STOXX50 trade ideas

EURO STOXX (wait for buying opportunity)EURO STOXX: we waiting for a downward move, causing havoc (year: 2020 - 2022) before buying, in anticipation of a multi decade bull market.

Some Insights with regard to STOXX50 20 Years Long insights. All labeled. I always believe this should be an ABC wave correction but the United States market is going delusion that makes me doubt myself. However, the EU market seems to represent a possible ABC correction, with C point being a truncation. I am waiting to see if 2986 could be a potential support zone. Because if this level doesn't hold, the overall positive trend zone of Stoxx 50 will be broken. Another possible support level is 2706. I currently have no position. But if those levels don't defend, I would consider opening more shorts. TP 2300 at least.

Two set play ideas for shortsBased on two recent resistance areas.

Large risk to reward ratio if we fall as far back as major support and still good even if we reach minor support (target).

ANALISIS DE LA COYUNTURA DE WALL STREETEl mercado desde el punto de vista de elliott, están claras las opciones conviven, opciones alcistas y bajistas, nosotros hemos operado la bajista, pero sabemos que la alcista es posible y el mercado nos dirá si estamos equivocados o acertados, esta es una de las veces que el análisis está mucho más claro que la operatoria.

You know when it is so bullish 1% down feels we are upEurostoxx 50 futs reversing right on the 200 day average. To buy the dip or not to buy it here?

Euro Stoxx 50 - 2 possible scenarios?As always, there is risk in the markets and these two scenarios, whilst both bullish, offer differing paths. The equity markets really took off on Friday......was that a 3rd wave in progress or a massive fake out (on dodgy employment figures). I wish I knew the answer.

Euro Stoxx 50 (EU50 fut) - Impulse wave patternEuro Stoxx 50 (EU50 fut) is in 3rd internal of 3rd C up in ABC zigzag wave pattern, which confirm by the steepness of price movement.

EUR - SX5E - Long position..Bullish sentiment returned?If the EUR SX5E Top 50 Can consolidate above the EMA price should continue up to the next level on the Fibonacci retracement before breaking down or ranging lower. This should create a stronger EUR in the FX Markets against both Major/Minor Pairs

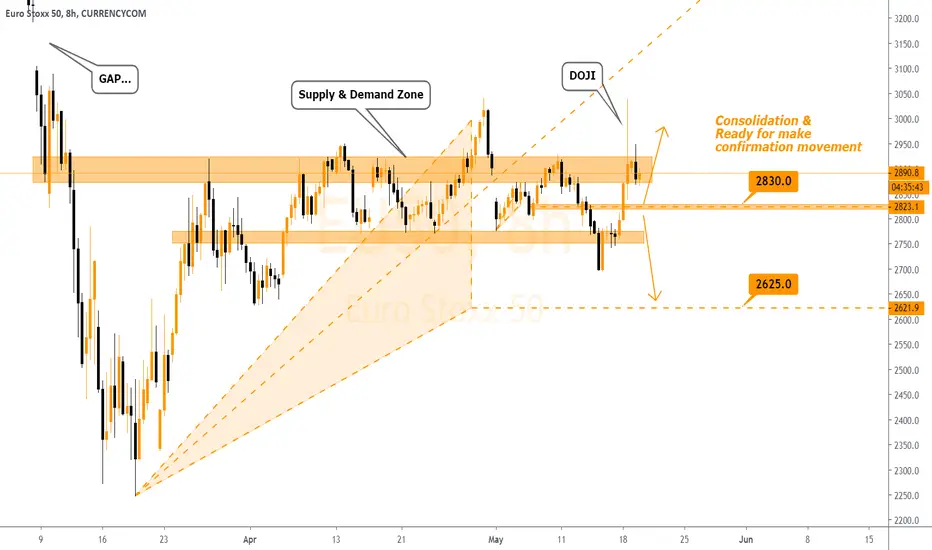

EU50 Decision Level is nearEU50 Decision Level is near

Potential long continuation is posible but the price into a technical perspective due to the massive Doji formation

Lets wait for a confirmation in the market

Remember that fundamentals for European Union is not the best

Pair to look at EURUSD, EURJPY, EURAUD, EURCAD ...