baba wait and see option contracts, identifying a trend reversal, lets wait about a week or so and lets keep an eye on it

AHLA trade ideas

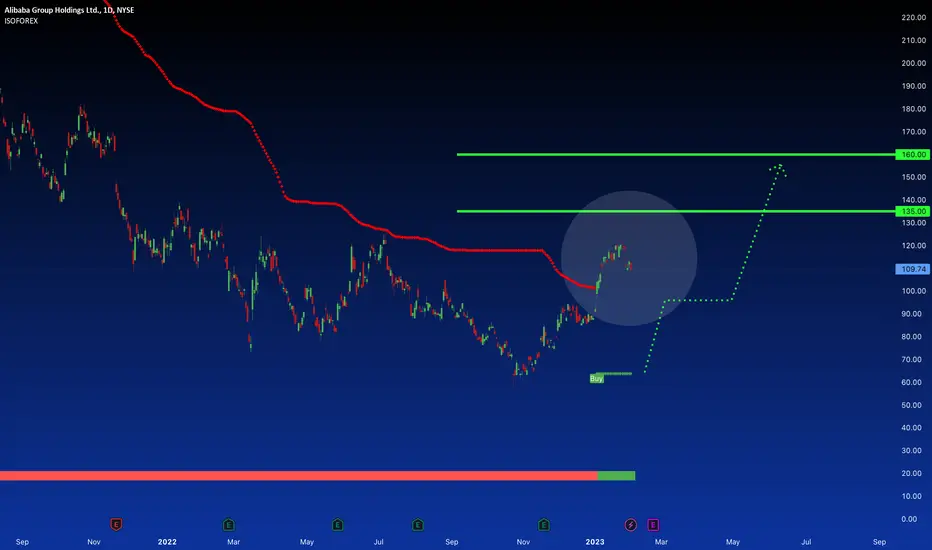

BIG $BABA HnS Swing Position IdeaSupport in gray box isnt only valid support.

Generally just looking for the next shoulder to form, but this might already be a good entry area.

This would be a beautiful HnS and the breakout could take us far.

Keep a lookout for where else the shoulder may form, break gray bos and shoulder can still form lower, hard invalidation is if we get new lows below 'head'.

9988|Alibaba Wave Projection | Bullish Divergence - Rebound?Price action and chart pattern trading - Minor downtrend ending diagonal pattern with MACD bullish divergence

> A possible wave 4.3 minor downtrend wave at the lower support 0.786 extension of wave 4.1 and upcoming rebound wave 4.4 to 0.382 - 0.5 fibonacci retraced from wave 4.3.

> Target upside +10 - 12% while downside is -6%, RRR: 1.5:1

> The final downtrend wave 5 could be slightly below Target H&S zone.

Always trade with affordable risk and respect your stoploss, nothing is 100%

BABA weekly chart make or breakOn the weekly chart, BABA is currently forming a bullish reversal pattern known as an inverted head and shoulders. However, it is also at a critical support level that needs to hold if the bulls want to continue the uptrend. The $85-$89 range has been a strong support and resistance area in the past and needs to act as support now to propel BABA higher. On the bearish side, the January high was a lower high, which could be interpreted as a bear pullback with targets around the previous low or even lower.

Furthermore, the increasing volume on the last week's big drop is more bearish than bullish, and the price is below all major moving averages, indicating a bearish trend.

Although the RSI has cooled down and is ready to go up again, the MACD green ticks are ticking lower while the MACD line is turning, and it seems to be on the verge of crossing below the signal line.

Overall: BABA is in a situation where the bulls need to step in, or the stock will experience further pain in the coming weeks or months. The price is currently at a crucial support level, and it needs to hold to initiate an uptrend and possibly trigger the inverted head and shoulders pattern. If the price breaks above the January high, it would confirm the pattern as there is a neckline.

However, if buyers do not step in and sellers continue to sell, the stock will experience a bearish pullback, and it may drop to lower levels. Additionally, $60 is a significant low from 2015, 2016, and 2023, and it should act as a support level. If this level does not hold, BABA may test the all-time low (ATL).

BABA (Long Swing Idea - trendline bounce, fib retracement, S&R)Trade Rationale:

BABA is looking great for a 2 to 4 week expiration Options Call swing play. It is currently holding a previous resistance turned support area between $100 and $103. In confluence with this level, BABA has also completed a fibonacci retracement back to the 50% level almost perfectly. It is also holding the 200 ema on the 4H and Daily timeframes in confluence with the formation of a falling wedge and 3rd touch on the current uptrend support line (created from the lows of the Oct 24th and Nov 9th daily candles). While we're at it, let's go ahead and add in the bullish divergence on the 4H and Daily timeframes. NOTE: There are currently 4 gaps on BABA's chart right now, 2 above current price and 3 below current price.

Trade Idea:

I am looking to play calls with at least a 2 to 4 week expiration date with a strike price of 107c (Targeting the first gap above current price between $106.63 and $107.79.) The more time on the contract the less THETA decay eats away at the value of the contract. Also consider a contract with a breakeven close to your target as well as an options contract that doesn't have high Implied Volatility, because if IV slows and begins to revert back to the mean value your options contracts could still loss value from IV crush. Basically control for the effect that the options greeks will have on your contracts to maximize gains and minimize losses. My ultimate take profit is at the origin of the falling wedge which is also the beginning of the second gap above the current price between $113 and $116. I will look to place a STOP LOSS (Exit Trade) below $101.87 and 100.53 and will exit if a daily candle closes below these levels.

Alibaba | Fundamental AnalysisThe previous several years have been petty tough for e-commerce giant Alibaba Group, to say the least. After peaking amid the coronavirus pandemic, the company lost nearly 80% of its value over the next two years. Since then, the company has rallied, up 78% from its October 2022 low, but still a far cry from the levels that preceded the COVID-19 pandemic.

Needless to say, these have been challenging times for Alibaba and its investors. And while the company still has a considerable way to go and overcome challenges, here are a few reasons to be optimistic about Alibaba stock.

China begins to roll back quarantine restrictions

China's anti-COVID-19 policies have undoubtedly hurt Alibaba. The ban has negatively impacted China's overall economic activity, and taking into account Alibaba's size and how entrenched it is in the Chinese economy (which is the second largest in the world), it has had a direct impact on the company.

In addition to people spending less during store closures in China, this policy has also hurt Alibaba's logistics network, particularly due to road and highway closures. All of this led to the company's first-ever low YoY revenue growth in June 2022.

But there should be brighter days ahead. No one can say for sure when China will fully open its doors, but some parts of the country have begun to take steps in that direction in December last year. If the situation is similar to the U.S., a reopening in China could boost economic growth with the help of improved spending and household consumption. Alibaba should benefit from this.

Cloud business growth

Cloud infrastructure and services are becoming an important part of any business that uses the Internet for its operations. In Q3 of 2022 alone, global spending on cloud infrastructure services rose to $57 billion, bringing total spending in the past 12 months to $217 billion.

With a 5% market share, Alibaba Cloud lags behind market leaders Amazon Web Services, Microsoft Azure, and Alphabet Google Cloud (34%, 21%, and 11%, respectively), but the trend is there.

For the quarter that ended Sept. 30, 2022, Alibaba Cloud revenue grew 4% YoY to more than $2.9 billion, driven by public cloud growth. More encouraging, however, should be the growth in Alibaba Cloud's non-Internet Industry (NII) customers. The number of NII customers grew 20 percent year over year to 58 percent of total cloud revenue.

These strong results were achieved at the expense of government services, telecommunications companies, and financial services. Cloud services are integral to all three of these areas, which could lead to long-term recurring revenue for Alibaba.

The global cloud computing market is projected to reach more than $1.7 trillion by 2029, at an average annual growth rate of just under 20 percent. Even if Alibaba Cloud can't make the top three in market share, it will have plenty of room for success as it expands the overall pie.

Jack Ma's departure from Ant Group

No one was surprised when Jack Ma, Alibaba's founder, announced he was stepping down as chairman. Although Ma had led Alibaba's development and triumph, his departure did not affect the company too much because the leadership was already in new hands.

However, many were shocked when Ma announced that he was giving up control of fintech giant Ant Group, in which Alibaba has a 33% stake. Ant Group was scheduled to go public in November 2020 with a capitalization of about $37 billion, but the stock was canceled at the last minute largely because of regulatory scrutiny.

With Ma no longer controlling Ant Group, the likelihood that the company could restart its initial public offering (IPO) process has increased significantly, though it likely won't be smooth. Ant Group's IPO could bring Alibaba a large cash infusion that could be used as China's quarantine restrictions ease.

Baba looking for a bottom again (potential bullish long term)The falling wedge has played out with an extension and we have now hit support so a short term bounce is likely. We still have a gap to fill and potential support levels to test should we fail to rise above the longer term Inverse H&S bottom for now (this pattern remains valid should we remain above the all time lows during this correction). Ultimately, expectations are for a move to the 180 level once current broader market weakness and correction plays out. Looking to take this long trade once the next support level is tested.

Not investment advice and do your own due diligence!

BABA Alibaba Options Ahead of EarningsIf you haven`t sold BABA when Charlie Munger did:

or reentered when it was cheaper than the IPO:

Now looking at the BABA Alibaba options chain ahead of earnings , I would buy the $110 strike price Calls with

2023-8-18 expiration date for about

$10.20 premium.

If the options turn out to be profitable Before the earnings release, I would sell at least 50%.

I have chosen that expiration date to allow me to be wrong and not close the position and to have a bigger gain by the expiration date, if BABA Alibaba keeps on climbing.

Looking forward to read your opinion about it.

BabaAfter a great move to the upside a month ago baba has non stop been selling off. Starting to slip off peoples radars or at least mine. We’ll now that I’m finally coming back to it I’m reaizinf how bullish this chart is ! I think if we can start piping above 105 we can see this bull trend start the next leg to the upside ! This will be a monster idea to start to pay close attention to!!!

Looks like we curently just rejexted off that upper trending line so next support down can still make a new low. Mabey that 100$ psychological support will be the area to buy. Next fib down is also 97 but I think that would be a bit low for this specific trend line drawing. Howver if we do get there I would reevaluate this idea and pattern drawing.

For now watch 100$ support and 105 reistance !

ALIBABA Potential for Bullish Rise | 14th February 2023Looking at the H4 chart, my overall bias for ALIBABA is bullish due to the current price being above the Ichimoku cloud , indicating a bullish market.

Looking for a pullback buy entry at 92.85, where the overlap support is. Stop loss will be at 84.32, where the previous overlap support is. Take profit will be at 121.28, where the recent high is.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.