Possible Scenario for the Bond FundSimply took a previous move the Bond Fund already made, and inverted it, copy pasted and voila. It has already happened before

TLT trade ideas

Do we continue the wedge…Bonds have been hit hard and Crypto at Ath trend lines, do we need to finish the wedge

Bottom in for bonds, flight to safety trade coming soon $100+If we look at the chart of TLT, you can see that we're forming a bottoming reversal pattern.

We had a spike low down to $83 back to the middle of May and have now reclaimed the structure. I think that move marked the bottom.

I think it's very likely that bonds spike in the near future, if they can make it over the $92 resistance level, then I think price will see continuation and likely break the pattern finding the first resistance at that $101 level.

That said, I think this is the start of a larger move higher in bonds that will take us all the way up to the top resistance levels over the course of the next few years before the move is done and we start the long term trend in rates higher.

TLT short - warning signs from JapanTLT is making 20-day lows (red candles in the main chart), while continuing to make 20-week lows on a weekly chart (not shown). Meanwhile, looking at a proxy of net buying/selling (bottom panel), we have flipped from buying to selling.

Looking at Japanese bond yields, 10-year JGBs (JP10Y) just broke out of tight range. This is the third attempt to trade above ~1.59% recently, which we saw earlier today. As Japan's is one of the world's leading overseas investors, this is an obvious warning sign for bonds globally.

There is good risk/reward to short bonds here, with a stop-loss if the price closes at a 20-day high. If a 20-day high is made, the candles will change color from red to green.

Both indicators (Breakout Trend and Buying/Selling Proxy) are available for free on TradingView.

Opening (IRA): TLT September 19th 82 Short Put... for a .90 credit.

Comments: Adding to my position at strikes slightly better than what I currently have on ... .

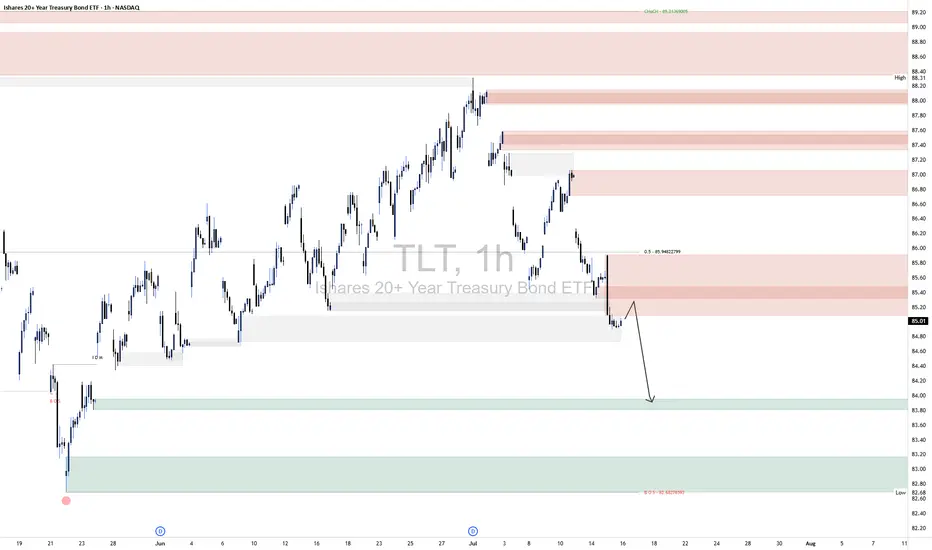

TLT ShortTLT 1H Technical Analysis

📈 Outlook:

The current setup suggests a bearish continuation scenario:

A corrective move toward the 85.20–85.60 supply.

Rejection from this area confirms continuation of the downtrend.

Target: 83.20–83.60, where resting liquidity and untested demand reside.

This sequence follows a classic liquidity sweep + supply mitigation + continuation pattern. Unless price breaks convincingly above 85.80, the bearish outlook remains intact.

🔼 Supply Zones (Bearish Liquidity Layers):

Primary Zone: 85.20–85.60

This is the most immediate area of interest, aligning closely with the 50% equilibrium level of the last bearish impulse (~85.84). Price is likely to reject from here as it also coincides with a previously unmitigated supply block and market inefficiency.

Stacked Supply Above: 86.40–88.00

Should price break the lower supply, these zones will come into play. However, the current structure suggests strong probability of rejection before reaching these levels.

🔽 Demand Zones (Target Areas):

First Demand: 83.20–83.60

This is your marked initial downside target. It represents the next logical draw on liquidity and aligns with prior accumulation and support structure. It’s likely to act as a temporary reaction zone or the next entry point for accumulation.

Deeper Demand Zone: 82.40–82.80

Marked by your secondary border, this range offers higher time-frame confluence and could act as the final sweep zone if the 83s fail to hold.

Opening (IRA): TLT Sept 19th 83 Short Put... for an .88 credit.

Comments: Camping out with a strike slightly below the 52-week low, where the options contract is paying a smidge more than 1% of the strike price in credit.

I don't really need more TLT, but wouldn't mind being assigned more at a lower price than the stock element of my covered calls.

How Will Uncle Sam Strike Back? – U.S. Treasuries on the Edge📉 How Will Uncle Sam Strike Back? – U.S. Treasuries on the Edge

After covering leveraged loans ( BKLN ), junk bonds ( HYG ), and investment-grade corporates ( LQD ), we now focus on the most important piece of the U.S. credit puzzle: Treasuries.

Specifically, the long end of the curve — tracked by TLT .

📊 What the Chart Shows

Left Panel (3D Chart)

• All-time highs in Feb 2020 at $179.80

• Long-term trendline going back to 2004

• Critical support was broken in 2022 — a structural breakdown

Right Panel (8H Chart)

• Clear descending channel since 2020

• Price has rejected from the channel top multiple times

• Recent bounces off the lower channel suggest a potential final flush

🧠 What Happened in 2022? (can't blame Trump for that...)

This wasn’t politics — it was policy.

• The Fed's fastest hiking cycle in decades

• Liquidity evaporated

• Long-duration bonds were abandoned

• The key trendline that had held for years was finally lost

That line — once support — is now resistance.

📐 My Technical Expectation

I expect one final slide before a reversal.

• Channel base sits at ~$76.32

• My projection targets $71.30 or even $68

• That would mark new all-time lows for TLT

🟡 After that? I expect a macro reversal , targeting:

• 🔼 $101 – mid-channel reversion

• 🔼 $112–115 – former support zone (2019–2022), now resistance

🔍 Macro Context

This chart isn’t just about price.

It reflects how markets are pricing confidence in U.S. debt .

And right now?

That confidence is shaky . With Trump turning 'orange' and taking it out against almost everyone else: China but also his allies(EU, Canada, Japan, etc )

🔄 Recap of the Series So Far:

• BKLN – record leveraged loan outflows

• HYG – junk bonds bounced at historical support

• LQD – investment grade bonds holding steady

• TLT – U.S. Treasuries under pressure, and possibly breaking down

📌 Next up?

🟧 CRYPTOCAP:BTC

Because when the world begins to question Treasuries , the search for alternative stores of value begins.

One Love,

The FXPROFESSOR 💙

ps. wait for the next posts...they might be epic!

TLT is currently in the Wyckoff accumulation phaseBased on the provided weekly and daily charts for the iShares 20+ Year Treasury Bond ETF (TLT), here is a Wyckoff analysis and a potential trading strategy using a diagonal option spread.

### **Wyckoff Analysis of TLT**

**Weekly Chart:**

The weekly chart for TLT appears to be in the early stages of a potential **accumulation phase**. Here's a breakdown of the key price action in the context of Wyckoff principles:

* **Selling Climax (SC):** The sharp sell-off culminating in the low around $83.30 can be interpreted as a Selling Climax. This is where the downward momentum peaks as panicked investors sell heavily.

* **Automatic Rally (AR):** Following the SC, the price bounced to form a high. This rally is largely technical in nature as short-covering and bargain hunting come into the market. This helps to define the upper boundary of a potential trading range.

* **Secondary Test (ST):** The subsequent decline from the AR to retest the area of the SC low is a Secondary Test. Ideally, this test occurs on lower volume than the SC, which would indicate diminishing selling pressure. From the chart, it appears there was a retest of the lows.

Currently, the price action on the weekly chart suggests that TLT is in **Phase B** of accumulation. This phase is characterized by the "building of a cause" where the "smart money" is accumulating positions. Price action in Phase B can be volatile as it moves between the support established by the SC and the resistance of the AR.

**Daily Chart:**

The daily chart provides a more granular view and supports the accumulation thesis from the weekly chart. The recent price action on the daily chart shows a series of higher highs and higher lows, which can be interpreted as a **Sign of Strength (SOS)** within the larger accumulation structure. This suggests that demand is starting to overcome supply.

### **Trading TLT with a Bullish Diagonal Call Spread**

Given the analysis that TLT is in a potential accumulation phase, a bullish long-term outlook is appropriate. A bullish diagonal call spread is a suitable strategy to capitalize on a potential gradual price increase while also benefiting from time decay.

This strategy is also known as a "Poor Man's Covered Call" and involves:

* **Buying a longer-dated, in-the-money (ITM) or at-the-money (ATM) call option.** This acts as a surrogate for owning the underlying ETF.

* **Selling a shorter-dated, out-of-the-money (OTM) call option.** The premium received from selling this call reduces the cost of the long call and generates income.

**How to structure the trade:**

1. **Long Call Selection:**

* **Expiration:** Choose a longer-dated expiration, for instance, 4-6 months out, to give the accumulation and subsequent markup phase time to develop.

* **Strike Price:** Select a strike price that is in-the-money or close to the current price of TLT (around $87.39). An ITM call will have a higher delta, meaning it will move more in line with the price of TLT.

2. **Short Call Selection:**

* **Expiration:** Select a shorter-dated expiration, typically 30-45 days out. This allows for more frequent income generation as you can "roll" the short call to the next month as it expires.

* **Strike Price:** Choose a strike price that is out-of-the-money. A good starting point would be a strike near a resistance level. Looking at the daily chart, a potential near-term resistance level might be around the $90-$92 area.

**Example Trade (Illustrative Purposes Only):**

* **Buy to open:** 1 TLT call option with an expiration 6 months from now and a strike price of $85.

* **Sell to open:** 1 TLT call option with an expiration in 30 days and a strike price of $90.

**Trade Management:**

* **If TLT rallies towards the short call strike ($90):** You can choose to close the entire spread for a profit or roll the short call up and out to a higher strike and a later expiration to continue collecting premium.

* **If TLT trades sideways:** The short call will lose value due to time decay (theta), and you can potentially buy it back for a lower price than you sold it for, or let it expire worthless. You can then sell another short call for the following month.

* **If TLT declines:** The value of your long call will decrease, but this will be partially offset by the premium received from the short call. The risk is limited to the initial net debit paid to establish the position.

> **Disclaimer:** This information is for educational purposes only and should not be considered financial advice. Options trading involves significant risk and is not suitable for all investors. It is crucial to conduct your own thorough research and consult with a qualified financial advisor before making any investment decisions.

TLT long into Sept. 26th?I had TLT on my calendar (from the very EXPERIMENTAL dowsing work that I do) for yesterday and today from readings I did on 5/22 & 5/18.

Being that it was looking like a swing low in this date window, I checked this morning, & from the very experimental work that I do, I get that it's heading to around $100. I had a prior post suggesting a larger bottom in place, and this appears to have been accurate.

The date for exit (VERY EXPERIMENTAL & for journaling purposes) I get is Sept. 26th.

*** NOTE ***

I post things here as a method of journaling ideas. If it aligns with YOUR OWN WORK, great. I'm pretty sure everyone has their good and bad streaks no matter what method they use.

So, I had a rough patch after finding out my incredibly special companion kitty was dying. Did I know att this would affect my work? No! I tried to stay "normal" ( for me ;) ). Did I learn something? Of course, & in the future I will allow myself more downtime to come back to balance.

No one really knows what's going on in my life, but I guess this work is probably more subject than other methods to emotional or energetic disruptions. I always clear my energy, but in certain circumstances it may be better to just chill. I'm learning as I go. If you have any advice on making this work better, please lmk.

$TLT Rising Channel or Bear Flag?Is it time to invest in NASDAQ:TLT ? It looks positive to me. With inflation cooling down it looks like bond prices could increase, which means rates are lower. We do have a Fed Meeting coming up so there could be more volatility depending on the “Feds” messaging.

I am taking this long today with a ½ size position. I will place my stop just “below” yesterdays low of $85.46. I am going long because I see a series of higher lows and higher highs. And I have a well-defined risk level of about 1% to know if I am wrong.

If you like this idea, please make it your own. Make sure you follow your trading plan.

Trade Long on TLT: Opportunities Amid Weakness in Treasuries

Targets:

- T1 = $86.50

- T2 = $88.00

Stop Levels:

- S1 = $84.00

- S2 = $83.00

**Wisdom of Professional Traders:**

This analysis synthesizes insights from thousands of professional traders and market experts, leveraging collective intelligence to identify high-probability trade setups. The wisdom of crowds principle suggests that aggregated market perspectives from experienced professionals often outperform individual forecasts, reducing cognitive biases and highlighting consensus opportunities in TLT.

**Key Insights:**

TLT, which represents long-term U.S. Treasury bonds, is currently trading at discounted levels following recent declines. This weakness stems from macroeconomic concerns and tightening monetary policies. Traders are paying close attention to the Federal Reserve's stance on interest rates, as hawkish behavior continues to suppress bond prices. However, current oversold conditions paired with strong technical levels around $85.00 suggest a potential reversal. A move higher could be catalyzed by dovish signals from policymakers or slowing inflation data, which may ease investor fears about prolonged rate hikes.

Treasuries often act as safe havens during volatile market conditions, and seasoned investors see value in entering positions during times of weakness. Traders should also monitor global economic indicators, as international risk events could fuel additional demand for long-term U.S. bonds.

**Recent Performance:**

Over the past week, TLT has experienced bearish pressure, losing nearly $1.50 in value. The asset's decline mirrors broader fixed-income struggles, with junk bonds (JNK) showing parallel weakness. However, late-stage declines and deceleration in momentum suggest stabilization might soon occur. TLT has maintained its position near the critical $85.00 support zone, hinting at limited further downside, especially as bond yields stabilize.

**Expert Analysis:**

Technical analysts highlight that TLT's Relative Strength Index (RSI) is approaching oversold territory, reinforcing the likelihood of bullish momentum. Historical price action indicates that dips below $85.00 historically see swift recoveries, driven by renewed buying interest from institutional players. Additionally, macroeconomists suggest that reduced bond issuance paired with moderating inflation could support TLT prices in the medium term.

The current price range provides a favorable risk-to-reward ratio for those with an intermediate to long-term outlook. Tactical entries at these levels could yield gains if market dynamics shift in favor of easing rate pressures or economic uncertainties drive bond demand.

**News Impact:**

Recent news highlights sustained investor caution as markets digest hawkish rhetoric from the Federal Reserve and await key economic data such as CPI and employment figures. While TLT remains under pressure from elevated bond yields, geopolitical tensions and emerging-market volatility could bolster demand for U.S. Treasury bonds as a safe-haven play. Events such as unexpectedly weak inflation data or dovish commentary from policymakers could further aid TLT's recovery.

**Trading Recommendation:**

Based on the analysis, TLT presents a favorable long opportunity for traders looking to capitalize on oversold conditions and technical support around $85.00. The proposed targets of $86.50 and $88.00 provide attainable high-probability price points, while stop-loss levels at $84.00 and $83.00 ensure minimal risk exposure. Monitoring macroeconomic indicators and policy announcements will be crucial in confirming the bullish outlook. Entering long positions at current levels provides a compelling risk-to-reward setup, aligning with professional trader consensus.

TLT: Possible bottom very soonHello,

Fed waiting to reduce rates and when they actually do it will impact TLT and may mark the bottom for TLT.

Looking at this fractal, it is following this pattern near perfectly, which indicates the bottom very soon.

Happy trading NASDAQ:TLT

$TLT breaking down? $80 target?TLT looks to be breaking down out of a bear flag.

We've already had multiple touches of the lower trend line and now it looks like price has broken through.

I think the most likely target is $79-80, but I've included multiple supports just incase we see a larger move than I'm expecting.

I'm looking to buy those levels should they hit as I think we'll see a longer term bullish move afterwards.

TLT is going on a TILT to the UPSIDEPerfect storm brewing. Everyone thinks TLT going down more. Rates should come down and send this flying to the upside. Chart arc has a double touchpoint on the long term and medium term. Its a FIESTA!

No refinance for u! $TLTContinuation of bearish behavior means you stuck with your 6-7% mortgage rate for awhile. But don't be sad maybe that will be considered a good rate in the future. TLT still looking or support check back around $77 to see what happens next!

Bond Market Crisis - Opportunity?Pay close attention to the bond market, particular to the 20 Year Treasury yield which is creeping back up. This is really bad news for the markets, yields could spike higher which could send the market tumbling. This cascade effect could provide an optimal entry into TLT - which is an inverse play on interest rates.

There is currently no reason for the Fed reserve to reduce interest rates. Inflation is creeping back up and the cost implications of tariffs are yet to truly felt in the inflation readings. Meanwhile, the US has lost its perfect credit rating and the debt burden continues to grow. The Fed will not reduce rates if inflation shows no sign of abating. Note that in the UK inflation is back up and I expect this to also be the case in the US.

My plan is to watch this play out and look for opportunity in TLT. I don’t want to get caught up bag holding stocks if there is a major bond crisis. As far as the chart is concerned, I expect a double bottom pattern and bullish confirmation with a break of the neckline.

None of this is financial advice, do what’s best for you.

TLT Is Yelling at UsYou typically see a migration to TLT when people are looking for a safe haven from troubled markets

I posted about TLT previously and thought we were about to see a rush to the trade because of potential market weakness

Well as we know this Bull market continued to show legs and subsequently TLT has been grounded on the launching pad

The market is yet again showing classic signs of topping

Are we saying that the market is about to crash? NO..not yet

What we are saying is that liquidity is leaving the equities markets in droves and TLT will most likely be a place where that liquidity finds a home

So pay close attention to TLT over the next 6 months because its going to tell you everything you need to know about this bull market

TLT Long Here or CloseI expect TLT to rally this summer since rate cuts are more likely then not

TP1 91

TP2 96

Equities VS Bonds, why the current divergence?Introduction: should we finally go back to buying bonds? While the equity market has rebounded vertically since mid-April and the start of a period of trade diplomacy between the USA and its main trading partners, bond prices have remained at a low level.

Although both realized and implied volatility have fallen sharply in recent weeks (see our bearish analysis of the VIX at the end of April), how can we explain such a divergence between the recovery in US stock prices and a bond price still at the bottom?

For bonds, is this an opportunity to position at an attractive price?

1) First of all, take a look at the two charts below, which show the underlying trend and the recent trend of the S&P 500 (for the equities market) and the 20-year US interest rate contract (to represent the bond market)

Chart showing weekly Japanese candlesticks on the S&P 500 future contract

Graph showing monthly Japanese candlesticks on the US 20-year bond contract

2) The reasons for the outperformance of equities versus bonds are numerous and fundamental

The underperformance of bonds versus equities is based on a combination of fundamental factors:

- Firstly, corporate profit forecasts remain optimistic for the next 12 months, creating a favorable arbitrage for the equity market (see our previous analysis of the S&P 500 index).

- The Federal Reserve's (FED) intransigence in the face of the risk of a rebound in inflation against the backdrop of the trade war. The market does not expect a resumption of the US federal funds rate cut before the monetary policy decision on Wednesday September 17. The inverted correlation between interest rates and bond prices is therefore a factor putting pressure on prices.

- Beyond monetary policy, the United States' fiscal trajectory is also a topic of debate. The Republican bill to massively lower taxes could further deepen the federal deficit and add to an already colossal public debt, keeping long-term interest rates high. All the more so since, according to the Peterson Foundation, nearly $9.3 trillion in debt will mature over the next 12 months, adding to the estimated $2 trillion in deficit financing needs.

- The new all-time high in global liquidity is creating a favorable arbitrage for risky assets in the stock market, due to the positive long-term correlation between the S&P 500 index and global liquidity

3) Even so, current bond prices are in a technical zone of long-term interest, and forward-looking fundamentals could allow bonds to rebound in the coming months

The latest macroeconomic indicators confirm a loss of momentum in the US economy. In April, producer prices suffered their sharpest contraction in five years, suggesting that companies are absorbing some of the higher costs associated with trade tensions. At the same time, retail sales stalled, as consumers cut back on purchases in the face of persistent inflation on imported goods. If confirmed, these signs of a slowdown could lead to a “flight to quality” phenomenon, i.e. arbitrage in favor of the bond market over the coming months.

The chart below is a reminder that the US bond market is currently at a major technical support level.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

TLT Longdemand Zone, confirmed once, not fresh

Long entry 85.3

no Stop ,

Target 94, 101

Risk management is much more important than a good entry point.

I am not a PRO trader.

In my trading plan, the Max Risk of each short term trade should be less than 1% of an account.