Threat or Catalyst? Impact of MasOrange IPO on TelefonicaThreat or Catalyst? Impact of the Upcoming MasOrange IPO on Telefónica

By Ion Jauregui – Analyst at ActivTrades

The potential IPO of MasOrange, valued between €5.37 and €9.44 billion based on applied EV/EBITDA multiples (ranging from 7x to 8.4x), could significantly reshape the competitive landscape of Spain’s telecommunications sector. The new entity, formed by the merger of MásMóvil and Orange Spain, aims to capitalize on a market that is once again showing appetite for new public listings. But what impact could this operation have on Telefónica?

The Return of a Real Threat in the Domestic Market

MasOrange is not just another telecom operator. With a leading customer share in Spain, an already deployed fiber optic network, and EBITDA margins above the industry average (37.9%), it is emerging as a highly efficient competitor. Although it carries a high net debt (€14.11 billion), it benefits from projected synergies of €500 million by 2027, which could justify a premium valuation versus other operators. Furthermore, the potential entry of a new partner into its shared fiber subsidiary with Vodafone—valued at up to €10 billion—could unlock capital, reduce leverage, and increase the appeal of its upcoming IPO.

For Telefónica, this represents added pressure in its most strategic market: Spain. While the company diversifies across Latin America, Germany, and the UK, its domestic market remains key for cash flow generation. A well-capitalized, listed MasOrange could intensify price competition, compress margins, and pressure Telefónica's local profitability.

Fundamental Analysis of Telefónica: Financial Stabilization Amid Structural Challenges

Telefónica has achieved progressive financial stabilization in recent years after a period marked by high debt and structural revenue pressure in mature markets. As of Q1 2025, the company reported the following key figures:

Revenue: €10.15 billion (+1.1% YoY), driven by growth in Germany and Brazil.

OIBDA: €3.20 billion, with a margin of 31.5%.

Net financial debt: €26.3 billion, improved from €27.48 billion at year-end 2023.

Net profit: €509 million (+9.6% YoY).

Telefónica has strengthened its financial profile through the sale of non-core assets and the rotation of infrastructure, such as towers and data centers. This has helped reduce debt and improve ROCE. It has also maintained an attractive dividend policy, with a €0.30 cash dividend per share for 2025, offering a yield close to 6.5% at current prices.

By region, Brazil and Germany continue to perform well, while Spain remains a mature, low-growth market characterized by high competition and regulatory pressure. In this context, the entry of a more efficient, fiber-leveraged MasOrange could negatively impact margins and market share in Spain.

Telefónica is investing in digital transformation, artificial intelligence, and 5G network deployment, although these efforts have yet to translate into double-digit revenue growth. The company also maintains a strategic alliance with the Spanish government (SEPI), which now holds over 10% of its capital—a potential source of stability amid possible corporate moves in the sector.

Technical Analysis: Bearish Pressure

Telefónica shares are currently trading at €4.56 as of Monday’s open, down -0.13% from Friday’s session. The stock appears to have lost momentum from the recent quarterly earnings release and has entered a sideways phase. Nevertheless, its long-term uptrend remains intact. Since the golden cross on April 14, the 50-day moving average continues to expand above the 100- and 200-day averages. The price is currently supported by the 50-day moving average.

The RSI shows slight overbought conditions at 56.32%, while the MACD suggests a weakening trend accompanied by a bell curve pointing to a control level around €4.08. As long as the current support at €4.43 holds, we may see a push to test the recent high of €4.628. However, if this momentum lacks strength, the price could retest the support zone, and a break below it could lead to a pullback with €4.43 as the first potential stopping point.

Conclusion

MasOrange's return to the stock market reshapes the playing field. For Telefónica, the risk lies not so much in the newcomer’s valuation, but in its operational efficiency, fiber advantage, and renewed investment capacity. While Telefónica remains a global reference in telecom, this move could force the company to accelerate its transformation and defend its share in its most mature and competitive market.

*******************************************************************************************

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and such should be considered a marketing communication.

All information has been prepared by ActivTrades ("AT"). The information does not contain a record of AT's prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.

TNE5 trade ideas

Telefónica: Consolidation or the Start of a New Bullish Phase?Ion Jauregui –ActivTrades Analyst

Telefónica is experiencing one of its strongest market moments in recent years, with a nearly 20% appreciation so far in 2025 and a share price that has reached €4.73. These are levels not seen since July 2022, sparking renewed investor interest, although questions remain regarding its ability to sustain this momentum.

Fundamental Analysis

The company is undergoing a structural transformation aimed at improving profitability and reducing operational risk. In this regard, it has accelerated the divestment of assets in less strategic Latin American markets such as Ecuador, Peru, Argentina, Uruguay, and Colombia, focusing instead on its core operations in Europe and Brazil. This strategy has allowed Telefónica to reduce its exposure to currency volatility and improve capital allocation efficiency.

Despite reporting a net loss of €1.304 billion for the fiscal year, this figure is primarily attributable to accounting write-downs related to asset disposals and does not undermine its cash flow generation capacity or its commitment to maintain the annual dividend of €0.30. With a customer base exceeding 390 million and a solid infrastructure network, the operator remains a key player in the markets where it operates. Its current focus on financial discipline and risk profile improvement aligns with an environment in which operational stability and efficiency outweigh aggressive growth strategies.

Technical Analysis

From a technical perspective, Telefónica broke through a significant resistance level at €4.430 at the end of May — a ceiling in place since its sharp price drop in 2020. This breakout was accompanied by a notable increase in volume, adding validity to the move.

The current price of €4.610 aligns with a medium-term high. If the stock manages to consolidate above the €4.628 high in the coming weeks, it could pave the way toward €5.00, where the next relevant resistance level lies, coinciding with the current point of control at €5.064. Conversely, a failure to hold above current levels could lead to a retracement toward the current moving average around €3.930 or slightly above, where previous highs now act as support. The RSI currently stands in overbought territory at 64.67%, suggesting there may still be room for an upward move toward the €5.00 point of control zone if bullish momentum persists.

Conclusion

Telefónica is at a pivotal stage in its strategic redefinition, a process that has begun to reflect positively in its share price. This shift is driven by a more rational approach to risk management, a clear focus on priority markets, and a sustained commitment to financial discipline. The technical breakout from historic resistance levels strengthens the case for a continued bullish trend, although caution remains warranted: further upside will depend on sustained consolidation above current levels and the emergence of solid catalysts to support the company’s narrative. After years of sideways movement, the stock has finally broken out — now comes the true test: turning this rally into a lasting trend.

*******************************************************************************************

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and such should be considered a marketing communication.

All information has been prepared by ActivTrades ("AT"). The information does not contain a record of AT's prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.

Telefónica: Dividend load shedding in HispamBy Ion Jauregui - ActivTrades Analyst

The “strategic review” announced by CEO Marc Murtra focuses on the Hispanic American market, a sector that has shown negative results for years. In 2024, business in countries such as Argentina, Colombia, Chile, Peru and Mexico generated 'red numbers' that reached 2,432 million euros, as gains in Ecuador, Venezuela and Uruguay did not offset the falls in the other markets.

To reverse this situation, Telefónica has accelerated the divestment process in Latin America. In just twenty days, the sale of the Argentine subsidiary brought in extraordinary proceeds of 1,190 million euros. This transaction was closed with no risk of reversal, as the amount was already in the company's cash, and there is no possibility that the Argentinean government, headed by Javier Milei, will modify the transaction. Likewise, last Thursday the agreement for the sale of the Colombian subsidiary was announced. Millicom committed to acquire 67.5% of Coltel (Colombia Telecomunicaciones) for 368 million euros, a transaction pending regulatory permits in that country. 1,558 million, funds that Telefónica plans to allocate to two crucial objectives: debt reduction and consolidation of dividend payments.

If these proceeds are applied in full to the repayment of liabilities, the group's debt could fall by 5.7%, from 27,161 million euros to 25,603 million euros in mid-March. According to several analysts, these divestments will not only avoid future burdens, but will also generate resources for reinvestment in more prosperous markets or sectors. This strategy is in line with the so-called “dead horse theory”, which recommends divesting assets that no longer add value. It is worth noting that Latin America represents 27% of Telefónica's workforce, with 27,570 employees, which means that the exit from this region would imply a significant structural reduction in the organization.

Finally, Murtra stressed at the Mobile World Congress the need for large European telecommunications companies to consolidate and grow in order to strengthen their technological capacity. With this series of operations, Telefónica is not only preparing to improve its financial situation, but is also laying the foundations for a more competitive and efficient future.

If we analyze all this in perspective, it only remains to see that Murtra is seeking to recover the share price value that it has been losing since 2020 when it was trading at 7.592 euros/share. In mid-2022 its highs were at €5.064 and consequently it then fell in price to its lows of €3.237. The range that the company has developed has fluctuated from May 2020 to the present between 4.430 and 3.535 euros/share. 3.923 in the middle zone all this time. The current price after such a disentailment in Spanish America has resulted in a price recovery to 4.347 euros, a value in the upper part of this range. The last few sessions the price has climbed from the middle of the checkpoint after bouncing off the 3.764 level on January 24. This is just a symptom that the strategy of getting rid of the burden since the beginning of the year is only looking for “red numbers” to turn green to ensure this dividend in a very controversial quarterly closing for the Spanish company.

It remains to monitor the evolution of the company's investment strategy for the long term this year, to see if the company regains the path of upward recovery.

*******************************************************************************************

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and such should be considered a marketing communication.

All information has been prepared by ActivTrades ("AT"). The information does not contain a record of AT's prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acing on the information provided does so at their own risk.

TELEFONICATELEFONICA is presenting a humungus 20 year large harmonic structure and is locally confirming levels as support.

Easy to manage risk here, will hit TPs when you are 90 years old.

Enjoy : )

Telefónica restructures its strategic plan towards BrazilBy Ion Jauregui - ActivTrades Analyst

Latin America divestment plan

Telefónica has put its subsidiary in Uruguay, valued at up to $400 million, up for sale. This move is in line with its divestment strategy in Latin America, where it also plans to sell assets in Argentina and Mexico. The Uruguayan subsidiary, based in Montevideo, is facing a loss of customers due to competition from Claro and state-owned Antel. The company hopes to attract bids for a small market with declining revenues but high investment demands.

Key assets and business value

Telefónica Uruguay's most valuable assets are its mobile frequency licenses, which cover the 850 MHz, 700 MHz and 1,900 MHz bands, essential for 2G, 3G, 4G and 5G services. Movistar Uruguay stands out as the largest private operator in the country, with 1.4 million customers and 97% coverage of the territory. Estimates suggest that the sale value would range between US$350 million and US$400 million, a figure similar to the offer it received three years ago from Supercanal-Arlink (now Super), although unsuccessful at the time.

Fierce competition and loss of customers.

Movistar Uruguay faces strong competition. In recent months, it has lost 32,750 net lines, while Claro has gained 38,000 lines and Antel, although with a slight negative balance, maintains its market leadership. According to URSEC data, Movistar ranks second in the Uruguayan mobile market with a 29% share, compared to 49% for Antel and 22% for Claro.

Declining revenues and market challenges

The Uruguayan mobile market is experiencing a slowdown, with subscriptions stagnating since the end of 2023. Movistar Uruguay also offers business services, backed by more than 70 stores, 1,300 employees and more than 5,000 suppliers and partners. However, competitive pressures and high investment costs limit growth.

Regional outlook and next steps

Beyond Uruguay, Telefónica faces similar challenges in other Latin American markets. In Mexico, the company is looking for a buyer for a business that generates 960 million euros, but with low profit margins due to the high proportion of prepaid customers. In Colombia, the sale process is in its final phase, with Millicom as the main interested party. In addition, the situation in Peru is critical after Movistar Peru filed for insolvency proceedings, forcing Telefónica to guarantee services for 13 million customers.

Telefónica continues to consolidate its position in key markets such as Brazil, while redefining its strategy in other Latin American territories to optimize its profitability and business focus.

Telefónica Analysis

Since the end of 2022 the company has been looking to recover its share price by having an upward cycle. June and October 2024 were two occasions where it sought to pierce the 4.6 euros without success. This data with the RSI currently at 60.87% overbought indicates that the price could bounce towards the current control point (POC) at 3.960 euros. If the company continues to recover positions we could see another new attempt to reach 4.6 in this quarter's income statement.

*******************************************************************************************

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and such should be considered a marketing communication.

All information has been prepared by ActivTrades ("AT"). The information does not contain a record of AT's prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acing on the information provided does so at their own risk.

TEF - 1 year RECTANGLE══════════════════════════════

Since 2014, my markets approach is to spot

trading opportunities based solely on the

development of

CLASSICAL CHART PATTERNS

🤝Let’s learn and grow together 🤝

══════════════════════════════

Hello Traders ✌

After a careful consideration I came to the conclusion that:

- it is crucial to be quick in alerting you with all the opportunities I spot and often I don't post a good pattern because I don't have the opportunity to write down a proper didactical comment;

- since my parameters to identify a Classical Pattern and its scenario are very well defined, many of my comments were and would be redundant;

- the information that I think is important is very simple and can easily be understood just by looking at charts;

For these reasons and hoping to give you a better help, I decided to write comments only when something very specific or interesting shows up, otherwise all the information is shown on the chart.

Thank you all for your support

🔎🔎🔎 ALWAYS REMEMBER

"A pattern IS NOT a Pattern until the breakout is completed. Before that moment it is just a bunch of colorful candlesticks on a chart of your watchlist"

═════════════════════════════

⚠ DISCLAIMER ⚠

The content is The Art Of Charting's personal opinion and it is posted purely for educational purpose and therefore it must not be taken as a direct or indirect investing recommendations or advices. Any action taken upon these information is at your own risk.

Telefonica Partners Chainlink For Security Against SIM Swap ScamTelefónica ( BME:TEF ), a global telecommunications company, has partnered with Chainlink Labs, a prominent player in the blockchain space. This partnership aims to leverage Chainlink Functions, recognized as a top-tier Web3 connectivity solution. By integrating Telco capabilities into the blockchain industry, Telefónica ( BME:TEF ) and Chainlink are addressing the growing need for secure and reliable data transmission within decentralized networks. Chainlink Functions serve as a critical element in this collaboration, facilitating the seamless connection between blockchain-based smart contracts and real-world data sources.

These oracles play a pivotal role in ensuring the accuracy and integrity of data used in automated decision-making processes within the Web3 space. In essence, Telefónica’s ( BME:TEF ) partnership with Chainlink signifies a significant advancement in the integration of telecommunications infrastructure with blockchain technology. This integration not only enhances the functionality of decentralized applications but also reinforces the security measures essential for the widespread adoption of Web3 solutions.

GSMA Open Gateway Initiative and Recent Security Breach

The GSMA Open Gateway initiative introduces standardized Telco APIs aimed at bridging the gap between telecommunications and the Web3 ecosystem. These APIs, developed under the guidance of the GSMA, provide a platform for integrating pioneering Telco capabilities into decentralized networks. One of the primary objectives of the initiative is to address various challenges within the Web3 space, such as fraud prevention and secure account creation, by leveraging the robust infrastructure of telecommunications networks.

Recently, the U.S. Securities and Exchange Commission (SEC) fell victim to a security breach attributed to a SIM swap attack. This breach occurred when unauthorized entities gained control of the SEC’s official account on a social media handle, leading to the dissemination of false information regarding the approval of bitcoin exchange-traded funds. This incident underscores the pressing need for heightened security measures within the Web3 ecosystem to mitigate the risks posed by such attacks.

Enhancing Security with GSMA Open Gateway SIM SWAP API & Chainlink

The integration between the GSMA Open Gateway SIM SWAP API and Chainlink Functions marks a Pivotal milestone in bolstering security measures within the Web3 ecosystem. This collaboration allows for the seamless connection between telecommunications infrastructure and blockchain technology, enhancing the overall security and reliability of decentralized networks.

Beyond transaction security, this integration offers broader security benefits for Web3 applications and decentralized finance (DeFi) services. By leveraging the GSMA Open Gateway API via Chainlink, developers can enhance two-factor authentication (2FA) mechanisms and implement more robust fraud detection protocols. This comprehensive approach to security not only safeguards against SIM swap attacks but also strengthens overall security measures within the Web3 ecosystem, promoting trust and reliability among users and stakeholders alike.

TEF | High Volume Telecom | OversoldTelefonica, S.A., together with its subsidiaries, provides telecommunications services in Europe and Latin America. The company's mobile and related services and products comprise mobile voice, value added, mobile data and Internet, wholesale, corporate, roaming, fixed wireless, and trunking and paging services. Its fixed telecommunication services include PSTN lines; ISDN accesses; public telephone services; local, domestic, and international long-distance and fixed-to-mobile communications; corporate communications; supplementary value-added services; video telephony; intelligent network; and telephony information services, as well as leases and sells handset equipment. The company also provides Internet and broadband multimedia services comprising Internet service provider, portal and network, retail and wholesale broadband access, narrowband switched access, high-speed Internet through fibre to the home, and voice over Internet protocol services. In addition, it offers leased line, virtual private network, fibre optics, web hosting and application, outsourcing and consultancy, desktop, and system integration and professional services. Further, the company offers wholesale services for telecommunication operators, including domestic interconnection and international wholesale services; leased lines for other operators; and local loop leasing services, as well as bit stream services, wholesale line rental accesses, and leased ducts for other operators' fiber deployment. Additionally, it provides video/TV services; smart connectivity and services, and consumer IoT products; financial and other payment, security, cloud computing, advertising, big data, and digital telco experience services; virtual assistants; digital home platforms; and Movistar Home devices. It also offers online telemedicine, home insurance, music streaming, and consumer loan services. The company was incorporated in 1924 and is headquartered in Madrid, Spain.

$TEF with a Bearish outlook following its earnings #Stocks The PEAD projected a Bearish outlook for $TEF after a Negative over reaction following its earnings release placing the stock in drift C with an expected accuracy of 60%.

Buy $TEF - NRPicks 08 JulTelefónica, S.A., provides telecommunications services in Europe and Latin America. The company's mobile-related services and products comprise mobile voice, mobile data and Internet, wholesale, corporate, roaming, fixed wireless, and trunking and paging services.

'Calling' on bids!I definitely like how the bulls defended that 4.72-78 zone for the past 2 weeks. It tells me they are preparing to take this stock up. The favourable earnings results could be the catalyst. I will get in at the break of 5 and target 6 with sl at 4.55 for a 1:2.2 risk to reward ratio. Caution should be taken at the 5.5 zone where the trade could end prematurely, so at that zone any sign of retardation I will exit.

Risk management crucial!

Buy $TEF - NRPicks 10 DecTelefónica, S.A., provides telecommunications services in Europe and Latin America. The company's mobile-related services and products comprise mobile voice, value-added, mobile data, Internet, roaming, fixed wireless and paging services.

Revenue TTM 46.7B

Net Income TTM 11.8B

Net Margin TTM 25.4%

Debt/EBITDA TTM 4.55x

P/S 0.53

P/B 0.89

P/E 2.07

Telefonica: The perfect choice for a DIVIDEND strategyHere at Human Traders, we've been following Telefonica closely. Its fundamentals look better than ever. They reduced its debt from €56Bn in 2011 to €25bn in 2021. Alvaro Pallete, CEO of Telefonica has done an incredible job in term of debt reduction and company management. The dividend is also very interesting. We bought Telefonica when the dividend yield was more than 12%. Still the dividend yield now is more than 6%, one of the bests in Spain, a country where almost every company offers attractive dividend yields. In terms of competition, the telecommunication sector has always been fierce, but Telefonica remains as the main company in the sector in Spain and strong presence in LATAM. With Movistar+, they follow the same strategy plan as AT&T with streaming services.

Regarding technical analysis, you can clearly see the downtrend of the last 15 years has been really strong, but we believe this time there could be a breakout of the main resistance level. It will take some time, but with this high-dividend yield, we can wait as long as we need. If you follow a dividend strategy, we recommend to have this one in your portfolio. For those who follow performance only, wait for the breakout of the resistance level to enter, o enter on the bottom area of the last channel. As you can see there was an important bullish divergence last year, and we don't expect the stock price to fall below that area, unless there is another market crisis like the one we saw back in March 2020. There is also the possibility of a rally in the telecommunication sector, one the most smashed sectors in the last 15 years, but interestingly, it's one of the most important ones in society.

Telefonica 2023 ForecastPrice action is consistently maintaining the strong trendline seen in previous years.

Plenty of upside which should be achieved with relative ease.

Happy trading.

Buy $TEF - NRPicks 16 AbrTelefónica, S.A., together with its subsidiaries, provides telecommunications services in Europe and Latin America. The company's mobile and related services and products include mobile voice, value-added, mobile data, Internet, wholesalers, corporate, roaming, fixed wireless, trunking and paging services.

$TEF is a solid and very profitable company, closed in 2020 with:

- Revenue $53B

- EBITDA $13.5B

- $9B CASH

- LT DEBT$51.6B

- P/S 0.48

- P/B of 1.82

- dividend yield 10.29%.

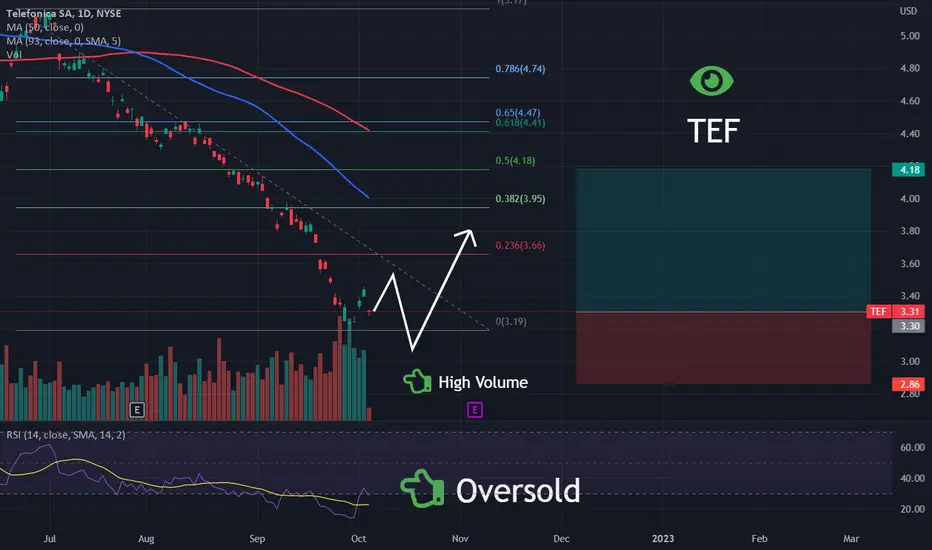

TELEFÓNICA: Bullish bat patternO2-Virgin operation in May. Before mid March, important date when competitors will provide information.

Technical analysis shows a bullish bat pattern and its prophecy being accomplished today. Fibonacci retracement level 0.236 has been reached and tomorrow TEF may try to conquer 3.80 once again if profit taking doesn't make the stock flat all over the session. Long term perspective clearly bullish if UK regulator issues positive news.

Telefonica Chart AnalysisShort Term: short till 23 May 2021

Support (TP for short) : 2,70

Long Term: Entry between 2,70 and 3,5 Long