Momentum Long + Short Strategy (BTC 3H)Momentum Long + Short Strategy (BTC 3H)

🔍 How It Works, Step by Step

Detect the Trend (📈/📉)

Calculate two moving averages (100-period and 500-period), either EMA or SMA.

For longs, we require MA100 > MA500 (uptrend).

For shorts, we block entries if MA100 exceeds MA500 by more than a set percentage (to avoid fading a powerful uptrend).

Apply Momentum Filters (⚡️)

RSI Filter: Measures recent strength—only allow longs when RSI crosses above its smoothed average, and shorts when RSI dips below the oversold threshold.

ADX Filter: Gauges trend strength—ensures we only enter when a meaningful trend exists (optional).

ATR Filter: Confirms volatility—avoids choppy, low-volatility conditions by requiring ATR to exceed its smoothed value (optional).

Confirm Entry Conditions (✅)

Long Entry:

Price is above both MAs

Trend alignment & optional filters pass ✅

Short Entry:

Price is below both MAs and below the lower Bollinger Band

RSI is sufficiently oversold

Trend-blocker & ATR filter pass ✅

Position Sizing & Risk (💰)

Each trade uses 100 % of account equity by default.

One pyramid addition allowed, so you can scale in if the move continues.

Commission and slippage assumptions built in for realistic backtests.

Stops & Exits (🛑)

Long Stop-Loss: e.g. 3 % below entry.

Long Auto-Exit: If price falls back under the 500-period MA.

Short Stop-Loss: e.g. 3 % above entry.

Short Take-Profit: e.g. 4 % below entry.

🎨 Why It’s Powerful & Customizable

Modular Filters: Turn on/off RSI, ADX, ATR filters to suit different market regimes.

Adjustable Thresholds: Fine-tune stop-loss %, take-profit %, RSI lengths, MA gaps and more.

Multi-Timeframe Potential: Although coded for 3 h BTC, you can adapt it to stocks, forex or other cryptos—just recalibrate!

Backtest Fine-Tuned: Default settings were optimized via backtesting on historical BTC data—but they’re not guarantees of future performance.

⚠️ Warning & Disclaimer

This strategy is for educational purposes only and designed for a toy fund. Crypto markets are highly volatile—you can lose 100 % of your capital. It is not a predictive “holy grail” but a rules-based framework using past data. The parameters have been fine-tuned on historical data and are not valid for future trades without fresh calibration. Always practice with paper-trading first, use proper risk management, and do your own research before risking real money. 🚨🔒

Good luck exploring and experimenting! 🚀📊

BTCUSD

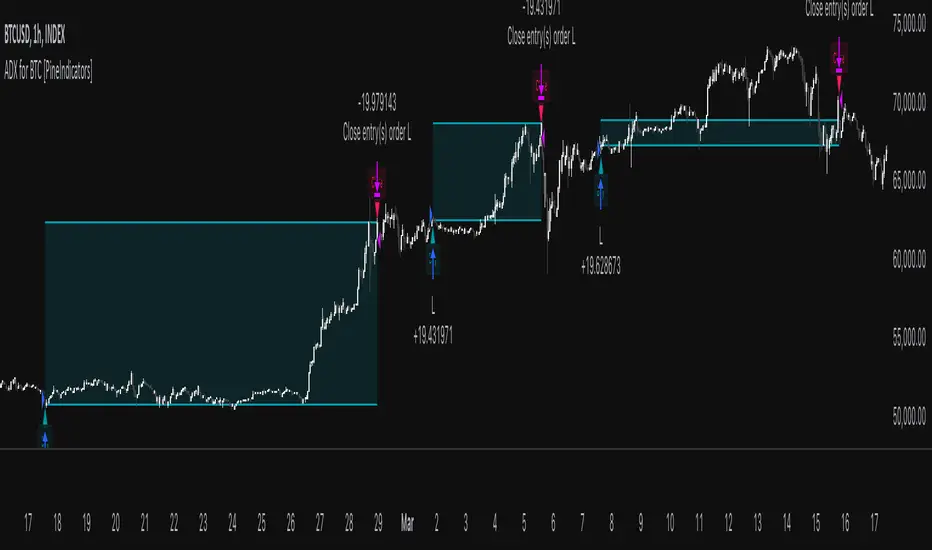

ADX for BTC [PineIndicators]The ADX Strategy for BTC is a trend-following system that uses the Average Directional Index (ADX) to determine market strength and momentum shifts. Designed for Bitcoin trading, this strategy applies a customizable ADX threshold to confirm trend signals and optionally filters entries using a Simple Moving Average (SMA). The system features automated entry and exit conditions, dynamic trade visualization, and built-in trade tracking for historical performance analysis.

⚙️ Core Strategy Components

1️⃣ Average Directional Index (ADX) Calculation

The ADX indicator measures trend strength without indicating direction. It is derived from the Positive Directional Movement (+DI) and Negative Directional Movement (-DI):

+DI (Positive Directional Index): Measures upward price movement.

-DI (Negative Directional Index): Measures downward price movement.

ADX Value: Higher values indicate stronger trends, regardless of direction.

This strategy uses a default ADX length of 14 to smooth out short-term fluctuations while detecting sustainable trends.

2️⃣ SMA Filter (Optional Trend Confirmation)

The strategy includes a 200-period SMA filter to validate trend direction before entering trades. If enabled:

✅ Long Entry is only allowed when price is above a long-term SMA multiplier (5x the standard SMA length).

✅ If disabled, the strategy only considers the ADX crossover threshold for trade entries.

This filter helps reduce entries in sideways or weak-trend conditions, improving signal reliability.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when:

✅ ADX crosses above the threshold (default = 14), indicating a strengthening trend.

✅ (If SMA filter is enabled) Price is above the long-term SMA multiplier.

🔻 Exit Conditions

A position is closed when:

✅ ADX crosses below the stop threshold (default = 45), signaling trend weakening.

By adjusting the entry and exit ADX levels, traders can fine-tune sensitivity to trend changes.

📏 Trade Visualization & Tracking

Trade Markers

"Buy" label (▲) appears when a long position is opened.

"Close" label (▼) appears when a position is exited.

Trade History Boxes

Green if a trade is profitable.

Red if a trade closes at a loss.

Trend Tracking Lines

Horizontal lines mark entry and exit prices.

A filled trade box visually represents trade duration and profitability.

These elements provide clear visual insights into trade execution and performance.

⚡ How to Use This Strategy

1️⃣ Apply the script to a BTC chart in TradingView.

2️⃣ Adjust ADX entry/exit levels based on trend sensitivity.

3️⃣ Enable or disable the SMA filter for trend confirmation.

4️⃣ Backtest performance to analyze historical trade execution.

5️⃣ Monitor trade markers and history boxes for real-time trend insights.

This strategy is designed for trend traders looking to capture high-momentum market conditions while filtering out weak trends.

Swing High/Low Pivots Strategy [LV]The Swing High/Low Pivots Strategy was developed as a counter-momentum trading tool.

The strategy is suitable for any market and the default values used in the input settings menu are set for Bitcoin (best on 15min). These values, expressed in minimum ticks (or pips if symbol is Forex) make this tool perfectly adaptable to every symbol and/or timeframe.

Check tooltips in the settings menu for more details about every user input.

STRTEGY ENTRY & EXIT MECHANISMS:

Trades Entry based on the detection of swing highs and lows for short and long entries respectively, validated by:

- Limit orders placed after each new pivot level confirmation

- Moving averages trend filter (if enabled)

- No active trade currently open

Trades Exit when the price reaches take-profit or stop-loss level as defined in the settings menu. A double entry/second take-profit level can be enabled for partial exits, with dynamic stop-loss adjustment for the remaining position.

Enhanced Trade Precision:

By limiting entries to confirmed swing high (HH, LH) or swing low (HL, LL) pivot points, the strategy ensures that trades occur at levels of significant price reversals. This precision reduces the likelihood of entering trades in the midst of a trend or during uncertain price action.

Risk Management Optimization:

The strategy incorporates clearly defined stop-loss (SL) and take-profit (TP) levels derived from the pivot points. This structured approach minimizes potential losses while locking in profits, which is critical for consistent performance in volatile markets.

Trend Filtering for Better Entry:

The use of a configurable moving average filter adds a layer of trend validation. This prevents entering trades against the dominant market trend, increasing the probability of success for each trade.

Avoidance of Noise:

The lookback period (length parameter) confirms pivots only after a set number of bars, effectively filtering out market noise and ensuring that entries are based on reliable, well-defined price movements.

Adaptability Across Markets:

The strategy is versatile and can be applied across different markets (Forex, stocks, crypto) due to its dynamic use of ticks and pips converters. It adapts seamlessly to varying price scales and asset types.

Dual Quantity Entries:

The original and optionnal double-entry mechanism allows traders to capture both short-term and extended profits by scaling out of positions. This adaptive approach caters to varying risk appetites and market conditions.

Clear Visualization:

The plotted pivot points, entry limits, SL, and TP levels provide visual clarity, making it easy for traders to track the strategy's behavior and make informed decisions.

Automated Execution with Alerts:

Integrated alerts for both entries and exits ensure timely actions without the need for constant market monitoring, enhancing efficiency. Configurable alert messages are suitable for API use.

Any feedback, comments, or suggestions for improvement are always welcome.

Hope you enjoy!

Rsi Long-Term Strategy [15min]Hello, I would like to present to you The "RSI Long-Term Strategy" for 15min tf

The "RSI Long-Term Strategy " is designed for traders who prefer a combination of momentum and trend-following techniques. The strategy focuses on entering long positions during significant market corrections within an overall uptrend, confirmed by both RSI and volume. The use of long-term SMAs ensures that trades are made in line with the broader market trend. The stop-loss feature provides risk management by limiting losses on trades that do not perform as expected. This strategy is particularly well-suited for longer-term traders who monitor 15-minute charts but look for substantial trend reversals or continuations.

Indicators and Parameters:

Relative Strength Index (RSI):

- The RSI is calculated using a 10-period length. It measures the magnitude of recent price changes to evaluate overbought or oversold conditions. The script defines oversold conditions when the RSI is at or below 30 and overbought conditions when the RSI is at or above 70.

Volume Condition:

-The strategy incorporates a volume condition where the current volume must be greater than 2.5 times the 20-period moving average of volume. This is used to confirm the strength of the price movement.

Simple Moving Averages (SMA):

- The strategy uses two SMAs: SMA1 with a length of 250 periods and SMA2 with a length of 500 periods. These SMAs help identify long-term trends and generate signals based on their crossover.

Strategy Logic:

Entry Logic:

A long position is initiated when all the following conditions are met:

The RSI indicates an oversold condition (RSI ≤ 30).

SMA1 is above SMA2, indicating an uptrend.

The volume condition is satisfied, confirming the strength of the signal.

Exit Logic:

The strategy closes the long position when SMA1 crosses under SMA2, signaling a potential end of the uptrend (a "Death Cross").

Stop-Loss:

A stop-loss is set at 5% below the entry price to manage risk and limit potential losses.

Buy and sell signals are highlighted with circles below or above bars:

Green Circle : Buy signal when RSI is oversold, SMA1 > SMA2, and the volume condition is met.

Red Circle : Sell signal when RSI is overbought, SMA1 < SMA2, and the volume condition is met.

Black Cross: "Death Cross" when SMA1 crosses under SMA2, indicating a potential bearish signal.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

I hope the strategy will be helpful, as always, best regards and safe trades

;)

Quatro SMA Strategy [4h]Hello, I would like to present to you The "Quatro SMA" strategy

Strategy is based on four simple moving averages of different lengths and monitoring trading volume. The key idea is to identify strong market trends by comparing short-term moving averages with the long-term SMA. The strategy generates buy signals when all short-term SMAs are above the SMA(200) and the volume confirms the strength of the move. Similarly, sell signals are generated when all short-term SMAs are below the SMA(200), and the volume is sufficiently high.

The strategy manages risk by applying a stop loss and three different Take Profit levels (TP1, TP2, TP3), with varying percentages of the position closed at each level.

Each Take Profit level is triggered at a specific percentage gain, with the position being closed gradually depending on the achieved targets. The percentage of the position closed at each TP level is also defined by the user.

Indicators and Parameters:

Simple Moving Averages (SMA):

The script utilizes four simple moving averages with different lengths (4, 16, 32, 200). The first three SMAs (SMA1, SMA2, SMA3) are used to determine the trend direction, while the fourth SMA (with a length of 200) serves as a support/resistance line.

Volume:

The script monitors trading volume and checks if the current volume exceeds 2.5 times the average volume of the last 40 candles. High volume is considered as confirmation of trend strength.

Entry Conditions:

- Long Position: Triggered when SMA1 > SMA2 > SMA3, the closing price is above SMA(200), and the volume condition is met.

- Short Position: Triggered when SMA1 < SMA2 < SMA3, the closing price is below SMA(200), and the volume condition is met.

Exit Conditions:

- Long Position: Closed when SMA1 < SMA2 < SMA3 and the closing price is above SMA(200).

- Short Position: Closed when SMA1 > SMA2 > SMA3 and the closing price is below SMA(200).

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

I hope the strategy will be helpful, as always, best regards and safe trades

;)

BTC outperform atrategy### Code Description

This Pine Script™ code implements a simple trading strategy based on the relative prices of Bitcoin (BTC) on a weekly and a three-month basis. The script plots the weekly and three-month closing prices of Bitcoin on the chart and generates trading signals based on the comparison of these prices. The code can also be applied to Ethereum (ETH) with similar effectiveness.

### Explanation

1. **Inputs and Variables**:

- The user selects the trading symbol (default is "BINANCE:BTCUSDT").

- `weeklyPrice` retrieves the closing price of the selected symbol on a weekly interval.

- `monthlyPrice` retrieves the closing price of the selected symbol on a three-month interval.

2. **Plotting Data**:

- The weekly price is plotted in blue.

- The three-month price is plotted in red.

3. **Trading Conditions**:

- A long position is suggested if the weekly price is greater than the three-month price.

- A short position is suggested if the three-month price is greater than the weekly price.

4. **Strategy Execution**:

- If the long condition is met, the strategy enters a long position.

- If the short condition is met, the strategy enters a short position.

This script works equally well for Ethereum (ETH) by changing the symbol input to "BINANCE:ETHUSDT" or any other desired Ethereum trading pair.

Bitcoin Futures vs. Spot Tri-Frame - Strategy [presentTrading]Prove idea with a backtest is always true for trading.

I developed and open-sourced it as an educational material for crypto traders to understand that the futures and spot spread may be effective but not be as effective as they might think. It serves as an indicator of sentiment rather than a reliable predictor of market trends over certain periods. It is better suited for specific trading environments, which require further research.

█ Introduction and How it is Different

The "Bitcoin Futures vs. Spot Tri-Frame Strategy" utilizes three different timeframes to calculate the Z-Score of the spread between BTC futures and spot prices on Binance and OKX exchanges. The strategy executes long or short trades based on composite Z-Score conditions across the three timeframes.

The spread refers to the difference in price between BTC futures and BTC spot prices, calculated by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges.

BTCUSD 1D L/S Performance

█ Strategy, How It Works: Detailed Explanation

🔶 Calculation of the Spread

The spread is the difference in price between BTC futures and BTC spot prices. The strategy calculates the spread by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges. This spread serves as the primary metric for identifying trading opportunities.

Spread = Weighted Average Futures Price - Weighted Average Spot Price

🔶 Z-Score Calculation

The Z-Score measures how many standard deviations the current spread is from its historical mean. This is calculated for each timeframe as follows:

Spread Mean_tf = SMA(Spread_tf, longTermSMA)

Spread StdDev_tf = STDEV(Spread_tf, longTermSMA)

Z-Score_tf = (Spread_tf - Spread Mean_tf) / Spread StdDev_tf

Local performance

🔶 Composite Entry Conditions

The strategy triggers long and short entries based on composite Z-Score conditions across all three timeframes:

- Long Condition: All three Z-Scores must be greater than the long entry threshold.

Long Condition = (Z-Score_tf1 > zScoreLongEntryThreshold) and (Z-Score_tf2 > zScoreLongEntryThreshold) and (Z-Score_tf3 > zScoreLongEntryThreshold)

- Short Condition: All three Z-Scores must be less than the short entry threshold.

Short Condition = (Z-Score_tf1 < zScoreShortEntryThreshold) and (Z-Score_tf2 < zScoreShortEntryThreshold) and (Z-Score_tf3 < zScoreShortEntryThreshold)

█ Trade Direction

The strategy allows the user to specify the trading direction:

- Long: Only long trades are executed.

- Short: Only short trades are executed.

- Both: Both long and short trades are executed based on the Z-Score conditions.

█ Usage

The strategy can be applied to BTC or Crypto trading on major exchanges like Binance and OKX. By leveraging discrepancies between futures and spot prices, traders can exploit market inefficiencies. This strategy is suitable for traders who prefer a statistical approach and want to diversify their timeframes to validate signals.

█ Default Settings

- Input TF 1 (60 minutes): Sets the first timeframe for Z-Score calculation.

- Input TF 2 (120 minutes): Sets the second timeframe for Z-Score calculation.

- Input TF 3 (180 minutes): Sets the third timeframe for Z-Score calculation.

- Long Entry Z-Score Threshold (3): Defines the threshold above which a long trade is triggered.

- Short Entry Z-Score Threshold (-3): Defines the threshold below which a short trade is triggered.

- Long-Term SMA Period (100): The period used to calculate the simple moving average for the spread.

- Use Hold Days (true): Enables holding trades for a specified number of days.

- Hold Days (5): Number of days to hold the trade before exiting.

- TPSL Condition (None): Defines the conditions for taking profit and stop loss.

- Take Profit (%) (30.0): The percentage at which the trade will take profit.

- Stop Loss (%) (20.0): The percentage at which the trade will stop loss.

By fine-tuning these settings, traders can optimize the strategy to suit their risk tolerance and trading style, enhancing overall performance.

Trend Deviation strategy - BTC [IkkeOmar]Intro:

This is an example if anyone needs a push to get started with making strategies in pine script. This is an example on BTC, obviously it isn't a good strategy, and I wouldn't share my own good strategies because of alpha decay.

This strategy integrates several technical indicators to determine market trends and potential trade setups. These indicators include:

Directional Movement Index (DMI)

Bollinger Bands (BB)

Schaff Trend Cycle (STC)

Moving Average Convergence Divergence (MACD)

Momentum Indicator

Aroon Indicator

Supertrend Indicator

Relative Strength Index (RSI)

Exponential Moving Average (EMA)

Volume Weighted Average Price (VWAP)

It's crucial for you guys to understand the strengths and weaknesses of each indicator and identify synergies between them to improve the strategy's effectiveness.

Indicator Settings:

DMI (Directional Movement Index):

Length: This parameter determines the number of bars used in calculating the DMI. A higher length may provide smoother results but might lag behind the actual price action.

Bollinger Bands:

Length: This parameter specifies the number of bars used to calculate the moving average for the Bollinger Bands. A longer length results in a smoother average but might lag behind the price action.

Multiplier: The multiplier determines the width of the Bollinger Bands. It scales the standard deviation of the price data. A higher multiplier leads to wider bands, indicating increased volatility, while a lower multiplier results in narrower bands, suggesting decreased volatility.

Schaff Trend Cycle (STC):

Length: This parameter defines the length of the STC calculation. A longer length may result in smoother but slower-moving signals.

Fast Length: Specifies the length of the fast moving average component in the STC calculation.

Slow Length: Specifies the length of the slow moving average component in the STC calculation.

MACD (Moving Average Convergence Divergence):

Fast Length: Determines the number of bars used to calculate the fast EMA (Exponential Moving Average) in the MACD.

Slow Length: Specifies the number of bars used to calculate the slow EMA in the MACD.

Signal Length: Defines the number of bars used to calculate the signal line, which is typically an EMA of the MACD line.

Momentum Indicator:

Length: This parameter sets the number of bars over which momentum is calculated. A longer length may provide smoother momentum readings but might lag behind significant price changes.

Aroon Indicator:

Length: Specifies the number of bars over which the Aroon indicator calculates its values. A longer length may result in smoother Aroon readings but might lag behind significant market movements.

Supertrend Indicator:

Trendline Length: Determines the length of the period used in the Supertrend calculation. A longer length results in a smoother trendline but might lag behind recent price changes.

Trendline Factor: Specifies the multiplier used in calculating the trendline. It affects the sensitivity of the indicator to price changes.

RSI (Relative Strength Index):

Length: This parameter sets the number of bars over which RSI calculates its values. A longer length may result in smoother RSI readings but might lag behind significant price changes.

EMA (Exponential Moving Average):

Fast EMA: Specifies the number of bars used to calculate the fast EMA. A shorter period results in a more responsive EMA to recent price changes.

Slow EMA: Determines the number of bars used to calculate the slow EMA. A longer period results in a smoother EMA but might lag behind recent price changes.

VWAP (Volume Weighted Average Price):

Default settings are typically used for VWAP calculations, which consider the volume traded at each price level over a specific period. This indicator provides insights into the average price weighted by trading volume.

backtest range and rules:

You can specify the start date for backtesting purposes.

You can can select the desired trade direction: Long, Short, or Both.

Entry and Exit Conditions:

LONG:

DMI Cross Up: The Directional Movement Index (DMI) indicates a bullish trend when the positive directional movement (+DI) crosses above the negative directional movement (-DI).

Bollinger Bands (BB): The price is below the upper Bollinger Band, indicating a potential reversal from the upper band.

Momentum Indicator: Momentum is positive, suggesting increasing buying pressure.

MACD (Moving Average Convergence Divergence): The MACD line is above the signal line, indicating bullish momentum.

Supertrend Indicator: The Supertrend indicator signals an uptrend.

Schaff Trend Cycle (STC): The STC indicates a bullish trend.

Aroon Indicator: The Aroon indicator signals a bullish trend or crossover.

When all these conditions are met simultaneously, the strategy considers it a favorable opportunity to enter a long trade.

SHORT:

DMI Cross Down: The Directional Movement Index (DMI) indicates a bearish trend when the negative directional movement (-DI) crosses above the positive directional movement (+DI).

Bollinger Bands (BB): The price is above the lower Bollinger Band, suggesting a potential reversal from the lower band.

Momentum Indicator: Momentum is negative, indicating increasing selling pressure.

MACD (Moving Average Convergence Divergence): The MACD line is below the signal line, signaling bearish momentum.

Supertrend Indicator: The Supertrend indicator signals a downtrend.

Schaff Trend Cycle (STC): The STC indicates a bearish trend.

Aroon Indicator: The Aroon indicator signals a bearish trend or crossover.

When all these conditions align, the strategy considers it an opportune moment to enter a short trade.

Disclaimer:

THIS ISN'T AN OPTIMAL STRATEGY AT ALL! It was just an old project from when I started learning pine script!

The backtest doesn't promise the same results in the future, always do both in-sample and out-of-sample testing when backtesting a strategy. And make sure you forward test it as well before implementing it!

Furthermore this strategy uses both trend and mean-reversion systems, that is usually a no-go if you want to build robust trend systems .

Don't hesitate to comment if you have any questions or if you have some good notes for a beginner.

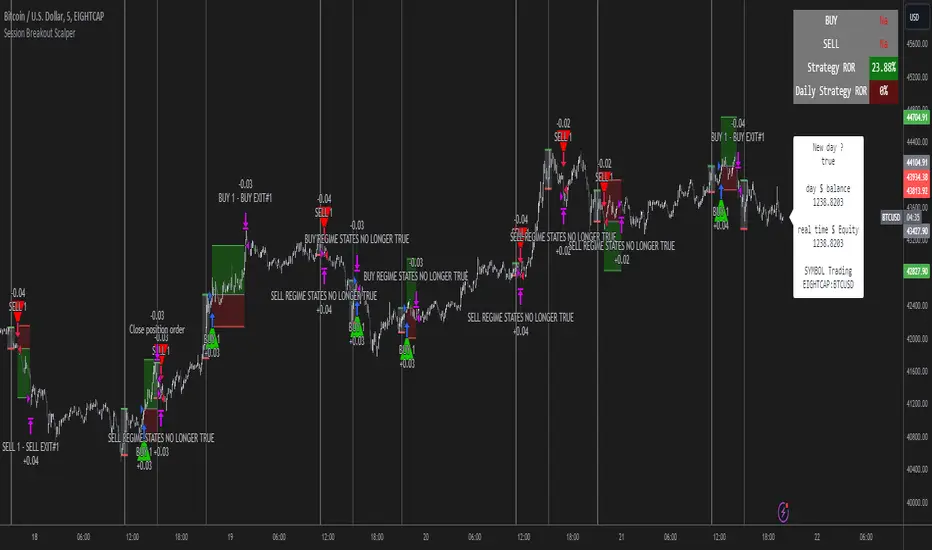

Session Breakout Scalper Trading BotHi Traders !

Introduction:

I have recently been exploring the world of automated algorithmic trading (as I prefer more objective trading strategies over subjective technical analysis (TA)) and would like to share one of my automation compatible (PineConnecter compatible) scripts “Session Breakout Scalper”.

The strategy is really simple and is based on time conditional breakouts although has more ”relatively” advanced optional features such as the regime indicators (Regime Filters) that attempt to filter out noise by adding more confluence states and the ATR multiple SL that takes into account volatility to mitigate the down side risk of the trade.

What is Algorthmic Trading:

Firstly what is algorithmic trading? Algorithmic trading also known as algo-trading, is a method of using computer programs (in this case pine script) to execute trades based on predetermined rules and instructions (this trading strategy). It's like having a robot trader who follows a strict set of commands to buy and sell assets automatically, without any human intervention.

Important Note:

For Algorithmic trading the strategy will require you having an essential TV subscription at the minimum (so that you can set alerts) plus a PineConnecter subscription (scroll down to the .”How does the strategy send signals” headings to read more)

The Strategy Explained:

Is the Time input true ? (this can be changed by toggling times under the “TRADE MEDIAN TIMES” group for user inputs).

Given the above is true the strategy waits x bars after the session and then calculates the highest high (HH) to lowest low (LL) range. For this box to form, the user defined amount of bars must print after the session. The box is symmetrical meaning the HH and LL are calculated over a lookback that is equal to the sum of user defined bars before and after the session (+ 1).

The Strategy then simultaneously defines the HH as the buy level (green line) and the LL as the sell level (red line). note the strategy will set stop orders at these levels respectively.

Enter a buy if price action crosses above the HH, and then cancel the sell order type (The opposite is true for a stop order).

If the momentum based regime filters are true the strategy will check for the regime / regimes to be true, if the regime if false the strategy will exit the current trade, as the regime filter has predicted a slowing / reversal of momentum.

The image below shows the strategy executing these trading rules ( Regime filters, "Trades on chart", "Signal & Label" and "Quantity" have been omitted. "Strategy label plots" has been switched to true)

Other Strategy Rules:

If a new session (time session which is user defined) is true (blue vertical line) and the strategy is currently still in a trade it will exit that trade immediately.

It is possible to also set a range of percentage gain per day that the strategy will try to acquire, if at any point the strategy’s profit is within the percentage range then the position / trade will be exited immediately (This can be changed in the “PERCENT DAY GAIN” group for user inputs)

Stops and Targets:

The strategy has either static (fixed) or variable SL options. TP however is only static. The “STRAT TP & TP” group of user inputs is responsible for the SL and TP values (quoted in pips). Note once the ATR stop is set to true the SL values in the above group no longer have any affect on the SL as expected.

What are the Regime Filters:

The Larry Williams Large Trade Index (LWLTI): The Larry Williams Large Trade Index (LWTI) is a momentum-based technical indicator developed by iconic trader Larry Williams. It identifies potential entries and exits for trades by gauging market sentiment, particularly the buying and selling pressure from large market players. Here's a breakdown of the LWTI:

LWLTI components and their interpretation:

Oscillator: It oscillates between 0 and 100, with 50 acting as the neutral line.

Sentiment Meter: Values above 75 suggest a bearish market dominated by large selling, while readings below 25 indicate a bullish market with strong buying from large players.

Trend Confirmation: Crossing above 75 during an uptrend and below 25 during a downtrend confirms the trend's continuation.

The Andean Oscillator (AO) : The Andean Oscillator is a trend and momentum based indicator designed to measure the degree of variations within individual uptrends and downtrends in the prices.

Regime Filter States:

In trading, a regime filter is a tool used to identify the current state or "regime" of the market.

These Regime filters are integrated within the trading strategy to attempt to lower risk (equity volatility and/or draw down). The regime filters have different states for each market order type (buy and sell). When the regime filters are set to true, if these regime states fail to be true the trade is exited immediately.

For Buy Trades:

LWLTI positive momentum state: Quotient of the lagged trailing difference and the ATR > 50

AO positive momentum state: Bull line > Bear line (signal line is omitted)

For Sell Trades:

LWLTI negative momentum stat: Quotient of the lagged trailing difference and the ATR < 50

AO negative momentum state: Bull line < Bear line (signal line is omitted)

How does the Strategy Send Signals:

The strategy triggers a TV alert (you will neet to set a alert first), TV then sends a HTTP request to the automation software (PineConnecter) which receives the request and then communicates to an MT4/5 EA to automate the trading strategy.

For the strategy to send signals you must have the following

At least a TV essential subscription

This Script added to your chart

A PineConnecter account, which is paid and not free. This will provide you with the expert advisor that executes trades based on these strategies signals.

For more detailed information on the automation process I would recommend you read the PineConnecter documentation and FAQ page.

Dashboard:

This Dashboard (top right by defualt) lists some simple trading statistics and also shows when a trade is live.

Important Notice:

- USE THIS STRATEGY AT YOUR OWN RISK AND ALWAYS DO YOUR OWN RESEARCH & MANUAL BACKTESTING !

- THE STRATEGY WILL NOT EXHIBIT THE BACKTEST PERFORMANCE SEEN BELOW IN ALL MARKETS !

3kilos BTC 15mThe "3kilos BTC 15m" is a comprehensive trading strategy designed to work on a 15-minute timeframe for Bitcoin (BTC) or other cryptocurrencies. This strategy combines multiple indicators, including Triple Exponential Moving Averages (TEMA), Average True Range (ATR), and Heikin-Ashi candlesticks, to generate buy and sell signals. It also incorporates risk management features like take profit and stop loss.

Indicators

Triple Exponential Moving Averages (TEMA): Three TEMA lines are used with different lengths and sources:

Short TEMA (Red) based on highs

Long TEMA 1 (Blue) based on lows

Long TEMA 2 (Green) based on closing prices

Average True Range (ATR): Custom ATR calculation with EMA smoothing is used for volatility measurement.

Supertrend: Calculated using ATR and a multiplier to determine the trend direction.

Simple Moving Average (SMA): Applied to the short TEMA to smooth out its values.

Heikin-Ashi Close: Used for additional trend confirmation.

Entry & Exit Conditions

Long Entry: Triggered when the short TEMA is above both long TEMA lines, the Supertrend is bullish, the short TEMA is above its SMA, and the Heikin-Ashi close is higher than the previous close.

Short Entry: Triggered when the short TEMA is below both long TEMA lines, the Supertrend is bearish, the short TEMA is below its SMA, and the Heikin-Ashi close is lower than the previous close.

Take Profit and Stop Loss: Both are calculated as a percentage of the entry price, and they are set for both long and short positions.

Risk Management

Take Profit: Set at 1% above the entry price for long positions and 1% below for short positions.

Stop Loss: Set at 3% below the entry price for long positions and 3% above for short positions.

Commission and Pyramiding

Commission: A 0.07% commission is accounted for in the strategy.

Pyramiding: The strategy does not allow pyramiding.

Note

This strategy is designed for educational purposes and should not be considered as financial advice. Always do your own research and consider consulting a financial advisor before engaging in trading.

The Z-score The Z-score, also known as the standard score, is a statistical measurement that describes a value's relationship to the mean of a group of values. It's measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean.

The concept of Z-score was introduced by statistician Carl Friedrich Gauss as part of his "method of the least squares," which was an important step in the development of the normal distribution and Z-score tables. It's a key concept in statistics and is used in various statistical tests.

In financial analysis, Z-scores are used to determine whether a data point is usual or unusual. You can think of it as a measure of how many standard deviations an element is from the mean. For instance, a Z-score of 1.0 would denote a value that is one standard deviation from the mean. Z-scores are also used to predict probabilities, with Z-scores having a distribution that is expected to be normal.

In trading, a Z-score is used to determine how often a trading system may produce a string of winners or losers. It can help a trader to understand whether the losses or profits they see are something that the system would most likely produce, or if it's a once in a blue moon situation. This helps traders make decisions about when to start or stop a system.

I just wanted to play a bit with the Z-score I guess.

Feel free to share your findings if you discover additional applications for this strategy or identify timeframes where it appears to perform more optimally.

How it works:

This strategy is based on a statistical concept called Z-score, which measures the number of standard deviations a data point is from the mean. In other words, it helps determine how unusual or usual a data point is.

In the context of this strategy, Z-score is applied to a 10-period EMA (Exponential Moving Average) of Heikin-Ashi candlestick close prices. The Z-score is calculated over a look-back period of 25 bars.

The EMA of the Z-score is then calculated over a 20-bar period, and the upper and lower thresholds (bounds for buy and sell signals) are defined using the 90th and 10th percentiles of this EMA score.

Long positions are taken when the Z-score crosses above the lower threshold or crosses above the mid-line (50th percentile). An additional long entry is made when the Z-score crosses above the highest value the EMA has been in the past 100 periods.

Short positions are initiated when the EMA crosses below the upper threshold, lower threshold or the highest value the EMA has been in the past 100 periods.

Positions are closed when opposing entry conditions are met, for example, a long position is closed when the short entry condition is true, and vice versa.

Set your desired start date for the strategy. This can be modified in the timestamp("YYYY MM DD") function at the top of the script.

Kimchi Premium StrategyThis strategy is based on the Korea Premium, also known as the “Kimchi Premium,” which indicates how expensive or cheap the price of Bitcoin in Korean Won on a Bitcoin exchange in South Korea is relative to the price of Bitcoin being traded in USD or Tether. Inverse Kimchi Premium RSI was newly defined to create a strategy with Kimchi Premium. Assuming that the larger the kimchi premium, the greater the individual's purchasing power. In this case, if the Inverse Kimchi Premium RSI falls and closes the candle below the bear level, a short is triggered. Long is the opposite.

This strategy defaults to a combination of the traditional RSI and the Inverse Kimchi Premium RSI. If the user wishes to unlock the Inverse Kimchi Premium RSI combination and only use it as a traditional RSI strategy, the following settings can be used.

Use Combination of Inverse Kimchi Premium RSI: Uncheck

Resolution: Chart (4hr Candle)

Source: Close

Length of RSI: 14

Bull Level: 74

Bear Level: 25

__________________________________________________________________________________

김치프리미엄(김프) 전략은 달러 혹은 테더로 거래되고 있는 비트코인 가격 대비 한국에 있는 비트코인 거래소의 비트코인 원화 가격이 얼마나 비싸고 싼 지를 나타내는 코리아 프리미엄, 일명 "김치 프리미엄" 지표를 기반으로 만들어졌습니다. 김치 프리미엄을 가지고 전략을 만들기위해 Inverse Kimchi Premium RSI를 새롭게 정의하였습니다. 김치 프리미엄이 커질수록 개인의 매수세가 커진다고 가정하고, 이 경우 Inverse Kimchi Premium RSI이 하락하여 Bear Level 아래에서 캔들 마감을 하면 Short을 트리거 합니다. Long은 그 반대입니다.

이 전략은 전통적인 RSI와 Inverse Kimchi Premium RSI을 조합하여 기본값을 설정하였습니다. 유저가 원한다면 Inverse Kimchi Premium RSI의 조합을 해제하고 전통적인 RSI 전략으로만 사용하려면 아래 다음의 설정값을 사용할 수 있습니다.

Use Combination of Inverse Kimchi Premium RSI: 체크 해제

Resolution: Chart (4hr Candle)

Source: Close

Length of RSI: 14

Bull Level: 74

Bear Level: 25

ATR Mean Reversion Strategy V1**Long Only Strategy**

When Price drops below the ATR band below it will enter a buy on the next candle open

SL at current price minus ATR* ATR multiplier

TP at Mean EMA or if higher than Mean EMA and current candle low is below previous candle low or if price is above ATR

NB: I would highly recommend a low fee broker (I use ICmarkets raw spread account) due to the fact that this is a decently high frequency trading strategy you will rack up a lot of commission, if you use and exchange like Bybit or Binance the strategy will not be profitable due to the high commissions.

Trend Following based on Trend ConfidenceThis is a Trend Following strategy based on the Trend Confidence indicator.

The goal of this strategy is to be a simple Trend Following strategy, but also to be as precise as possible when it comes to the question 'how confident are we that a linear trend is ongoing?'. For this we calculate the 'confidence' of a linear trend in the past number of closing prices. The idea of this strategy is that past a certain confidence, the ongoing linear trend is more likely to continue than not.

Trend Confidence:

The Trend Confidence shows us how strong of a linear trend the price has made in the past number (given by Length parameter) of closing prices. The steepness of the price change makes the Trend Confidence more extreme (more positive for an uptrend or more negative for a downtrend), and the deviation from a straight line makes the Trend Confidence less extreme (brings the confidence closer to 0). This way we can filter out signals by wild/sudden price moves that don't follow a clear linear trend.

Math behind the Trend Confidence:

A linear fit is made on the past number of closing prices, using Ordinary Linear Regression. We have the steepness of the linear fit: b in y=a+bx . And we have the standard deviation of the distances from the closing prices to the linear fit: sd . The Trend Confidence is the ratio b/sd .

Entries and Exits:

For entry and exit points we look at how extreme the Trend Confidence is. The strategy is based on the assumption that past a certain confidence level, the ongoing linear trend is more likely to continue than not.

So when the Trend Confidence passes above the 'Long entry" threshold, we go Long. After that when the Trend Confidence passes under the 'Long exit' threshold, we exit. The Long entry should be a positive value so that we go Long once a linear uptrend with enough confidence has been detected.

When the Trend Confidence passes below the 'Short entry' threshold, we go Short. After that when the Trend Confidence passes above the 'Short exit' threshold, we exit. The Short entry should be a negative value so that we go Short once a linear downtrend with enough confidence has been detected.

Default Parameters:

The strategy is intended for BTC-USD market, 4 hour timeframe. The strategy also works on ETH-USD with similar parameters.

The Length is arbitrarily set at 30, this means we look at the past 30 closing prices to determine a linear trend. Note that changing the length will change the range of Trend Confidence values encountered.

The default entry and exit thresholds for Longs and Shorts do not mirror each other. This is because the BTC-USD market goes up more heavily and more often than it goes down. So the ideal parameters for Longs and Shorts are not the same.

The positive results of the strategy remain when the parameters are slightly changed (robustness check).

The strategy uses 100% equity per trade, but has a 10% stop loss so that a maximum of 10% is risked per trade.

Commission is set at 0.1% as is the highest commission for most crypto exchanges.

Slippage is set at 5 ticks, source for this is theblock.co.

BTC Hashrate ribbonsBTC Hash Rate ribbons / Hash Rate cross

This strategy goes long when BTCs Hash Rate 30 day moving average crosses above the 60 day moving average, signifying that miner capitulation is over and recovery has started.

When the opposite signal is given, which signifies the beginning of miner capitulation, the strategy goes short (or flat, depending on configuration). This is generally considered the most popular Hash Rate related strategy.

The strategy is based on this medium article: medium.com

Thanks to the recent integration of IntoTheBlock data into Tradingview, we can now effortlessly show Hash Rate data on our chart,

keep in mind however, that IntoTheBlock doesn't provide Hash Rate data on timeframes below daily, so this strategy is based used on the daily, weekly or even monthly time frames.

Hash Rate definition:

The Bitcoin hash rate is the number of times per second that computers on the Bitcoin network are hashing data to verify transactions and perform the encryption that secures the network. The hash rate is an indicator of how healthy the Bitcoin network is at any given time, and is driven primarily by difficulty mining and the number of miners. Generally, a high hash rate is considered a good thing.

More precisely, the Bitcoin hash rate is the number of times per second that computers on the Bitcoin network are hashing data to verify transactions and perform the encryption that secures the network.

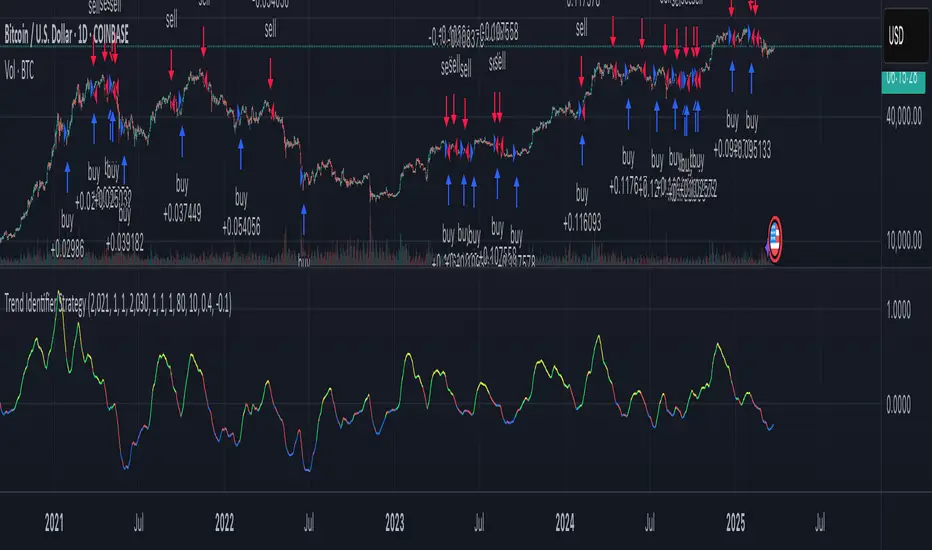

Trend Identifier StrategyTrend Identifier Strategy for 1D BTC.USD

The indicator smoothens a closely following moving average into a polynomial like plot and assumes 4 staged cycles based on the first and the second derivatives. This is an optimized strategy for long term buying and selling with a Sortino Ratio above 3. It is designed to be a more profitable alternative to HODLing. It can be combined with 'Accumulation/Distribution Bands & Signals' and 'Exponential Top and Bottom Finder'.

Fast v Slow Moving Averages Strategy (Variable) [divonn1994]This is a simple moving average based strategy that takes 2 moving averages, a Fast and a Slow one, plots them both, and then decides to enter a 'long' position or exit it based on whether the two lines have crossed each other. It goes 'long when the Fast Moving Average crosses above the Slow Moving Average. This could indicate upwards momentum in prices in the future. It then exits the position when the the Fast Moving Average crosses back below. This could indicate downwards momentum in prices in the future. This is only speculative, though, but sometimes it can be a very good indicator/strategy to predict future action.

I've tried some strategy settings and I found different promising strategies. Here are a few:

BTCUSD ( BitStamp ) 1 Day Timeframe : EMA, Fast length 25 bars, Slow length 62 bars => 28,792x net profit (default)

BTCUSD ( BitStamp ) 1 Day Timeframe : VWMA, Fast length 21 bars, Slow length 60 bars => 15,603x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : SMA, Fast length 18 bars, Slow length 51 bars => 19,507x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : RMA, Fast length 20 bars, Slow length 52 bars => 5,729x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : WMA, Fast length 29 bars, Slow length 60 bars => 19,869x net profit

Features:

-You can choose your preferred moving average: SMA , EMA , WMA , RMA & VWMA .

-You can change the length average for each moving average

-I made the background color Green when you're currently in a long position and Red when not. I made it so you can see when you'd be actively in a trade or not. The Red and Green background colors can be toggled on/off in order to see other indicators more clearly overlayed in the chart, or if you prefer a cleaner look on your charts.

-I also have a plot of the Fast moving average and Slow moving average together. The Opening moving average is Purple, the Closing moving average is White. White on top is a sign of a potential upswing and purple on top is a sign of a potential downswing. I've made this also able to be toggled on/off.

Let me know if you think I should change anything with my script, I'm always open to constructive criticism so feel free to comment below :)

Trade HourThis script is just finds the best hour to buy and sell hour in a day by checking chart movements in past

For example if the red line is on the 0.63 on BTC/USDT chart it mean the start of 12AM hour on a day is the best hour to buy (all based on

It's just for 1 hour time-frame but you can test it on other charts.

IMPORTANT: You can change time Zone in strategy settings.to get the real hours as your location timezone

IMPORTANT: Its for now just for BTC/USDT but you can optimize and test for other charts...

IMPORTANT: A green and red background color calculated for show the user the best places of buy and sell (green : positive signal, red: negative signals)

settings :

timezone : We choice a time frame for our indicator as our geo location

source : A source to calculate rate of change for it

Time Period : Time period of ROC indicator

About Calculations:

1- We first get a plot that just showing the present hour as a zigzag plot

2- So we use an indicator ( Rate of change ) to calculate chart movements as positive and negative numbers. I tested ROC is the best indicator but you can test close-open or real indicator or etc as indicator.

3 - for observe effects of all previous data we should indicator_cum that just a full sum of indicator values.

4- now we need to split this effects to hours and find out which hour is the best place to buy and which is the best for sell. Ok we should just calculate multiple of hour*indicator and get complete sum of it so:

5- we will divide this number to indicator_cum : (indicator_mul_hour_cum) / indicator_cum

6- Now we have the best hour to buy! and for best sell we should just reverse the ROC indicator and recalculate the best hour for it!

7- A green and red background color calculated for show the user the best places of buy and sell that dynamically changing with observing green and red plots(green : positive signal, red: negative signals) when green plot on 15 so each day on hour 15 the background of strategy indicator will change to 15 and if its go upper after some days and reached to 16 the background green color will move to 16 dynamically.

Rate Of Change Trend Strategy (ROC)This is very simple trend following or momentum strategy. If the price change over the past number of bars is positive, we buy. If the price change over the past number of bars is negative, we sell. This is surprisingly robust, simple, and effective especially on trendy markets such as cryptos.

Works for many markets such as:

INDEX:BTCUSD

INDEX:ETHUSD

SP:SPX

NASDAQ:NDX

NASDAQ:TSLA

Fukuiz Octa-EMA + Ichimoku (Strategy)This strategy is based EMA of 8 different period and Ichimoku Cloud which works better in 1hr 4hr and daily time frame.

#A brief introduction to Ichimoku #

The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

#A brief introduction to EMA#

An exponential moving average ( EMA ) is a type of moving average (MA) that places a greater weight and significance on the most recent data points. The exponential moving average is also referred to as the exponentially weighted moving average . An exponentially weighted moving average reacts more significantly to recent price changes than a simple moving average ( SMA ), which applies an equal weight to all observations in the period.

#How to use#

The strategy will give entry points itself, you can monitor and take profit manually(recommended), or you can use the exit setup.

EMA (Color) = Bullish trend

EMA (Gray) = Bearish trend

#Condition#

Buy = All Ema (color) above the cloud.

SELL= All Ema turn to gray color.

Saturday Strategy BTC By KziI take the hypothèse that saturday is the most stable day of the week because, no SP500, no fed announcement and no weekly closure.

My Strategy is very simple:

Take the friday color (Red = Short // Green = Long)

Then open at the friday close price

Take a small pourcentage (1 or 2 %) then close.

What ever close on midnight.

Work Well on the 1h chart.

The Yellow is the saturday.

Maybe we can add the monthly close information to avoid opening trade on saturday if we are at this event.

Enjoy and give me your comment.

Kzi

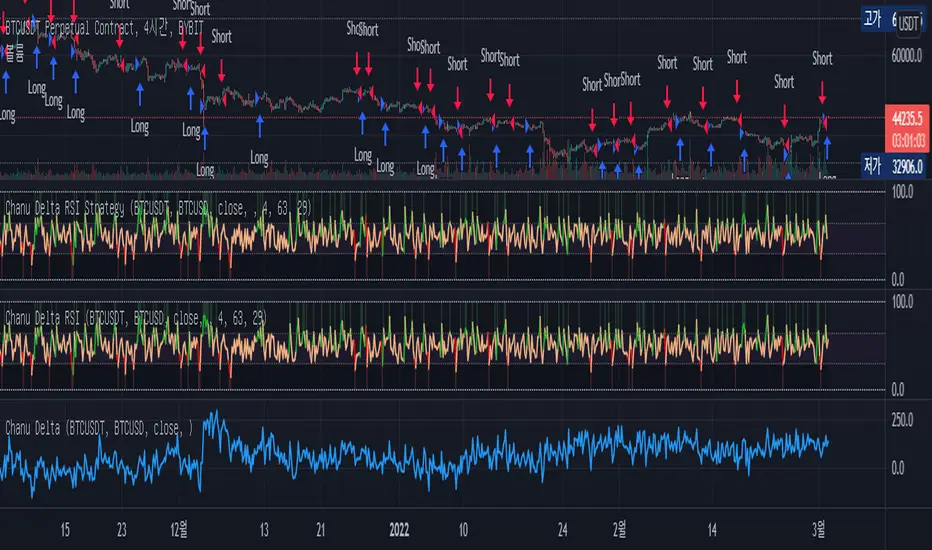

Chanu Delta RSI StrategyThis strategy is built on the Chanu Delta RSI , which indicates the strength of the Bitcoin market. The problem with the previous Chanu Delta Strategy was that it was simply based on the price difference between the two Bitcoin markets, so there was no universality. However, this new Chanu Delta RSI strategy solves the problem by introducing an RSI that compares the price difference trend.

When the Chanu Delta RSI hits “Bull Level” and “Bear Level” and closes the candle, long and short signals are triggered respectively. The example shown on the screen is a default setting optimized for a 4-hour candlestick strategy based on the Bybit BTCUSDT futures market. You can use it by adjusting the setting value and modifying it to suit you.

This strategy is selectable from both reference and large amplitude BTCUSD markets in order to enable fine backtesting. I recommend using BYBIT:BTCUSDT for the reference market and COINBASE:BTCUSD for the large amplitude market.

(Note) Using the "Chanu Delta RSI" to know the current indicator value in real time, it is convenient to predict the signal of the strategy.

(Note) Because the Chanu Delta RSI represents the price difference based on the Bybit BTCUSDT futures market, backtesting is possible from March 2020.

_____________________________________________________________

이 전략은 비트코인 시장의 강점을 나타내는 Chanu Delta RSI를 기반으로 합니다. 기존 Chanu Delta 전략의 문제점은 단순히 두 비트코인 시장의 가격차를 기준으로 하여 보편성이 없었다는 점이다. 하지만 이번 새로운 Chanu Delta RSI 전략은 가격차이 추세를 비교하는 RSI를 도입해 문제를 해결했습니다.

Chanu Delta RSI가 "Bull Level"과 "Bear Level"에 도달하고 봉마감하면 롱, 숏 신호가 각각 트리거됩니다. 화면에 보이는 예시는 Bybit BTCUSDT 선물 시장을 기반으로 한 4시간 캔들스틱 전략에 최적화된 기본 설정입니다. 설정값을 조정하여 자신에게 맞게 수정하여 사용하시면 됩니다.

이 전략은 정밀한 백테스팅을 가능하게 하기 위해 참조 및 큰 진폭 BTCUSD 시장에서 모두 선택할 수 있습니다. 참조 시장에는 BYBIT:BTCUSDT를 사용하고 큰 진폭 시장에는 COINBASE:BTCUSD를 사용하는 것이 좋습니다.

(주) "Chanu Delta RSI"를 이용하여 현재 지표 값을 실시간으로 알 수 있어 전략의 시그널을 예측하는데 편리합니다.

(주) Chanu Delta RSI는 바이비트 BTCUSDT 선물시장을 기준으로 가격차이를 나타내므로 2020년 3월부터 백테스팅이 가능합니다.

BTC Cap Dominance RSI StrategyThis strategy is based on the BTC Cap Dominance RSI indicator, which is a combination of the RSI of Bitcoin Market Cap and the RSI of Bitcoin Dominance. The concept of this strategy is to get a good grasp of the bitcoin market flow by combining bitcoin dominance as well as bitcoin market cap.

BTC Cap Dominance (BCD) RSI is defined as:

BCD RSI = (BTC Cap RSI + BTC Dominance RSI) / 2

Case 1 (Bull market):

Both Cap RSI and Dominance RSI values are high

Case 2 (Neutral market):

Cap RSI is high but Dominance RSI is low

Cap RSI is low but Dominance RSI is high

Case 3 (Bear market):

Both Cap RSI and Dominance RSI values are low

When the BCD RSI value closes the candle above the Bull level, it triggers a long signal and when the value closes below the Bear level, it triggers a short signal.

(Note) Please note that TradingView's market cap symbols (CRYPTOCAP:TOTAL and CRYPTOCAP:TOTAL2) started in January 2020, so strategy backtesting is possible from this point on.

(Note) Since the real-time BCD RSI value does not come out with this strategy, it is recommended to use it together because the current value can be known and the long-short signal can be predicted in advance by using a separate BCD RSI Index together.

If "Use Combination of dominance RSI ?" is not checked in addition to the recommended default value of the strategy, the recommended values are Length (14), Bull level (74), Bear level (25).

_______________________________________________________________________

이 전략은 비트코인 시가총액의 RSI와 비트코인 도미넌스 RSI를 조합하여 만든 BTC Cap Dominance RSI 지표를 기반으로 만들어졌습니다. 이 전략의 컨셉은 비트코인 시가총액뿐만 아니라 비트코인 도미넌스를 조합함으로써 비트코인 시장 흐름을 잘 파악할 수 있도록 하는 것입니다.

BTC Cap Dominance (BCD) RSI는 다음과 같이 정의하였습니다.

BCD RSI = (BTC Cap RSI + BTC Dominance RSI) / 2

Case 1 (강세 장):

Cap RSI와 Dominance RSI 값 모두 높은 경우

Case 2 (횡보 장):

Cap RSI는 높지만 Dominance RSI는 낮은 경우

Cap RSI는 낮지만 Dominance RSI는 높은 경우

Case 3 (약세 장):

Cap RSI와 Dominance RSI 값 모두 낮은 경우

BCD RSI 값이 Bull level 위에서 캔들 마감할 경우 long 신호를 트리거하고 Bear level 아래에서 캔들 마감할 경우 short 신호를 트리거합니다.

(주의) 트레이딩뷰의 시가총액 심볼들 (CRYPTOCAP:TOTAL과 CRYPTOCAP:TOTAL2)이 2020년 1월부터 시작하였으므로 이 시점부터 전략 백테스팅이 가능한 점을 유의하십시오.

(주의) 이 전략은 실시간 BCD RSI 값이 나오지 않기 때문에 별도의 BCD RSI Index를 함께 사용하면 현재 값을 알 수 있어 롱숏 신호를 사전에 예측할 수 있으므로 함께 사용하기를 권장합니다.

전략의 추천 기본값 외에 "Use Combination of dominance RSI ?"를 체크하지 않는 경우 권장하는 값은 Length (14), Bull level (74), Bear level (25) 입니다.