Quick View: $UAL- On the Hourly chart, bullish crossover with pullback already recorded. EMAs always in a bullish order

- The daily sees a first bullish crossover

1UAL trade ideas

OptionsMastery: Inverse head and shoulders on UAL! 🔉Sound on!🔉

📣Make sure to watch fullscreen!📣

Thank you as always for watching my videos. I hope that you learned something very educational! Please feel free to like, share, and comment on this post. Remember only risk what you are willing to lose. Trading is very risky but it can change your life!

United Airlines Holdings, IncKey arguments in support of the idea.

International routes continue to experience high demand. While the U.S. domestic market is in a less favorable position, especially the low-cost carrier (LCC) segment, the company is benefiting from foreign tourists. However, it's worth noting that the U.S. Travel Association (USTA) reports the opposite: demand from U.S. citizens for domestic tourism remains strong. We expect the situation in domestic flights to improve by summer 2025. During the reporting period, United emphasized that its premium offerings continue to drive revenue growth, with demand from American tourists for international flights remaining stable.

Our 12-month forecast maintains the possibility of a positive surprise for the company. UAL’s pricing power is generally stronger than that of competitors, allowing the company to maintain a high level of revenue per passenger mile and profit margins.

Progress in tariff negotiations has given a strong boost to the stock. Currently, UAL shares are trading above their 200-day moving average with an RSI near overbought levels. However, if political progress continues, this momentum could persist. The 2-month target price for UAL is $97, and we recommend setting a stop loss at $72.8.

The 2-month target price for UAL is $97. We recommend setting a stop loss at $72.

UAL - Bottoming out?Rising momentum is seen for UAL after mid-term stochastic oscillator performs an oversold crossover and rising momentum. Furthermore, the 23-period RSI has rose steadily above the zero line.

Meanwhile, price action saw a strong potential inverted head and shoulder with an ascending triangle in place. Ichimoku's conversion and base line has performed a crossover, indicating an early signs of uptrend returning. Will buy spot or wait for a small retracement until 73.46. or 68.00 to enter a buy. 1st target at 100.00

United Airlines Holdings, (NASDAQ: $UAL) Surge 6% on Strong Q1Shares of United Airlines Holdings, (NASDAQ: NASDAQ:UAL ) saw a noteworthy uptick of 6% on Wednesday's premarket session after the industry leaders reported it swung to a profit in the first quarter as revenue hit a record high, sending shares surging in extended trading Tuesday, further extending gains to premarket session.

The Chicago-based carrier posted first-quarter revenue of $13.2 billion, up 5% year-over-year and above the analyst consensus from Visible Alpha.1 Adjusted net income of $302 million, or 91 cents per share, compared to a loss of $50 million, or 15 cents per share, a year earlier, and also topped Wall Street’s estimates.

United Says It Expects 'Resilient' Earnings in Q2

The results come amid an uncertain economic environment for airlines. Last week, Visual Approach Analytics warned that air travel could face "demand destruction" as a result of the Trump administration's tariff policies, and rival carrier Delta (DAL) withdrew its full-year outlook, citing “current uncertainty."

Looking ahead, United said it expects "resilient earnings" in the second quarter and full fiscal year, despite macroeconomic challenges. The airline said it plans to reduce off-peak flying on lower-demand days.

Technical Outlook

United shares jumped nearly 7% in after-hours trading, extending gains to Wednesday premarket session. The stock has lost nearly a third of its value so far in 2025 through Tuesday’s close. The daily price chart depicts a bullish flag pattern with the asset gearing to break the ceiling of the flag - a move that will cement the bullish campaign for NASDAQ:UAL shares.

Further more, with the RSI at 44.97, NASDAQ:UAL shares are well ready for a bullish campaign capitalizing on the moderate momentum of the market.

United Airlines Holdings, Inc. (UAL) In the fourth quarter of 2024, United Airlines reported an operating profit of $1.5 billion on revenue of $14.7 billion, achieving a margin exceeding 10% due to strong winter demand.

MORNINGSTAR.COM

Analysts have set a median price target of $113.88 for UAL, with estimates ranging from a low of $100.00 to a high of $150.00.

I think $UAL have potential for a big drop comingRaising Wedge on UAL. I think once this trend is over it can fall to 90 a share i will be shorting in the 110s

Trading Journal UAL was surprsingly leading while market was going through its correction. Who knew airlines stocks can be a growth stock in 2024. Anyways, I bought on the breakout, it trended nicely higher, earnings gap ( I added more). Unfortunately my bought price went higher and then it sold off two days.

It hit the stop of -7% SO I have to get out.. but the stock looks good even though there was two days of heavy selling volume days

Robust travel demandUpdate: I'm in long. There is a chance for a pullback where I expect to be able to average in my order for a better price, so I'm not fully sized, but I still don't want to miss out if we push up from here.

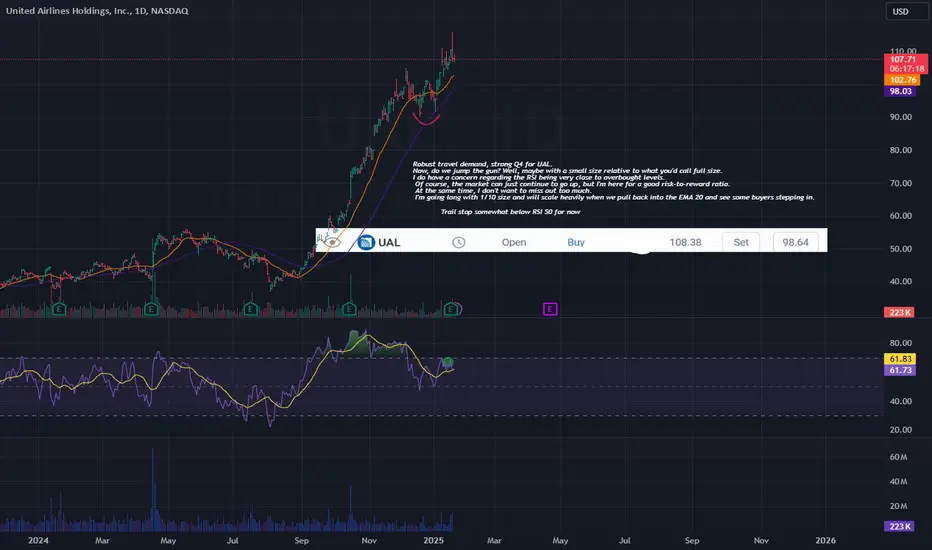

Robust travel demand, strong Q4 for UALRobust travel demand, strong Q4 for UAL.

Now, do we jump the gun? Well, maybe with a small size relative to what you'd call full size.

I do have a concern regarding the RSI being very close to overbought levels.

Of course, the market can just continue to go up, but I'm here for a good risk-to-reward ratio.

At the same time, I don't want to miss out too much.

I'm going long with 1/10 size and will scale heavily when we pull back into the EMA 20 and see some buyers stepping in.

UAL .. United Airlines levels and corresponding volumeJust a quick snapshot of the 30 min chart with a volume @ price footprint.

Those lines have some big air gaps which supported wild moves, both up and down.

So if good numbers... it hits those three bars above...if bad, then you have a three count on the way down...

UAL United Airlines Holdings Options Ahead of EarningsIf you haven`t bought UAL before the previous earnings:

Now analyzing the options chain and the chart patterns of UAL United Airlines Holdings prior to the earnings report this week,

I would consider purchasing the 105usd strike price Puts with

an expiration date of 2025-1-24,

for a premium of approximately $4.05.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

One Good Trade: UAL Broke OutUAL had a previous strong slide along the bands rally and then it pulled back into a complex pullback. It looked like bears had control a few weeks ago but now we broke out of the complex pull back with new momentum and then retested the breakout point creating a higher low and with yesterday's price, a new relative high.

looking for a pinch on the bottom 2 BB and also stochs to retracAs many indicators have this coming down, it doesn't seem like there is much room left for it to go before we see a reversal. Looking at 20 or lower on the stochastic and a few more points on the trend before I look for a reversal.

Head& shoulders on UAL. Again a clear head& shoulders on UAL. Maybe tomorrow but propably Monday to Wednesday we'll see if it completes or not

40% rapid descent for United Airlines holding, IncOn the above monthly chart price action has enjoyed a 180% upward move. There is evidence in the chart for a strong pivot, which includes:

1) Price action strikes legacy support for resistance test.

2) No market structure backtest to confirm support on breakout. A 40% correction is required to confirm.

3) On the 5 day chart (below) 17! Green candles print until market resistance. This is the strongest rally ever in the history of this stock before a market pivot. Previous to that was the 9 straight green candles on October 2016, which was followed by a 25% correction.

4) Short interest, 4%.. the market is far too bullish.

Is it possible price action continues to rise? Sure.

Is it probable? No.

Ww

5 day

$UAL. New meme stock. To the moonUnited airlines, nothing short of unprecedented move. In four months quadrupling shareholders value. Nothing short of spectacular. However, according to Simply Wall Street fair value is at $17.62. Fundamentally nothing changed in the last 4 months, at least not to cause this kind of move. Technically both the decline from Dec 2019 and the moonshot from August 2024 have moved at exactly same angle. And if this happens again one can expect the next downturn to be quick. Might consolidate before heading down like in the last cycle. Time will tell. I see it going to $114, Blow off maybe $120 ish, then down.

Time will tell

EVERY INDICATOR IS AN ANSWER IN THIS CASE THE MACD DEATHCROSSAfter showing signs of making its way higher, the MACD indicates a more bearish stance on the horizon for this ticker, mid-70s, in the coming sessions.

Short Term Play Targeting 80$ PutsThe stock is extermely overbought on different timeframes. So far the puts have not paid off but the stock will have to retrace at some point. Targets on 2hr chart.

United Airlines Holdings, Inc. (NASDAQ: UAL) 1. Company Overview

Headquarters: United Airlines Holdings, Inc., based in Chicago, Illinois, operates globally with a robust domestic and international flight network. It’s part of the Star Alliance, enhancing its global reach.

Market Position: United is one of the largest U.S. airlines by fleet size, with strategic expansions in international routes. It leverages partnerships, fleet modernization, and customer loyalty to compete in the post-pandemic aviation industry.

2. Financial Performance

Q3 2024 Highlights: United reported revenue of $14.8 billion, with a year-over-year profit dip of 15% due to rising fuel and operational costs. However, strong passenger revenue from leisure and business travel balanced this impact. Earnings per share (EPS) exceeded analyst expectations, supporting a strong positive market sentiment around UAL stock.

Revenue and Earnings Forecast: Analysts project revenue growth of 7.1% in 2025, reaching approximately $61.3 billion, with EPS growth at 18.5%, totaling an expected $12.29. This forecast reflects optimism for United’s revenue resilience and cost control strategies. The company’s forward P/E ratio of around 7.12 positions it competitively within the sector.

3. Key Developments and Strategic Initiatives

Route Expansion: United’s strategy focuses on capturing market share in high-demand regions. Recently, United announced new routes to Africa, Europe, and Latin America, catering to a growing base of international travelers, particularly in business and luxury travel segments.

Loyalty Program Adjustments: United has revised its MileagePlus program requirements, increasing thresholds for spending and miles. This move is designed to incentivize frequent, high-spending travelers, aligning with a broader airline trend to maximize revenue from loyalty programs.

Cost Control and Operational Efficiency: United has streamlined fleet maintenance and optimized routes to manage expenses. However, external factors such as fuel costs and potential union negotiations remain areas of focus for continued cost management.

4. Market Sentiment and Analyst Ratings

Current Price and Target: UAL shares closed at $87.51 on November 8, 2024. Analysts provide a 12-month average target of $78.94, suggesting a potential downside due to high valuation following recent stock gains. However, most analysts rate UAL as a “Strong Buy” due to strategic growth and profitability projections.

Short Interest: UAL has a short interest ratio of 5.05%, slightly increased from last month, indicating some investor caution. The “days to cover” ratio of 2.1 is within normal range, suggesting minimal short pressure.

5. Risks and Challenges

Fuel Costs and Operational Costs: Rising fuel prices and increased maintenance costs have impacted profitability. United is countering these through fleet upgrades and operational efficiencies but remains vulnerable to cost volatility.

Regulatory Changes: Recent policies from the Department of Transportation, mandating more flexible refund options for flight cancellations, may impact United’s ability to manage cash flows from ticket sales effectively. This regulatory focus on consumer rights could shape industry practices moving forward.

Market Competition: United faces intense competition from both legacy carriers like Delta and low-cost airlines. Its growth strategy relies on attracting higher-margin customers through enhanced service offerings, new routes, and loyalty incentives.

6. Growth Outlook

International Market Expansion: United’s aggressive route expansions aim to capture emerging market growth in travel demand, especially in underserved regions and high-demand routes.

Technological Innovation: United is investing in technology to enhance operational efficiencies and customer service. Digital innovations in booking, maintenance, and in-flight services are expected to improve customer experience, helping to retain high-value clients and boost loyalty.

Revenue and EPS Prospects: Revenue is projected to increase steadily through 2025, supported by expanded travel demand and strategic pricing. Analysts remain cautiously optimistic that United’s focus on operational efficiencies and customer loyalty could drive sustained profitability.

Summary

United Airlines is well-positioned for growth, with strong analyst support and significant expansions in high-demand markets. While high costs and regulatory changes present challenges, United’s strategic initiatives and positive earnings trends contribute to a cautiously optimistic outlook. The stock is rated as a "Strong Buy" among analysts, reflecting confidence in United’s strategic direction and growth potential in the coming year.

UAL overextendedshould hit a brick wall once 80$ is reached, as per my previous analysis i expected it to be the final target. will be shorting today 79.9 - 80.9 - 81.9, and 78$ as a quick scalp

$UAL with a neutral outlook following its earnings #StocksThe PEAD projected a neutral outlook for NASDAQ:UAL after a positive under reaction following its earnings release placing the stock in drift A with an expected accuracy of 70%.

UAL United Airlines Holdings Options Ahead of EarningsIf you haven`t bought UAL before the previous earnings:

Now analyzing the options chain and the chart patterns of UAL United Airlines Holdings prior to the earnings report this week,

I would consider purchasing the 62.5usd strike price Calls with

an expiration date of 2025-1-17,

for a premium of approximately $6.40.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.