Crunch time for Crisp (r) ?CRISPR Therapeutics

Short Term - We look to Buy a break of 59.19 (stop at 54.06)

Further upside is expected and we look to set longs in early trade. A bullish reverse Head and Shoulders has formed. A break of yesterdays high would confirm bullish momentum. A higher correction is expected. Although the anticipated move higher is corrective, it does offer ample risk/reward today.

Our profit targets will be 70.94 and 79.82

Resistance: 60.00 / 70.95 / 80.00

Support: 58.00 / 50.00 / 42.00

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

CRSP/N trade ideas

Long-term descending wedge breakout - BULLISHA clear breakout pattern on multiple timeframes on the classic descending wedge supported by bullish MACD.

$CRSP ~ Correction looks complete...Correction looks complete and now we are working on a five wave structure to the upside. Would expect upside to fair market value as shown.

#CRSP $CRSP easy follow the buy sell why not to double check for assured profit before you pay a dime

Easy line to follow and simple chart be your guide here , it works for a week in #trade

Long (potential takeover, solid pipeline, tons of cash)- potential aim for takover (I suppose by VRTX ) . Company has 2.5B in cash, no debt with market cap about 4.5B$ (EV = 2.0 B)

- solid pipeline and probably will be first who get FDA approval for commercial CRISPR product

- got most of up front payment for milestones in CRISPR among competitors ( about 1b$ from Vertex and collaboration with Bayer). BEAM for example got only 300m$ in up front payment, NTLA even less.

That means CRSP has enough cash for 4 years R&D without share offering and sustain global recession.

No brainer alpha at a cheap price1) Crisper has a lot of cash on hand to survive through tightening of QE and fund pipeline without dilution

2) Potential takeover by $VRTX or other compamy at current prices VERY possible.

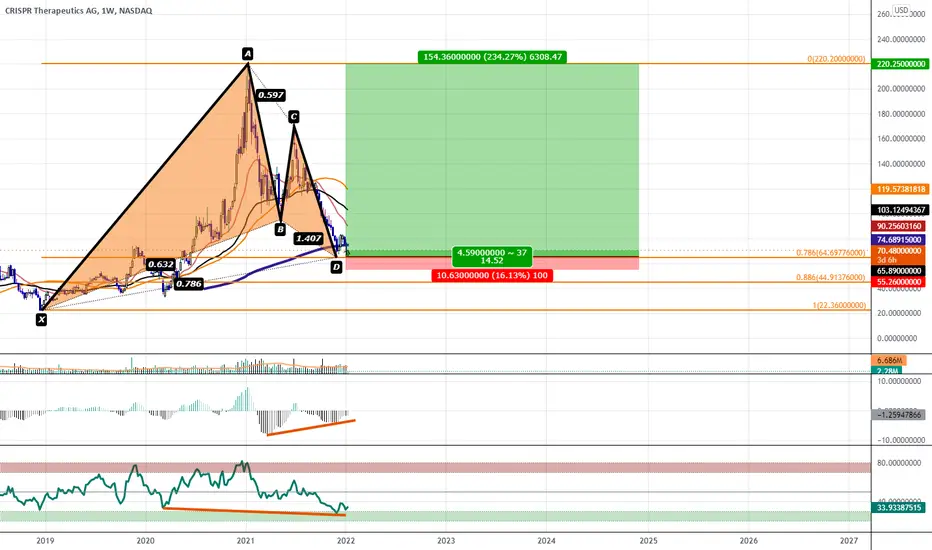

Bullish Gartley with Bullish Divergence Visible on the WeeklyWe have Classic Divergence on the MACD and Hidden Bullish Divergence on the RSI visible on the Weekly chart at the PCZ of a Bullish Gartley.

CRISPR- The future of medicine?I would buy 40% at this price

then if the price drops to $30-40 I'd buy the rest of the 60%

crispr call..aejfj;agiojagwejga ldak;jjewjg ag akgje;aijgwei vaie;jgijewpogjpwaeg wamaj;wefj pij;aewpfjoefj

$crsp - consolidation continues...I expect this to consolidate for the next few weeks.. probably into Q1/Q2 2022... leading to an eventual breakout to retest ATH

CRISPR Therapeutic needs to break 83.46. This is a critical testCrispr has been moving up since the Morning star break out on 13th December. Its further progress hinges on breaking the 83.46 resistance. It has tried piercing this resistance twice but failed. The resistance line at 83.46 and the upward support channel formed since 14th December at $70.37 is intersecting 83.46 on 28th December and CRSP has to break out before that to make any further progress. Option strategies can be deployed to exploit the opportunity either way.

nice downtrend break here! looking for a rally now 🍿fresh breakout past a 5 month downtrend on CRSP ! if it holds and doesn't break back into the trend potential price targets for early 2022 area 98.31-113.89-129.47

like and follow for more 💘

CRSPCRSP It's time to update the idea. The care turned out to be very deep, although this option of leaving for zone 77 was supposed. Now we have dropped out of the channel a little, we will count for an error, we are also holding on to the ema200 during the week, we have formed hidden divergences during the week, taking into account the potential of the company, the growth of xbi and the VRTX partner may be interesting.

It may still come down and test the "trend", but we are already at a good level

50sma is the next resistanceBroke through the yellow downward trendline today with volume. The 50sma coincides with my gray trendline. Big upside if it can break through that.

Time to buy CRSPCatalysts coming in 2022 and weekly trend changes based on heiken ashii candles, plus the bounce at 74+- which was prior resistance, plus analyst ratings make this an attractive buy for me at these levels.

CRSP on a major weekly level. What's coming next? Today we will take a look at CRISPR Therapeutics.

Which are the main technical elements we can see here?

a) The price is against a major Support/Resistance level, working since 2018. The price reaction on these zones tends to provide solid insight into future movements.

b) Let's assume the price bounces on the current zone; what can we expect?

- A movement towards the descending trendline around 100.00. IF that happens, that would be a take-profit level for me. Why? Because we tend to observe corrections once the price reaches a major level. You don't want to be insight a sideways movement for 100 days

c) Let's assume that the price breaks the current level and keeps falling. What can we expect?

- A movement towards the ascending trendline around 50.00. That would be the next level where I would start thinking again about bullish reversals.

d) I'm a position trader. What is the most relevant level right now to develop setups?

-If that's your case, I want to see first a breakout of the descending trendline; IF that happens, I want to see a correction of around 50 days. IF that is the case, I will be interested in trading that breakout for the long term. However, at the moment, we are far away from that situation, and I would stay away from this chart for long-term setups.

Thanks for reading! Feel free to share your view of this in the comments.

CRISPR BUY OR NOT TO BUY..?Third Quarter 2021 Financial Results

• Cash Position: Cash, cash equivalents, and marketable securities were $2,477.4 million as of

September 30, 2021, compared to $2,589.4 million as of June 30, 2021. The decrease in cash of

$112.0 million was primarily driven by cash used in operating activities to support ongoing

research and development of the Company’s clinical and pre-clinical programs.

• Revenue: Total collaboration revenue was $0.3 million for the third quarter of 2021, compared to

$0.1 million for the third quarter of 2020. Collaboration revenue primarily consisted of revenue

recognized in connection with our collaboration agreements with Vertex.

• R&D Expenses: R&D expenses were $105.3 million for the third quarter of 2021, compared to

$71.0 million for the third quarter of 2020. The increase in expense was driven by the development

activities supporting the advancement of the hemoglobinopathies program and wholly-owned

immuno-oncology programs, as well as increased headcount and supporting facilities, related

expenses.

• G&A Expenses: General and administrative expenses were $24.4 million for the third quarter of

2021, compared to $21.5 million for the third quarter of 2020. The increase in general and

administrative expenses for the year was primarily driven by headcount-related expenses.

• Net Loss: Net loss was $127.2 million for the third quarter of 2021, compared to a net loss of

$92.4 million for the third quarter of 2020.

crisprtx.gcs-web.com

MACD: BEARISH CROSS

RSI: OVERSOLD

VOLUME: LOW

CURRENT SUPPORT @ 1.272 FIB

1.618 IS YOUR IMPULSE TARGET FOR A BREAK IN EITHER DIRECTION

Puzzled on this one honestly, looks like it wants to go lower, but we'll see at the weekly close. Keep an eye on the SPY index.

DYOR

PRACTICE RISK MANAGEMENT

GOOD LUCK

Return to the mean-Covid ignored. We returned to the mean.

-Purple area = consolidation zone = buy zone.

CRISPR is a truely amazing discovery. Imagine if we could perfectly edit genes within 5 or 10 years. I don't think everyone understands how big this is. Good luck! Target 1 = double top, other 2 the fibonacci extensions.

Edit: Don't buy before we stay above the 20MA.