Could Microstrategy be a 1 Trillion dollar mcap company?!Microstrategy and Michael Saylor evoke a spectrum of opinions, with analysts offering a diverse range of potential future valuations.

High risk, high reward!

The destiny of Microstrategy’s market capitalization is clearly linked to Bitcoin’s performance. The company has been utilizing debt to acquire the cryptocurrency, aiming to create significant spreads. This leverage is the reason why the stock has significantly outperformed Bitcoin throughout 2024.

I am confident that Bitcoin can indeed reach $200k, with a potential upper price target of $250K for this cycle, indicating a potentially explosive Q3 and Q4.

The lingering question is how much additional FOMO and premium Saylor can cultivate for his leveraged vehicle in such an environment?

That's why charting is such a key component to any personal investing strategy IMHO, as we navigate these markets.

MSTR trade ideas

MSTR - EWAVESThis analysis of MicroStrategy (MSTR) is rooted purely in the principles of Elliott Wave Theory. We are closely monitoring both the inner and outer wave degrees to identify the ongoing structure, potential reversals, and continuation patterns. The goal is to map the impulsive and corrective phases across multiple timeframes, giving a high-probability roadmap of price action. This approach helps in understanding the market’s fractal nature and positioning for key inflection points based on wave maturity.

MSTRFVG broken so mstr is a moon guys i have shares from last week but most of my money is in nvidia if im right ill make 6 figures off of this bounce

$MSTR bear flag forming; Daily $350 targetHello, quick mobile chart posting here. Simple looking bear flagging forming. Bitcoin having some downside action, I imagine Saylor will be buying some Bitcoin soon again as well. This should see $350. Looking for a short. + geopolitical turmoil hits crypto/Bitcoin the hardest and most violent. The 20 and 50 EMA are aligned as well with the Supertrend Downtrend showing $350.

WSL.

Dead Cat BounceOn the daily level, we see a 5.09% risk on the upside, whereas on the downside the risk factor comes in at 4.07% for now. From a risk perspective, resistance on a closing basis stands at 40685, yet the risk on the downside begins at 37135.

MSTR Long IdeaIF Bitcoin breaks new ATH next few weeks, MSTR cup and handle impossible to ignore with a target of 1.618 fibonacci extension as target 1......

Moonboi thoughts.

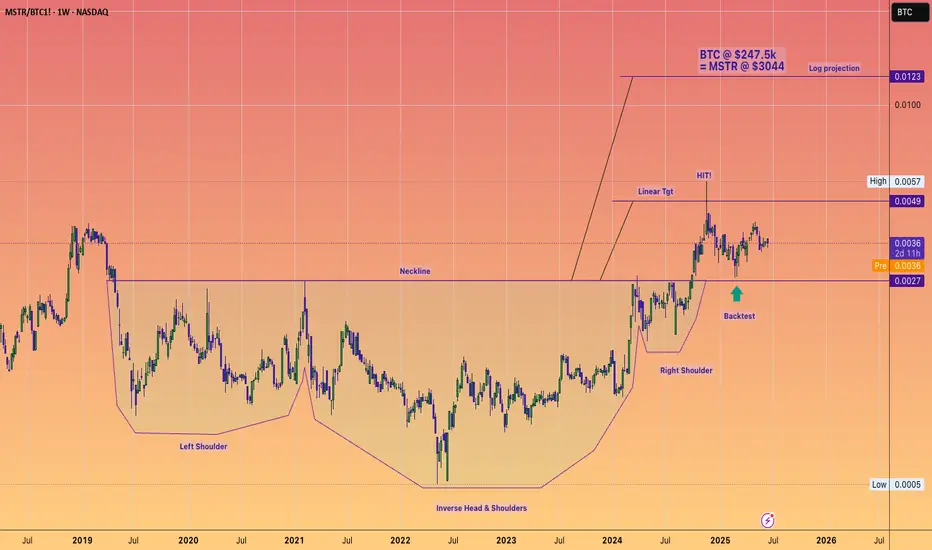

MSTR in SatoshisI'm touching base on MSRT/BTC because we had another touch of this overhead - confirming the overhead basically, and predicting that if we touch this overhead again, we get a breakout.

Nothing has changed in the gameplan. It's just taking time. Time is a rare luxury, and most people don't have it, so the market works to strip the impatient and give to the patient. The market is tuned against you, and still you think you can outwit the market, but it's impossible if you don't have time, and very few do.

$MSTR ONCE IN A LIFETIMEMSTR working on an inside month

Looking for a breakout if we can clear the monthly HIGH last add on the 618 Fibonacci was A HUGE WINNER!

Will keep yall posted here all I ask is drop a LIKE for me!

Navigating MSTR’s Price Swings: A Smart Options ApproachOverview

MicroStrategy (MSTR) has continued to capture market attention due to its aggressive Bitcoin strategy and significant stock price volatility. In 2025, MSTR surged 41% in one quarter but also reported a massive $4.22 billion net loss in Q1, raising concerns about long-term financial stability. Analysts remain divided, setting price targets ranging from $200 to $650, largely dependent on Bitcoin’s performance and broader market conditions.

Key Developments Impacting MSTR

✔ Bitcoin Exposure: MSTR maintains a large Bitcoin position, making its stock highly correlated to BTC’s price movements.

✔ AI Integration: The company is investing in AI-driven products, which could provide diversification outside of Bitcoin.

✔ Institutional View: Analysts remain split on MicroStrategy’s valuation due to its uncertain revenue model.

✔ Macro Volatility: Market-wide sentiment, interest rates, and crypto regulations will influence MSTR’s trajectory.

Options Strategy for the Week

🚀 Iron Condor Setup for June 6 Expiration

To capitalize on MSTR’s volatility while managing risk, an Iron Condor strategy is structured within a controlled range:

- Inner Range: Sell Calls at 395 and Puts at 335

- Coverage: Buy Calls at 415 and Puts at 315

✅ Objective: Profiting from sideways price movement while minimizing exposure to extreme volatility.

✅ Risk Management: If MSTR breaks above 415 or below 315, the long positions hedge against excessive losses.

mstr/ibitthis is might be a good chart to use to see when the convertible bond holders of mstr are trading the gamma...

Back to 400+ , SoonMSTR on inv h&s look to be going to 391. Over Could make the gap a magnet. Just idea ( education only)

MicroStrategy: The Dumbest Bet on WallStreetMicroStrategy: The Bitcoin Bet Masquerading as a Tech Company

Introduction: A Software Company Turned Crypto Casino

Once upon a time, MicroStrategy was a business intelligence firm. Today, it’s a Bitcoin holding company disguised as a software business.

Its market cap has ballooned to over $100 billion, not because of its software, but because of its aggressive Bitcoin purchases. Investors aren’t buying a company—they’re buying a leveraged bet on Bitcoin.

And that bet? It’s built on debt, dilution, and dangerous financial engineering.

The Math Problem: MicroStrategy’s Obscene Valuation

MicroStrategy is worth three times the value of its Bitcoin holdings. Let that sink in.

If you buy MicroStrategy stock, you’re effectively paying three times the price of Bitcoin. It’s like buying Bitcoin at $245,000 per coin when the actual market price is far lower.

This isn’t investing, it’s financial insanity.

The Debt Trap: How MicroStrategy Keeps the Illusion Alive

MicroStrategy’s entire strategy revolves around issuing debt to buy more Bitcoin. It has borrowed $7.27 billion through convertible bonds.

Here’s how the cycle works:

MicroStrategy issues debt at low interest rates.

It uses the money to buy Bitcoin.

The stock price rises because investors think it’s a genius move.

The company issues more shares to raise more money.

It buys more Bitcoin—and the cycle repeats.

This is not a sustainable business model. It’s a Ponzi-like structure that depends entirely on Bitcoin’s price continuing to rise.

The Accounting Trick: Hiding the Losses

MicroStrategy has been misleading investors with custom financial metrics. It created terms like BTC Yield and BTC $ Gain to make its Bitcoin strategy look profitable.

But in reality? It recently disclosed a $5.91 billion unrealized loss on its Bitcoin holdings. And when that news broke, its stock dropped 8.67% in a single day.

This isn’t a company, it’s a high-stakes gamble.

The Risk: What Happens When the Bubble Bursts?

MicroStrategy’s survival depends on Bitcoin’s price never crashing. If Bitcoin falls, MicroStrategy’s stock collapses.

And here’s the worst part:

If Bitcoin crashes, MicroStrategy might have to sell its holdings, triggering a death spiral.

If investors lose confidence, the company can’t issue more debt, and the illusion falls apart.

If regulators step in, MicroStrategy’s entire strategy could be dismantled.

This isn’t a safe investment. It’s a ticking time bomb.

Conclusion: The Dumbest Bet on Wall Street

MicroStrategy isn’t a tech company. It’s a leveraged Bitcoin casino.

Investors aren’t buying innovation, they’re buying hype, debt, and financial engineering. And when the illusion fades, reality will come crashing down.

So ask yourself: Are you investing in a business? Or are you just buying the dream—before it bursts?

MSTR - The Saylor in the Storm!Hello TradingView Family / Fellow Traders. This is Richard, also known as theSignalyst.

📈MSTR has been overall bullish trading within the rising channel marked in blue. (log chart)

Currently, it is in a correction phase within the falling red channel.

Moreover, the red zone is a strong demand.

🏹 Thus, the highlighted blue circle is a strong area to look for buy setups as it is the intersection of demand and lower trendlines acting as non-horizontal support.

📚 As per my trading style:

As #MSTR approaches the blue circle, I will be looking for bullish reversal setups (like a double bottom pattern, trendline break , and so on...)

📚 Always follow your trading plan regarding entry, risk management, and trade management.

Good luck!

All Strategies Are Good; If Managed Properly!

~Rich

Wedge pattern - Bullish Strategy (MSTR)My expectations for June for Microstrategy stock aka Strategy. Ofc, It all depends heavily on BITSTAMP:BTCUSD

PONZI Running out of steam TOP has been in moon bois1HR bear flag LOADING!!

Look at all the JUICY gaps to fill below. Yum Yum get ya sum!!

MSTR I Pullback and More Potential GrowthWelcome back! Let me know your thoughts in the comments!

** MSTR Analysis - Listen to video!

We recommend that you keep this pair on your watchlist and enter when the entry criteria of your strategy is met.

Please support this idea with a LIKE and COMMENT if you find it useful and Click "Follow" on our profile if you'd like these trade ideas delivered straight to your email in the future.

Thanks for your continued support!Welcome back! Let me know your thoughts in the comments!

Strategy Set To Drop —Selling Bitcoin?If you knew a stock was going to crash but this stock is related to Bitcoin and always moves with Bitcoin but now is about to detach, would you tell others?

Bitcoin is already trading at a new All-Time High and six weeks green. Ok, let's forget about Bitcoin because this is about MicroStrategy (now Strategy).

The MSTR stock is bearish now. Very bearish.

The top happened in November 2024.

9-May 2025 we have a long-term lower high. Days at resistance and this lower high is confirmed.

A scandal is about to be uncovered?

A change of "strategy"? Hah, nice play on words.

Is strategy going to have a change of strategy?

This change of strategy obviously will end up screwing everybody who holds this stock?

I don't know... I mean, who knows.

Here is what I know. The chart signals are pointing down. Bearish confirmed so, down we go.

Namaste.

MSTR Weekly Options Trade Plan 2025-05-24MSTR Weekly Analysis Summary (2025-05-24)

Summary of Each Model’s Key Points

Grok/xAI Report

Technicals: Short-term and daily charts show bearish momentum but oversold conditions (5-min RSI ~22, price near lower Bollinger Band) hint at a bounce. Sentiment: Elevated VIX (22.29), negative Bitcoin-bet headlines, insider sell-offs; max pain at $400 may cap upside. Direction: Moderately Bearish with potential for a relief rally. Trade: Buy $370 call at $13.00, aiming for +25% ($16.25), stop at 20% loss ($10.40), 65% confidence.

Claude/Anthropic Report

Technicals: Deep bearish momentum below all EMAs; M5 RSI oversold, daily RSI near oversold. Sentiment: Rising VIX, mixed Bitcoin headlines, heavy put open interest at $350–$360. Direction: Moderately Bearish but conflicting bounce signals. Trade: No trade—confidence only 45%.

Llama/Meta Report

Technicals: Bearish trend on both timeframes; oversold M5 RSI. Sentiment: Elevated volatility; mixed news; max pain theory. Direction: Moderately Bearish. Trade: Buy $367.50 put (ask $12.30–bid $11.85), profit +20%, stop 50%, 70% confidence.

Gemini/Google Report

Technicals: Overwhelming bearish across EMAs, RSI, MACD, price breaks on high volume. Sentiment: VIX rising, negative news, skewed options flow. Direction: Strongly Bearish. Trade: Buy weekly $310 put (est. ask ~$0.70), target 100–200% gains, stop at $0.35, 65% confidence.

DeepSeek Report

Technicals: Bearish on both charts but oversold; mixed reversal vs. continuation signals. Sentiment: VIX up, mixed news, distant max pain. Direction: Neutral/Unclear. Trade: No trade—confidence 55%. Areas of Agreement and Disagreement

Agreement

Broadly bearish technical setup: price under EMAs, negative MACD, RSI oversold short term. Elevated volatility (VIX ~22) supporting larger swings. Weekly expiry options, with traders positioned for downside (heavy put OI).

Disagreement

Trade bias: Grok favors a call bounce; Llama and Gemini prefer deep-OTM puts; Claude and DeepSeek opt out. Strike choice: Ranges from near-the-money calls ($370) to far-OTM puts ($310). Confidence thresholds and risk/reward preferences differ, leading to divergent trade/no-trade conclusions. Conclusion and Recommendation

Overall Market Direction Consensus: Bearish (various intensities from moderate to strong).

Recommended Trade: Buy a naked weekly put.

• Strike Selection: $355 put offers a balance of liquidity (OI 2,042), premium ($7.45 ask), and proximity to current price (downside leverage without needing an extreme move). • Expiry: 2025-05-30 weekly. • Premium: $7.45 (within or near preferred risk range). • Entry Timing: At market open. • Profit Target: +25% (~$9.31). • Stop Loss: –20% (~$5.96). • Position Size: 1 contract. • Confidence Level: 65%.

Key Risks and Considerations

A short-term bounce could spike implied vol and lift call skew, hurting put value. Support at $362 may hold, capping downside. Elevated volatility could widen spreads; ensure limit orders. Maintain strict stop-loss to prevent outsized premium decay losses.

TRADE_DETAILS (JSON Format)

{ "instrument": "MSTR", "direction": "put", "strike": 355.0, "expiry": "2025-05-30", "confidence": 0.65, "profit_target": 9.31, "stop_loss": 5.96, "size": 1, "entry_price": 7.45, "entry_timing": "open", "signal_publish_time": "2025-05-25 09:30:00 UTC-04:00" } 📊 TRADE DETAILS 📊 🎯 Instrument: MSTR 🔀 Direction: PUT (SHORT) 🎯 Strike: 355.00 💵 Entry Price: 7.45 🎯 Profit Target: 9.31 🛑 Stop Loss: 5.96 📅 Expiry: 2025-05-30 📏 Size: 1 📈 Confidence: 65% ⏰ Entry Timing: open 🕒 Signal Time: 2025-05-24 14:57:32 EDT

Disclaimer: This newsletter is not trading or investment advice but for general informational purposes only. This newsletter represents my personal opinions based on proprietary research which I am sharing publicly as my personal blog. Futures, stocks, and options trading of any kind involves a lot of risk. No guarantee of any profit whatsoever is made. In fact, you may lose everything you have. So be very careful. I guarantee no profit whatsoever, You assume the entire cost and risk of any trading or investing activities you choose to undertake. You are solely responsible for making your own investment decisions. Owners/authors of this newsletter, its representatives, its principals, its moderators, and its members, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission, CFTC, or with any other securities/regulatory authority. Consult with a registered investment advisor, broker-dealer, and/or financial advisor. By reading and using this newsletter or any of my publications, you are agreeing to these terms. Any screenshots used here are courtesy of TradingView. I am just an end user with no affiliations with them. Information and quotes shared in this blog can be 100% wrong. Markets are risky and can go to 0 at any time. Furthermore, you will not share or copy any content in this blog as it is the authors' IP. By reading this blog, you accept these terms of conditions and acknowledge I am sharing this blog as my personal trading journal, nothing more.

Short MicroStrategy as Bitcoin Volatility Intensifies

Targets:

- T1 = $355.43

- T2 = $343.68

Stop Levels:

- S1 = $375.00

- S2 = $385.00

**Wisdom of Professional Traders:**

This analysis synthesizes insights from thousands of professional traders and market experts, leveraging collective intelligence to identify high-probability trade setups. The wisdom of crowds principle suggests that aggregated market perspectives from experienced professionals often outperform individual forecasts, reducing cognitive biases and highlighting consensus opportunities in MicroStrategy.

**Key Insights:**

- MicroStrategy continues to exhibit a strong correlation with Bitcoin price movements due to its extensive cryptocurrency holdings. This linkage makes the stock especially vulnerable to Bitcoin's ongoing volatility.

- With Bitcoin showing signs of weakness and skepticism surrounding its near-term recovery, MicroStrategy faces heightened bearish pressure, compounded by its leveraged exposure to the crypto market.

- The company’s business model, combined with significant shareholder dilution, places additional risks on equity holders during times of unfavorable cryptocurrency market conditions.

**Recent Performance:**

MicroStrategy has seen a sharp pullback from its 52-week highs of $543 to its current price of $369.51, following a substantial 31% retracement. This decline mirrors Bitcoin's recent 4% dip, showcasing the tight alignment between the two assets. While the stock previously attempted to recover from its support near the 200-period moving average, it has struggled to maintain an upward trajectory amidst continued crypto-related volatility.

**Expert Analysis:**

Market experts highlight the critical risks in MicroStrategy’s strategy, particularly in its decision to fund Bitcoin purchases through debt and equity issuances. While this leverages its bullish thesis on Bitcoin, it significantly amplifies risks when sentiment turns bearish.

Overall, analysts forecast limited upside compared to downside risks, advising caution and favoring short positions. The underperformance of MicroStrategy relative to Bitcoin—attributed to operational inefficiencies and shareholder dilution—further underscores the pessimism around the stock’s outlook.

**News Impact:**

Recent updates about MicroStrategy’s $2.1 billion share issuance for Bitcoin acquisitions have heightened the perception of risk surrounding the company's equity. This reliance on external funding and its singular focus on Bitcoin make the stock acutely sensitive to cryptocurrency dynamics. As Bitcoin struggles to regain upward momentum, MicroStrategy’s share price faces ongoing pressure, aligning with wider bearish sentiment in the crypto market.

**Trading Recommendation:**

MicroStrategy remains a high-risk, Bitcoin-sensitive equity, making it an attractive short opportunity in the current environment. Targets are set at $355.43 (T1) and $343.68 (T2), with stop-loss thresholds carefully managed at $375.00 (S1) and $385.00 (S2). Traders are advised to maintain disciplined risk controls to navigate potential reversals, but the overall bearish setup supports a strong short positioning outlook at this time.

$MSTR Is Preparing For A Dive...NASDAQ:MSTR : We cannot ignore the downside risks at this point. With $430.35 intact, NASDAQ:MSTR is poised for a significant downward move toward the March lows or lower to complete wave (C) of a simple zigzag correction.

Bitcoin Income: STRK vs IBIT – Dividends, Covered CallsThis video provides a performance breakdown between two Bitcoin-related financial instruments—STRK (Strike) and IBIT—through the lens of passive income generation. I compare traditional buy-and-hold strategies with more active income tactics such as covered calls. Key insights include:

STRK provided the best return YTD (26%) and yielded approximately 1.54% in passive dividends, requiring minimal effort—just buy, hold, and collect.

IBIT, while slightly trailing in growth (13%), is optimized for a covered call strategy, offering an impressive 6% income yield through active options trading.

The analysis highlights the trade-off between simplicity and engagement—STRK is more passive-friendly, while IBIT offers higher yields for those willing to manage options.

This is ideal for tech-savvy investors exploring Bitcoin ETFs and derivative income strategies, weighing convenience versus return potential.

MSTR....it's happening (GET OUT)MSTR is insanely fragile and has been pumped with hot air for a while now. Good to leverage with MSTZ :) Best of luck and always do your own due diligence

MSTR: Island = Evening StarAnother key detail is that MSTR has gapped down.

And with a gap up on 8 May, the area above is now an island.

If MSTR closes in this area, then if we blended the island into 1 candle, then an Evening Star pattern is printing.

Also considering that this move began with a high momentum upside shakeout ,this is starting to look quite bearish.

And so this may be a leading indicator for Bitcoin.

Not advice