Bollinger Bands Entry/Exit ThresholdsBollinger Bands Entry/Exit Thresholds

Author of enhancements: chuckaschultz

Inspired and adapted from the original 'Bollinger Bands Breakout Oscillator' by LuxAlgo

Overview

Pairs nicely with Contrarian 100 MA

The Bollinger Bands Entry/Exit Thresholds is a powerful momentum-based indicator designed to help traders identify potential entry and exit points in trending or breakout markets. By leveraging Bollinger Bands, this indicator quantifies price deviations from the bands to generate bullish and bearish momentum signals, displayed as an oscillator. It includes customizable entry and exit signals based on user-defined thresholds, with visual cues plotted either on the oscillator panel or directly on the price chart.

This indicator is ideal for traders looking to capture breakout opportunities or confirm trend strength, with flexible settings to adapt to various markets and trading styles.

How It Works

The Bollinger Bands Entry/Exit Thresholds calculates two key metrics:

Bullish Momentum (Bull): Measures the extent to which the price exceeds the upper Bollinger Band, expressed as a percentage (0–100).

Bearish Momentum (Bear): Measures the extent to which the price falls below the lower Bollinger Band, also expressed as a percentage (0–100).

The indicator generates:

Long Entry Signals: Triggered when the bearish momentum (bear) crosses below a user-defined Long Threshold (default: 40). This suggests weakening bearish pressure, potentially indicating a reversal or breakout to the upside.

Exit Signals: Triggered when the bullish momentum (bull) crosses below a user-defined Sell Threshold (default: 80), indicating a potential reduction in bullish momentum and a signal to exit long positions.

Signals are visualized as tiny colored dots:

Long Entry: Blue dots, plotted either at the bottom of the oscillator or below the price bar (depending on user settings).

Exit Signal: White dots, plotted either at the top of the oscillator or above the price bar.

Calculation Methodology

Bollinger Bands:

A user-defined Length (default: 14) is used to calculate an Exponential Moving Average (EMA) of the source price (default: close).

Standard deviation is computed over the same length, multiplied by a user-defined Multiplier (default: 1.0).

Upper Band = EMA + (Standard Deviation × Multiplier)

Lower Band = EMA - (Standard Deviation × Multiplier)

Bull and Bear Momentum:

For each bar in the lookback period (length), the indicator calculates:

Bullish Momentum: The sum of positive deviations of the price above the upper band, normalized by the total absolute deviation from the upper band, scaled to a 0–100 range.

Bearish Momentum: The sum of positive deviations of the price below the lower band, normalized by the total absolute deviation from the lower band, scaled to a 0–100 range.

Formula:

bull = (sum of max(price - upper, 0) / sum of abs(price - upper)) * 100

bear = (sum of max(lower - price, 0) / sum of abs(lower - price)) * 100

Signal Generation:

Long Entry: Triggered when bear crosses below the Long Threshold.

Exit: Triggered when bull crosses below the Sell Threshold.

Settings

Length: Lookback period for EMA and standard deviation (default: 14).

Multiplier: Multiplier for standard deviation to adjust Bollinger Band width (default: 1.0).

Source: Input price data (default: close).

Long Threshold: Bearish momentum level below which a long entry signal is generated (default: 40).

Sell Threshold: Bullish momentum level below which an exit signal is generated (default: 80).

Plot Signals on Main Chart: Option to display entry/exit signals on the price chart instead of the oscillator panel (default: false).

Style:

Bullish Color: Color for bullish momentum plot (default: #f23645).

Bearish Color: Color for bearish momentum plot (default: #089981).

Visual Features

Bull and Bear Plots: Displayed as colored lines with gradient fills for visual clarity.

Midline: Horizontal line at 50 for reference.

Threshold Lines: Dashed green line for Long Threshold and dashed red line for Sell Threshold.

Signal Dots:

Long Entry: Tiny blue dots (below price bar or at oscillator bottom).

Exit: Tiny white dots (above price bar or at oscillator top).

How to Use

Add to Chart: Apply the indicator to your TradingView chart.

Adjust Settings: Customize the Length, Multiplier, Long Threshold, and Sell Threshold to suit your trading strategy.

Interpret Signals:

Enter a long position when a blue dot appears, indicating bearish momentum dropping below the Long Threshold.

Exit the long position when a white dot appears, indicating bullish momentum dropping below the Sell Threshold.

Toggle Plot Location: Enable Plot Signals on Main Chart to display signals on the price chart for easier integration with price action analysis.

Combine with Other Tools: Use alongside other indicators (e.g., trendlines, support/resistance) to confirm signals.

Notes

This indicator is inspired by LuxAlgo’s Bollinger Bands Breakout Oscillator but has been enhanced with customizable entry/exit thresholds and signal plotting options.

Best used in conjunction with other technical analysis tools to filter false signals, especially in choppy or range-bound markets.

Adjust the Multiplier to make the Bollinger Bands wider or narrower, affecting the sensitivity of the momentum calculations.

Disclaimer

This indicator is provided for educational and informational purposes only.

Buythedip

Ticker Pulse Meter + Fear EKG StrategyDescription

The Ticker Pulse Meter + Fear EKG Strategy is a technical analysis tool designed to identify potential entry and exit points for long positions based on price action relative to historical ranges. It combines two proprietary indicators: the Ticker Pulse Meter (TPM), which measures price positioning within short- and long-term ranges, and the Fear EKG, a VIX-inspired oscillator that detects extreme market conditions. The strategy is non-repainting, ensuring signals are generated only on confirmed bars to avoid false positives. Visual enhancements, such as optional moving averages and Bollinger Bands, provide additional context but are not core to the strategy's logic. This script is suitable for traders seeking a systematic approach to capturing momentum and mean-reversion opportunities.

How It Works

The strategy evaluates price action using two key metrics:

Ticker Pulse Meter (TPM): Measures the current price's position within short- and long-term price ranges to identify momentum or overextension.

Fear EKG: Detects extreme selling pressure (akin to "irrational selling") by analyzing price behavior relative to historical lows, inspired by volatility-based oscillators.

Entry signals are generated when specific conditions align, indicating potential buying opportunities. Exits are triggered based on predefined thresholds or partial position closures to manage risk. The strategy supports customizable lookback periods, thresholds, and exit percentages, allowing flexibility across different markets and timeframes. Visual cues, such as entry/exit dots and a position table, enhance usability, while optional overlays like moving averages and Bollinger Bands provide additional chart context.

Calculation Overview

Price Range Calculations:

Short-Term Range: Uses the lowest low (min_price_short) and highest high (max_price_short) over a user-defined short lookback period (lookback_short, default 50 bars).

Long-Term Range: Uses the lowest low (min_price_long) and highest high (max_price_long) over a user-defined long lookback period (lookback_long, default 200 bars).

Percentage Metrics:

pct_above_short: Percentage of the current close above the short-term range.

pct_above_long: Percentage of the current close above the long-term range.

Combined metrics (pct_above_long_above_short, pct_below_long_below_short) normalize price action for signal generation.

Signal Generation:

Long Entry (TPM): Triggered when pct_above_long_above_short crosses above a user-defined threshold (entryThresholdhigh, default 20) and pct_below_long_below_short is below a low threshold (entryThresholdlow, default 40).

Long Entry (Fear EKG): Triggered when pct_below_long_below_short crosses under an extreme threshold (orangeEntryThreshold, default 95), indicating potential oversold conditions.

Long Exit: Triggered when pct_above_long_above_short crosses under a profit-taking level (profitTake, default 95). Partial exits are supported via a user-defined percentage (exitAmt, default 50%).

Non-Repainting Logic: Signals are calculated using data from the previous bar ( ) and only plotted on confirmed bars (barstate.isconfirmed), ensuring reliability.

Visual Enhancements:

Optional moving averages (SMA, EMA, WMA, VWMA, or SMMA) and Bollinger Bands can be enabled for trend context.

A position table displays real-time metrics, including open positions, Fear EKG, and Ticker Pulse values.

Background highlights mark periods of high selling pressure.

Entry Rules

Long Entry:

TPM Signal: Occurs when the price shows strength relative to both short- and long-term ranges, as defined by pct_above_long_above_short crossing above entryThresholdhigh and pct_below_long_below_short below entryThresholdlow.

Fear EKG Signal: Triggered by extreme selling pressure, when pct_below_long_below_short crosses under orangeEntryThreshold. This signal is optional and can be toggled via enable_yellow_signals.

Entries are executed only on confirmed bars to prevent repainting.

Exit Rules

Long Exit: Triggered when pct_above_long_above_short crosses under profitTake.

Partial exits are supported, with the strategy closing a user-defined percentage of the position (exitAmt) up to four times per position (exit_count limit).

Exits can be disabled or adjusted via enable_short_signal and exitPercentage settings.

Inputs

Backtest Start Date: Defines the start of the backtesting period (default: Jan 1, 2017).

Lookback Periods: Short (lookback_short, default 50) and long (lookback_long, default 200) periods for range calculations.

Resolution: Timeframe for price data (default: Daily).

Entry/Exit Thresholds:

entryThresholdhigh (default 20): Threshold for TPM entry.

entryThresholdlow (default 40): Secondary condition for TPM entry.

orangeEntryThreshold (default 95): Threshold for Fear EKG entry.

profitTake (default 95): Exit threshold.

exitAmt (default 50%): Percentage of position to exit.

Visual Options: Toggle for moving averages and Bollinger Bands, with customizable types and lengths.

Notes

The strategy is designed to work across various timeframes and assets, with data sourced from user-selected resolutions (i_res).

Alerts are included for long entry and exit signals, facilitating integration with TradingView's alert system.

The script avoids repainting by using confirmed bar data and shifted calculations ( ).

Visual elements (e.g., SMA, Bollinger Bands) are inspired by standard Pine Script practices and are optional, not integral to the core logic.

Usage

Apply the script to a chart, adjust input settings to suit your trading style, and use the visual cues (entry/exit dots, position table) to monitor signals. Enable alerts for real-time notifications.

Designed to work best on Daily timeframe.

Ticker Pulse Meter BasicPairs nicely with the Contrarian 100 MA located here:

and the Enhanced Stock Ticker with 50MA vs 200MA located here:

Description

The Ticker Pulse Meter Basic is a dynamic Pine Script v6 indicator designed to provide traders with a visual representation of a stock’s price position relative to its short-term and long-term ranges, enabling clear entry and exit signals for long-only trading strategies. By calculating three normalized metrics—Percent Above Long & Above Short, Percent Above Long & Below Short, and Percent Below Long & Below Short—this indicator offers a unique "pulse" of market sentiment, plotted as stacked area charts in a separate pane. With customizable lookback periods, thresholds, and signal plotting options, it empowers traders to identify optimal entry points and profit-taking levels. The indicator leverages Pine Script’s force_overlay feature to plot signals on either the main price chart or the indicator pane, making it versatile for various trading styles.

Key Features

Pulse Meter Metrics:

Computes three percentages based on short-term (default: 50 bars) and long-term (default: 200 bars) lookback periods:

Percent Above Long & Above Short: Measures price strength when above both short and long ranges (green area).

Percent Above Long & Below Short: Indicates mixed momentum (orange area).

Percent Below Long & Below Short: Signals weakness when below both ranges (red area).

Flexible Signal Plotting:

Toggle between plotting entry (blue dots) and exit (white dots) signals on the main price chart (location.abovebar/belowbar) or in the indicator pane (location.top/bottom) using the Plot Signals on Main Chart option.

Entry/Exit Logic:

Long Entry: Triggered when Percent Above Long & Above Short crosses above the high threshold (default: 20%) and Percent Below Long & Below Short is below the low threshold (default: 40%).

Long Exit: Triggered when Percent Above Long & Above Short crosses above the profit-taking level (default: 95%).

Visual Enhancements:

Plots stacked area charts with semi-transparent colors (green, orange, red) for intuitive trend analysis.

Displays threshold lines for entry (high/low) and profit-taking levels.

Includes a ticker and timeframe table in the top-right corner for quick reference.

Alert Conditions: Supports alerts for long entry and exit signals, integrable with TradingView’s alert system for automated trading.

Technical Innovation: Combines normalized price metrics with Pine Script v6’s force_overlay for seamless signal integration on the price chart or indicator pane.

Technical Details

Calculation Logic:

Uses confirmed bars (barstate.isconfirmed) to calculate metrics, ensuring reliability.

Short-term percentage: (close - lowest(low, lookback_short)) / (highest(high, lookback_short) - lowest(low, lookback_short)).

Long-term percentage: (close - lowest(low, lookback_long)) / (highest(high, lookback_long) - lowest(low, lookback_long)).

Derived metrics:

pct_above_long_above_short = (pct_above_long * pct_above_short) * 100.

pct_above_long_below_short = (pct_above_long * (1 - pct_above_short)) * 100.

pct_below_long_below_short = ((1 - pct_above_long) * (1 - pct_above_short)) * 100.

Signal Plotting:

Entry signals (long_entry) use ta.crossover to detect when pct_above_long_above_short crosses above entryThresholdhigh and pct_below_long_below_short is below entryThresholdlow.

Exit signals (long_exit) use ta.crossover for pct_above_long_above_short crossing above profitTake.

Signals are plotted as tiny circles with force_overlay=true for main chart or standard plotting for the indicator pane.

Performance Considerations: Optimized for efficiency by calculating metrics only on confirmed bars and using lightweight plotting functions.

How to Use

Add to Chart:

Copy the script into TradingView’s Pine Editor and apply it to your chart.

Configure Settings:

Short Lookback Period: Adjust the short-term lookback (default: 50 bars) for sensitivity.

Long Lookback Period: Set the long-term lookback (default: 200 bars) for broader context.

Entry Thresholds: Modify high (default: 20%) and low (default: 40%) thresholds for entry conditions.

Profit Take Level: Set the exit threshold (default: 95%) for profit-taking.

Plot Signals on Main Chart: Check to display signals on the price chart; uncheck for the indicator pane.

Interpret Signals:

Long Entry: Blue dots indicate a strong bullish setup when price is high relative to both lookback ranges and weakness is low.

Long Exit: White dots signal profit-taking when strength reaches overbought levels.

Use the stacked area charts to assess trend strength and momentum.

Set Alerts:

Create alerts for Long Entry and Long Exit conditions using TradingView’s alert system.

Customize Visuals:

Adjust colors and thresholds via TradingView’s settings for better visibility.

The ticker table displays the symbol and timeframe in the top-right corner.

Example Use Cases

Swing Trading: Use entry signals to capture short-term bullish moves within a broader uptrend, exiting at profit-taking levels.

Trend Confirmation: Monitor the green area (Percent Above Long & Above Short) for sustained bullish momentum.

Market Sentiment Analysis: Use the stacked areas to gauge bullish vs. bearish sentiment across timeframes.

Notes

Testing: Backtest the indicator on your chosen market and timeframe to validate its effectiveness.

Compatibility: Built for Pine Script v6 and tested on TradingView as of June 20, 2025.

Limitations: Signals are long-only; adapt the script for short strategies if needed.

Enhancements: Consider adding a histogram for the difference between metrics or additional thresholds for nuanced trading.

Acknowledgments

Inspired by public Pine Script examples and designed to simplify complex market dynamics into a clear, actionable tool. For licensing or support, contact Chuck Schultz (@chuckaschultz) on TradingView. Share feedback in the comments, and happy trading!

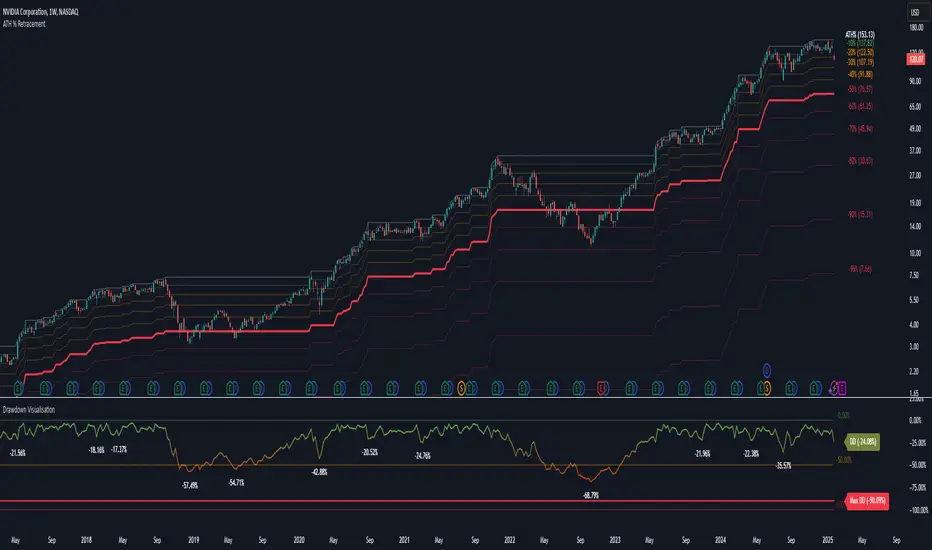

Drawdown Visualisation█ OVERVIEW

The Drawdown Visualisation indicator calculates and displays the instrument’s drawdown (in percent) relative to its all‐time high (ATH) from a user‐defined start date. It provides customisable options for label appearance, threshold lines (0%, –50%, –100%), and can plot historic drawdown levels via pivot detection.

█ USAGE

This indicator should be used with the Percentage Retracement from ATH indicator.

█ KEY FEATURES

Custom Date Settings — Use a custom start date so that only specified price action is considered.

Retracement Level Calculation — Determines ATH and computes multiple retracement levels using percentages from 0% to –100%.

Visual Signals and Customisation — Plots configurable horizontal lines and labels that display retracement percentages and prices.

Time Filtering — Bases calculations on data from the desired time period.

Historic Drawdowns — Display historical drawdowns

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

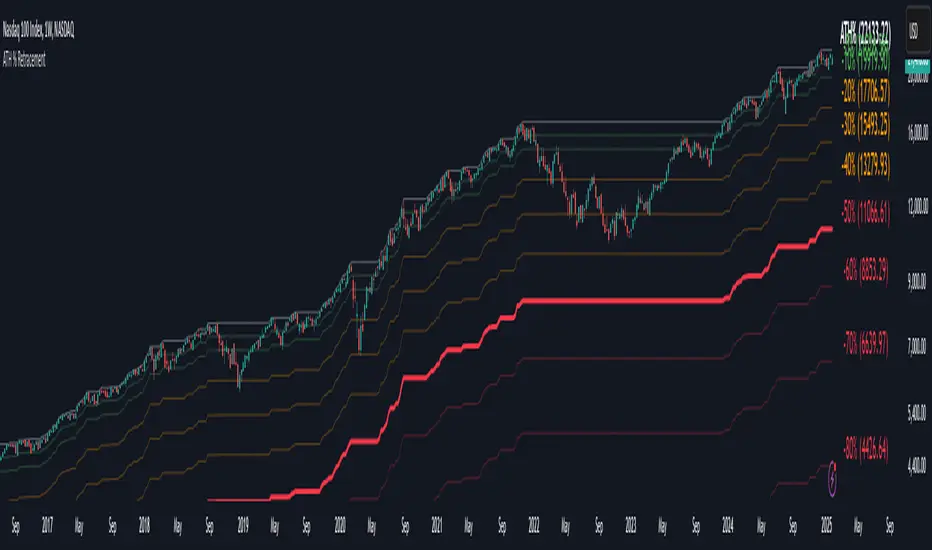

Percentage Retracement from ATH█ OVERVIEW

The Percentage Retracement from ATH indicator is a dynamic trading utility designed to help traders gauge market pullbacks from the peak price. By calculating key retracement levels based on the All-Time High (ATH) and user‑defined percentage inputs, it offers clear visual cues to assist in identifying potential support and resistance zones.

█ KEY FEATURES

Custom Date — Use a custom start date so the indicator only considers specified price action.

Retracement Calculation — Determines ATH and calculates levels based on user‑defined percentages (0% to –100%).

Visual Customisation — Plots configurable horizontal lines and labels showing retracement percentages and prices.

Time Filtering — Uses time filtering to base levels on the desired data period.

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

3 Down, 3 Up Strategy█ STRATEGY DESCRIPTION

The "3 Down, 3 Up Strategy" is a mean-reversion strategy designed to capitalize on short-term price reversals. It enters a long position after consecutive bearish closes and exits after consecutive bullish closes. This strategy is NOT optimized and can be used on any timeframes.

█ WHAT ARE CONSECUTIVE DOWN/UP CLOSES?

- Consecutive Down Closes: A sequence of trading bars where each close is lower than the previous close.

- Consecutive Up Closes: A sequence of trading bars where each close is higher than the previous close.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The price closes lower than the previous close for Consecutive Down Closes for Entry (default: 3) consecutive bars.

The signal occurs within the specified time window (between Start Time and End Time).

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average).

2. EXIT CONDITION

A Sell Signal is generated when the price closes higher than the previous close for Consecutive Up Closes for Exit (default: 3) consecutive bars.

█ ADDITIONAL SETTINGS

Consecutive Down Closes for Entry: Number of consecutive lower closes required to trigger a buy. Default = 3.

Consecutive Up Closes for Exit: Number of consecutive higher closes required to exit. Default = 3.

EMA Filter: Optional 200-period EMA filter to confirm long entries in bullish trends. Default = disabled.

Start Time and End Time: Restrict trading to specific dates (default: 2014-2099).

█ PERFORMANCE OVERVIEW

Designed for volatile markets with frequent short-term reversals.

Performs best when price oscillates between clear support/resistance levels.

The EMA filter improves reliability in trending markets but may reduce trade frequency.

Backtest to optimize consecutive close thresholds and EMA period for specific instruments.

RSI OB/OS Strategy Analyzer█ OVERVIEW

The RSI OB/OS Strategy Analyzer is a comprehensive trading tool designed to help traders identify and evaluate overbought/oversold reversal opportunities using the Relative Strength Index (RSI). It provides visual signals, performance metrics, and a detailed table to analyze the effectiveness of RSI-based strategies over a user-defined lookback period.

█ KEY FEATURES

RSI Calculation

Calculates RSI with customizable period (default 14)

Plots dynamic overbought (70) and oversold (30) levels

Adds background coloring for OB/OS regions

Reversal Signals

Identifies signals based on RSI crossing OB/OS levels

Two entry strategies available:

Revert Cross: Triggers when RSI exits OB/OS zone

Cross Threshold: Triggers when RSI enters OB/OS zone

Trade Direction

Users can select a trade bias:

Long: Focuses on oversold reversals (bullish signals)

Short: Focuses on overbought reversals (bearish signals)

Performance Metrics

Calculates three key statistics for each lookback period:

Win Rate: Percentage of profitable trades

Mean Return: Average return across all trades

Median Return: Median return across all trades

Metrics calculated as percentage changes from entry price

Visual Signals

Dual-layer signal display:

BUY: Green triangles + text labels below price

SELL: Red triangles + text labels above price

Semi-transparent background highlighting in OB/OS zones

Performance Table

Interactive table showing metrics for each lookback period

Color-coded visualization:

Win Rate: Gradient from red (low) to green (high)

Returns: Green for positive, red for negative

Time Filtering

Users can define a specific time window for the indicator to analyze trades, ensuring that performance metrics are calculated only for the desired period.

Customizable Display

Adjustable table font sizes: Auto/Small/Normal/Large

Toggle option for table visibility

█ PURPOSE

The RSI OB/OS Strategy Analyzer helps traders:

Identify mean-reversion opportunities through RSI extremes

Backtest entry strategy effectiveness across multiple time horizons

Optimize trade timing through visual historical performance data

Quickly assess strategy robustness with color-coded metrics

█ IDEAL USERS

Counter-Trend Traders: Looking to capitalize on RSI extremes

Systematic Traders: Needing quantitative strategy validation

Educational Users: Studying RSI behavior in different market conditions

Multi-Timeframe Analysts: Interested in forward returns analysis

Internal Bar Strength (IBS) Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a long position when the IBS indicates oversold conditions and exits when the IBS reaches overbought levels. This strategy was designed to be used on the daily timeframe.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- **Low IBS (≤ 0.2)**: Indicates the close is near the bar's low, suggesting oversold conditions.

- **High IBS (≥ 0.8)**: Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value drops below the Lower Threshold (default: 0.2).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value rises to or above the Upper Threshold (default: 0.8). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy exits trades. Default is 0.8.

Lower Threshold: The IBS level at which the strategy enters long positions. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for ranging markets and performs best when prices frequently revert to the mean.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Bollinger Bands Reversal Strategy Analyzer█ OVERVIEW

The Bollinger Bands Reversal Overlay is a versatile trading tool designed to help traders identify potential reversal opportunities using Bollinger Bands. It provides visual signals, performance metrics, and a detailed table to analyze the effectiveness of reversal-based strategies over a user-defined lookback period.

█ KEY FEATURES

Bollinger Bands Calculation

The indicator calculates the standard Bollinger Bands, consisting of:

A middle band (basis) as the Simple Moving Average (SMA) of the closing price.

An upper band as the basis plus a multiple of the standard deviation.

A lower band as the basis minus a multiple of the standard deviation.

Users can customize the length of the Bollinger Bands and the multiplier for the standard deviation.

Reversal Signals

The indicator identifies potential reversal signals based on the interaction between the price and the Bollinger Bands.

Two entry strategies are available:

Revert Cross: Waits for the price to close back above the lower band (for longs) or below the upper band (for shorts) after crossing it.

Cross Threshold: Triggers a signal as soon as the price crosses the lower band (for longs) or the upper band (for shorts).

Trade Direction

Users can select a trade bias:

Long: Focuses on bullish reversal signals.

Short: Focuses on bearish reversal signals.

Performance Metrics

The indicator calculates and displays the performance of trades over a user-defined lookback period ( barLookback ).

Metrics include:

Win Rate: The percentage of trades that were profitable.

Mean Return: The average return across all trades.

Median Return: The median return across all trades.

These metrics are calculated for each bar in the lookback period, providing insights into the strategy's performance over time.

Visual Signals

The indicator plots buy and sell signals on the chart:

Buy Signals: Displayed as green triangles below the price bars.

Sell Signals: Displayed as red triangles above the price bars.

Performance Table

A customizable table is displayed on the chart, showing the performance metrics for each bar in the lookback period.

The table includes:

Win Rate: Highlighted with gradient colors (green for high win rates, red for low win rates).

Mean Return: Colored based on profitability (green for positive returns, red for negative returns).

Median Return: Colored similarly to the mean return.

Time Filtering

Users can define a specific time window for the indicator to analyze trades, ensuring that performance metrics are calculated only for the desired period.

Customizable Display

The table's font size can be adjusted to suit the user's preference, with options for "Auto," "Small," "Normal," and "Large."

█ PURPOSE

The Bollinger Bands Reversal Overlay is designed to:

Help traders identify high-probability reversal opportunities using Bollinger Bands.

Provide actionable insights into the performance of reversal-based strategies.

Enable users to backtest and optimize their trading strategies by analyzing historical performance metrics.

█ IDEAL USERS

Swing Traders: Looking for reversal opportunities within a trend.

Mean Reversion Traders: Interested in trading price reversals to the mean.

Strategy Developers: Seeking to backtest and refine Bollinger Bands-based strategies.

Performance Analysts: Wanting to evaluate the effectiveness of reversal signals over time.

Buy on 5 day low Strategy█ STRATEGY DESCRIPTION

The "Buy on 5 Day Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous five days. It enters a long position when specific conditions are met and exits when the price exceeds the high of the previous day. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE 5-DAY LOW?

The 5-Day Low is the lowest price observed over the last five days. This level is used as a reference to identify potential oversold conditions and reversal points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous five days (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous day (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support levels.

It is sensitive to oversold conditions, as indicated by the 5-Day Low, and overbought conditions, as indicated by the previous day's high.

Backtesting results should be analyzed to optimize the strategy for specific instruments and market conditions.

3-Bar Low Strategy█ STRATEGY DESCRIPTION

The "3-Bar Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous three bars. It enters a long position when specific conditions are met and exits when the price exceeds the highest high of the previous seven bars. This strategy is suitable for use on various timeframes.

█ WHAT IS THE 3-BAR LOW?

The 3-Bar Low is the lowest price observed over the last three bars. This level is used as a reference to identify potential oversold conditions and reversal points.

█ WHAT IS THE 7-BAR HIGH?

The 7-Bar High is the highest price observed over the last seven bars. This level is used as a reference to identify potential overbought conditions and exit points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous three bars (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

If the EMA Filter is enabled, the close price must also be above the 200-period Exponential Moving Average (EMA).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

MA Period: The lookback period for the 200-period EMA used in the EMA Filter. Default is 200.

Use EMA Filter: Enables or disables the EMA Filter for long entries. Default is disabled.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support and resistance levels.

It is sensitive to oversold conditions, as indicated by the 3-Bar Low, and overbought conditions, as indicated by the 7-Bar High.

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments.

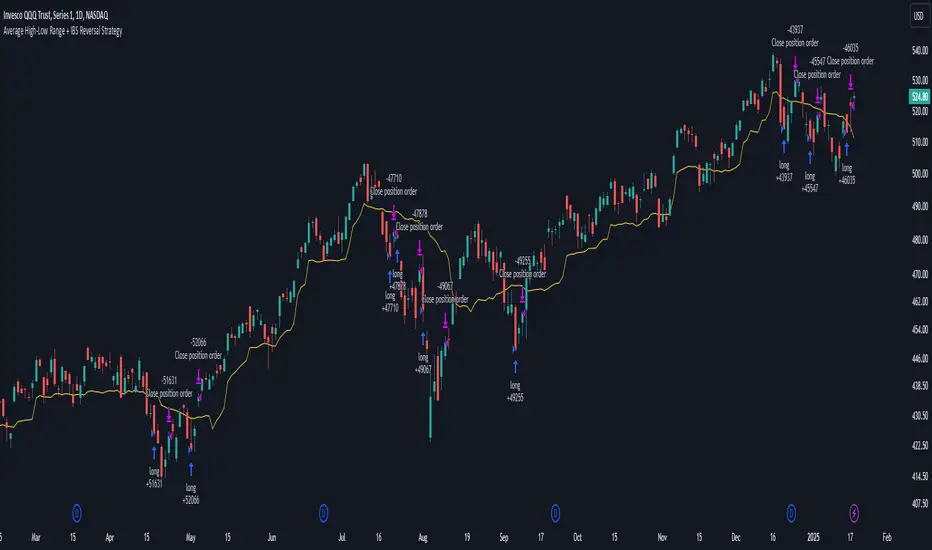

Average High-Low Range + IBS Reversal Strategy█ STRATEGY DESCRIPTION

The "Average High-Low Range + IBS Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates significantly from its average high-low range and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the price shows strength by exceeding the previous bar's high. This strategy is suitable for use on various timeframes.

█ WHAT IS THE AVERAGE HIGH-LOW RANGE?

The Average High-Low Range is calculated as the Simple Moving Average (SMA) of the difference between the high and low prices over a specified period. It helps identify periods of increased volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been below the buy threshold (calculated as `upper - (2.5 * hl_avg)`) for a specified number of consecutive bars (`bars_below_threshold`).

The IBS value is below the specified buy threshold (`ibs_buy_treshold`).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the average high-low range. Default is 20.

Bars Below Threshold: The number of consecutive bars the price must remain below the buy threshold to trigger a Buy Signal. Default is 2.

IBS Buy Threshold: The IBS value below which a Buy Signal is triggered. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from its average high-low range.

It is sensitive to oversold conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length, Bars Below Threshold, and IBS Buy Threshold parameters for specific instruments.

Pulse Profiler [QuantraSystems]Pulse Profiler

Introduction

The Pulse Profiler ( ℙℙ ) is specifically designed to unambiguously indicate weakening momentum after a strong impulse. The upper and lower standard deviation bands also allow the user to assess the strength of an impulse and differentiate it from general noise.

Due to the ℙℙ ’s rapid responsiveness to exhaustion in price movement it is ideally used for the trader to recognize when to start taking profit when combined with other indicators.

The novum is that by dynamically balancing its sensitivity to recent movements the ℙℙ considers the asset’s inherent volatility. By reducing noise without sacrificing signal, and by visualizing it in our typical modern QuantraAI style, the ℙℙ enhances the traders’ ability to distinguish impulses with weakening momentum from strong trending movements.

Legend

Impulse: The ℙℙ showing strength based on momentum and volume.

Dynamic standard deviation bands: Rolling probability based bands based on a rolling normal distribution. Adjustable, recommended are σ = 1.5 to σ = 2.5.

Neutral lines: Dynamic thresholds which get often respected as support or resistance.

Case Study

To properly employ the ℙℙ , the trader should use it to identify out-of-the-ordinary 𝓲𝓶𝓹𝓾𝓵𝓼𝓮𝓼 which cause a following exhaustion.

The rolling standard deviation bands incorporate the asset’s historical behavior in regards to its inherent volatility on a rolling basis. If the asset shows strong 𝓲𝓶𝓹𝓾𝓵𝓼𝓮𝓼 that go beyond the rolling standard deviation, the event has been highly improbable. The trader then needs to determine if the price change was caused by critical external factors. If not, it is highly probable that the momentum exhausts and that price movement plateaus to enter a range.

These signals indicate that it is highly probable that closing a position upon these conditions is the correct choice.

If the 𝓲𝓶𝓹𝓾𝓵𝓼𝓮 reverses and retraces into the opposite direction, while moving more than 1.5σ across just 3 bars on the 4H chart, the signal indicates that a reversal is pushing the price down – in both momentum and volume.

A sharp reversal thus becomes more probable than not.

The ℙℙ can also be calibrated to find possible trend exhaustions on a longer timeframe (1D).

Please always use multiple Quantra indicators to add confirmations to your signals.

Recommended Settings

Swing Trading (4H chart)

Standard Deviation Lookback: 150

Standard Deviation Multiplier (σ): 2.5

Display Variant: Classic

Choose Mode for Bar Coloring: Signal

Trend exhaustion (1D chart)

Standard Deviation Lookback: 200

Standard Deviation Multiplier (σ): 2.0

Display Variant: Classic

Choose Mode for Bar Coloring: Extremes

Notes

Quantra Standard Value Contents:

The Heikin-Ashi (HA) candle visualization smoothes out the signal line to provide more informative insights into momentum and trends. This allows earlier entries and exits by observing the indicator values transformed by the HA.

Various visualization options are available to adjust the indicator to the user’s preference: Aside from HA, a classic line, or a hybrid of both.

A special feature of Quantra’s indicators is that they are probabilistically built - therefore they work well as confluence and can easily be stacked to increase signal accuracy.

To add to Quantra's indicators’ utility we have added the option to change the price bars colors based on different signals:

Choose Mode for Coloring

Trend Following (Indicator above mid line counts as uptrend, below is downtrend)

Extremes (Everything beyond the SD bands is highlighted to signal mean reversion)

Candles (Color of HA candles as barcolor)

Reversions (Only for HA) (Reversion Signals via the triangles if HA candles change trend while beyond the SD bands, high probability entries/exits)

The ℙℙ is also sensitive to divergences for those interested in utilizing this feature.

Through a special combination of price, volume and momentum you get a holistic overview on the impulse strengths of movements.

The two neutral lines in the center act as dynamic, volume and volatility adjusted thresholds. Often the signal line respects them as support and resistance.

The upper and lower standard deviation lines express the rarity of an impulse based on the asset’s inherent volatility.

The indicator needs a long enough timespan to build up its probability estimation, therefore the asset needs sufficient price history.

The indicator requires thorough volume data. If the source of an asset pair does not forward it, try to find another source or exchange for the same pair.

Signal Mode on the 4H chart is a relevant part of this indicator when used in isolation and helps to analyze momentum adjusted by volatility.

Methodology

The ℙℙ combines the Arnaud Legoux Moving Average (ALMA) with a bespoke volume and momentum calculation, with a classical Exponential Moving Average (EMA) on price data.

The ℙℙ itself integrates ALMA for volume and momentum with an EMA calculation on price, creating a unique blend that expresses impulses using their three raw main components.

The indicator calculates dynamic standard deviation bands based on an adjustable lookback period and the adjustable sigma (σ), to signal when the impulse strength is just uncommon or even extraordinary when compared to the usual price movements:

σ = 1.5 the probability of similar impulse strength occuring is 13.37% / 2, hence ~ 6.69%

σ = 2.0 the probability of similar impulse strength occuring is ~ 2.28%

σ = 2.5 the probability of similar impulse strength occuring is ~ 0.62%

By detecting extremely improbable conditions the indicator can create an inversely highly probable signal to its user.

Neutral bands are calculated based on the ℙℙ alongside a rolling, dynamic multiplier. This effectively provides dynamic thresholds for approximating common volatility.

Heikin Ashi method: The indicator uses a custom function to calculate Heikin Ashi values, useful for smoothing impulse data and identifying trends.

Reversion Signals: Specifically for Heikin Ashi displays, we plot triangles as signals, useful to easily spot potential reversals.

The Signal Mode uses these different thresholds to highlight significant market moves.

Dip & Rip Patterns - The Quant Science🇺🇸

GENERAL OVERVIEW

This indicator detects Dip and Rip patterns by quickly highlighting them on the chart.

These patterns have become popular during the pandemic period mainly in the stock, ETF and cryptocurrency markets on which traders use two interesting strategies:

Buy The Dip

Sell The Rip

Before going into the merits of this technical indicator, let's understand what these two patterns mean and what they identify precisely.

Rip (Rise In Price) : wants to identify a market condition in which the price rises rapidly, for example from $100 to $110 in a few minutes or hours.

Dip (Drop In Price) : wants to identify a market condition in which the price drops rapidly, for example from $100 to $90 in a few minutes or hours.

HOW TO USE

For a better user experience, we recommend choosing a neutral colour for the candles while analysing with this indicator. You can quickly change the colour in Chart Settings > Symbol > Candles .

Depending on the configuration set by the user, the indicator will show Dip (Dip In Price) patterns in red and Rip (Rise In Price) patterns in green.

When the pattern forms, a circle will be displayed and a vertical line will be coloured on the chart along with the body of the candle. The user will then be able to quickly and easily track the configured market conditions.

In this example, we decided to use a 4H timeframe on the BTC/USDT pair (Binance).

Set in the user interface:

Period: 20

Dip (%): -25

Rip (%): 20

Price falls by 25% or more in 80 hours (Dip Pattern).

Price rise by 25% or more in 80 hours (Rip Pattern).

The user can easily configure the parameters via the user interface in the Inputs section (A) and change the indicator design in the Properties section (B).

🇮🇹

PANORAMICA GENERALE

Questo indicatore rileva i Dip e Rip patterns evidenziandoli velocemente sul grafico.

Questi patterns sono diventati famosi durante il periodo pandemico principalmente nel mercato delle azioni, ETF e Criptovalute su cui i trader utilizzano due interessanti strategie:

Buy The Dip

Sell The Rip

Prima di entrare nel merito di questo indicatore tecnico, comprendiamo il significato di questi due pattern e cosa identificano precisamente.

Rip (Rise In Price) : vuole identificare una condizione di mercato in cui il prezzo sale rapidamente, per esempio passando da 100$ a 110$ in pochi minuti o poche ore.

Dip (Drop In Price) : vuole identificare una condizione di mercato in cui il prezzo cala rapidamente, per esempio passando da 100$ a 90$ in pochi minuti o poche ore.

UTILIZZO

Per una migliore esperienza utente consigliamo di scegliere un colore neutro per le candele mentre si analizza con questo indicatore. Puoi cambiare velocemente il colore in Chart Settings > Symbol > Candles .

In base alla configurazione impostata dall'utente l'indicatore mostrerà in rosso i pattern Dip (Dip In Price) e in verde i pattern Rip (Rise In Price).

Quando il pattern si forma verrà visualizzato un cerchio e una linea verticale sul grafico che sarà colorata insieme al corpo della candela. L'utente quindi potrà tracciare facilmente e velocemente le condizioni di mercato configurate.

In questo esempio abbiamo deciso di utilizzare un timeframe 4H con l'obbiettivo di ricercare i patterns sul pair BTC/USDT (Binance).

Impostiamo nell'interfaccia utente:

Period: 20

Dip (%): -25

Rip (%): 20

Il prezzo diminuisce del 25% o più in 80 ore (Dip Pattern).

Il prezzo aumenta del 25% o più in 80 ore (Rip Pattern).

L' utente può configurare facilmente i parametri attraverso l'interfaccia utente nella sezione Inputs (A) e modificare il design dell'indicatore nella sezione Properties (B).

BTFD strategy [3min]Hello

I would like to introduce a very simple strategy to buy lows and sell with minimal profit

This strategy works very well in the markets when there is no clear trend and in other words, the trend going sideways

this strategy works very well for stable financial markets like spx500, nasdaq100 and dow jones 30

two indicators were used to determine the best time to enter the market:

volume + rsi values

volume is usually the number of stocks or contracts traded over a certain period of time. Thus, it is an important indicator of market activity and liquidity. Each transaction constitutes an individual exchange between the buyer and the seller and constitutes the trading volume of a given instrument or asset.

The RSI measures the strength of uptrends versus downtrends. The signal is the entry or exit of the indicator value of the oversold or overbought level of the market. It is assumed that a value below or equal 30 indicates an oversold level of the market, and an RSI value above or equal 70 indicates an overbought level.

the strategy uses a maximum of 5 market entries after each candle that meets the condition

uses 5 target point levels to close the position:

tp1= 0.4%

tp2= 0.6%

tp3= 0.8%

tp4= 1.0%

tp5= 1.2%

after reaching a given profit value, a piece of the position is cut off gradually, where tp5 closes 100% of the remaining position

each time you enter a position, a stop loss of 5.0% is set, which is quite a high value, however, when buying each, sometimes very active downward price movement, you need a lot of space for market decisions in which direction it wants to go

to determine the level of stop loss and target point I used a piece of code by RafaelZioni , here is the script from which a piece of code was taken

this strategy is used for automation, however, I would recommend brokers that have the lowest commission values when opening and closing positions, because the strategy generates very high commission costs

Enjoy and trade safe ;)

LNL Pullback ArrowsBuying the dip has never been easier! LNL Pullback Arrows are here to pinpoint the best possible entries for the trend following setups. With the Pullback Arrows, trader can pick his own approach and risk level thanks to four different types of arrows. The goal of these arrows is to force the traders to scale in & out of trades which is in my opinion crucial when it comes to trend following strategies. These arrows were designed primarily for the daily & weekly time frame (swing trading).

Four Types of Pullback Arrows:

1. Aggro Arrows - Ideal for aggresive approach during parabolic trends. Sometimes trends are so strong that the price barely revisits the daily 8 EMA. This is where the aggro arrows can perfectly pinpoint the aggresive high risk entries. Ideal for halfsize or 1/4 size of the full position. Aiming for quick 1-2 day moves targeting the recent high/low. These arrows could be also named as scalping arrows for the swing traders. A quick In & Out.

2. HalfSize Arrows - Medium risk approach. First arrows to scale in. HalfSize arrows are the first sign that the pullback might be ending, yet there is still some space left for an even deeper pullback. That is the reason why they are called half-size. Ideally taken with half-sized position. When trading the HalfSize Arrows, It is better to have some "spare ammo in the gun" ready to use.

3. FullSize Arrows - Regular risk approach. These arrows represent a zone where the core of the posititon should be taken. The point of validity for the trend is not that far away, meaning the risk can be kept tight. Ideal for scailing the other halfs or quarters of the full position. Also great for more conservative traders or environments with higher volatility.

4. Rare Arrows - Offer the best risk to reward entries during the trend. Rare Arrows should be the "last kick" of the retracement, therefore stops can be positioned really tight. They either trigger the stop immidiately or they provide another juicy leg up or down in the direction of the trend. However, they really do appear rarely.

Simple EMA Cloud:

A simple cloud based on 21 and 55 exponential moving averages. This default length creates a pullback zone that is wide enough for the conservative traders but also give the opportunities to more aggresive traders. Alternatives such as 8 & 21, or 21 & 34 are forming the zone that is too aggresive and usually too thin. Of course, cloud can be fully adjusted or turned off completely. The only role of the cloud is to gauge the trend.

Tips & Tricks:

1.Importance of the Scailing

- As already stated, scailing is crucial to this since there is no way of knowing the exact level at which the price magically bounce every time. It is hard to tell where and which EMA will be respected. How can we know it will be 21 EMA every time? or 34 EMA or 10 EMA or 100 SMA or 50 DMA ... Single MA does not make a trend. This is the reason why scailing is so important. Scailing can make a difference.

2. Nothing is Perfect

- Same as any other study, nothing works 100% perfectly. Sometimes the setup will go right against you and sometimes the price will fade away sideways and breaks off the structure of the trend. This is not a magic certainty tool. This is just another probability tool.

3. Point of Validity & Other Studies

- Even though the pullback arrows can be a stand-alone strategy. It is important to use other indicators that visualize the actual trend. Whether its EMA Cloud or EMAs or DMI Bars or Keltner Channels, there should be something that validates the trend, something that tells the trend is over. (Pullback Arrows are not showing the actual stops!).

Hope it helps.

CryptoFall v1.0.0Category: Trend Analysis

Timeframe:

- Best on 4H, D

- Faster on 30M, 1H

Suggested Use: In uptrend.

Input option: Is possible to use "Alternative Time Frame" using other candles on different Time Frame charts.

Logic: The tradable market range is calculated, on which the Fibonacci levels are automatically calculated, at this point the entries could be defined entering on the important zone levels.

The calculation takes into account a combination of indicators such as:

- Fibonacci Retracement ( FibRetr )

- Theory of W. D. Gann .

Entry: The indicator uses Fibonacci levels to identify a good time to enter using the Buy the Dip approach (i.e. considering that a typical pullback is in the range between 0.382 and 0.618).

Tips: The best way to enter the market is always to split the positions so as not to enter entirely and expose yourself with all your capital, @TheSocialCryptoClub insists on a careful management of the orders so as to be able to mediate the price depending on the depth of the retracements.

Exit: Defined by the investor's long-term objective.

Thanks for attention.

Automatic half priceJapanese below / 日本語説明は下記

This indicator automatically draws half price lines based on the logic below.

Today’s half price: Half price between today’s high and low

Yesterday’s half price: Half price between yesterday’s high and low

Half price as hidden support and resistance

As a characteristic of market, price sometimes tests previous day’s half price first when previous day ends with bullish candle, then tries new high.

Example1: USDJPY Daily chart: New high after testing previous day’s half price

July9 ends with bullish candle. July10 candle tests previous day’s half first, then records new high.

Example2: USDJPY 1H chart: New high after testing today’s half price

Another example is that today’s half is tested by NY session.

In this case, Asian & European session is an uptrend. When the NY session starts, it tests the half of Asian & Euro sessions’ gain then records new high.

———————————————————————

押し目戻り目として意識される半値を自動描画するインジケーターです。

当日半値: 当日日足ローソク足の高値と安値の半値

先日半値: 先日日足ローソク足の高値と安値の半値

<参考>

押し目戻り目として意識される半値

相場の動きの特徴として、例えば前日の日足ローソク足が陽線で引けた場合、前日の陽線の半値付近を一度試してから上昇するという動きがよく見られます。

例1 ドル円日足: 前日の半値を試してから上昇

7/9は陽線で引けています。翌日7/10のローソク足は前日の半値付近を試した後、高値更新をしています。

例2 ドル円 1時間足: 当日の半値を試してから上昇

8/10のアジア時間と欧州時間は上昇トレンドです。NY時間がスタートした時、アジア時間と欧州時間の上昇の半値付近を試した後、高値更新をしています。

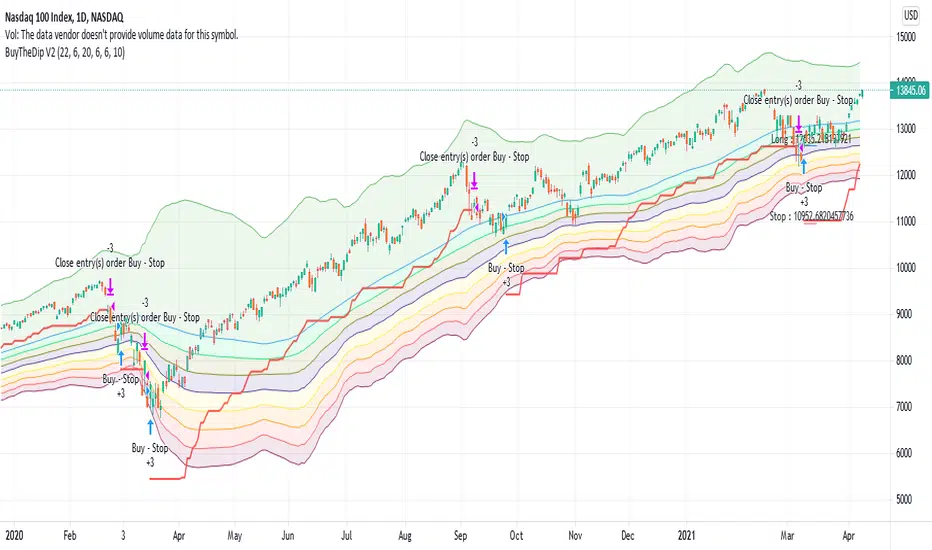

BuyTheDip V2This is enhanced version of BuyTheDip Strategy which can be used for stocks and cryptos as well along with indices.

In addition to V1, the enhancement include breaking the zone into multiple levels based on multiple standard deviation Bollinger bands. Dip is confirmed only when price bounce back certain levels from the bottom. If price keeps going down, strategy does not generate signal.

Input parameters are as below:

ATR Parameters : AtrLength and AtrMult to calculate trailing stops

Trailing Condition parameters : TrailAfterBars, TrailTargetState - Trailing does not happen immediately. It either waits for TrailAfterBars to complete or price moves up by TrailTargetState levels in multi bollinger band level setup - whichever happens first.

Force Exit Parameters : If the price state based on multi-bollinger bands drop by TargetStopStateDiff level from its peak, then it will force exit from the trade if ExitOnFailureSignal is checked.

Entry Filters : It is not a dip if the instrument is already in downtrend. ConsiderYearlyHighLow , ConsiderNewLongTermHighLows and ConsiderMAAlignment are used for filtering entries so that we only buy the dip for uptrending instruments.

Optimized RSI Strategy - Buy The Dips (by Coinrule)Buy low and sell high is every trader's mantra. While this approach looks straightforward in theory, it's sometimes challenging to put into practice. That requires stress-management to buy when price drops and resolution in selling when the price is rising. RSI is a useful tool to implement long-term and effective trading strategies. The script presents an optimized RSI trading strategy that uses a Moving average to spot the best time to buy the dip.

The strategy buys when the RSI is lower than 35, and at the same time, the price is below the MA100. In this way, the approach helps avoid catching early dips, increasing buying when the bottom approaches.

The position closes when the RSI value is above 65 . Depending on the volatility of the coins that the strategy will trade, it's possible to adjust the RSI exit value to chase larger profits.

The setup is optimized on a 15-minutes time frame and trading cryptocurrencies versus USD or stable coins.

The strategies was backtested over 150 times with multiple setups and coin to assess the best long-term system.

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Multi Time Frame Buy the Dips (by Coinrule)Buying the dips is a relatively easy automated trading strategy that can return impressive profits, especially during uptrend times. Not all price drops are for buying, though. This trading system is based on a multi time frame buy-the-dip approach to optimize each trade.

The strategy catches sudden price drops on a 1-hr time frame when the price increases significantly in the last 12 hours. During steep uptrends, profit-taking price actions result in flash crashes that provide great opportunity to enter at convenient prices.

Buy Condition

The setup of the script is optimized on a 30 min time frame. You can adjust the parameters to fit different time frames.

The system gets a buy signal when

- the price drops 1% from the two previous candles (1 hour time frame = two 30-min candles)

- the price is up 3% from the last 12 hours (twenty-four 30-min candles equal the desired time frame)

Sell Condition

Each trade comes with a stop loss of 3% and a take profit of 4%.

This setup has been optimized, running over 150 backtests on more than 20 different crypto trading pairs.

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Buy the Dips (by Coinrule)Taking your first steps into automated trading may be challenging. Coinrule's mission is to make it as easy as possible, also for beginners.

Here follows the best trading strategy to get started with Coinrule. This strategy doesn't involve complex indicators, yet was proved to be effective in the long term for many coins. Results seem to be improved when trading a coin vs Bitcoin.

The strategy buys the dips of a coin to sell with a profit. A stop-loss protects every trade.

Crypto markets offer high volatility and, thus, excellent opportunities for trading. Excluding times of severe downtrend, buying the dip is a simple and effective long-term trading strategy. The buy-signal is set to a 2% drop in a 30-minutes time frame.

Each trade comes with a take profit and a stop loss. Both set at 2%.

You can adjust these percentages to the market volatility as an advanced setup. You can backtest the outcomes using the backtesting tool from Tradingview

The strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

BuyTheDipWell, I often had arguments in online forum with a guy who claimed to time the market perfectly without any technical analysis or prior experience. He often claimed that technical analysis does not work and it only works when you trade on other's emotions. He also argued that algorithmic trading isn't profitable - if so, everyone would do that. Hence, I thought I will convert his idea to algorithm.

In his own words, the strategy is as below:

Chose an instrument which is in full uptrend.

Wait for the panic sell and buy the dip

Once market recovers back exit immediately

It seems to do just fine with indexes. But, not so good when it comes to stocks.