US10Y : Going UP - WHY???Bond yield has been going up these past few days. What is happening? Many would think that this is because of recent events like the 'hot' jobs market and sticky headline inflation which may cause the Fed to continue hiking rates - higher/longer. Sounds plausible??? Maybe. It may look like the MARKET is now going along with the Fed instead of disagreeing with it earlier by driving yield down.

Note that inflation expectation is FALLING.

There is ONE consequence of a HIGHER yield. ASSET price will come down. The stock market and home prices will CRASH.

Already the country's finances is in a BAD shape. US is expected to pay up to $1T in interest alone. The consumer is already drowning in debt as evidence by the higher credit card debt at a time when interest is also a an all time HIGH. Both country and people may not last long holding up their finances.

So what is causing yield to rise?

One third of US DEBT outstanding is maturing this year. That is nearly $7T. And of the $7T, roughly $4T matures in the first 4 months of 2023. Since all these debt needs to be roll-over, this causes an increase in supply which means HIGHER YIELD!!!

This is crazy. With high yield, asset price will fall which leads to RECESSION. With recession, tax revenue will fall which will require US to borrow more. All these is happening while the Fed is doing QT!!!

So what kind of landing are we expecting? It is definitely not a SOFT landing. It is also not going to be a HARD landing. In my opinion, when debt is so HIGH, both public and private, it is going to be a CRASH LANDING. The consequence for the US and the entire world is devastating.

Good luck to us all.

US10Y trade ideas

US10Y - ST Pullback in Yield Ahead? Charted is a proposed price pathway for the 10yr T Bonds.

I'm looking for an easing in yield soon... in the 4.125 area (.786 Fib level) specifically, sometime in early March.

This will represent the top of the b wave of wave 4 off the Aug. 2020 low.

This expectation flies in the face of recently released inflation related news. As such my parameters are well defined here. A move beyond the afore mentioned yield will make me reassess the trade.

I'm seeing correlated markets showing signs of synergy with the expected outcome of this move.

Specifically I am expecting a move up in oil, technical ST pullback in DXY and a technical bounce in gold...which will fail and complete a fantastic short set-up.

See my Gold idea...

us rates trend downUs rates are getting weaker and showing that rates might be at least peak and need correction.. but just follow trend.. not predicting it.

US 10Y Bond - Correction lowerPrice did not do an impulse from Oct 2022, so we are in a complex correction.

Targetting a move to 3.4 for now.

US10Y - TLT Part 2Unfortunately this website won't go past 20 years for 30Y yields, so I'm posting 10Y

Anyways, the notion that the Fed is done at 5% is pure fallacy. We're seeing inflation we haven't seen since the 80's, and a lot of it is structural. Aside from labor shortage and Russian oil, we have way too much deficit spending by the government and the Fed balance sheet exploded during the COVID QE.

Having taken out college loans at 10% interest, I wouldn't be surprised at all if yields went above 10%. People pegging the peak at 5 or 6% are gonna be in for a freakin' shock. I also expect rates to stay high until the Fed balance sheet comes back down, and we're talking 10 years or so because they're under water on all of the MBS they hold.

That doesn't mean the stock market has to go down though, the stock market went up in that era aside from the '87 crash. Focus in inflation trades, stay away from bonds, especially TLT, lol.

Note: I realize TLT is 20Y+, but no historical charts available for anything besides 10Y

Fading Bonds rally Long US10Year Yield / Short TY Future fading the YTD bond rally driven by Central Banks Pivot hope misread by markets, it seems that the short positioning has exacerbated the buying so far this year.

Things should start to normalise into month end and ahead of FED/ ECB meetings in February.

Short US10Y Future - Expect the Yield rise by 20bps

US10Y, XAUUSD AND DXY CONFLUENCE Hi trader

The xauusd is trying support and the us10yr is testing previous resistance, but the dxy is already in a breakout phase, so guess? :)

My trading strategy isn't intended to be used as a signal service. It's a process of gaining knowledge of market structure and improving my trading abilities.

Like and subscribe and happy trading to all

US10Y SELLWelcome to my account. There is a high probability that the market will go down. With a strong model formation. Double button. He also made the area retest twice. The price fails to breach the broken resistance 3.900. I think the price will be negative over time. And we see its price is 3500. In the first stage

10 Year yield Elliot wave count ideaobviously its risky to try to put EW on something like the US10Y yield with so many issues in the world right now but i couldnt help notice how clean the count looks at the moment.

NOT trading advice.

Yields in the long runTaking a long term view, we should never forget what 10y yields did this year. We are in a era of high treasury returns, right in time as the governments safety is at its worst.

US10Y - consolidating TVC:US10Y will consolidating for a while. Can tell a direction until it breakthrough the resistance or the support.

2023 Market Projections: Leading Indicators and AnalysisTVC:US10Y

The recent market response to data on CPI , PPI, and the selloff in the bond market, coupled with hints from the Fed about potentially raising rates towards 5% to 5.25%, provide important insights into where the markets could be heading in the coming weeks.

Looking at the weekly chart of the 10-year Treasury yield, we can see a massive rising wedge pattern with a bull flag inside the wedge . The break out of the bull flag last week has a target of 5% to 5.25%, which aligns with the Fed's projected peak policy and the top of the wedge in the chart. There are some bullish signs in this chart, a hidden bullish divergence on the weekly with both the RSI and MACD , indicating a bullish continuation of the trend. Additionally, there is a bullish divergence on the daily chart , as shared a few days ago.

These signals increase the likelihood of a bullish move in the 10-year yield, and if this plays out as projected, it could lead to high selling pressure in markets, including the stock market and crypto. Higher yields can reduce the profitability and spending power of companies and individuals, and make stocks and cryptocurrencies less attractive as investment options. It's important to keep a close eye on the bond market and monitor any potential impacts on other markets.

This could mark the final leg down or a bottoming process in the current bear market, with the last leg down typically being a massive one. In the coming weeks, there may be a triple bearish divergence that develops on the 10-year yield, which could signal a nearby bottom in bonds. The stock market is expected to follow suit weeks later.

It's worth noting that this analysis is based on confluence and projections around recent developments, leading indicators, and technical analysis projection methods. However, there are no confirmations on many aspects of it yet, and there is always a degree of unpredictability in financial markets. Therefore, it's important to acknowledge the uncertainties and potential risks involved in making projections based on technical analysis . It's also important to emphasize that this is not financial advice, and readers should always do their own research (DYOR) before making any investment decisions. Seeking professional financial advice before making significant investment decisions is also highly recommended.

10-Year Treasury Yield Ready to Extend Advance to 2022 Highs?The 10-year Treasury yield has been rising since the end of January in the aftermath of a Bullish Morning Star candlestick pattern.

Now, prices are approaching the December high at 3.905 after confirming a breakout above a falling trendline from October.

Meanwhile, a bullish Golden Cross is set to form between the 20- and 50-day Simple Moving Averages, further offering an upside technical bias.

Confirming a breakout above the December high exposes the 78.6% Fibonacci retracement level at 4.118 towards the 2022 peak at 4.335.

US10Y

Elliot would have bond yields for a correction now. Out of the low we have 5 clear waves up. We've got the big spike out 5 and also around this time we have a mass acceptance/expectation of the rally in this going further.

This looks like a breakout, it looks like it's going higher - but in the EW cycle it would be due a sharp down first.

(This is TA. Not a fundie forecast, but news sometimes catches up)

US 10 YEAR YIELDS (LONG ANALYSIS)The US10Y has moved as we expected from our first analysis and up 11% SO FAR🙌. We have finally seen a break above the wedge, indicating that bullish momentum is getting stronger. We still have plenty more upside to go, for the rest of Q1.

This long analysis is positively supported by DXY bulls & Gold bears, which we are currently witnessing take place as well. All markets playing out well!

Yield InversionReally strange market, the yield inversion continues to grow. This site actually allows price calculations, this is 10Y yield minus 2Y yield.

Stock market still acting bullish, but I'm not feeling it.

US Government Bonds 10YR Yield LONGUS Government Bonds 10YR Yield. Time-frame = 1 month. In 2005-2007 (red circle) - a double top was built (determined automatically by my script) from which the downward movement began for further accumulation. 2009-2019 (green rectangle) - long-term accumulation (balance). 2019-2022 (blue circle) - responsive activity (long entry by key players). 2022-2023 long to the upper limit of the balance. The last 3 months - a retest to one of the key balance levels. 2023 - expect further upward movement towards the 5.000% area (towards the upper border of the double top)

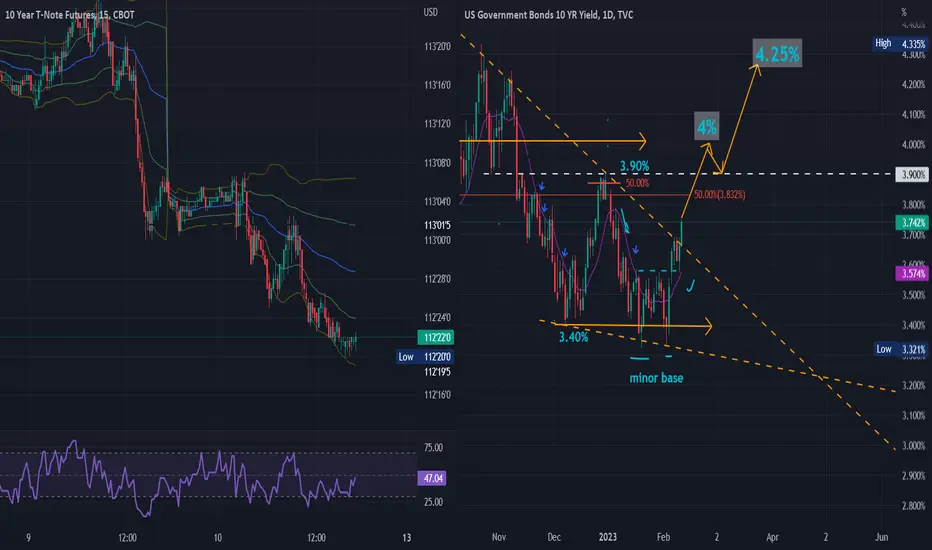

US 10-year yields could test 4% after breaking out of wedgeFollowing the blowout non-farm payrolls number (Feb 3rd), 10-year yields enjoyed a productive week, confirming a minor base in the 3.33% area ahead of a falling diagonal breakout. This has the 10-year poised to re-test 3.90% with possible room to test the psychological 4% region. Look for over-stretched daily indicators to limit potential upside after Tuesday's US Inflation report. That said, a hotter CPI print could trigger a move to 4% easily! At that point, 3.90% would likely become support for a long-term target of 4.25% to 4.35%. If, however, the 3.90% region proves to be more resistant than expected or perhaps isn't even tested, then the 3.58% to 3.40% area will largely determine whether US 10-year yields are continuing to trend higher.

Sell ZN (10-year futures) @ spot (112'22) or Buy ETF TBT @ 30

Target: ZN 112 (1st) 110 (2nd) TBT 32.67 (1st) 40 (2nd) target***

Stop: ZN 114 TBT 28.13

Yield inversion vs SPX - We are building a baseSPX goes up as the yield inversion builds a base and starts rising.

Best time to sell at the top is when yield curve starts curving up.

The key is looking at the RSI levels.

For DOT COM bubble + financial crisis, RSI started going up. Clear bullish divergence.

US10Y : Comparison with the EFFRThese last few days have seen bond yield rising. It is as a direct result of the recent 25bps rate hike.

If you look at the chart above, which is the US10Y less the EFFR, it seems the difference had reached the MAXIMUM based on historical results. Which means to say, the US10Y had already reached the MAXIMUM. From now on, any rise would be in lockstep with the amount of future potential rate hike.

We can also see that once the above difference reached its historical low, the next question that arise is when the Fed will start to PIVOT and cut rates. If you look at 2007, it can actually take some time.

P/S : As always, do not just believe what I say. Use your common sense.

What Makes this Yield Curve Inversion so Different?An Inverted yield curve in the context of a 2% inflation environment holds a different meaning than, an Inverted Yield Curve in a high inflation environment......

Market Expectations of Disinflation led to this Inverted Yield Curve:

The Nominal Inversion of the yield curve is caused by the expectation that inflation will fall steadily. Believe it or not an Inverted Yield Curve is the best case scenario for the Fed. A Nominal Inversion during a high inflation period shows that markets have confidence/belief in the Fed's Policy to bring inflation down to 2%. Most of the inversion seen in the yield curve today is nominal....

The Nominal Yield Curve vs. the Real Yield Curve:

Nominal Yield – Real Yield = Breakeven Inflation Rate.

Real Yield = Nominal Yield - Breakeven Inflation Rate

The Breakeven Inflation Rate represents what inflation would have to be in order for investors to “break even” when buying a bond. The general thought process is: If you believe the inflation rate will be greater than the breakeven rate buy Treasury Inflation-Protected (TIP) bonds.

Notice how the Yield Curve for Nominal Yields is a lot more Inverted than the Yield Curve for Real Yields. Hence, the inversion in today's Yield Curve is mainly nominal. Below I calculate out the Real Yield for the treasuries with Breakeven TIP Data from FRB St.Louis.

Nominal Break-even

US02Y: 4.3% - (RealYield) = 3.0% = 1.3% RealYield for US02Y

US05Y: 3.6% - (RealYield) = 2.3% = 1.3% RealYield for US05Y

US07Y: 3.6% - (RealYield) = 2.4% = 1.2% RealYield for US07Y

US10Y: 3.4% - (RealYield) = 2.2% = 1.2% RealYield for US10Y

US10Y/US02Y Nominal Yield Curve: 3.4% - 4.3% = -0.8% (Inverted)

US10Y/US02Y Real Yield Curve: 1.2% - 1.3% = -0.1% (Inverted)

The bond market expects for inflation to remain above trend the next 1-2 years and decrease dramatically after that. As you can see, the nominal yield curve is very inverted even though, the real interest rate is pretty much held constant across thee curve. The Real Interest Rate remains between 1.3% and 1.2%. The Yield Curve Inversion in Nominal terms is: -0.8% and in Real Terms is: -0.1%.

Partners in Crime: Unemployment and the Yield Curve:

When consumers start to save more, companies start to see earnings deteriorate. In turn, they cut costs by letting workers go. The US10Y/US02Y yield curve is a proxy for Unemployment. Unemployment rises as, the market starts to expect rate cuts from the fed. It is only when the spread on the US10Y/US02Y starts trending up does unemployment start to rise. The spread of the US10Y/US02Y yield curve starts to trend upwards when the 2 year rate plummets as, markets start to price in a recession. Currently, the Yield Curve is still declining signaling that unemployment will remain low.

So what does this all mean???

A recession is not as close as many people are saying. People have been calling for a recession since April. This yield curve also signifies that markets are more or less believe that the fed will engineer a soft anding and bring inflation back to the 2% target. If you don't believe the disinflationary narrative spread by the fed there is an opportunity for you to make money on what markets are mispricing.

What will you do the next time a fake guru waves an inverted yield curve in your face to scare you into a subscription?

US 10 YR Yield vs SPX hit a resistance that started other bottomZoom out and in Oct US 10 Year yields hit a supply level from Dec 2018 which started that big rally, we rejected hard from that in Oct. Now heading into resistance on shorter timeframes that started the other two major equities bottoms. If this rejects here which I think it can that will keep the rally continuing.

10Y US bond Yield at important junctureNear important Trend resistance and 200 MA, if passed it could trigger sell-off sentiment on equity markets

www.tradingview.com