Historical Correlation [LuxAlgo]The Historical Correlation tool aims to provide the historical correlation coefficients of up to 10 pairs of user-defined tickers starting from a user-defined point in time.

Users can choose to display the historical values as lines or the most recent correlation values as a heat map.

🔶 USAGE

This tool provides historical correlation coefficients, the correlation coefficient between two assets highlight their linear relationship and is always within the range (-1, 1).

It is a simple and easy to use statistical tool, with the following interpretation:

Positive correlation (values close to +1.0): the two assets move in sync, they rise and fall at the same time.

Negative correlation (values close to -1.0): the two assets move in opposite directions: when one goes up, the other goes down and vice versa.

No correlation (values close to 0): the two assets move independently.

The user must confirm the selection of the anchor point in order for the tool to be executed; this can be done directly on the chart by clicking on any bar, or via the date field in the settings panel.

For the parameter Anchor period , the user can choose between the following values NONE, HOURLY, DAILY, WEEKLY, MONTHLY, QUARTERLY and YEARLY. If NONE is selected, there will be no resetting of the calculations, otherwise the calculations will start from the first bar of the new period.

There is a wide range of trading strategies that make use of correlation coefficients between assets, some examples are:

Pair Trading: Traders may wish to take advantage of divergences in the price movements of highly positively correlated assets; even highly positively correlated assets do not always move in the same direction; when assets with a correlation close to +1.0 diverge in their behavior, traders may see this as an opportunity to buy one and sell the other in the expectation that the assets will return to the likely same price behavior.

Sector rotation: Traders may want to favor some sectors that are expected to perform in the next cycle, tracking the correlation between different sectors and between the sector and the overall market.

Diversification: Traders can aim to have a diversified portfolio of uncorrelated assets. From a risk management perspective, it is useful to know the correlation between the assets in your portfolio, if you hold equal positions in positively correlated assets, your risk is tilted in the same direction, so if the assets move against you, your risk is doubled. You can avoid this increased risk by choosing uncorrelated assets so that they move independently.

Hedging: Traders may want to hedge positions with correlated assets, from a hedging perspective, if you are long an asset, you can hedge going long a negative correlated asset or going short a positive correlated asset.

Traders generally need to develop awareness, a key point is to be aware of the relationships between the assets we hold or trade, the historical correlation is an invaluable tool in our arsenal which allows us to make better informed decisions.

On this chart we have an example of historical correlations for several futures markets.

We can clearly see how positively correlated the Nasdaq100 and Dow30 are with the SP500 over the whole period, or how the correlation between the Euro and the SP500 falls from almost +85% to almost -4% since 2021.

As we can see, correlations, like everything else in the market, are not static and vary over time depending on many factors, from macro to technical and everything in between.

🔹 Heatmap

The chart above shows the tool with the default settings and the Drawing Mode set to 'HEATMAP'.

We can see the current correlation between the assets, in this case the FX pairs.

The highest positive correlation is +90% (+0.90) between EURUSD and GBPUSD.

The highest negative correlation is -78% (-0.78) between EURUSD and USDJPY.

The pair with no correlation is AUDUSD and EURCAD with 1% (0.01)

On the above chart we can see the current correlations for the futures markets.

Currently, the assets that are less correlated to the SP500 are NaturalGas and the Euro, the more positive correlations are Nasdaq100 and Dow20, and the more negative correlations are the Yen, Treasury Bonds and 10-Year Notes.

🔶 DETAILS

🔹 Anchor Period

This chart shows the standard FX correlations with the Anchor Period set to `MONTHLY`.

We can clearly see how the calculations restart with the new month, in this case we can clearly see the differences between the correlations from month to month.

Let us look at the correlation coefficient between GBPUSD and USDJPY

In January, their correlation started at close to -100%, rose to close to +50%, only to fall to close to 0% and remain there for the second half of the month.

In February it was -90% in the first few days of the month and is now around -57%.

And between AUDUSD and EURCAD

Last month their correlation was negative for most of the month, reaching -70% and ending around -14%.

This month their correlation has never gone below +21% and at the time of writing is close to +53%.

🔶 SETTINGS

Anchor point: Starting point from which the tool is executed

Anchor period: At the beginning of each new period, the tool will reset the calculations

Pairs from 1 to 10: For each pair of tickers, you can: enable/disable the pair, select the color and specify the two tickers from which you wish to obtain the correlation

🔹 Style

Drawing Mode: Output style, `LINES` will show the historical correlations as lines, `HEATMAP` will show the current correlations with a color gradient from green for correlations near 1 to red for correlations near -1.

Centered Oscillators

CAPACE MARKETThis custom indicator combines the Moving Average Convergence Divergence (MACD) and the Relative Strength Index (RSI) into a single trading tool. It calculates the MACD and RSI values, then averages these two indicators to create a composite line. This average line is intended to capture the momentum and relative strength of the market simultaneously, potentially offering a more nuanced view of market conditions.

Key features of the indicator include:

Visualization of MACD and RSI Lines: It plots the MACD and RSI values as separate lines on the chart, allowing traders to see the behavior of each indicator clearly.

Average Line: A line representing the average of the MACD and RSI indicators is plotted, providing a synthesized view of both momentum and strength.

Entry Points Indication: The indicator uses red dots to mark the points where the average line crosses over or under the MACD or RSI lines. These intersections are meant to signal potential entry points for traders.

Market Condition Highlighting: The background color changes based on whether the average line is above or below zero. A green background suggests a positive market condition (bullish), while a red background indicates a negative market condition (bearish).

This tool aims to offer traders an integrated perspective by combining the insights of both MACD and RSI, potentially aiding in the identification of entry and exit points as well as the overall market sentiment.

Divergence Toolkit (Real-Time)The Divergence Toolkit is designed to automatically detect divergences between the price of an underlying asset and any other @TradingView built-in or community-built indicator or script. This algorithm provides a comprehensive solution for identifying both regular and hidden divergences, empowering traders with valuable insights into potential trend reversals.

🔲 Methodology

Divergences occur when there is a disagreement between the price action of an asset and the corresponding indicator. Let's review the conditions for regular and hidden divergences.

Regular divergences indicate a potential reversal in the current trend.

Regular Bullish Divergence

Price Action - Forms a lower low.

Indicator - Forms a higher low.

Interpretation - Suggests that while the price is making new lows, the indicator is showing increasing strength, signaling a potential upward reversal.

Regular Bearish Divergence

Price Action - Forms a higher high.

Indicator - Forms a lower high.

Interpretation - Indicates that despite the price making new highs, the indicator is weakening, hinting at a potential downward reversal.

Hidden divergences indicate a potential continuation of the existing trend.

Hidden Bullish Divergence

Price Action - Forms a higher low.

Indicator - Forms a lower low.

Interpretation - Suggests that even though the price is retracing, the indicator shows increasing strength, indicating a potential continuation of the upward trend.

Hidden Bearish Divergence

Price Action - Forms a lower high.

Indicator - Forms a higher high.

Interpretation - Indicates that despite a retracement in price, the indicator is still strong, signaling a potential continuation of the downward trend.

In both regular and hidden divergences, the key is to observe the relationship between the price action and the indicator. Divergences can provide valuable insights into potential trend reversals or continuations.

The methodology employed in this script involves the detection of divergences through conditional price levels rather than relying on detected pivots. Traditionally, divergences are created by identifying pivots in both the underlying asset and the oscillator. However, this script employs a trailing stop on the oscillator to detect potential swings, providing a real-time approach to identifying divergences, you may find more info about it here (SuperTrend Toolkit) . We detect swings or pivots simply by testing for crosses between the indicator and its trailing stop.

type oscillator

float o = Oscillator Value

float s = Trailing Stop Value

oscillator osc = oscillator.new()

bool l = ta.crossunder(osc.o, osc.s) => Utilized as a formed high

bool h = ta.crossover (osc.o, osc.s) => Utilized as a formed low

// Note: these conditions alone could cause repainting when they are met but canceled at a later time before the bar closes. Hence, we wait for a confirmed bar.

// The script also includes the option to immediately alert when the conditions are met, if you choose so.

By testing for conditional price levels, the script achieves similar outcomes without the delays associated with pivot-based methods.

type bar

float o = open

float h = high

float l = low

float c = close

bar b = bar.new()

bool hi = b.h < b.h => A higher price level has been created

bool lo = b.l > b.l => A lower price level has been created

// Note: These conditions do not check for certain price swings hence they may seldom result in inaccurate detection.

🔲 Setup Guide

A simple example on one of my public scripts, Standardized MACD

🔲 Utility

We may auto-detect divergences to spot trend reversals & continuations.

🔲 Settings

Source - Choose an oscillator source of which to base the Toolkit on.

Zeroing - The Mid-Line value of the oscillator, for example RSI & MFI use 50.

Sensitivity - Calibrates the sensitivity of which Divergencies are detected, higher values result in more detections but less accuracy.

Lifetime - Maximum timespan to detect a Divergence.

Repaint - Switched on, the script will trigger Divergencies as they happen in Real-Time, could cause repainting when the conditions are met but canceled at a later time before bar closes.

🔲 Alerts

Bearish Divergence

Bullish Divergence

Bearish Hidden Divergence

Bullish Hidden Divergence

As well as the option to trigger 'any alert' call.

The Divergence Toolkit provides traders with a dynamic tool for spotting potential trend reversals and continuations. Its innovative approach to real-time divergence detection enhances the timeliness of identifying market opportunities.

FVG OscillatorThe FVG Oscillator, developed by OmegaTools and available on TradingView, is a specialized analytical tool designed to offer traders insight into the market's potential direction through the lens of Fair Value Gaps (FVGs). This script combines traditional oscillator functionality with a unique focus on FVGs, providing a nuanced approach to understanding market dynamics.

Understanding FVGs and Their Importance:

Fair Value Gaps (FVGs) are identified when there's a discrepancy between the high price of one session and the low of the subsequent session (or vice versa), indicating areas where price movements have skipped over, creating a gap. These gaps often signal potential price movement areas, as markets may move to "fill" these gaps. The FVG Oscillator is designed to quantify these occurrences and their potential impact on market direction.

Key Features of the FVG Oscillator:

- Adjustable Lookback Period: Traders can set the number of bars back (defaulted at 50) to adjust the sensitivity of the oscillator to recent market activity.

- Visual Area Representation: The option to display areas of positive and negative FVG occurrences provides a visual representation of market sentiment over the selected period.

- Color Customisation: Users can personalize the oscillator's appearance with color selections for positive and negative movements, enhancing readability and analysis.

- Volume and ATR Confirmation: Incorporates volume data and Average True Range (ATR) filtering to verify FVG occurrences, adding a layer of validation to the identified gaps.

Operational Mechanism:

The oscillator tallies bullish FVG occurrences as positive values and bearish FVG occurrences as negative values over the specified lookback period. It then applies volume and ATR criteria to confirm the significance of these gaps. The final output is an oscillator line that reflects the net value of bullish versus bearish FVGs, alongside histograms that show the width (or significance) of long and short patterns based on confirmed FVGs.

How to Use the FVG Oscillator:

- After adding the FVG Oscillator to your TradingView chart, adjust the 'Bars Back' input to tailor the oscillator's sensitivity to your trading strategy.

- Use the net value line to gauge the overall market sentiment based on FVG occurrences; a higher net value suggests bullish sentiment, while a lower value indicates bearish sentiment.

- The histograms provide an additional layer of insight, highlighting the relative strength and significance of confirmed bullish and bearish FVGs.

Application in Trading:

The FVG Oscillator is intended as an analytical tool to complement your existing trading strategy. By offering a unique perspective on FVG occurrences and their potential market implications, the oscillator can help inform your trading decisions. However, traders are encouraged to combine this tool with other forms of analysis and employ sound risk management practices.

Originality and Usefulness:

This oscillator is original in its integration of FVG analysis with traditional oscillator metrics, offering traders a novel tool for market analysis. Its usefulness lies in its ability to provide a quantitative and visual representation of FVGs, aiding traders in identifying potential market movements.

Disclaimer:

It is important for traders to understand that the financial markets are inherently unpredictable, and the FVG Oscillator is not a predictive tool nor does it guarantee trading success. It should be used as part of a comprehensive trading strategy, incorporating additional market analysis and risk management practices. Remember, past performance does not necessarily predict future results, and trading involves risks, including the potential loss of capital.

Fair Value Gaps Mitigation Oscillator [LuxAlgo]The Fair Value Gaps Mitigation Oscillator is an oscillator based on the traditional Fair Value Gaps (FVGs) imbalances. The oscillator displays the current total un-mitigated values for the number of FVGs chosen by the user.

The indicator also displays each New FVG as a bar representing the current ratio of the New FVG in relation to the current un-mitigated total for its direction.

🔶 USAGE

When an FVG forms, it is often interpreted as strong market sentiment in the direction of the gap. For example, an upward FVG during an uptrend is typically seen as a confirmation of the strength and continuation of the trend, as it indicates that buyers are willing to purchase at higher prices without much resistance, suggesting strong demand and positive sentiment.

By analyzing the mitigation (or lack thereof), we can visualize the increase of directional strength in a trend. This is where the proposed oscillator is useful.

🔶 DETAILS

The oscillator's values are expressed as Percentages (%). Each FVG is allocated 100% of the total of its width with a max potential value of 100 and minimum potential value of 0.

Based on the "FVG Lookback" Input, the FVGs are scaled to fit within the range of +1 to -1. Using a higher "FVG Lookback" value will allow you to get indications of longer-term trends.

A higher value of the normalized bullish FVG areas suggest a stronger and cleaner uptrend, while lower values of the bearish the normalized bullish FVG areas suggest a stronger and cleaner downtrend.

+1 or -1 indicates that there is a Full Lookback of FVGs, and each one is fully un-mitigated, and the opposite direction of FVGs is entirely Mitigated.

When the price closes over/under or within an FVG it begins to get mitigated, when this happens the % of mitigation is subtracted from the total.

When a New FVG is formed, a Histogram bar is created representing the ratio of the current FVG's width to the total width off all un-mitigated FVGs.

The entire bar represents 100% of total un-mitigated FVG Width.

The filled area represents the current FVG's width relative to the whole.

A 50% hash mark is also displayed for reference.

🔶 SETTINGS

FVG Lookback - Determines the number of FVGs (Bullish and Bearish Pairs) to keep in memory for analysis.

MACD by Take and TradeImproved version of MACD with asymmetrical BUY and SELL approaches.

This indicator is based on popular MACD one, but with some "tricks" designed to make it more applicable to the rapidly changing crypto market.

Key benefits:

Dynamic auto-adjusted threshold to filter out weak signals

Highlighted BUY/SELL signals with divergence (if a signal is accompanied by divergence, for example, price makes a new high while macd has a second high below the first, this signal is considered stronger and will be highlighted in a darker color)

Boost BUY signals on very slow market in accumulation phase

Not symmetric! It uses 2 different signal lines, which allows to obtain SELL signals earlier comparing to classic MACD approach

Classic concept of MACD

Classic MACD, in its simplest case, consists of two lines - macd line and signal line. Macd line is a difference between so-called "fast" and "slow" EMA lines (there are just a Exponential Moving Average lines with different windows: "12" for fast and "26" for slow). Signal line is just a smoothed "macd" line.

When macd line crosses signal line from bottom to up and intersection point < 0, this is "BUY" signal. And vise versa, when macd line crosses signal line from top to bottom, and intersection point > 0, this is "SELL" signal.

Parameters used in default configuration of classic MACD indicator:

Fast line: EMA-12

Slow line: EMA-26

Signal line: EMA-9

Problem of classic concept

Classic MACD indicator usually gives not bad "BUY" signals, especially if using them not for operational trading but for "investment" strategy. But "SELL" signalls usually generated too late. Simply because the market tends to fall much faster than it rises.

Possible solution (the main feature of our version of MACD)

To make indicator react faster on SELL condition, while still keeping it reliable for BUY signals, we decided to use two signal lines . Faster than default signal line (with window=6) for BUY signals and much faster than default (with window=2) for SELL signals.

This approach allowed us to receive sell signals earlier and exit deals on more favorable prices. Trade off of this change - is the number of SELL signals - there were more of them. However, this does not matter, since we receive the very first sell signal with a "very fast signal line" much earlier than with classic indicator settings.

Parameters we use in our improved MACD indicator:

Fast line: EMA-12

Slow line: EMA-24

Faster signal line: EMA-6

Much faster signal line: EMA-2

Removing noise (false triggerings)

Other drawback of classic MACD - it generates a lot of "weak" (false) signals. This signals are generated when macd crosses signal line much close to zero-line. And usually there are a lot of such intersections.

To remove this kind of noise, we added a trigger threshold, which by default is equal to 2.5% of the average asset price over a long period of time. Due to the link to the average price, this threshold automatically takes a specific value for each trading pair. Threshold 2.5% works perfect for all trading pairs for 1D timeframe. For other timeframes user can (and maybe will want) change it.

Boost weak BUY signals in a prolonged bear market

Signals on bearish stage are usually very weak, because there is no volatility, and no price impulse. And such signals will be filtered out as "noise" - see above. But this time is perfect time to buy! Therefore, we further boost the buy signals in a prolonged bear market so that they can pass through the filter and appear on the chart. Bearish period is the best time to invest!

Developed by Take and Trade. Enjoy using it!

Cycle Oscillator V2 [OmegaTools]Introducing the "Cycle Oscillator" by OmegaTools, an innovative addition to your TradingView analysis toolkit. This script is designed to offer a unique approach to understanding market cycles without the need for volume data, making it versatile across various market conditions and asset classes.

Key Features:

- Cycle Length Customization: Tailor the cycle length from 10 to 200 bars to fit the specific rhythm of the market you're analyzing, ensuring relevance and precision.

- Smoothness Adjustment: Fine-tune the oscillator's smoothness to capture the essence of market movements with options ranging from 1 to 20.

- Aesthetic Flexibility: Choose your preferred colors for the oscillator's upward and downward movements, personalizing your chart to your liking.

- Historical Mode: Toggle the historical mode to either focus on real-time analysis or review past cycle data for backtesting and study.

- Candle Color Modes: Enhance your visual analysis with optional candle coloring based on trend, signals, or extensions, providing immediate insight into market conditions.

Usage Guide:

1. Setting Up: Easily adjust the cycle length and smoothness to match the market's current volatility and your trading style.

2. Understanding Market Cycles: The oscillator plots the average deviation from three distinct moving averages, offering a clear view of potential market turns or continuations.

3. Identifying Overbought/Oversold Conditions: Utilize the upper and lower bounds to recognize extreme market conditions, guiding your entry and exit decisions.

4. Visual Enhancements: Customize the visual aspects, including colors and candle coloring, to make your analysis both effective and aesthetically pleasing.

5. Anticipating Market Movements: The script provides forward-looking lines to suggest potential future highs or lows, aiding in predictive analysis.

Designed with both novice and experienced traders in mind, the "Cycle Oscillator" is a testament to OmegaTools' commitment to providing high-quality, innovative trading tools. Whether you're looking to refine your trading strategy or seeking new analytical perspectives, this script offers a comprehensive solution to navigating the ebbs and flows of the financial markets.

Join the community of traders enhancing their TradingView experience with the "Cycle Oscillator" by OmegaTools. Start exploring deeper market insights and unlock new trading opportunities today.

Reversal Zones [UAlgo]🔶Description:

"Reversal Zones " aims to identify potential reversal zones in price movements. The indicator provides visual signals on the chart, indicating potential overbought and oversold conditions based on the calculated values. It offers traders insights into possible turning points in the market, aiding in decision-making processes regarding entry and exit points.

🔶Key Features:

Bollinger Bands Percentile (BB Percentile):

Bollinger Bands Percentile is utilized in this script to gauge the current price position relative to its recent volatility. By calculating the percentile rank of the current price within the Bollinger Bands, traders can identify extreme price levels. This assists in recognizing potential overbought or oversold conditions, where price may be due for a reversal.

Choppiness Index (CI):

The Choppiness Index is employed here to measure the market's trendiness or choppiness. By evaluating the efficiency of the price movement, CI helps traders determine whether the market is trending or consolidating.

Commodity Channel Index (CCI):

The Commodity Channel Index is integrated into this script to capture price momentum. CCI quantifies the relationship between the current price, a moving average, and standard deviation. Traders use CCI to identify overbought or oversold conditions and potential trend reversals.

By averaging and smoothing these values, traders can obtain a clearer picture of potential turning points in the market. The final smoothed combination signal aims to reduce noise and provide more reliable insights.

🔶Disclaimer:

Please note that this script is provided for informational and educational purposes only and should not be considered as financial advice.

Trading in financial markets involves risk, and past performance is not necessarily indicative of future results.

Users should conduct their own research and analysis or consult with a qualified financial advisor before making any investment decisions based on this indicator.

The creators of this script are not liable for any losses incurred from trading activities.

Shadow Range IndexShadow Range Index (SRI) introduces a new concept to calculate momentum, shadow range.

What is range?

Traditionally, True Range (TR) is the current high minus the current low of each bar in the timeframe. This is often used successfully on its own in indicators, or as a moving average in ATR (Average True Range).

To calculate range, SRI uses an innovative calculation of current bar range that also considers the previous bar. It calculates the difference between its maximum upward and maximum downward values over the number of bars the user chooses (by adjusting ‘Range lookback’).

What is shadow range?

True Range (TR) uses elements in its calculation (the highs and lows of the bar) that are also visible on the chart bars. Shadow range does not, though.

SRI calculates shadow range in a similar formula to range, except that this time it works out the difference between the minimum upward and minimum downward movement. This movement is by its nature less than the maximums, hence a shadow of it. Although more subtle, shadow range is significant, because it is quantifiable, and goes in one direction or another.

Finally, SRI smoothes shadow range and plots it as a histogram, and also smoothes and plots range as a signal line. Useful up and down triangles show trend changes, which optionally colour the chart bars.

Here’s an example of a long trade setup:

In summary, Shadow Range Index identifies and traces maximum and minimum bar range movement both up and down, and plots them as centred oscillators. The dynamics between the two can provide insights into the chart's performance and future direction.

Credit to these authors, whose MA or filters form part of this script:

@balipour - Super Smoother MA

@cheatcountry - Hann window smoothing

@AlgoAlpha - Gaussian filter

MACD / Connectable [Azullian]Enhance your market insight with the MACD indicator. Monitor momentum to make more informed trading decisions, facilitating the development of stronger strategies.

This connectable MACD indicator is part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

█ UNIFORM SETTINGS AND A WAY OF WORK

Although connectable indicators may have specific weight scoring conditions, they all aim to follow a standardized general approach to weight scoring settings, as outlined below.

■ Connectable indicators - Settings

• 🗲 Energy: Energy applies an ATR multiplier to the plotted shapes on the chart. A higher value plots shapes farther away from the candle, enhancing visibility.

• ☼ Brightness: Brightness determines the opacity of the shape plotted on the chart, aiding visibility. Indicator weight also influences opacity.

• → Input: Use the input setting to specify a data source for the indicator. Here you can connect the indicator to other indicators.

• ⌥ Flow: Determine where you want to receive signals from:

○ Both: Weights from this indicator and the connected indicator will apply

○ Indicator only: Only weights from this indicator will apply

○ Input only: Only weights from the connected indicator will apply

• ⥅ Weight multiplier: Multiply all weights in the entire indicator by a given factor, useful for quickly testing different indicators in a granular setup.

• ⥇ Threshold: Set a threshold to indicate the minimum amount of weight it should receive to pass it through to the next indicator.

• ⥱ Limiter: Set a hard limit to the maximum amount of weight that can be fed through the indicator.

■ Connectable indicators - Weight scoring settings

▢ Weight scoring conditions

• SM – Signal mode: Enable specific conditions for weight scoring

○ All: All signals will be scored.

○ Entries only: Only entries will score.

○ Exits only: Only exits will score.

○ Entries & exits: Both entries and exits will score.

○ Zone: Continuous scoring for each candle within the zone.

• SP – Signal period: Defines a range of candles within which a signal can score.

• SC - Signal count: Specifies the number of bars to retrospectively examine and score.

○ Single: Score for a single occurrence

○ All occurrences: Score for all occurrences

○ Single + Threshold: Score for single occurrences within the signal period (SP)

○ Every + Threshold: Score for all occurrences within the signal period (SP)

▢ Weight scoring direction

• ES: Enter Short weight

• XL: Exit long weight

• EL: Enter Long weight

• XS: Exit Short weight

▢ Weight scoring values

• Weights can hold either positive or negative scores. Positive weights enhance a particular trading direction, while negative weights diminish it.

█ MACD - INDICATOR SETTINGS

■ Main settings

• Enable/Disable Indicator: Toggle the entire indicator on or off.

• S - Source: Choose an alternative data source for the MACD calculation.

• T - Timeframe: Select an alternative timeframe for the MACD calculation.

• FL - Fast Length: Define the number of bars or periods used in the MACD calculation for the fast length.

• SL - Fast Length: Define the number of bars or periods used in the MACD calculation for the slow length.

• SM - Smoothing: Smooths the averaged MACD over a specified period.

• C - Condition Define the smoothing amount

○ Above/Below zero: : Trigger when the MACD line is above or below zero

○ All: : Trigger on all conditions

■ MACD Scoring functionality

• The MACD scores long entries when it crosses above its smoothed value and is below the zero line.

• The MACD scores long exits when it crosses below its smoothed value after a long entry.

• The MACD scores long zones the entire time the MACD line is above its smoothed value and below zero.

• The MACD scores short entries when it crosses below its smoothed value and is above the zero line.

• The MACD scores short exits when it crosses above its smoothed value after a short entry.

• The MACD scores short zones the entire time the MACD line is below its smoothed value and above zero.

█ PLOTTING

• Standard: Symbols (EL, XS, ES, XL) appear relative to candles based on set conditions. Their opacity and position vary with weight.

• Conditional Settings: A larger icon appears if global conditions are met. For instance, with a Threshold(⥇) of 12, Signal Period (SP) of 3, and Scoring Condition (SC) set to "EVERY", an MACD signaling over two times in 3 candles (scoring 6 each) triggers a larger icon.

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with a signal filter and strategy

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, monitor, or strategy .

Let's connect the MACD to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load MACD / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the MACD to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : MACD / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

CCI / Connectable [Azullian]Sharpen your analysis of market trends with the CCI indicator. Effectively evaluate market cycles and identify potential reversals, enriching your strategic planning.

This connectable CCI indicator is part of an indicator system designed to help test, visualize and build strategy configurations without coding. Like all connectable indicators , it interacts through the TradingView input source, which serves as a signal connector to link indicators to each other. All connectable indicators send signal weight to the next node in the system until it reaches either a connectable signal monitor, signal filter and/or strategy.

█ UNIFORM SETTINGS AND A WAY OF WORK

Although connectable indicators may have specific weight scoring conditions, they all aim to follow a standardized general approach to weight scoring settings, as outlined below.

■ Connectable indicators - Settings

• 🗲 Energy: Energy applies an ATR multiplier to the plotted shapes on the chart. A higher value plots shapes farther away from the candle, enhancing visibility.

• ☼ Brightness: Brightness determines the opacity of the shape plotted on the chart, aiding visibility. Indicator weight also influences opacity.

• → Input: Use the input setting to specify a data source for the indicator. Here you can connect the indicator to other indicators.

• ⌥ Flow: Determine where you want to receive signals from:

○ Both: Weights from this indicator and the connected indicator will apply

○ Indicator only: Only weights from this indicator will apply

○ Input only: Only weights from the connected indicator will apply

• ⥅ Weight multiplier: Multiply all weights in the entire indicator by a given factor, useful for quickly testing different indicators in a granular setup.

• ⥇ Threshold: Set a threshold to indicate the minimum amount of weight it should receive to pass it through to the next indicator.

• ⥱ Limiter: Set a hard limit to the maximum amount of weight that can be fed through the indicator.

■ Connectable indicators - Weight scoring settings

▢ Weight scoring conditions

• SM – Signal mode: Enable specific conditions for weight scoring

○ All: All signals will be scored.

○ Entries only: Only entries will score.

○ Exits only: Only exits will score.

○ Entries & exits: Both entries and exits will score.

○ Zone: Continuous scoring for each candle within the zone.

• SP – Signal period: Defines a range of candles within which a signal can score.

• SC - Signal count: Specifies the number of bars to retrospectively examine and score.

○ Single: Score for a single occurrence

○ All occurrences: Score for all occurrences

○ Single + Threshold: Score for single occurrences within the signal period (SP)

○ Every + Threshold: Score for all occurrences within the signal period (SP)

▢ Weight scoring direction

• ES: Enter Short weight

• XL: Exit long weight

• EL: Enter Long weight

• XS: Exit Short weight

▢ Weight scoring values

• Weights can hold either positive or negative scores. Positive weights enhance a particular trading direction, while negative weights diminish it.

█ CCI - INDICATOR SETTINGS

■ Main settings

• Enable/Disable Indicator: Toggle the entire indicator on or off.

• S - Source: Choose an alternative data source for the CCI calculation.

• T - Timeframe: Select an alternative timeframe for the CCI calculation.

• LE - Length: Define the number of bars or periods used in the CCI calculation.

• OB - Overbought Level: Determine the CCI value at which overbought conditions are met.

• OS - Oversold Level: Specify the CCI value at which oversold conditions are met.

■ Scoring functionality

• The CCI scores long entries when the CCI enters OS: oversold area

• The CCI scores long exits when the CCI exits OS: oversold area

• The CCI scores long zones the entire time the CCI is in OS: oversold area

• The CCI scores short entries when the CCI enters OB: overbought area

• The CCI scores short exits when the CCI exits OB: overbought area

• The CCI scores short zones the entire time the CCI is in OB: overbought area

█ PLOTTING

• Standard: Symbols (EL, XS, ES, XL) appear relative to candles based on set conditions. Their opacity and position vary with weight.

• Conditional Settings: A larger icon appears if global conditions are met. For instance, with a Threshold(⥇) of 12, Signal Period (SP) of 3, and Scoring Condition (SC) set to "EVERY", an CCI signaling over two times in 3 candles (scoring 6 each) triggers a larger icon.

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with a signal filter and strategy

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, monitor, or strategy .

Let's connect the CCI to a connectable signal filter and a strategy :

1. Load all relevant indicators

• Load CCI / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the CCI to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : CCI / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select a strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

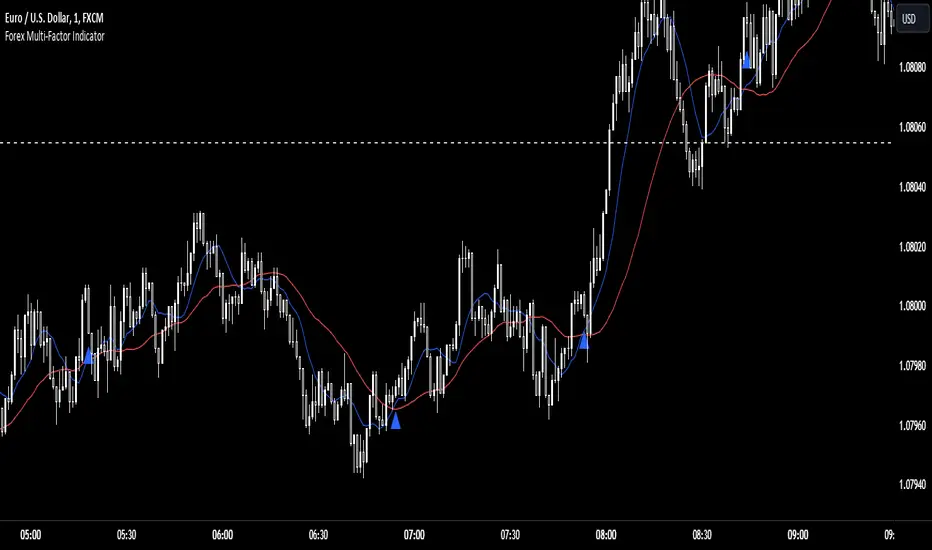

Forex Multi-Factor IndicatorMoving Averages (MA):

Two moving averages are plotted on the chart: a fast MA (blue line) and a slow MA (red line).

The fast MA is calculated using a shorter period (10 periods by default), while the slow MA is calculated using a longer period (30 periods by default).

Moving averages help identify trends by smoothing out price fluctuations. When the fast MA crosses above the slow MA, it suggests a bullish trend, and when the fast MA crosses below the slow MA, it suggests a bearish trend.

Relative Strength Index (RSI):

The RSI indicator (orange line) is plotted on a separate axis.

RSI measures the speed and change of price movements and oscillates between 0 and 100.

RSI values above 70 are considered overbought, indicating a potential reversal to the downside, while RSI values below 30 are considered oversold, indicating a potential reversal to the upside.

Volume Moving Average (Volume MA):

The volume moving average (purple line) is plotted on the same axis as the volume.

The volume moving average is calculated over a specified period (20 periods by default).

Volume analysis provides insights into the strength of price movements. When the volume increases along with price movements, it suggests strong conviction from traders.

Buy and Sell Signals:

Buy signals (green triangle) are generated when all of the following conditions are met:

The fast MA crosses above the slow MA (indicating a bullish trend).

The RSI is below the oversold level (indicating potential upward momentum).

The current price is above the fast MA, and the volume is higher than the volume MA (indicating positive volume trend).

Sell signals (red triangle) are generated when all of the following conditions are met:

The fast MA crosses below the slow MA (indicating a bearish trend).

The RSI is above the overbought level (indicating potential downward momentum).

The current price is below the fast MA, and the volume is lower than the volume MA (indicating negative volume trend).

Overall, this multi-factor indicator combines moving averages, RSI, and volume analysis to identify potential buying and selling opportunities in the Forex market. Traders can use the signals generated by this indicator as part of their trading strategy, but it's important to consider other factors such as risk management and market conditions before making trading decisions

CBO (Candle Bias Oscillator)The Candle Bias Oscillator (CBO) with volume and ATR scaling is a unique technical analysis tool designed to capture market sentiment through the analysis of candlestick patterns, volume momentum, and market volatility. This indicator is built on the foundation of assessing the bias within a candlestick's body and wicks, adjusted for market volatility using the Average True Range (ATR), and further refined by comparing the Rate of Change (ROC) in volume and the adjusted bias. The culmination of these calculations results in the CBO, a smoothed oscillator that highlights potential market turning points through divergence analysis.

Key Features:

Bias Calculations: Utilizes the relationship between the candle's body and wicks to determine the market's immediate bias, offering a nuanced view beyond simple price action. Have you ever wanted to quantify exactly how bullish or bearish a particular candle or candlestick pattern is? Whether it's dojis, hammers, engulfing, gravestones, evening morning star, three soldiers etc. you don't have to memorize 50 candlestick patterns anymore.

Volatility Adjustment: Employs the ATR to adjust the bias calculation, ensuring the oscillator remains relevant across varying market conditions by accounting for volatility.

Momentum and Divergence: Measures the momentum in volume and bias through ROC calculations, identifying divergence that may signal reversals or significant price movements.

Signal Line: A smoothed version of the CBO, derived from its own values, serving as a benchmark for identifying potential crossovers and divergences.

Utility and Application:

The CBO with Divergence Scaling is developed for traders who seek a deeper understanding of market dynamics beyond price movements alone. It is particularly useful for identifying potential reversals or continuation patterns early, by highlighting divergence between market sentiment (as expressed through candlestick bias) and actual volume movements. In this way, it aligns us retail traders with institutional traders and smart money. This indicator is versatile and can be applied across various time frames and market instruments, offering value to both short-term traders and long-term investors.

How to Use:

Trend Identification: The direction and value of the CBO provide insights into the prevailing market trend. A positive oscillator value may indicate bullish sentiment, while a negative value suggests bearish sentiment.

Signal Line Crossovers: Crossovers between the CBO and its signal line can be used as potential buy or sell signals. A crossover above the signal line might indicate a buying opportunity, whereas a crossover below could suggest a selling point.

Divergence: Discrepancies between the CBO and price action (especially when confirmed by volume ROC) can highlight potential reversals.

Customization and Parameters: This script allows users to adjust several parameters, including oscillator periods, signal line periods, ATR periods, and ROC periods for divergence, to best fit their trading strategy and the characteristics of the market they are analyzing.

Conclusion:

The Custom Bias Oscillator with Divergence Scaling is a comprehensive tool designed to offer traders a multi-faceted view of market conditions, combining elements of price action, volatility, and momentum. By integrating these aspects into a single indicator, it aims to provide a more rounded and actionable insight into market trends and potential turning points.

To comply with best practices and ensure clarity regarding the informational nature of the Custom Bias Oscillator (CBO) tool, it's crucial to include a disclaimer about the non-advisory nature of the script. Here's a suitable disclaimer that you can add to the end of your script description or publication:

Disclaimer:

The Custom Bias Oscillator (CBO) with Divergence Scaling and its accompanying analysis are provided as tools for educational and informational purposes only and should not be construed as financial advice. The creator of this indicator does not guarantee any specific outcomes or profit, and all users should be aware of the risks involved in trading and investing. Users should conduct their own research and consult with a professional financial advisor before making any investment decisions. The use of this indicator is at the user's own risk, and the creator bears no responsibility for any direct or consequential loss arising from any use of this tool or the information provided herein.

Donchian Channel Trend MeterInspired by the Chande Trend Meter (this is not the Chande Trend Meter), this indicator aims to show the trend so you can make trading decisions accordingly. This is calculated by looking at Donchian Channels over a number of lengths (20, 40, 60 periods, etc.), converting them to percent, and then applying a weighting and smoothing similar to the Know Sure Thing Indicator. This results in smooth trend line that is not disturbed by large fluctuations in price action.

When the line is below 20%, you have a strong down trend. Values between 20 - 40% are a weak down trend. Values between 40 - 60% are no trend (slightly bullish or bearish if above or below 50%). Similarly, 60 - 80% is a weak uptrend, and above 80% is a strong uptrend. Trade signals can be turned on or off that correspond to crosses over 50%. It can be useful in spotting divergence.

Adaptive Fisherized Z-scoreHello Fellas,

It's time for a new adaptive fisherized indicator of me, where I apply adaptive length and more on a classic indicator.

Today, I chose the Z-score, also called standard score, as indicator of interest.

Special Features

Advanced Smoothing: JMA, T3, Hann Window and Super Smoother

Adaptive Length Algorithms: In-Phase Quadrature, Homodyne Discriminator, Median and Hilbert Transform

Inverse Fisher Transform (IFT)

Signals: Enter Long, Enter Short, Exit Long and Exit Short

Bar Coloring: Presents the trade state as bar colors

Band Levels: Changes the band levels

Decision Making

When you create such a mod you need to think about which concepts are the best to conclude. I decided to take Inverse Fisher Transform instead of normalization to make a version which fits to a fixed scale to avoid the usual distortion created by normalization.

Moreover, I chose JMA, T3, Hann Window and Super Smoother, because JMA and T3 are the bleeding-edge MA's at the moment with the best balance of lag and responsiveness. Additionally, I chose Hann Window and Super Smoother because of their extraordinary smoothing capabilities and because Ehlers favours them.

Furthermore, I decided to choose the half length of the dominant cycle instead of the full dominant cycle to make the indicator more responsive which is very important for a signal emitter like Z-score. Signal emitters always need to be faster or have the same speed as the filters they are combined with.

Usage

The Z-score is a low timeframe scalper which works best during choppy/ranging phases. The direction you should trade is determined by the last trend change. E.g. when the last trend change was from bearish market to bullish market and you are now in a choppy/ranging phase confirmed by e.g. Chop Zone or KAMA slope you want to do long trades.

Interpretation

The Z-score indicator is a momentum indicator which shows the number of standard deviations by which the value of a raw score (price/source) is above or below the mean value of what is being observed or measured. Easily explained, it is almost the same as Bollinger Bands with another visual representation form.

Signals

B -> Buy -> Z-score crosses above lower band

S -> Short -> Z-score crosses below upper band

BE -> Buy Exit -> Z-score crosses above 0

SE -> Sell Exit -> Z-score crosses below 0

If you were reading till here, thank you already. Now, follows a bunch of knowledge for people who don't know the concepts I talk about.

T3

The T3 moving average, short for "Tim Tillson's Triple Exponential Moving Average," is a technical indicator used in financial markets and technical analysis to smooth out price data over a specific period. It was developed by Tim Tillson, a software project manager at Hewlett-Packard, with expertise in Mathematics and Computer Science.

The T3 moving average is an enhancement of the traditional Exponential Moving Average (EMA) and aims to overcome some of its limitations. The primary goal of the T3 moving average is to provide a smoother representation of price trends while minimizing lag compared to other moving averages like Simple Moving Average (SMA), Weighted Moving Average (WMA), or EMA.

To compute the T3 moving average, it involves a triple smoothing process using exponential moving averages. Here's how it works:

Calculate the first exponential moving average (EMA1) of the price data over a specific period 'n.'

Calculate the second exponential moving average (EMA2) of EMA1 using the same period 'n.'

Calculate the third exponential moving average (EMA3) of EMA2 using the same period 'n.'

The formula for the T3 moving average is as follows:

T3 = 3 * (EMA1) - 3 * (EMA2) + (EMA3)

By applying this triple smoothing process, the T3 moving average is intended to offer reduced noise and improved responsiveness to price trends. It achieves this by incorporating multiple time frames of the exponential moving averages, resulting in a more accurate representation of the underlying price action.

JMA

The Jurik Moving Average (JMA) is a technical indicator used in trading to predict price direction. Developed by Mark Jurik, it’s a type of weighted moving average that gives more weight to recent market data rather than past historical data.

JMA is known for its superior noise elimination. It’s a causal, nonlinear, and adaptive filter, meaning it responds to changes in price action without introducing unnecessary lag. This makes JMA a world-class moving average that tracks and smooths price charts or any market-related time series with surprising agility.

In comparison to other moving averages, such as the Exponential Moving Average (EMA), JMA is known to track fast price movement more accurately. This allows traders to apply their strategies to a more accurate picture of price action.

Inverse Fisher Transform

The Inverse Fisher Transform is a transform used in DSP to alter the Probability Distribution Function (PDF) of a signal or in our case of indicators.

The result of using the Inverse Fisher Transform is that the output has a very high probability of being either +1 or –1. This bipolar probability distribution makes the Inverse Fisher Transform ideal for generating an indicator that provides clear buy and sell signals.

Hann Window

The Hann function (aka Hann Window) is named after the Austrian meteorologist Julius von Hann. It is a window function used to perform Hann smoothing.

Super Smoother

The Super Smoother uses a special mathematical process for the smoothing of data points.

The Super Smoother is a technical analysis indicator designed to be smoother and with less lag than a traditional moving average.

Adaptive Length

Length based on the dominant cycle length measured by a "dominant cycle measurement" algorithm.

Happy Trading!

Best regards,

simwai

---

Credits to

@cheatcountry

@everget

@loxx

@DasanC

@blackcat1402

ML - Momentum Index (Pivots)Building upon the innovative foundations laid by Zeiierman's Machine Learning Momentum Index (MLMI), this variation introduces a series of refinements and new features aimed at bolstering the model's predictive accuracy and responsiveness. Licensed under the Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License (CC BY-NC-SA 4.0), my adaptation seeks to enhance the original by offering a more nuanced approach to momentum-based trading.

Key Features :

Pivot-Based Analysis: Shifting focus from trend crosses to pivot points, this version employs pivot bars to offer a distinct perspective on market momentum, aiding in the identification of critical reversal points.

Extended Parameter Set: By integrating additional parameters for making predictions, the model gains improved adaptability, allowing for finer tuning to match market conditions.

Dataset Size Limitation: To ensure efficiency and mitigate the risk of calculation timeouts, a cap on the dataset size has been implemented, balancing between comprehensive historical analysis and computational agility.

Enhanced Price Source Flexibility: Users can select between closing prices or (suggested) OHLC4 as the basis for calculations, tailoring the indicator to different analysis preferences and strategies.

This adaptation not only inherits the robust framework of the original MLMI but also introduces innovations to enhance its utility in diverse trading scenarios. Whether you're looking to refine your short-term trading tactics or seeking stable indicators for long-term strategies, the ML - Momentum Index (Pivots) offers a versatile tool to navigate the complexities of the market.

For a deeper understanding of the modifications and to leverage the full potential of this indicator, users are encouraged to explore the tooltips and documentation provided within the script.

The Momentum Indicator calculations have been transitioned to the MLMomentumIndex library, simplifying the process of integration. Users can now seamlessly incorporate the momentumIndexPivots function into their scripts to conduct detailed momentum analysis with ease.

Relative Strength Scoring SystemRelative Strength Scoring System :

Important prerequisite :

This indicator can be loaded on any forex chart, i.e. a currency pair, but must not be loaded on any other asset due to certain market closures.

The chart timeframe must be less than or equal to the trading timeframe, which is the indicator's first parameter. A timeframe equal to that of the "Trading Timeframe" parameter is preferable.

Introduction :

This indicator measures the relative strength of a currency against all other currencies using spread formulas. It gives an indication of which currencies are bullish, neutral or bearish. The ultimate aim of this indicator is to find out which pair will generate a higher probability of gain than the others by pairing the most bullish pair with the most bearish pair.

Spread formulas :

To find the relative strength of a currency compared with others, we use the following spreads formulas :

USD = (FX:USDJPY/100+SAXO:USDEUR+FX:USDCHF+SAXO:USDGBP+FX:USDCAD+SAXO:USDAUD+FX_IDC:USDNZD)/7

JPY = (SAXO:JPYUSD/100+FX_IDC:JPYAUD/100+FX_IDC:JPYCAD/100+FX_IDC:JPYNZD/100+FX_IDC:JPYCHF/100+SAXO:JPYEUR/100+FX_IDC:JPYGBP/100)/7

CHF = (FX:CHFJPY/100+SAXO:CHFUSD+SAXO:CHFEUR+FX_IDC:CHFGBP+FX_IDC:CHFCAD+SAXO:CHFAUD+FX_IDC:CHFNZD)/7

EUR = (FX:EURJPY/100+FX:EURUSD+FX:EURCHF+FX:EURGBP+FX:EURCAD+FX:EURAUD+FX:EURNZD)/7

GBP = (FX:GBPJPY/100+FX:GBPUSD+FX:GBPCHF+SAXO:GBPEUR+FX:GBPCAD+FX:GBPAUD+FX:GBPNZD)/7

CAD = (FX:CADJPY/100+SAXO:CADUSD+FX:CADCHF+FX_IDC:CADGBP+SAXO:CADEUR+FX_IDC:CADAUD+FX_IDC:CADNZD)/7

AUD = (FX:AUDJPY/100+FX:AUDUSD+FX:AUDCHF+SAXO:AUDGBP+FX:AUDCAD+SAXO:AUDEUR+FX:AUDNZD)/7

NZD = (FX:NZDJPY/100+FX:NZDUSD+FX:NZDCHF+SAXO:NZDGBP+FX:NZDCAD+SAXO:NZDAUD+SAXO:NZDEUR)/7

CRYPTO = (BITSTAMP:BTCUSD+BITSTAMP:ETHUSD+BITSTAMP:LTCUSD+BITSTAMP:BCHUSD)/4

Timeframes :

As mentioned in the prerequisites, the chart timeframe must not be greater than the trading timeframe. The latter corresponds to the timeframe chosen by the trader to enter a position, and is the indicator's first parameter. Once this has been chosen, the algorithm selects the timeframes of the "Trend" and "Velocity" charts. Here's how it allocates them :

Trading TF => ("Velocity TF", "Trend TF")

"5min" => ("15min ", "60min")

"15min" => ("60min ", "4h")

"30min" => ("2h ", "8h")

"60min" => ("4h ", "12h")

"4h" => ("12h", "1D")

"6h" => ("1D", "3D")

"8h" => ("1D", "4D")

"12h" => ("2D", "1W")

"1D" => ("3D", "1W")

Trend Scoring System :

When the timeframe of the trend graph has been allocated, the algorithm will establish this graph's score using three criteria :

Trend chart pivot points: if the last two pivots, high and low, are increasing, the score is 1; if they are decreasing, the score is -1; else the score is 0.

SMA: if its slope is increasing with a candle strictly above the SMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

MACD: if the MACD is positive, the score is 1, if it is negative, the score is -1; else it's 0.

We then sum the scores of these three criteria to find the trend score.

Velocity Scoring System :

In the same way, we analyze the score of the "velocity" graph with its corresponding timeframe using three criteria :

The EMA: if its slope is increasing with a candle strictly above the EMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

The RSI: if the RSI's EMA has an increasing slope with an RSI strictly greater than the value of this EMA, the score is 1; and if the RSI's EMA has a decreasing slope with an RSI strictly less than this EMA, the score is -1; otherwise it is 0.

SAR parabolic: if the SAR is below the price, the score is 1; if it is above the price, the score is -1.

We then sum the scores of these three criteria to find the velocity score.

Relative Strength Scoring System :

Once the trend score and velocity score have been calculated, we determine the relative strength score of each currency using the following algorithm :

If trend score >=2 and velocity score >=2, the currency is bullish.

If trend score <=2 and velocity score <=2, currency is bearish

If (trendScore>=2 or velocityScore>=2) and (trendScore=1 or velocityScore=1) the currency is not yet bullish

If (trendScore<=2 or velocityScore<=2) and (trendScore=-1 or velocityScore=-1) the currency is not yet bearish.

Otherwise the currency is neutral

Parameters :

Trading Timeframe: the trading timeframe chosen by the trader for which he makes his position entry and exit decisions. Default is 1h

Pivot Legs: Parameter used for the chart "Trend" setting the pivot strength to the right and left of high/low. Default is 2

SMA Length: SMA length of the chart "Trend". Default is 20

MACD Fast Length: Length of the MACD fast SMA calculated on the chart "Trend". Default is 12

MACD Slow Length: Length of the MACD slow SMA calculated on the chart "Trend". Default is 26

MACD Signal Length: Length of the MACD signal SMA calculated on the chart "Trend". Default is 9

EMA Length: EMA length of the "Velocity" graph. Default is 13

RSI Length: RSI length of the "Velocity" graph. Default is 14

RSI EMA Length: Length of the RSI EMA. Default is 9

Parabolic SAR Start: Start of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Increment: Increment of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Max: Maximum of the SAR parabola in the "Velocity" graph. Default is 0.2

Conclusion :

This indicator has been designed to determine the relative strength of the major currencies against each other. The aim is to know which pair to trade at the right time in order to maximize the probability of a successful trade. For example, if the USD is bullish and the NZD bearish, we'll short the NZDUSD pair.

Enjoy this indicator and don't forget to take the trade ;)

F.B_Consolidation Range Identifier

The "F.B_Consolidation Range Identifier" (F.B_CRI) is an indicator aimed at identifying consolidation areas in the price chart. Here is an explanation of the logic and usage of this indicator:

Calculation of Standard Deviation

This indicator analyzes the market's volatility by considering the standard deviation of price movements over a defined period. A higher standard deviation indicates larger price movement, while a lower standard deviation suggests potential consolidation, where price movements are limited.

Derivation of Standard Deviation

To track changes in volatility, the derivative of the standard deviation is calculated. Positive derivative values indicate increasing volatility, while negative values suggest a decrease in volatility. This allows for the identification of potential consolidation phases where volatility decreases, and the market may stabilize.

Identification of Consolidation Phase

The indicator signals potential consolidation phases when the standard deviation is low and/or the derivative of the standard deviation is negative. To represent consolidation phases on the chart, the standard deviation line, background, and candles are colored red. However, it's important to note that the display is customizable and can be configured according to individual needs.

🚨 Important 🚨

The indicator only indicates whether consolidation phases exist. If the standard deviation line, background, or candles are gray, it indicates that a trend exists in general, but not whether it is bullish or bearish. It is advisable to use other analytical tools to confirm the direction of the trend.

Candlestick Bias OscillatorCandlestick Bias Oscillator (CBO)

The Candlestick Bias Oscillator (CBO) with Signal Line is a pioneering indicator developed for the TradingView platform, designed to offer traders a nuanced analysis of market sentiment through the unique lens of candlestick patterns. This indicator stands out by merging traditional concepts of price action analysis with innovative mathematical computations, providing a fresh perspective on trend detection and potential market reversals.

Originality and Utility

At the core of the CBO's originality is its method of calculating the bias of candlesticks. Unlike conventional oscillators that may rely solely on closing prices or high-low ranges, the CBO incorporates both the body and wick of candlesticks into its analysis. This dual consideration allows for a more rounded understanding of market sentiment, capturing both the directional momentum and the strength of price rejections within a single oscillator.

Mathematical Foundations

1. Body Bias: The CBO calculates the body bias by assessing the relative position of the close to the open within the day's range, scaled to a -100 to 100 range. This calculation reflects the bullish or bearish sentiment of the market, based on the day's closing momentum.

Body Bias = (Close−Open)/(High−Low) x 100

Wick Bias: Similarly, the wick bias calculation takes into account the lengths of the upper and lower wicks, indicating rejection levels beyond the body's close. The balance between these wicks is scaled similarly to the body bias, offering insight into the market's indecision or rejection of certain price levels.

Wick Bias=(Lower Wick−Upper Wick)/(Total Wick Length) × 100

3. Overall Bias and Oscillator: By averaging the body and wick biases, the CBO yields an overall bias score, which is then smoothed over a user-defined period to create the oscillator. This oscillator provides a clear visual representation of the market's underlying sentiment, smoothed to filter out the noise.

4. Signal Line: A secondary smoothing of the oscillator creates the signal line, offering a trigger for potential trading signals when the oscillator crosses this line, indicative of a change in market momentum.

How to Use the CBO:

The CBO is versatile, suitable for various trading strategies, including scalping, swing trading, and long-term trend following. Traders can use the oscillator and signal line crossovers as indications for entry or exit points. The relative position of the oscillator to the zero line further provides insight into the prevailing market bias, enabling traders to align their strategies with the broader market sentiment.

Why It Adds Value:

The CBO's innovative approach to analyzing candlestick patterns fills a gap in the existing array of TradingView indicators. By providing a detailed analysis of both candle bodies and wicks, the CBO offers a more comprehensive view of market sentiment than traditional oscillators. This can be particularly useful for traders looking to gauge the strength of price movements and potential reversal points with greater precision.

Conclusion: