[blackcat] L2 Double EMA Convergence and Diverence (DEMACD)Introduction:

The " L2 Double EMA Convergence and Divergence (DEMACD)" is a custom technical indicator designed for use in TradingView. It's based on the concept of Double Exponential Moving Averages (DEMA) and incorporates elements from the well-known Moving Average Convergence Divergence (MACD). This guide aims to provide an understanding of its definition, history, calculation, operations, usage, input settings, and style.

1. Definition:

The DEMACD indicator is designed to detect changes in price trends using a modified approach of the traditional MACD, with a focus on reducing lag. It does this by comparing two DEMAs of different lengths, providing traders with signals of converging and diverging trends.

2. History:

The concept of DEMA was introduced by Patrick Mulloy in 1994 to reduce the lag inherent in traditional EMAs. MACD, developed by Gerald Appel in the 1970s, is a trend-following momentum indicator that shows the relationship between two moving averages of a security's price. The DEMACD combines the quick response feature of DEMA with the reliable trend analysis of MACD.

3. Calculation Method:

DEMACD is calculated through several steps:

Smoothed price S is first computed as (3 * close + high + low + open) / 6.

DAYLINE is calculated as 2 * EMA(S, len_ema) - EMA(EMA(S, 5), len_ema).

The mainTrendLine is the EMA of the EMA of the closing price over len_dema periods.

DIF is the difference between the DAYLINE and mainTrendLine.

DEA is the EMA of DIF over len_smooth periods.

Finally, DEMACD is calculated as (DIF - DEA) * 2.

4. Basic Operations and Comparison with MACD:

DEMACD's key feature is its reduced lag compared to the traditional MACD. While MACD uses EMA, DEMACD uses DEMA, providing a faster and more accurate response to price changes. This makes it particularly useful in volatile market conditions where traditional MACD may lag.

5. Usage:

Similar to MACD, DEMACD is used for trend confirmation, crossover signals, and divergences:

Trend confirmation is observed when the DIF line is above or below the DEA line.

Crossover signals are generated when the DIF line crosses the DEA line.

Divergences between the DEMACD and price action can signal potential trend reversals.

6. Input Settings:

Users can configure the following settings in TradingView:

len_ema: Length of the EMA for DAYLINE.

len_dema: Length of the EMA for the main trend line.

len_smooth: Smoothing length for DEA.

Adjusting these settings allows traders to tailor the indicator to different trading styles and market conditions.

7. Style:

The DEMACD in TradingView is represented with different colors and line thicknesses:

DIF is plotted in red with a line thickness of 2.

DEA is plotted in gray, also with a line thickness of 2.

DEMACD histogram changes color based on its value relative to its previous value and zero.

Conclusion:

The " L2 Double EMA Convergence and Divergence (DEMACD)" is a versatile indicator that combines the rapid response of DEMA with the trend-following abilities of MACD. Its reduced lag makes it a valuable tool for traders looking for timely market signals. Proper understanding and application of its settings can enhance its effectiveness in various trading strategies.

Centered Oscillators

Monitor XThe Monitor X Indicator is a dynamic tool designed for any trading symbol, providing a quick and intuitive snapshot of price action relative to the latest closing level. With a user-friendly interface, this indicator allows traders to effortlessly gauge price movement and key levels.

Key Features:

1. Symbol Agnosticism:

Universally applicable to any trading symbol, the Monitor X Indicator ensures versatility and adaptability across various financial instruments.

2. Instant Price Insight:

Obtain immediate clarity on current market dynamics with a single glance. The indicator prominently displays the price line, facilitating swift analysis.

3. Last Close Comparison:

Easily assess the price's relationship to the most recent closing level. This feature provides valuable context for understanding market sentiment and potential support/resistance areas.

4. Customizable Display:

Tailor the indicator to your preferences with adjustable settings for line color, width, and opacity. This customization empowers traders to align the indicator with their unique trading strategies.

5. Intuitive Interface:

The clean and intuitive interface ensures a seamless user experience. Access crucial information effortlessly, allowing for quick decision-making.

How to Use:

1. Symbol Selection:

Apply the Monitor X Indicator to any trading symbol of your choice, ensuring a versatile tool for your entire portfolio.

2. Last Close Analysis:

Quickly assess how the current price relates to the previous close. This instant comparison aids in identifying potential entry and exit points.

3. Customization for Precision:

Fine-tune the indicator's appearance to suit your preferences. Adjust line colors, widths, and opacity settings for a personalized and efficient trading experience.

4. Swift Decision-Making:

Utilize the Monitor X Indicator for rapid decision-making. Gain insights into market movements at a glance, allowing you to stay ahead in dynamic trading environments.

Instant MACD (IMACD)The "Instant MACD" is a tailored version of the traditional Moving Average Convergence Divergence indicator, specifically designed to begin plotting with minimal data, such as in cases of high timeframe charts or newly listed trading instruments. Unlike the standard MACD that requires a substantial amount of data to provide accurate readings, the Instant MACD can deliver insights with as few as two candlesticks.

This iteration of the MACD utilizes the Chebyshev filter for the computation of both the fast and slow moving averages as well as for the signal line. The Chebyshev filter is known for its effectiveness in smoothing data series and reducing ripple effects, which is particularly advantageous when working with limited datasets.

The Instant MACD comprises several components. The histogram, which illustrates the difference between the MACD line and the signal line, adjusts its color based on the directional momentum; it transitions between shades of green and red as the histogram moves above or below the zero line and increases or decreases in value. The MACD line, depicted in blue, represents the disparity between the fast and slow Chebyshev moving averages. Complementing it is the signal line in orange, which is a Chebyshev-filtered mean of the MACD line and serves as an indicator of potential momentum shifts.

Additionally, the indicator includes a zero line for reference, aiding in the visualization of the convergence or divergence of the MACD and signal lines. To enhance its utility, the script encompasses alert conditions to notify users when there is a change in the trend of the histogram—specifically, when it transitions from a rising to a falling state and vice versa, potentially indicating shifts in market momentum.

Overall, the Instant MACD is an innovative tool for traders who require early trend signals in scenarios where traditional MACD analysis might be hampered by the lack of extensive historical data.

tl;dr this is identical to the regular macd but it starts working almost instantly.

Divergence AnalyzerUnlock the potential of your trading strategy with the Divergence Analyzer, a sophisticated indicator designed to identify divergence patterns between two financial instruments. Whether you're a seasoned trader or just starting, this tool provides valuable insights into market trends and potential trading opportunities.

Key Features:

1. Versatility in Symbol Selection:

- Choose from a wide range of symbols for comparison, including popular indices like XAUUSD and SPX.

- Seamlessly toggle between symbols to analyze divergences and make informed trading decisions.

2. Flexible Calculation Options:

- Customizable options allow you to use a different symbol for calculation instead of the chart symbol.

- Fine-tune your analysis by selecting specific symbols for comparison based on your trading preferences.

3. Logarithmic Scale Analysis:

- Utilizes logarithmic scales for accurate representation of price movements.

- Linear regression coefficients are calculated on the logarithmic scale, providing a comprehensive view of trend strength.

4. Dynamic Length and Smoothing:

- Adjust the length parameter to adapt the indicator to different market conditions.

- Smoothed linear regression with exponential moving averages enhances clarity and reduces noise.

5. Standard Deviation Normalization:

- Normalizes standard deviations over 200 periods, offering a standardized view of price volatility.

- Easily compare volatility levels across different symbols for effective divergence analysis.

6. Color-Coded Divergence Visualization:

- Clearly distinguish positive and negative divergences with customizable color options.

- Visualize divergence deltas with an intuitive color scheme for quick and effective interpretation.

7. Symbol Information Table:

- An included table provides at-a-glance information about the selected symbols.

- Identify Symbol 1 and Symbol 2, along with their corresponding positive and negative divergence colors.

How to Use:

1. Select symbols for analysis using the user-friendly inputs.

2. Customize calculation options based on your preferences.

3. Analyze the divergence delta plot for clear visual indications.

4. Refer to the symbol information table for a quick overview of selected instruments.

Empower your trading strategy with the Divergence Analyzer and gain a competitive edge in the dynamic world of financial markets. Start making more informed decisions today!

Instant RSI (IRSI)

Instant RSI is tailored for users seeking an effective RSI indicator for charts with limited historical data, such as new symbols or very high time frame charts. Its distinctiveness lies in employing a Chebyshev filter, an innovative approach that allows the RSI to initiate calculations with just two data points. The Chebyshev filter, traditionally used in signal processing, helps in smoothing data while minimizing lag, a critical aspect in fast-moving financial markets.

Key Features:

Chebyshev Filter Integration: The Chebyshev filter is fine-tuned to mimic a 14-period RMA's behavior, enhancing the RSI's responsiveness and accuracy with minimal data.

Customizable RSI and MA Settings: Users can modify the RSI's source, length, ripple effect, and style. An optional moving average overlay, also based on Chebyshev filtering, tuned to mimic an EMA set to 14.

Divergence Detection: I have also included the ability to adjust the divergence settings to allow for more flexibility over the built in RSI.

The script operates by applying the Chebyshev filter to the price movement's up and down components, forming the basis of the RSI calculation. When the moving average feature is activated, it further processes the RSI value through the Chebyshev filter for additional smoothing. This dual application of the Chebyshev filter is central to the script's design, offering a unique solution for situations where traditional RSI calculations might be less reliable due to data scarcity.

The divergence detection feature enhances the script's utility by signaling potential trend reversals, critical for strategic decision-making in trading. These features are visually represented on the chart, ensuring that users can easily interpret and react to the indicators.

In general this indicator should produce the exact same output as the built in RSI. This indicator is specifically designed to be used in conditions where the built in RSI will not work due to limited data.

In summary, the "Instant RSI" script is a practical option for those dealing with limited data scenarios, offering a unique blend of Chebyshev filter application for more responsive market analysis.

MACD Crossover with +/- FilterThis is to directly target when MACD crosses the Signal line. The purpose of this script is to target a +/- change of 3 in the MACD value after the most recent cross. It uses the value of the MACD line and holds it until a value of 3.00 + or - a crossover or crossunder happens. That's the significance of the red and green circles that appear on the chart. This is not financial advice, but I wanted to recreate what a friend of mine was doing manually and automate it for him.

The first circle that appears after MACD/SIGNAL lines cross would represent a potential trade idea. The circles after the first one match the intention of the first dot as they meet the condition of more than a value of -3 or +3 as the previous dot.

Inputs:

Standard Inputs as normal MACD (Moving Average Converging Divergence) within TradingView

Fast Length: User can change it to any value they want

Slow Length: User can change it to any value they want

Standard 12, 26, 9 as normal MACD // 9 being signal smoothing

Oscillator and Signal Line moving average type is using EMA's

Timeframe is dependent on user chart.

Circles are used for signaling the change in values. Red indicates a short-term bearish trend. Green indicates a short-term bullish trend.

Tested on lower timeframes:

1m, 3m, 5m, 15m, 60m

Not used as much on higher timeframes. Used for trading futures. This is what I use it for. It can be used for other futures than just NQ or ES, but those 2 are the ones that I've tested. Code it shown below for users to tinker with.

Style of indication symbol can be changed via settings within the indicator in the "Style" tab, as well as location of the symbol(s). Additionally, color can be changed as well, if you prefer different colors.

Not financial advice. Just trade ideas.

Relative Strength Trend Indicator (RSTI)This indicator is called the "Relative Strength Trend Indicator" (RSTI), designed to assess the relative strength of a trend.

Here is a detailed explanation of how it works and how traders can interpret it:

Indicator Operation:

1. Data Source (src): The indicator considers a data source, typically the closing price (close), but this can be adjusted according to the trader's preferences.

2. Period Length (Length): This determines the period used to calculate the simple moving average (SMA) of the data source. A longer period smoothes the indicator, while a shorter period makes it more responsive.

3. Multiplier (Multiplier): This is a multiplication factor applied to the Average True Range (ATR), adjusting the width of the bands.

4. Signal Length (Signal Length): This period is used to calculate the simple moving average of the relative strength (l_strength). It determines the sensitivity of the signal to changes in relative strength.

Interpretation of the Indicator:

1. Upper Strength Band (Upper Level): This line is drawn at 80 and represents a high strength level. When relative strength exceeds this value, it may indicate a potential overbought market.

2. Lower Strength Band (Lower Level): This line is drawn at 20 and represents a low strength level. When relative strength is below this value, it may indicate a potential oversold market.

3. RSTI Strength: The main line of the indicator, representing the calculated relative strength. When this line exceeds 50, it may indicate an uptrend, while a value below 50 may indicate a downtrend.

4. Filling Zones: These colored zones between levels 80 and 50, and between 50 and 20, can help quickly visualize relative strength. A colored zone above 50 indicates positive strength, while a colored zone below 50 indicates negative strength.

Qualities of the Indicator:

1. Adaptability: The use of ATR and the flexibility of parameters (length, multiplier, signal_length) allow the indicator to adapt to different market conditions.

2. Visual Clarity: Colored filling zones and horizontal lines make it easy to visualize relative strength levels.

3. Strength Signal: The signal line (RSTI Strength) allows traders to quickly spot changes in relative strength, facilitating decision-making.

4. Responsiveness: The combination of smoothed moving averages and relative strength indicators allows responsiveness to trend changes while reducing false signals.

It is essential to note that while this indicator can provide valuable insights, it is always recommended to use it in conjunction with other technical analysis tools for informed decision-making.

ROC & EMAIn summary, this allows you to plot the ROC, its EMA, and dynamically display the value of this EMA on the chart.

You can configure different lengths and colors.

Unpretentious code, just for the pleasure of sharing.

Thank you for sharing your comments with me, which will be welcome.

Ultimate Momentum"Ultimate Momentum" – Elevating Your Momentum Analysis

Experience a refined approach to momentum analysis with "Ultimate Momentum," a sophisticated indicator seamlessly combining the strengths of RSI and CCI. This tool offers a nuanced understanding of market dynamics with the following features:

1. Harmonious Fusion: Witness the dynamic interplay between RSI and CCI, providing a comprehensive understanding of market nuances.

2. Optimized CCI Dynamics: Delve confidently into market intricacies with optimized CCI parameters, enhancing synergy with RSI for a nuanced perspective on trends.

3. Standardized Readings: "Ultimate Momentum" standardizes RSI and CCI, ensuring consistency and reliability in readings for refined signals.

4. Native TradingView Integration: Immerse yourself in the reliability of native TradingView codes for RSI and CCI, ensuring stability and compatibility.

How RSI and CCI Work Together:

RSI (Relative Strength Index): Captures price momentum with precision, measuring the speed and change of price movements.

CCI (Commodity Channel Index): Strategically integrated to complement RSI, offering a unique perspective on price fluctuations and potential trend reversals.

Why "Ultimate Momentum"?

In a crowded landscape, "Ultimate Momentum" stands out, redefining how traders interpret momentum. Gain a profound understanding of market dynamics, spot trend reversals, and make informed decisions.

Your Insights Matter:

Share your suggestions to enhance "Ultimate Momentum" in the comments. Your feedback is crucial as we strive to deliver an unparalleled momentum analysis tool.

Triple Confirmation Kernel Regression Base [QuantraSystems]Kernel Regression Oscillator - BASE

Introduction

The Kernel Regression Oscillator (ᏦᏒᎧ) represents an advanced tool for traders looking to capitalize on market trends.

This Indicator is valuable in identifying and confirming trend directions, as well as probabilistic and dynamic oversold and overbought zones.

It achieves this through a unique composite approach using three distinct Kernel Regressions combined in an Oscillator. The additional Chart Overlay Indicator adds confidence to the signal.

This methodology helps the trader to significantly reduce false signals and offers a more reliable indication of market movements than more widely used indicators can.

Legend

The upper section is the Overlay. It features the Signal Wave to display the current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 3), which can indicate extremely rare situations which can lead to either a softening momentum in the trend or even a mean reversion situation.

The lower one is the Base Chart - This Indicator.

It features the Kernel Regression Oscillator to display a composite of three distinct regressions, also displaying current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 2), which can indicate extremely rare situations.

Case Study

To effectively utilize the ᏦᏒᎧ, traders should use both the additional Overlay and the Base

Chart at the same time. Then focus on capturing the confluence in signals, for example:

If the 𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮 on the Overlay and the ᏦᏒᎧ on the Base Chart both reside near the extreme of an Oversold zone the probability is higher than normal that momentum in trend may soften or the token may even experience a reversion soon.

If a bar is characterized by an Oversold Shading in both the Overlay and the Base Chart, then the probability is very high to experience a reversion soon.

In this case the trader may want to look for appropriate entries into a long position, as displayed here.

If a bar is characterized by an Overbought Shading in either Overlay or Base Chart, then the probability is high for momentum weakening or a mean reversion.

In this case the trade may have taken profit and closed his long position, as displayed here.

Please note that we always advise to find more confluence by additional indicators.

Recommended Settings

Swing Trading (1D chart)

Overlay

Bandwith: 45

Width: 2

SD Lookback: 150

SD Multiplier: 2

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Fast-paced, Scalping (4min chart)

Overlay

Bandwith: 75

Width: 2

SD Lookback: 150

SD Multiplier: 3

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Notes

The Kernel Regression Oscillator on the Base Chart is also sensitive to divergences if that is something you are keen on using.

For maximum confluence, it is recommended to use the indicator both as a chart overlay and in its Base Chart.

Please pay attention to shaded areas with Standard Deviation settings of 2 or 3 at their outer borders, and consider action only with high confidence when both parts of the indicator align on the same signal.

This tool shows its best performance on timeframes lower than 4 hours.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

The trend following functionality is indicated through the "𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮" Line, with optional "Up" and "Down" arrows to denote trend directions only (toggle “Show Trend Signals”).

Methodology

The Kernel Regression Oscillator takes three distinct kernel regression functions,

used at similar weight, in order to calculate a balanced and smooth composite of the regressions. Part of it are:

The Epanechnikov Kernel Regression: Known for its efficiency in smoothing data by assigning less weight to data points further away from the target point than closer data points, effectively reducing variance.

The Wave Kernel Regression: Similarly assigning weight to the data points based on distance, it captures repetitive and thus wave-like patterns within the data to smoothen out and reduce the effect of underlying cyclical trends.

The Logistic Kernel Regression: This uses the logistic function in order to assign weights by probability distribution on the distance between data points and target points. It thus avoids both bias and variance to a certain level.

kernel(source, bandwidth, kernel_type) =>

switch kernel_type

"Epanechnikov" => math.abs(source) <= 1 ? 0.75 * (1 - math.pow(source, 2)) : 0.0

"Logistic" => 1/math.exp(source + 2 + math.exp(-source))

"Wave" => math.abs(source) <= 1 ? (1 - math.abs(source)) * math.cos(math.pi * source) : 0.

kernelRegression(src, bandwidth, kernel_type) =>

sumWeightedY = 0.

sumKernels = 0.

for i = 0 to bandwidth - 1

base = i*i/math.pow(bandwidth, 2)

kernel = kernel(base, 1, kernel_type)

sumWeightedY += kernel * src

sumKernels += kernel

(src - sumWeightedY/sumKernels)/src

// Triple Confirmations

Ep = kernelRegression(source, bandwidth, 'Epanechnikov' )

Lo = kernelRegression(source, bandwidth, 'Logistic' )

Wa = kernelRegression(source, bandwidth, 'Wave' )

By combining these regressions in an unbiased average, we follow our principle of achieving confluence for a signal or a decision, by stacking several edges to increase the probability that we are correct.

// Average

AV = math.avg(Ep, Lo, Wa)

The Standard Deviation bands take defined parameters from the user, in this case sigma of ideally between 2 to 3,

to help the indicator detect extremely improbable conditions and thus take an inversely probable signal from it to forward to the user.

The parameter settings and also the visualizations allow for ample customizations by the trader. The indicator comes with default and recommended settings.

For questions or recommendations, please feel free to seek contact in the comments.

BDC - Bitcoin (BTC) Dominance Change [Logue]Bitcoin Dominance Change. Interesting things tend to happen when the Bitcoin dominance increases or decreases rapidly. Perhaps because there is overexuberance in the market in either BTC or the alts. In back testing, I found a rapid 13-day change in dominance indicates interesting switches in the BTC trends. Prior to 2019, the indicator doesn't work as well to signal trend shifts (i.e., local tops and bottoms) likely based on very few coins making up the crypto market.

The BTC dominance change is calculated as a percentage change of the daily dominance. You are able to change the upper bound, lower bound, and the period (daily) of the indicator to your own preferences. The indicator going above the upper bound or below the lower bound will trigger a different background color.

Use this indicator at your own risk. I make no claims as to its accuracy in forecasting future trend changes of Bitcoin.

Price PressureDescription:

The Price Pressure Indicator, developed by OmegaTools, is a robust and versatile tool designed to assist traders in analyzing market dynamics and identifying potential trend shifts. This open-source script, offers a unique approach to understanding price pressure over specified periods, enhancing the user's ability to make informed trading decisions.

Key Features:

1. Dynamic Length Configuration: The indicator allows users to customize the length parameter, ranging from 9 to 100, providing flexibility in adapting to different market conditions.

2. Extensions Control: Traders can fine-tune the extension levels (ob) between 50 and 90, allowing for precise adjustments based on their risk tolerance and trading preferences.

3. Normalization and Oscillation: The script employs a normalization function to standardize price data, offering a clearer representation of market pressure. The resulting oscillator visualizes the normalized pressure, highlighting potential market trends.

4. Pressure Calculation: The indicator calculates price pressure by considering the difference between the previous high and the current close, as well as the difference between the current close and the previous low. This innovative approach enhances the accuracy of pressure analysis.

5. Smoothing Option: While the script currently uses a simple moving average for smoothing, traders have the option to explore other smoothing methods by uncommenting the "smt" input line.

6. Visual Clarity: The indicator provides a visually intuitive representation of pressure and signal lines, aiding traders in quickly interpreting market conditions. The color-coded display enhances user experience, with the ability to discern bullish and bearish pressures.

7. Premium and Discount Zones: The script identifies premium and discount areas, assisting traders in spotting potential buying or selling opportunities. The premium and discount lines can be adjusted based on individual risk tolerance and strategy.

How to Use:

1. Adjust the length and extension parameters based on your trading preferences.

2. Interpret the oscillator and signal lines for insights into market pressure.

3. Utilize premium and discount zones to identify potential entry or exit points.

4. Experiment with different smoothing options for a customized analysis.

Concepts and Methodology:

The Price Pressure Indicator utilizes a normalization function and oscillation to quantify market pressure. By calculating the difference between highs and lows, the script provides a nuanced understanding of current market conditions. The smoothing option further refines the analysis, offering traders a comprehensive tool for trend identification.

Explore, experiment, and leverage the power of the Price Pressure Indicator to enhance your trading strategy on TradingView.

Chaos CypherOverview

Technically a smooth linear rate transformation, the "Chaos Cypher" drew some inspiration from the principles of Markov and chaos. Aside from price action, this combination provides a different lens through which to observe and interpret market movements. Markov models are based on the principle that future states depend only on the current state, not on the sequence of events that preceded it. Chaos theory deals with systems that are highly sensitive to initial conditions, a concept popularly referred to as the butterfly effect.

Efficient with Minimal Data: Designed to perform efficiently, the CC indicator is particularly useful in situations regardless of extensive historical data, except for obvious back testing, while still providing strength at identifying potential overbought/oversold zones and critical divergences.

Simplified Momentum Analysis: With further inspiration from the triple smoothed exponential rate, the CC actually uses linear regression for its calculations. This approach allows for a clear and more straightforward identification of deviations in momentum. The smoothing helps allow it to provide details while still operating at a fast pace due to the regression speed.

Adaptable to Various Timeframes: The transformation calculation then employed effectively narrows its scope in relation to the pace, enhancing its applicability across multiple timeframes and periods. This flexibility makes it a versatile tool suitable for various strategies and market conditions.

Fisher Transform Style Presentation: The indicator is presented in a style reminiscent of the Fisher Transform. However, this method of the script recalculates based on every individual dataset. To maintain efficiency, the adjustable length only applies to the regression rate.

The Chaos Cypher when compared to the Fisher Transform

Inversion Option for Leads: Lastly, an intriguing find when testing this script is the potential of the inversion option. This aspect proved particularly useful when searching for pullbacks on a trending market.

Conclusion

This indicator is designed to be forward-thinking and attempts to combine theoretical concepts with practicality. It has the ability to work with minimal data, adapt to various timeframes, and provide clear views of market movements. It back tested very well even when unrealistically used as a sole instrument.

"Two states differing by imperceptible amounts may eventually evolve into two considerably different states ... If, then, there is any error whatever in observing the present state—and in any real system such errors seem inevitable—an acceptable prediction of an instantaneous state in the distant future may well be impossible....In view of the inevitable inaccuracy and incompleteness of weather observations, precise very-long-range forecasting would seem to be nonexistent." -Edward Norton Lorenz

Dynamic Volume-Volatility Adjusted MomentumThis Indicator in a refinement of my earlier script PC*VC Moving average Old with easier to follow color codes, overbought and oversold zones. This script has converted the previous script into a standardized measure by converting it into Z-scores and also incorporated a volatility based dynamic length option. Below is a detailed Explanation.

The "Dynamic Volume-Volatility Adjusted Momentum" or "Nasan Momentum Oscillator" is designed to capture market momentum while accounting for volume and volatility fluctuations. It leverages the Typical Price (TP), calculated as the average of high, low, and close prices, and introduces the Price Coefficient (PC) based on deviations from the simple moving average (SMA) across various time frames. Additionally, the Volume Coefficient (VC) compares current volume to SMA, and calculates Intraday Volatility (IDV) which gauges the daily price range relative to the close. Then intraday volatility ratio is calculated ( IDV Ratio) as the ratio of current Intraday Volatility (IDV) to the average of IDV for three different length periods, which provides a relative measure of current intraday volatility compared to its recent historical average. An inter-day ATR based Relative Volatility (RV) is calculated to adjusts for changing market volatility based on which the dynamic length adjustment adapts the moving average (standard length is 14). The PC *VC/IDV Ratio integrates price, volume, and volatility information which provides a volume and volatility adjusted momentum. This volume and volatility adjusted momentum is converted into a standardized Z-Score. The Z-Score measures deviations from the mean. Color-coded plots visually represent momentum, and thresholds aid in identifying overbought or oversold conditions.

The indicator incorporates a nuanced approach to emphasize the joint impact of price and volume while considering the stabilizing effect of lower intraday volatility. Placing the volume ratio (VC) in the numerator means that higher volume positively contributes to the overall ratio, aligning with the observation that increased volumes often accompany robust price movements. Simultaneously, the decision to include the inverse of intraday volatility (1/IDV) in the denominator acts as a dampener, reducing the impact of extreme intraday volatility on the momentum indicator. This design choice aims to filter out noise, giving more weight to significant price changes supported by substantial trading activity. In essence, the indicator's design seeks to provide a more robust momentum measure that balances the influence of price, volume, and volatility in the analysis of market dynamics.

OneThingToRuleThemAll [v1.4]This script was created because I wanted to be able to display a contextual chart of commonly used indicators for scalping and swing traders, with the ability to control the visual representation on the charts as their cross-overs, cross-unders, or changes of state happen in real time. Additionally, I wanted the ability to control how or when they are displayed. While looking through other community projects, I found they lacked the ability to full customize the output controls and values used for these indicators.

The script leverages standard RSI/MACD/VWAP/MVWAP/EMA calculations to help a trader visually make more informed decisions on entering or exiting a trade, depending on their understanding on what the indicators represent. Paired with a table directly on the chart, it allows a trader to quickly reference values to make more informed decisions without having to look away from the price action or look through multiple indicator outputs.

The main functionality of the indicator is controlled within the settings directly on the chart. There a user can enable the visual representations, or disable, and configure how they are displayed on the charts by altering their values or style types.

Users have the ability to enable/disable visual representations of:

The indicator chart

RSI Cross-over and RSI Reversals

MACD Uptrends and Downtrends

VWAP Cross-overs and Cross-unders

VWAP Line

MVWAP Cross-overs and Cross-unders

MVWAP Line

EMA Cross-overs and Cross-unders

EMA Line

Some traders like to use these visual indications as thresholds to enter or exit trades. Its best to find out which ones work the best with the security you are trying to trade. Personally, I use the table as a reference in conjunction with the RSI chart indicators to help me decide a logical trailing stop if I am scalping. Some users might like the track EMA200 crossovers, and have visual representations on the chart for when that happens. However, users may use the other indicators in other methods, and this script provides the ability to be able to configure those both visually and by value.

The pine script code is open source and itself is fairly straightforward, it is mostly written to provide the ultimate level of control the the user of the various indicators. Please reach out to me directly if you would like a further understanding of the code and an explanation on anything that may be unclear.

Enjoy :)

-dead1.

TSI Market Timer + Volatility MeterThis is the TSI Market Timer. It is years in the making and it is comprised of four indicators in one. The stock (or source) is run through an indicator called the True Strength Indicator with settings(5,15) , then the TSI is run on both the Index(SPY) by default and what I call a Trigger line which is basically the TSI applied to the DXY (US Dollar Index).

Midline Volatility Indicator:

Lastly, we have a volatility indicator on the midline. The colors of the midline indicate levels of volatility. For the lowest volatility in the last 100 days, the dot turns dark blue. For the lowest volatility in 30 days, the dot turns aqua. For regular volatility, it remains orange. And last, for higher volatility of the last 100 days, it turns red. These are more or less arbitrary but they do come in handy.

Settings for Green/Red Shading:

Next on the indicator are the settings. You can toggle a color change between the stock/source and the index(spy). If the stock/source is greater than the index, it will color the area in between a green and if it is below the index, it will be red.

There is also a toggle for the stock/source and the trigger/DXY. This will also show green when the stock is above the trigger and red if it is below the trigger.

By turning on both of these, you get light green and dark green areas as well as red and darker red areas. The lighter green represent when the stock is above both the index and the trigger and conversely for the red areas.

Settings for vertical line crossings:

When the stock crosses the trigger/dxy line, it shows a green vertical line signal. When the stock crosses below the trigger/dxy, a red vertical line is shown.

You can turn these off by toggling them in the settings.

Stacked Condition:

Lastly, we have a "stacked condition" which shows up as a white triangle at the bottom when the condition of the stock being above the index and the trigger below the zero line.

New Highs:

If you see the stock line turn lime green, this indicates a new high was reached for the last 255 days/periods. This is like a new 52 week high signal.

Note:

This indicator is made mostly for the stock market. It may work ok during the week for crypto but using the trigger/dxy and index lines on the weekends doesn't work too well as they will be flat.

Also note that this indicator is not a recommendation to buy or sell any stock/instrument. It is only a study of market conditions. Any analysis should be followed up with volume analysis or other confirming indicators.

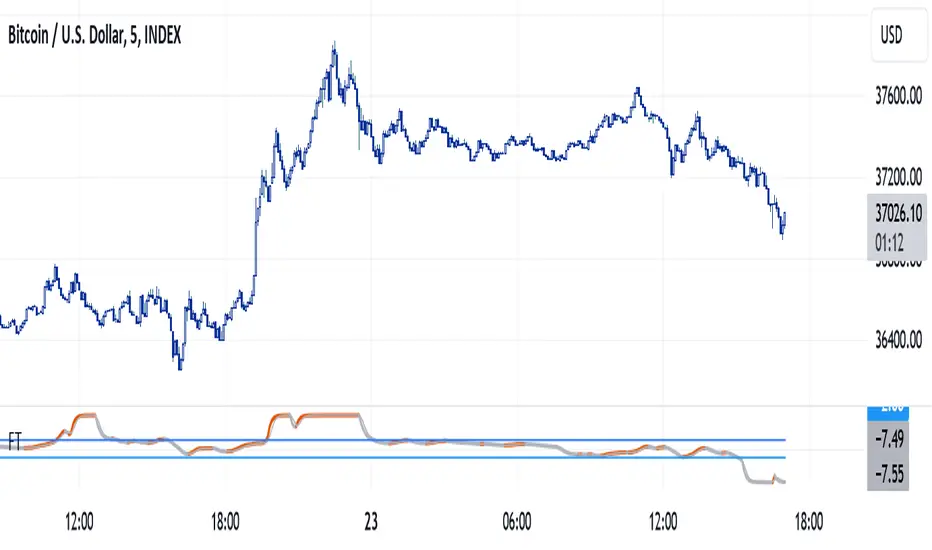

Fisher Transform RevisitedFisher Transform developped by Ehlers is used mostly to detect peaks and troughs, which it does with little lag, but there are many false signals. Looking at its formula and construction, we can revisit it for the purpose of detecting trends and flat market.

How do we want to do that? There are 3 different actions:

Increase the default value from usual 9 or 10 to 30

Show the indicator as seen from upper time frame with synthetic rolling candles

Change the weights in first formula in order to saturate the input signal, push the trend data to the limits, so therefore leaving a good view when market is flat

As can be seen from the chart above, the revisited Fisher is above 2 for uptrend markets, below -2 for downtrending markets and in-between when the market is flat.

Notes

Weights for Fisher transform formula can be changed as parameters. Recommended valeus are 0.6 and 0.6 to saturate signal. You may come back to original formula by setting 0.33 and 0.66.

Parameter n allows view from upper time, a multiple of current time frame. n = 1 for current chart, n = 5 for 5 minutes view on the 1 min chart

Usage

Of course, it should be not be used in standalone mode. Indicator is for trend traders who can stay away when market is flat. Trend start when indicator goes above 2 but like all trade indicators, it will be late; it is therefore a good idea to change n back to 1 to get a timely entry, to be confirmed of course with other elements of technical analysis.

Dynamic Trend Fusion (DTF)The "Dynamic Trend Fusion" (DTF) indicator is a powerful technical analysis tool for traders. It stands out from other indicators due to its adaptability and ability to provide insights into different trading styles. Users can choose from various trading options such as "Short-term Trading," "Long-term Trading," "Aggressive Short-term," "Conservative Long-term," "Balanced Approach," "High Sensitivity," "Low Sensitivity," "Day Trading," and "Swing Trading." These options allow traders to customize the indicator to suit their specific trading strategies.

DTF combines the Moving Average Convergence Divergence (MACD) and Relative Strength Index (RSI) indicators, normalizing them to a similar scale for a comprehensive view of market conditions. It then calculates a combined value and smoothes it using a moving average.

One of its standout features is the ability to identify bullish and bearish states, which is represented visually on the chart. When the indicator detects a transition from a bullish to a bearish state or vice versa, the color of the line changes.

Additionally, DTF offers alert conditions, notifying users when the market shifts into a bullish or bearish state, allowing for timely decision-making.

In summary, the DTF indicator sets itself apart by providing traders with a versatile tool that can be tailored to various trading styles and offers clear visual signals for trend changes, enhancing trading precision and efficiency.

Multi-data oscillatorThe multi-data oscillator is a tool created to help traders visualize clearly how an oscillator works and moves considering different input parameters.

In this tool, you can choose to visualize the script as the RSI, the CCI, the LOC indicator, a custom-created formula that simply shows the location of the data considering X past values, or the average of all of these three indicators.

In the settings, you can choose both the length of the indicator and the smoothing factor.

Additionally, the indicator has a gradient color that changes considering the deviation and the variance of the different lines used to calculate the average line, displayed with more thickness.

[KVA]nRSIThe nRSI stands as a groundbreaking enhancement of the traditional Relative Strength Index (RSI), specifically engineered for traders seeking a more refined and accurate tool in fast-moving markets.

Customizable Price Change Period (n): Unlike the traditional RSI which solely relies on a fixed period for average gains and losses, the nRSI introduces an additional parameter, n, to calculate price changes.

This adaptation focuses on minimizing market noise, sharpening the indicator's sensitivity to genuine trends and patterns.

Enhanced Signal Precision : By reducing the influence of short-term price spikes and fluctuations, the nRSI delivers a more precise signal. This precision is particularly crucial in volatile market conditions, where traditional indicators may be swayed by transient movements.

Ideal Usage

Strategic Trading Decisions : Ideal for traders who need to filter out insignificant price movements to make more strategic, informed trading decisions.

Reliable Divergence Spotting : Enhanced noise reduction aids in identifying more reliable divergences, key for predicting potential market reversals.

Trend Confirmation : The smoothed RSI, assisted by the moving average, becomes an invaluable tool for confirming the validity of market trends, minimizing false signals.

Detrended Price Rate of ChangeThe Detrended Price Rate of Change is an oscillator developed to help traders identify potential conditions of overbought and oversold markets.

The formula of the oscillator includes both the Detrended price formula, useful to spot divergences, and the Rate of change simplified formula, which helps in identifying overextended markets and gives useful information on price momentum.

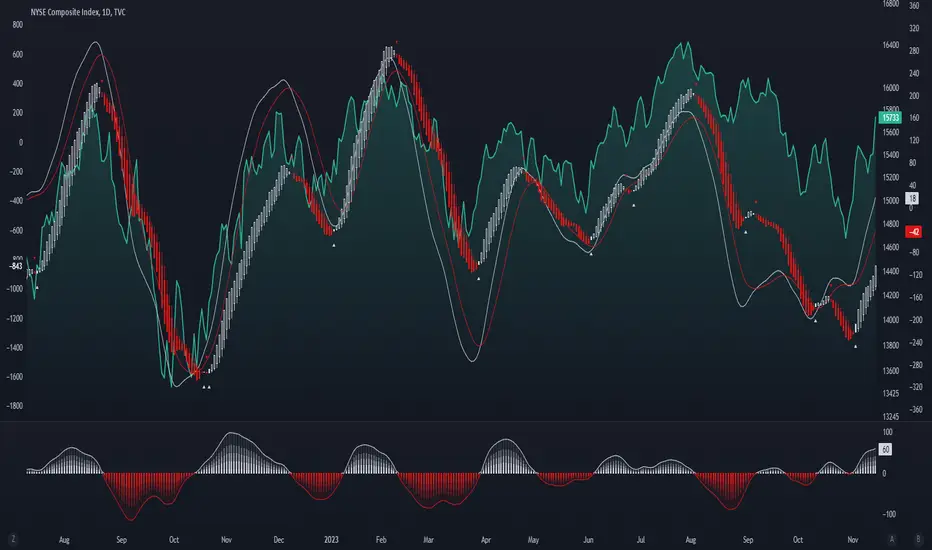

Enhanced McClellan Summation Index

The Enhanced McClellan Summation Index (MSI) is a comprehensive tool that transforms the MSI indicator with Heikin-Ashi visualization, offering improved trend analysis and momentum insights. This indicator includes MACD and it's histogram calculations to refine trend signals, minimize false positives and offer additional momentum analysis.

Methodology:

McClellan Summation Index (MSI) -

The MSI begins by calculating the ratio between advancing and declining issues in the specified index.

float decl = 𝘐𝘯𝘥𝘪𝘤𝘦 𝘥𝘦𝘤𝘭𝘪𝘯𝘪𝘯𝘨 𝘪𝘴𝘴𝘶𝘦𝘴

float adv = 𝘐𝘯𝘥𝘪𝘤𝘦 𝘢𝘥𝘷𝘢𝘯𝘤𝘪𝘯𝘨 𝘪𝘴𝘴𝘶𝘦𝘴

float ratio = (adv - decl) / (adv + decl)

It then computes a cumulative sum of the MACD (the difference between a 19-period EMA and a 39-period EMA) of this ratio. The result is a smoothed indicator reflecting market breadth and momentum.

macd(float r) =>

ta.ema(r, 19) - ta.ema(r, 39)

float msi = ta.cum(macd(ratio))

Heikin-Ashi Transformation -

Heikin-Ashi is a technique that uses a modified candlestick formula to create a smoother representation of price action. It averages the open, close, high, and low prices of the current and previous periods. This transformation reduces noise and provides a clearer view of trends.

type bar

float o = open

float h = high

float l = low

float c = close

bar b = bar.new()

float ha_close = math.avg(b.o, b.h, b.l, b.c)

MACD and Histogram -

The Enhanced MSI incorporates MACD and histogram calculations to provide additional momentum analysis and refine trend signals. The MACD represents the difference between the 12-period EMA and the 26-period EMA of the MSI. The histogram is the visual representation of the difference between the MACD and its signal line.

Options:

Index Selection - Choose from TVC:NYA , NASDAQ:NDX , or TVC:XAX to tailor the MSI-HA to the desired market index.

MACD Settings - Adjust the parameters for the MACD calculation to fine-tune the indicator's responsiveness.

Ratio Multiplier - Apply scaling to the MSI to suit different market conditions and indices.

Benefits of Heikin-Ashi -

Smoothed Trends - Heikin-Ashi reduces market noise, providing a more apparent and smoothed representation of trends.

Clearer Patterns - Candlestick patterns are more distinct, aiding in the identification of trend reversals and continuations.

Utility and Use Cases:

Trend & Momentum Analysis - Utilize the tool's Heikin-Ashi visualization for clearer trend identification in confluence with it's MACD and histogram to gain additional insights into the strength and direction of trends, while filtering out potential false positives.

Breadth Analysis - Explore market breadth through the MSI's cumulative breadth indicator, gauging the overall health and strength of the underlying market.

- Alerts Setup Guide -

The Enhanced MSI is a robust indicator that combines the breadth analysis of the McClellan Summation Index with the clarity of Heikin-Ashi visualization and additional momentum insights from MACD and histogram calculations. Its customization options make it adaptable to various indices and market conditions, offering traders a comprehensive tool for trend and momentum analysis.

MACD Pulse CheckThis custom script, titled " MACD Pulse Check ," is a modified and enhanced version of the traditional Moving Average Convergence Divergence (MACD) indicator, commonly used in trading for trend-following and momentum strategies. Here's a breakdown of its features and benefits over the traditional MACD:

Multiple MACD Lines with Different Parameters:

The script calculates six different MACD lines using various combinations of fast, slow, and signal lengths. This diverse range allows for a more comprehensive analysis of the market momentum and trend across different time scales and sensitivities.

Average of MACD Lines:

By averaging these six MACD lines, the script creates a more smoothed and potentially less noisy signal. This can help in reducing false signals and improving the reliability of trend indications.

Sideways Market Detection:

A unique feature of this script is its ability to identify sideways or range-bound markets using a user-defined threshold. This is calculated by comparing the current price to the price five candles ago and seeing if the change is within a certain percentage threshold. Identifying sideways markets is crucial as trend-following strategies like MACD typically perform poorly in these conditions.

Visual and Color-Coded Signals:

The script plots shapes (circles) on the chart, where the color (green for bullish, red for bearish, sideways price action will display as either a dull green or a dull red) quickly indicates the market condition. This visual representation makes it easier to interpret the signals at a glance, and spot sideways price action while still having a general idea of trend.

Benefits for Traders:

Versatility: By averaging multiple MACD lines, traders get a more nuanced view of the market momentum, potentially leading to more informed trading decisions.

Reduced False Signals:

The averaging process and sideways market detection can help in filtering out false or weak signals, which is a common issue with the traditional MACD.

Ease of Use:

The color-coded visual signals simplify the process of identifying market trends and conditions, making the tool accessible even for less experienced traders.

In summary, "MACD Pulse Check" enhances the traditional MACD by providing a more comprehensive, and visually intuitive tool, potentially leading to better trading decisions in varying market conditions. However, it's important to note that no indicator is foolproof and should always be used in conjunction with other analysis methods and sound risk management practices.