VXX - 1hrI am currently long vol, but only expecting a bounce into wave (iv) price targets. I'll be looking for another short set-up at that time. Closing above 22.39, and especially 23.21 would be a warning to anyone long 'sp500 imo. MACD did not make a new low during red wave (iii); instead MACD has positive divergence with a higher low whereas price has a series of lower lows. This condition could suggest the corrective interpretation of the decline (alt A) which projects into 25 -26 region (alt B). It'll likely be an indirect route with whipshaw. Trading 4th waves is difficult - as is trading corrective a-b-c moves. Preserve capital with stops, protect gains. Exiting with profit on a 3-wave move in vol land has no shame imo.

ATMP trade ideas

VXX - 30minSorry, that was meant to be a "LONG" vol position...not SHORT.

Constructive development this morning for those long volatility. I'm anticipating a series of corrective moves into the wave (iv) target region as shown. Remember, placement of the labels is not meant to indicate a prediction on exact timing. These are price regions...

Fib extensions and positive divergences on MACD helped identify the potential here. Use stops, preserve capital and protect gains, depending on your timeframe...

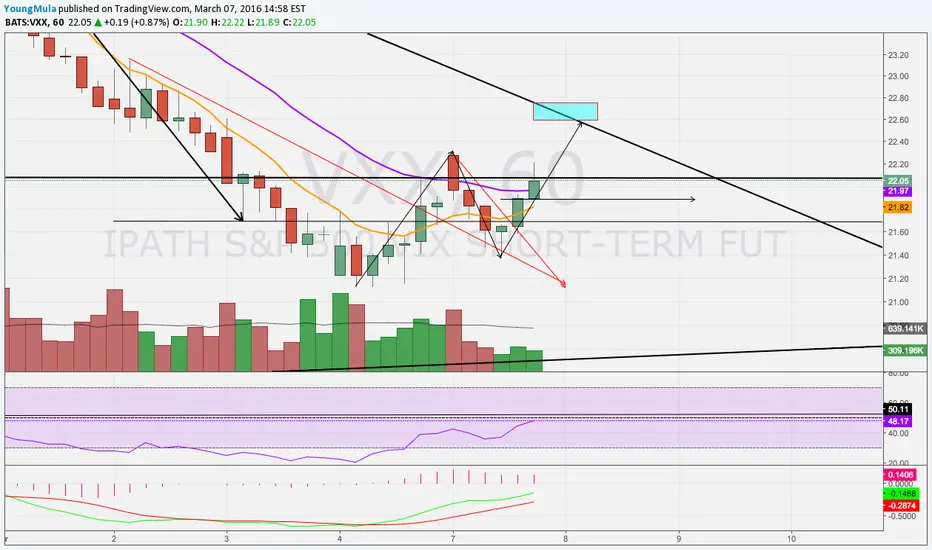

VXX - 30minVXX has turned up from indicated support, but has a lot to prove before higher targets are probable. See earlier 15min idea linked below.

Also note positive divergence on Stoch RSI and MACD.

VXX - 15 minNote resistance for wave (iv) and alternate B. I wouldn't hold out for B unless the 'sp500 starts breaking down through support, too.

VXX - 1hrHere's the other side of the volatility trade. Lesson, don't hold long vol in the face of a 3rd wave down...

I'm expecting a bounce between here and 18.20/.13 region back to 21.39 - 22.39 in wave (iv). Then continued decline to 14 region. Wouldn't be surprised by decay lower than 12.

ROLLING VXX MAY 20TH 21 SHORT CALL TO MAY 20TH 20 SHORT CALLRolled my VXX May 20th 21 short call down to the 20 short (same expiry) for an additional .27 ($27 credit).

This is part of my VXX synthetic/poor man's covered call ... .

Completes bearish Bat patternVXX with completion of bearish Bat pattern.

27-28 is a daily resistance zone. A close below 28 can expedite the reversal in VXX

Pattern completion - 29

Look at where VIX is... First pattern triggered the $SPY's rally to 195$ (see linked idea)

Now we have a second pattern to follow - Pay attention to VIX

Follow me on TradingView

Visit my blog - goo.gl

Subscribe to the newsletters - goo.gl

TRADE IDEA: VXX SYNTHETIC/POOR MAN'S COVERED CALLSynthetic covered calls using options are a good way to utilize capital efficiently as compared to buying the underlying outright and initiating, for example, a covered call. Were you to buy 100 shares of VXX at $14, it would cost $1400, with the current value of the short call reducing that cost basis by about $160, so it would cost around $1240 to put on, as compared to the $585 or so per contract to initiate this position. Moreover, you'd naturally have to wait until VXX struck $14 to get in at $14/share, so a synthetic gives you the added advantage of your being able to kind of "pick your price" and/or cost basis for the underlying, even though it's just a "synthetic" price.

Here, the September 16th 14 long call stands in for the stock (since it's mostly made up of intrinsic value), against which I sell calls to reduce my cost basis in the long option over time, the goal being to take off the entire setup in profit when the total credits collected for the short call (and any rolls) + the current price of the long option exceeds what I paid for the original setup.

Here are the metrics:

Sep 16th Long Call/April 15th 21 Short Call

Probability of Profit: Unknown

Max Profit: Unknown

Buying Power Effect: $585/contract (debit)

Unfortunately, the probability of profit and the max profit are unknown for this setup from the get go, since exactly how much credit you can collect for the rolling of the 21 short call in the months after setup is unknown and will vary over time. It is also possible that, depending on the price movement in the underlying.

I would also note that VXX, by nature, generally suffers from contango, so its price will naturally decline over time in the absence of backwardation. Consequently, it's entirely possible that price could break 14 at some point going forward. Naturally, that's okay as long as the amount of credit you receive for the rolls of the short call exceeds what you paid for the long call (currently, $745) and, of course, I'm assuming that price in VXX will be somewhat above 14 for the duration of the trade.

VXX daily - bearish - 2/19/2016Breakout failed. Now lost 3 supports (red lines, 10 day MA). RSI broke too and below 50.

VXX daily - looks like a cup handle - 2/6/2016I will be a buyer if it closes above the red. I will short it if blue support broke.