are updated every day 📈 If you encounter any problems during trading, these signals can serve as your reliable guide 🧭 Feel free to refer to them! I sincerely hope they'll be of great help to you 🌟

AUDUSD potential bullrunI am expecting from the weekly timeframe to form the wick that means the retracement from 2h timeframe and in the zone of AOI daily to have a shift of structure then continue to the upside, We'll see!

DISCLAIMER! The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by me.

My Thoughts #005My thoughts are that the pair will sell...

The daily trend is very much bullish and with trend once it have made a new High(HH)

We need to see it printing a new Low(HL)

Confirmation?

I see a Consolidation/Accumulation and the market is creating Highs confirmation for the manipulation what would come next would be distribution...

The pair might just continue buying

So use proper risk management

Let's do the most

$AUDUSD: low risk long entry GM gents, hope you're having a nice weekend.

I was looking at FX after hearing Warren Buffett's remarks about FX ('wise to own more currencies other than the Dollar') and noticed there's a buy signal in the Aussie Dollar.

I was long FX:USDJPY for a couple days already, so this is the same theme of a rebound in economically sensitive risk assets and commodity currencies.

Best of luck!

Cheers,

Ivan Labrie.

AUD/USD Opening Trends and Trading Strategies Next WeekThe AUD/USD has been in a range - bound fluctuation recently. 📈 In the short term, if the price can stay above the support level of 0.63340 and market risk - appetite sentiment rises, the AUD/USD is expected to challenge the target level of 0.64500. 🎯 However, if it breaks below the support level, it may trigger further downward adjustments. 📉

⚡⚡⚡ AUDUSD ⚡⚡⚡

🚀 Buy@0.6350 - 0.6380

🚀 TP 0.6400 - 0.6450

Accurate signals are updated every day 📈 If you encounter any problems during trading, these signals can serve as your reliable guide 🧭 Feel free to refer to them! I sincerely hope they'll be of great help to you 🌟

AUD/USD, Are Bull Set for a Breakout ?This analysis dates from the 3rd of May, this is in no way financial advice and should be taken into account in an objective way. Make your own opinion about it, don't take it for granted.

- AUD/USD is trading around the 0.64000 area on the daily chart, it has been consolidating around that area since April 21st following a 7 consecutive bull rally. Where it is heading to next still needs to be determined. Nevertheless, there is a clear Expanding Triangle dating since the start of 2025. (see image attached),(13th January, 03rd of Feb, 09th of April for the lower bar and 27 January, 20th Feb, 17th March, 23rd of April for the upside channel).

- This expanding triangle is similar to the one identified on NZD/USD which had an upside breakout and is now consolidating around the 0.59200.

- Whether there is an upcoming BO on Aussie Dollar is still TBT, but odds slightly favor the bulls following the strong rally in the first half of April. Nevertheless, it has been trading in a trading range since April 21st and there are no confirmed breakout yet. Needs to be closely watched in the coming days!! If bulls manage to get consecutive strong bull bars, this could set the stage for an measured move up for at a minimum a test of the 0.66000 area (downside channel from Feb 2021 to Nov 2024 on the Monthly).

- The Bear reversal case is harder to argue for, as they only managed to get one strong bear bar (04th April), with no follow through selling, The market has been trading for longer on the upper bracket of the extending triangle which means the market participant agree more on higher prices. Stay tuned for further updates !! Peace.

AUDUSD LOOKING FOR A PULLBACK TO 0.62700 AND PUMP TO 0.685AUDUSD looking for a retarcement to the goldbach FVG zone at 0.62700 and then a impulse to the higher order block to complete the return to origin

The VWAP Blueprint: Your Gateway to Smart Money MovesVWAP: Volume Weighted Average Price

What is VWAP?

VWAP stands for Volume Weighted Average Price. It’s a trading benchmark that gives the

average price an asset has traded at throughout the day, weighted by volume. This makes it

more accurate than a simple moving average, especially for intraday analysis.

Unlike regular moving averages that treat every price equally, VWAP emphasizes price levels

where heavier trading occurred, providing a realistic snapshot of the true average market price institutions and algorithms are interacting with.

The VWAP Bounce + Rejection Entry Strategy helps you enter trades at optimal zones of value

using the Volume-Weighted Average Price (VWAP). This dynamic line acts as a magnet for

price and often becomes a bounce zone when volume aligns.

Instead of guessing support or resistance levels, this strategy lets you use VWAP as a real-

time value guide, waiting for price to pull into it, show rejection, and bounce away with

momentum.

How VWAP Works

The VWAP is calculated cumulatively from the market open:

VWAP = (Cumulative Price × Volume) / Cumulative Volume

With each tick or candle:

Multiply the price by volume.

Add it to the previous cumulative total.

Divide by the total volume so far.

This means VWAP resets daily and builds throughout the session, offering real-time insight

Into what traders are willing to pay based on volume-weighted interest.

Why VWAP Matters

When price pulls back into VWAP and bounces with rejection, it signals that traders are

defending value. Smart money often uses VWAP as a tool for entries or exits. When you align

with that behavior and combine it with a clean rejection candle, you get a high-probability

trade setup that’s based on logic and flow, not emotion.

1. Institutional Benchmark

Institutions and smart money often aim to buy below VWAP (to secure a better-than-average

price) and sell above VWAP. So the line often acts as a magnet or barrier where decisions

cluster.

2. Intraday Bias Gauge

Price above VWAP: Buyers dominate; bullish bias.

Price below VWAP: Sellers control; bearish bias.

3. Support/Resistance & Mean Reversion

VWAP behaves like a dynamic equilibrium level. Price frequently:

Pulls back to VWAP during trends

Here's a clear down trend 50 and 200 ma cross over. Await a pull back to trend or ma for continuation.

Reverts to VWAP in consolidations

Finds support/resistance at or around VWAP

How to Use VWAP in Trading

1. Trend Confirmation

Use VWAP as a bias filter: if price is cleanly above, favor longs if below, favor shorts.

Combine it with higher highs/lows (or lower highs/lows) to validate trend strength.

2. Entry Opportunities

In an uptrend: look for pullbacks to VWAP as a buy zone

In a downtrend: look for retests of VWAP as a short opportunity.

3. Mean Reversion Strategy

If price is far extended from VWAP, and volume shows divergence or exhaustion, consider

fading the move with a target toward VWAP (especially in range-bound sessions).

4. Anchored VWAP

You can anchor VWAP to specific candles, like a major high, low, or news release, to gauge

value zones within a custom context.

Best Timeframes for VWAP

Intraday trading (1min to 15min): Ideal for scalpers and day traders.

VWAP resets daily it’s not designed for swing trading unless you're using anchored VWAP.

Pro Tips

Don’t use VWAP in isolation pair it with:

Market structure (HH/LL, BOS/CHoCH)

Volume spikes or divergence

Liquidity zones (order blocks, FVGs, imbalance)

Session opens (London/NY open confluence)

Use VWAP for confluence with other tools, not as a single trigger.

VWAP is more than just a line it's a window into the heartbeat of the market. It shows where

real money is positioned and whether you’re trading with or against that flow.

Used with structure and context, VWAP becomes a weapon for precision entries, smart risk, and clean execution.

Vwap entry types

1. VWAP Bounce (Mean Reversion Entry)

Best for: Range-bound or early in the session.

Entry: Price pulls back to VWAP and shows signs of rejection (e.g., pin bar, engulfing candle).

Confirmation: Look for confluence with support/resistance, order blocks, or volume spikes.

Stop: Below the recent swing low (if long).

Target: Prior high or key level.

2. VWAP Break and Retest (Trend Continuation)

Best for: Trending markets.

Entry: Price breaks above VWAP with momentum and retests it from the other side.

Confirmation: Lower time frame bullish structure, bullish candle on retest.

Stop: Below VWAP or structure low.

Target: pivot levels or structure high, fib levels.

3. VWAP Reclaim (Reversal Entry)

Best for: Capturing a shift in momentum.

Entry: Price moves below VWAP, then reclaims it (closes back above with strength).

Confirmation: Break of market structure + volume surge

Stop: Below reclaim candle.

Target: Range high or key fib levels.

4. VWAP Confluence with Other Indicators

Combine with:

Moving Averages: e.g., 9, 50 and 200 SMA OR EMA

Fibonacci retracement levels

Order blocks / Liquidity zones

Pivot points

Use VWAP as a dynamic support/resistance level and enter when multiple signals align.

Vwap examples

A Simple breakdown on AUDUSD Let's take a closer look and see how indecisive the AUDUSD is gonna be going back and forth and from my Analysis I'll be capitalizing from every move of the price ...

AUDUSD: Neutral View First Buy and Then Sell! Hey everyone!

Our first buy swing entry is going swimmingly! We’ve got over 500 pips running positively, and we reckon price can keep going up and then when it hits our selling zone, you can swing sell too. This is a fantastic opportunity where we can wait for price to do its thing and then when it reaches the sell zone, we can execute our order. But if you’re feeling adventurous and want to take a bit of a risk, you can take a buy entry at the given point and keep it up until it reaches our sell area.

With just one shot, we can make two entries!

Good luck and trade safely!

Thanks a bunch for your unwavering support! 😊

If you’d like to lend a hand, here are a few ways you can contribute:

- Like our ideas

- Comment on our ideas

- Share our ideas

Cheers,

Team Setupsfx_

❤️🚀