Line Break Chart StrategyHello All!

We should not pass this year without a gift!

My last publication in 2024 is Complete Line Break Chart Strategy with many features!

What is Line Break Chart?

" Line Break is a Japanese chart style that disregards time intervals and only focuses on price movements, similar to the Kagi and Renko chart styles. Line Break charts form a series of up and down bars (referred to as lines). Up lines represent rising prices, and down lines represent falling prices. New confirmed lines only form on the chart when closing prices break the range covered by previous lines. Users can control the number of past lines used in the calculation via the "Number of Lines" input in the chart settings. The typical "Number of Lines" setting is 3, meaning the chart forms a new up line when the closing price is above the high prices of the last three lines, and it forms a new down line when the closing price is below the past three lines' low prices. If the current price is higher, it is an up line and if it is lower, it is a down line. If the current closing price is the same or the move in the opposite direction is not large enough to warrant a reversal, l then no new line is draw n" by Tradingview. You can find it here

Now let's start examining the features of the indicator:

By using Line break reversals it shows trend on the main chart. You can create alert .

Moreover, you can decide which trade should be taken by using Risk Management in the indicator. You can set the " Maximum Risk " and then if the risk is more than you set then the trade is not taken. When trend changed it checks the distance between reversal level and open price and compare it with the Maximum Risk

Breakout:

It can find breakouts and shows on the chart. You can create alert for breakouts

It can show breakouts on the main chart:

Flip-Flops:

Upon looking at set of price break charts, the trader will notice that there are instances when uptrend blocks is followed by one reversal block, and then by a reversal to a series of uptrend blocks. The opposite is also possible: a series of downtrend blocks is followed by one reversal box and then by an immediate reversal to downtrend. This price action is called a " Flip-Flop ". This structure usually produces trend continuation signal. when we see this then we better use Buy/Sell stop order. lets see this on the chart:

Temporal Sequence Table:

Sequence frequency shows the frequency distribution of the number of sequential highs and the number of sequential lows that have been generated. This is quite important to the trader who is seeking to join a trend or put on a trade when the price break reverses into a new trend direction. For example, if the pattern over the past year has been that there never were more than nine consecutive high closes, it would make sense not to enter a position late into the sequence of new high closes.

also you can see market structure. I have tried to formalize it and show it under the table. so you can understand if it's choppy market.

"Number of Lines" has very important role. While using low time frames such seconds/minutes time frame you may want to choose higher number of lines such 5,6. ( this may minimize the risk of a whipsaw )

Gaps feature:

You can set Gaps on/off. if Gaps on then you can see how long it takes for each box

Reversal and Continuation Probability:

The script calculated Reversal level and Continuation probability of the trend by using Sequence frequency.

It also shows unconfirmed box and current closing price level:

Last but not least it has Overlay option for all items, and can show all items in the main chart!

P.S. I added alerts :)

Wish you all a happy new year!

Enjoy!

Forecasting

Longest Candles HighlighterDescription:

The Longest Candles Highlighter is a simple yet effective tool that identifies and highlights candles with significant price ranges. By visually marking candles that meet specific size criteria, this indicator helps traders quickly spot high-volatility moments or significant market moves on the chart.

Features:

1. Customizable Candle Range:

- Define the minimum and maximum candle size in pips using input fields.

- Tailor the indicator to highlight candles that are most relevant to your trading strategy.

2. Flexible for Different Markets:

- Automatically adjusts pip calculation based on the instrument type (Forex or non-Forex).

- Accounts for differences in pip values, such as the 0.01 pip for JPY pairs in Forex.

3. Visual Highlighting:

- Highlights qualifying candles with a customizable background color for easy identification.

- The default color is red, but you can choose any color to match your chart theme.

4. Precision and Efficiency:

- Quickly scans and identifies candles that meet your criteria, saving you time in analyzing charts.

- Works seamlessly across all timeframes and asset classes.

How It Works:

- The indicator calculates the range of each candle in pips by subtracting the low from the high and dividing by the appropriate pip value.

- It checks whether the candle's size falls within the user-defined minimum and maximum pip range.

- If the conditions are met, the background of the candle is highlighted with the specified color, drawing your attention to significant price movements.

Use Case:

- This indicator is ideal for identifying key market moments, such as breakouts, volatility spikes, or significant price movements.

- Traders can use it to quickly locate large candles on any chart, aiding in technical analysis and strategy development.

This tool simplifies the process of spotting important candles, empowering traders to make faster and more informed trading decisions.

JCM_MadridThis indicator provides dynamic bar coloring and buy/sell signals based on EMA relationships and price momentum. It allows traders to visually identify trend changes and potential trade opportunities directly on the chart.

Indicator Basics:

Name: The script is titled "JCM_Madrid".

Overlay: It overlays its calculations and outputs directly on the price chart.

User Inputs:

-Range: Defines the length of the EMA (Exponential Moving Average).

-Ref-1 and Ref-2: Set reference lengths for secondary EMAs used in the calculations.

-Source: The price data source for EMA calculations (e.g., close, open, high, low).

-Enable Buy/Sell: Boolean toggles to activate or deactivate buy and sell signals.

Calculations:

EMA Value: Computes the main EMA based on the source and Range.

CloseMA: The difference between the close price and the EMA.

SqzMA: The difference between a secondary EMA (Ref-1) and the main EMA.

RefMA: The difference between another secondary EMA (Ref-2) and the main EMA.

Bar Coloring:

Bars are colored based on the relationship between SqzMA and CloseMA:

Purple: When SqzMA > CloseMA.

Blue: When SqzMA < CloseMA.

Buy/Sell Signals:

A Buy Signal is generated when:

CloseMA crosses from below to above 0.

The close price is higher than the previous close.

Buy signals are enabled.

A Sell Signal is generated when:

CloseMA crosses from above to below 0.

The close price is lower than the previous close.

Sell signals are enabled.

Signals are displayed as labels on the chart:

"Buy": Green label below the candle.

"Sell": Yellow label below the candle

Compare TOTAL, TOTAL2, TOTAL3, and OTHERSCompare TOTAL, TOTAL2, TOTAL3, and OTHERS

This indicator compares the performance of major cryptocurrency market cap indices: TOTAL, TOTAL2, TOTAL3, and OTHERS. It normalizes each index's performance relative to its starting value and visualizes their relative changes over time.

Features

- Normalized Performance: Tracks the percentage change of each index from its initial value.

- Customizable Timeframe: Allows users to select a base timeframe for the data (e.g., daily, weekly).

- Dynamic Labels: Displays the latest performance of each index as a label on the chart, aligned to the right of the corresponding line for easy comparison.

- Color-Coded Lines: Each index is assigned a distinct color for clear differentiation:

-- TOTAL (Blue): Represents the total cryptocurrency market cap.

-- TOTAL2 (Green): Excludes Bitcoin.

-- TOTAL3 (Orange): Excludes Bitcoin and Ethereum.

-- OTHERS (Red): Represents all cryptocurrencies excluding the top 10 by market cap.

- Baseline Reference: Includes a horizontal line at 0% for reference.

Use Cases:

- Market Trends: Identify which segments of the cryptocurrency market are outperforming or underperforming over time.

- Portfolio Insights: Assess the impact of Bitcoin and Ethereum dominance on the broader market.

- Market Analysis: Compare smaller-cap coins (OTHERS) with broader indices (TOTAL, TOTAL2, and TOTAL3).

This script is ideal for traders and analysts who want a quick, visual way to track how different segments of the cryptocurrency market perform relative to each other over time.

Note: The performance is normalized to highlight percentage changes, not absolute values.

Pi Cycle MACD Inverse OscillatorPi Cycle MACD Inverse Oscillator with Gradient and Days Since Last Top

This indicator is ideal for Bitcoin traders seeking a robust tool to visualize long-term and short-term trends with enhanced clarity and actionable insights.

This script combines the concept of the Pi Cycle indicator with a unique MACD-based inverse oscillator to analyze Bitcoin market trends. It introduces several features to help traders understand market conditions better:

Inverse Oscillator:

- Oscillator ranges between 1 and -1.

- A value of 1 indicates the two moving averages (350 MA and 111 MA) are equal.

- A value of -1 indicates the maximum observed distance between the moving averages during the selected lookback period.

- The oscillator dynamically adjusts to price changes using a configurable scaling factor.

Gradient Visualization:

The oscillator line transitions smoothly from green (closer to -1) to yellow (at 0) and red (closer to 1).

The color gradient provides a quick visual cue for market momentum.

Days Since Last Pi Cycle Top:

Calculates and displays the number of days since the last "Pi Cycle Top" (defined as a crossover between the two moving averages).

The label updates dynamically and appears only on the most recent bar.

Conditional Fill:

Highlights the area between 0 and 1 with a green gradient when the price is above the long moving average.

Enhances visual understanding of the oscillator's position relative to key thresholds.

Inputs:

- Long Moving Average (350 default): Determines the primary trend.

- Short Moving Average (111 default): Measures shorter-term momentum.

- Oscillator Lookback Period (100 default): Defines the range for normalizing the oscillator.

- Price Scaling Factor (0.01 default): Adjusts the normalization to account for large price fluctuations.

How to Use:

- Use the oscillator to identify potential reversal points and trend momentum.

- Look for transitions in the gradient color and the position relative to 0.

- Monitor the "Days Since Last Top" label for insights into the market's cycle timing.

- Utilize the conditional fill to quickly assess when the market is in a favorable position above the long moving average.

ForecastPro by BinhMyco1. Overview:

This Pine Script implements a custom forecasting tool on TradingView, labeled "BinhMyco." It provides a method to predict future price movements based on historical data and a comparison with similar historical patterns. The script supports two types of forecasts: **Prediction** and **Replication**, where the forecasted price can be either based on price peaks/troughs or an average direction. The script also calculates a confidence probability, showing how closely the forecasted data aligns with historical trends.

2. Inputs:

- Source (`src`): The input data source for forecasting, which defaults to `open`.

- Length (`len`): The length of the training data used for analysis (fixed at 200).

- Reference Length (`leng`): A fixed reference length for comparing similar historical patterns (set to 70).

- Forecast Length (`length`): The length of the forecast period (fixed at 60).

- Multiplier (`mult`): A constant multiplier for the forecast confidence cone (set to 4.0).

- Forecast Type (`typ`): Type of forecast, either **Prediction** or **Replication**.

- Direction Type (`dirtyp`): Defines how the forecast is calculated — either based on price **peaks/troughs** or an **average direction**.

- Forecast Divergence Cone (`divcone`): A boolean option to enable the display of a confidence cone around the forecast.

3. Color Constants:

- Green (`#00ffbb`): Color used for upward price movements.

- Red (`#ff0000`): Color used for downward price movements.

- Reference Data Color (`refcol`): Blue color for the reference data.

- Similar Data Color (`simcol`): Orange color for the most similar data.

- Forecast Data Color (`forcol`): Yellow color for forecasted data.

4. Error Checking:

- The script checks if the reference length is greater than half the training data length, and if the forecast length exceeds the reference length, raising errors if either condition is true.

5. Arrays for Calculation:

- Correlation Array (`c`): Holds the correlation values between the data source (`src`) and historical data points.

- Index Array (`index`): Stores the indices of the historical data for comparison.

6. Forecasting Logic:

- Correlation Calculation: The script calculates the correlation between the historical data (`src`) and the reference data over the given reference length. It then identifies the point in history most similar to the current data.

- Forecast Price Calculation: Based on the type of forecast (Prediction or Replication), the script calculates future prices either by predicting based on similar bars or by replicating past data. The forecasted prices are stored in the `forecastPrices` array.

- Forecast Line Drawing: The script draws lines to represent the forecasted price movements. These lines are color-coded based on whether the forecasted price is higher or lower than the current price.

7. Divergence Cone (Optional):

- If the **divcone** option is enabled, the script calculates and draws a confidence cone around the forecasted prices. The upper and lower bounds of the cone are calculated using a standard deviation factor, providing a visual representation of forecast uncertainty.

8. Probability Table:

- A table is displayed on the chart, showing the probability of the forecast being accurate. This probability is calculated using the correlation between the current data and the most similar historical pattern. If the probability is positive, the table background turns green; if negative, it turns red. The probability is presented as a percentage.

9. Key Functions:

- `highest_range` and `lowest_range`: Functions to find the highest and lowest price within a range of bars.

- `ftype`: Determines the forecast type (Prediction or Replication) and adjusts the forecasting logic accordingly.

- `ftypediff`: Computes the difference between the forecasted and actual prices based on the selected forecast type.

- `ftypelim`, `ftypeleft`, `ftyperight`: Additional functions to adjust the calculation of the forecast based on the forecast type.

10. Conclusion:

The "ForecastPro" script is a unique tool for forecasting future price movements on TradingView. It compares historical price data with similar historical trends to generate predictions. The script also offers a customizable confidence cone and displays the probability of the forecast's accuracy. This tool provides traders with valuable insights into future price action, potentially enhancing decision-making in trading strategies.

---

This script provides advanced functionality for traders who wish to explore price forecasting, and can be customized to fit various trading styles.

Market Movement After OpenDescription:

This script provides a detailed visualization of market movements during key trading hours: the German market opening (08:00–09:00 UTC+1) and the US market opening (15:30–16:30 UTC+1). It is designed to help traders analyze price behavior in these critical trading periods by capturing and presenting movement patterns and trends directly on the chart and in an interactive table.

Key Features:

Market Movement Analysis:

Tracks the price movement during the German market's first hour (08:00–09:00 UTC+1) and the US market's opening session (15:30–16:30 UTC+1).

Analyzes whether the price moved up or down during these intervals.

Visual Representation:

Dynamically colored price lines indicate upward (green) or downward (red) movement during the respective periods.

Labels ("DE" for Germany and "US" for the United States) mark key moments in the chart.

Historical Data Table:

Displays the past 10 trading days' movement trends in an interactive table, including:

Date: Trading date.

German Market Movement: Up (▲), Down (▼), or Neutral (-) for 08:00–09:00 UTC+1.

US Market Movement: Up (▲), Down (▼), or Neutral (-) for 15:30–16:30 UTC+1.

The table uses color coding for easy interpretation: green for upward movements, red for downward, and gray for neutral.

Real-Time Updates:

Automatically updates during live trading sessions to reflect the most recent movements.

Highlights incomplete periods (e.g., ongoing sessions) to indicate their status.

Customizable:

Suitable for intraday analysis or broader studies of market trends.

Designed to overlay directly on any price chart.

Use Case:

This script is particularly useful for traders who focus on market openings, which are often characterized by high volatility and significant price movements. By providing a clear visual representation of historical and live data, it aids in understanding and capitalizing on market trends during these critical periods.

Notes:

The script works best when the chart is set to the appropriate timezone (UTC+1 for the German market or your local equivalent).

For precise trading decisions, consider combining this script with other technical indicators or trading strategies.

Feel free to share feedback or suggest additional features to enhance the script!

M2 Global Liquidity Index - Time-Shift - KHM2 Global Liquidity Index - Enhanced Time-Shift Indicator

Based on original work by @Mik3Christ3ns3n

Enhanced with advanced time-shift functionality and overlay capabilities.

Description:

This indicator tracks and visualizes the global M2 money supply from five major economies, allowing precise time-shift analysis for correlation studies. All values are converted to USD in real-time and aggregated to provide a comprehensive view of global liquidity conditions.

Key Features:

- Advanced time-shift capability (-1000 to +1000 days) with shape preservation

- Real-time currency conversion to USD

- Overlay functionality with main chart

- Right-scale display for better comparison

- Full historical data preservation during time shifts

Components Tracked:

- US M2 Money Supply (USM2)

- China M2 Money Supply (CNM2)

- Eurozone M2 Money Supply (EUM2)

- Japan M2 Money Supply (JPM2)

- UK M2 Money Supply (GBM2)

Primary Use Cases:

1. Correlation Analysis:

- Compare global liquidity trends with asset prices

- Identify leading/lagging relationships through time-shift

- Study monetary policy impacts across different time periods

2. Market Analysis:

- Track global liquidity conditions

- Monitor central bank policy effects

- Identify potential macro trend changes

Settings:

- Time Offset: Shift the M2 data backwards or forwards (-1000 to +1000 days)

- Positive values: Move M2 data into the future

- Negative values: Move M2 data into the past

- Zero: Current alignment

Technical Notes:

- Data updates follow central banks' M2 publication schedules

- All currency conversions performed in real-time

- Historical shape preservation during time-shifts

- Enhanced data consistency through lookahead mechanism

Credits:

Original concept and base code by @Mik3Christ3ns3n

Enhanced version includes advanced time-shift capabilities and shape preservation

License:

Pine Script™ code is subject to the terms of the Mozilla Public License 2.0

#M2 #GlobalLiquidity #MoneySupply #Macro #CentralBanks #MonetaryPolicy #TimeShift #Correlation #TradingIndicator #MacroAnalysis #LiquidityAnalysis #MarketIndicator

Pivot Highs/Lows with Bar CountsWhat does the indicator do?

This indicator adds labels to a chart at swing (a.k.a., "pivot") highs and lows. Each label may contain a date, the closing price at the swing, the number of bars since the last swing in the same direction, and the number of bars from the last swing in the opposite direction. A table is also added to the chart that shows the average, min, and max number of bars between swings.

OK, but how do I use it?

Many markets -- especially sideways-moving ones -- commonly cycle between swing highs and lows at regular time intervals. By measuring the number of bars between highs and lows -- both same-sided swings (i.e., H-H and L-L) and opposite-sided swings (i.e., H-L and L-H) -- you can then project the averages of those bar counts from the last high or low swing to make predictions about where the next swing high or low should occur. Note that this indicator does not make the projection for you. You have to determine which swing you want to project from and then use the bar counts from the indicator to draw a line, place a label, etc.

Example: Chart of BTC/USD

The indicator shows pivot highs and lows with bar counts, and it displays a table of stats on those pivots.

If you focus on the center section of the chart, you can see that prices were moving in a sideways channel with very regular highs and lows. This indicator counts the bars between these pivots, and you could have used those counts to predict when the next high or low may have occurred.

The bar counts do not work as well on the more recent section of the chart because there are no regularly time swings.

Market Open Levels v3This indicator "Market Open Levels v3" allows a chart user to automatically display up to 20 previous price levels at the open price of up to 8 different markets simultaneously on one indicator.

The user can specify custom labels for each market's price level, as well as adjust the GMT Offset to allow for market open times in a different timezone than the chart's displayed time.

Displays price level at specified market open times. For instance, if a user specifies a market opens at 08:00, then a price level (horizontal line) will be drawn at the most recent 08:00 candle's open price (if GMT Offset is set to 0).

See tooltips for more information on specific inputs.

Three Step Future-Trend [BigBeluga]Three Step Future-Trend by BigBeluga is a forward-looking trend analysis tool designed to project potential future price direction based on historical periods. This indicator aggregates data from three consecutive periods, using price averages and delta volume analysis to forecast trend movement and visualize it on the chart with a projected trend line and volume metrics.

🔵 Key Features:

Three Period Analysis: Calculates price averages and delta volumes from three specified periods, creating a consolidated view of historical price movement.

Future Trend Line Projection: Plots a forward trend line based on the calculated averag of three periods, helping traders visualize potential future price movement.

Avg Delta Volume and Future Price Label: Shows a delta average Volume a long with a Future Price label at the end of the projected trend line, indicating the possible future delta volume and future Price.

Volume Data Table: Displays a detailed table showing delta and total volume for each of the three periods, allowing quick volume comparison to support the projected trend.

This indicator provides a dynamic way to anticipate market direction by blending price and volume data, giving traders insights into both volume and trend strength in upcoming periods.

DCA Order Info PlannerDescription :

This script is a Dollar-Cost Averaging (DCA) order planner designed for SPOT, LONG, and SHORT markets. It automatically calculates the optimal price levels for your orders based on configurable parameters, while also considering leverage and liquidation price.

🔹 Key Features:

1. Automatic Order Planning:

- The script calculates price levels for your orders based on an adjustable scaling coefficient (default: 1.5).

- You can set the percentage interval between each order (default: 2%).

- Displays the number of units to buy/sell at each level.

2.Leverage Management:

- Integrates a configurable leverage and computes the liquidation price for LONG and SHORT positions.

3.Clear Visual Display:

- Markers on the chart indicating order levels with customizable labels.

- A summary table shows price levels and corresponding quantities.

- Visualizes Stop Loss and Take Profit levels if defined.

4.Automatic Alerts:

- Sends alerts when the price reaches an order level.

🔹 Customizable Parameters:

- Starting Price: Initial price for calculating orders.

- Budget: Total budget for DCA orders.

- Leverage: Multiplier for LONG/SHORT positions.

- Scaling Coefficient: Adjusts the spacing between order levels.

- Maximum DCA Levels: Limits the number of generated orders.

🔹 How to Use:

1. Configure the parameters according to your strategy.

2. The script displays order levels and quantities on the chart.

3. Use the summary table to manually input orders on your favorite trading platform.

This script is particularly useful in volatile market conditions to average your entry or exit price and manage risk effectively.

Supertrend with Correct Y-axis Scaling OLEG_SLSThe functionality of the script:

1. Supertrend Calculation:

-The trend (Supertrend line) is updated dynamically:

-If the price is above the previous trend, the line follows the upper limit.

-If the price is lower, the line follows the lower boundary.

2. Calculation of the Supertrend for the higher timeframe:

-The function is used to calculate the Supertrend for the hourly, regardless of the current timeframe on the chart.

3. Buy and Sell Signals:

-Buy signal: When the price crosses the Supertrend line up and is above the Supertrend line.

-A sales signal: When the price crosses the Supertrend line down and is below the Supertrend line.

4. Display on the chart

-The Supertrend line is displayed:

-Green if the price is above the Supertrend line.

-Red if the price is below the Supertrend line.

-The Supertrend line for the hourly timeframe is displayed in blue.

5. Alerts

Two types of alerts are created:

-Buy Alert: When there is a buy signal.

-Sell Alert: When there is a sell signal.

Features and recommendations:

-Supertrend works best in trending markets. In a sideways movement, it can give false signals.

-Check the signals on multiple timeframes for confirmation.

-Add additional indicators (for example, RSI or MACD) to filter the signals.

-Test the strategy on historical data before using it in real trading.

_________________________________________________________________________________

Функционал скрипта:

1. Расчет Supertrend:

-Тренд (линия Supertrend) обновляется динамически:

-Если цена выше предыдущего тренда, линия следует за верхней границей.

-Если цена ниже, линия следует за нижней границей.

2. Расчет Supertrend для старшего таймфрейма:

-Используется функция чтобы рассчитать Supertrend для часового,независимо от текущего таймфрейма на графике.

3. Сигналы покупки и продажи:

-Сигнал покупки: Когда цена пересекает линию Supertrend вверх и находится выше линии Supertrend.

-Сигнал продажи: Когда цена пересекает линию Supertrend вниз и находится ниже линии Supertrend.

4. Отображение на графике

-Линия Supertrend отображается:

-Зеленым, если цена выше линии Supertrend.

-Красным, если цена ниже линии Supertrend.

-Линия Supertrend для часового таймфрейма отображается синим цветом.

5. Оповещения

Создаются два типа оповещений:

-Buy Alert: Когда возникает сигнал на покупку.

-Sell Alert: Когда возникает сигнал на продажу.

Особенности и рекомендации:

-Supertrend лучше всего работает в трендовых рынках. В боковом движении может давать ложные сигналы.

-Проверяйте сигналы на нескольких таймфреймах для подтверждения.

-Добавьте дополнительные индикаторы (например, RSI или MACD) для фильтрации сигналов.

-Тестируйте стратегию на исторических данных перед использованием в реальной торговле.

The Dragons Maw [inspired by Kioseff Trading]The Dragon's Maw is a playful visualization tool that uses Monte Carlo simulation to create a dragon-like pattern on your chart. Although primarily intended for entertainment, it is also suitable for testing or falsifying the utility of this method's predictions.

What It Does:

- Generates multiple price path simulations that form the shape of a "fire-breathing" effect

- Shows upper and lower boundaries of all simulations as the dragon's "maw"

- Displays the dragon's "eye" and "ear" as a visual indicator of the historical data used

How It Works:

1. The indicator calculates returns from historical price data

2. Using Monte Carlo simulation with either normal distribution or bootstrap sampling, it generates multiple potential price paths

3. These paths are rendered with high transparency to create a fire/smoke effect showing the higher probability regions as denser color

4. It can be observed that the direction of the "fire" is influenced by recent price movement especially when set in relation to the "eye" position which indicates the limit of historical data used for the simulation

Educational Value:

Use the 'Move to the Left' parameter to position the dragon's head at different points in historical data. This feature serves as an excellent demonstration of the limitations of statistical price projections – you'll quickly see how the simulated paths diverge from what actually happened, highlighting why such projections should not be relied upon for trading decisions.

You might find, that it's not at all capable of 'predicting' sudden price movements but rather 'predicts' a continuation of the recent trend.

Features:

- Adjustable number of simulations (affects detail of the "fire" effect)

- Moveable dragon head (can be positioned at different points in price history)

- Customizable colors for the maw boundaries and fire effect

- Optional scale display for price levels

Note: This indicator is inspired by KioseffTrading's original work, with added features for visualization and positioning. While it uses statistical methods, it should be viewed as an artistic interpretation of price movement rather than a predictive tool.

Settings Guide:

- Upper/Lower Limit: Colors for the dragon's maw boundaries

- Fire Color: Color and transparency of the simulation paths

- Look Back: How far back to calculate the dragon's eye position

- Much Fire: Controls the density of simulation paths

- Length: Determines how far forward the simulation extends

The chart shows a clean view of the indicator's output, with the dragon's eye (o), ear, maw boundaries, and fire effect clearly visible on the right side of the chart by default.

Murad Picks Target MCThe Murad Picks Target Market Cap Indicator is a custom TradingView tool designed for crypto traders and enthusiasts tracking tokens in the Murad Picks list. This indicator dynamically calculates and visualizes the price targets based on Murad Mahmudov's projected market capitalizations, allowing you to gauge each token's growth potential directly on your charts.

Indicator support tokens:

- SPX6900

- GIGA

- MOG

- POPCAT

- APU

- BITCOIN

- RETARDIO

- LOCKIN

Key Features :

Dynamic Target Price Lines:

- Displays horizontal lines representing the price when the token reaches its projected market cap.

- Automatically adjusts for the active chart symbol (e.g., SPX, MOG, APU, etc.).

X Multiplier Calculation:

- Shows how many times the current price must multiply to achieve the target price.

- Perfect for understanding relative growth potential.

Customizable Inputs:

- Easily update target market caps and circulating supply for each token.

- Adjust visuals such as line colors and styles.

Seamless Integration:

- Automatically adapts to the token you’re viewing (e.g., SPX, MOG, APU).

- Clean and visually intuitive, with labels marking targets.

FuTech : Earnings (All 269 Fundamental Metrics of Tradingview)FuTech : Earnings Indicator

The FuTech : Earnings Indicator is a revolutionary tool, offering the most comprehensive integration of all 269 fundamental financial metrics available from the TradingView platform.

This groundbreaking indicator is designed to empower financial researchers, traders, investors, and analysts with an unmatched depth of data, enabling superior analysis and decision-making.

Overview

"FuTech : Earnings Indicator" is the first-ever indicator to provide a holistic comparison of fundamental financial metrics for any stock, covering quarterly, yearly, and trailing twelve months (TTM) periods.

This tool brings together key financial data from income statements, balance sheets, cash flows, and other critical metrics found in company annual reports.

It also incorporates additional unique features like per-employee data, R&D expenses, and capital expenditures (CapEx), which are typically hidden within dense financial statements of Annual Reports.

---

Key Features and Capabilities

1. Comprehensive Financial Metrics

- "FuTech : Earnings Indicator" offers access to all 269 fundamental metrics available on TradingView platform. This includes widely used data such as revenue, profit margins, and EPS, alongside more niche metrics like R&D expenditure, employee efficiency, and financial scores developed by renowned analysts.

- Users can explore income statement data (e.g., net income, gross profit), balance sheet items (e.g., total assets, liabilities), cash flow metrics, and other financial statistics such as Altman Score, per employee expenses etc. in unparalleled detail.

2. Comparison Across Time Periods

- "FuTech : Earnings Indicator" allows users to analyze data for:

- Quarterly periods (e.g., Q1, Q2, Q3, Q4).

- Yearly comparisons for a broad historical view.

- TTM analysis to observe the most recent trends and developments.

- Users can select a minimum of 4 periods up to an unlimited range for detailed comparisons in both quarter.

3. Dynamic Data Display

- Users can select up to 5 key metrics alongside the stock price column to focus their analysis on the most relevant data points.

- Highlighting with green and red symbols offers an intuitive and visual representation:

- Green : Positive trends or improvements.

- Red : Negative trends or deteriorations.

4. Automated Averages

- "FuTech : Earnings Indicator" automatically calculates averages of selected metrics across the chosen periods. This feature helps users quickly identify performance trends and smooth out anomalies, enabling faster and more reliable research.

5. Designed for Research Excellence

- FuTech serves a wide audience, including:

- Corporate finance professionals who need a deep dive into financial metrics.

- Individual investors seeking robust tools for investment analysis.

- Broking companies and equity research analysts performing stock analysis.

- Traders looking to incorporate fundamental metrics into their strategies.

- Technical analysts seeking a better understanding of price behavior in relation to fundamentals.

- Fundamental research aspirants who want an edge in their learning process.

6. Unmatched Detail for Deeper Insights

- By pulling all 269 Financial metrics from the TradingView, "FuTech : Earnings Indicator" enables:

- Cross-comparison of a stock’s performance with its historical benchmarks.

- Evaluation of rare data like R&D expenses, CapEx trends, and employee efficiency ratios for enhanced investment insights.

- This ensures users can study stocks in greater depth than ever before.

7. Enhanced Usability

- Simple to use and visually appealing, "FuTech : Earnings Indicator" is designed with researchers in mind.

- Its intuitive interface ensures even novice users can navigate the wealth of data without feeling overwhelmed.

Applications of FuTech : Earnings Indicator

FuTech : Earnings Indicator is incredibly versatile and has applications in diverse fields of financial research and trading:

1. Corporate Finance

- Professionals in corporate finance can leverage "FuTech : Earnings Indicator" to benchmark company performance, study efficiency ratios, and evaluate financial health across various metrics.

2. Investors and Traders

- Long-term investors can use the tool to study the fundamental strengths of a stock before making buy-and-hold decisions.

- Traders can incorporate "FuTech : Earnings Indicator" into their analysis to align comprehensive fundamental trends with their targeted technical signals.

3. Equity Research Analysts

- Analysts can streamline their workflows by quickly identifying trends, outliers, and averages across large datasets.

4. Education and Research

- "FuTech : Earnings Indicator" is ideal for students and aspiring financial analysts who want a practical tool for understanding real-world data.

How FuTech : Earnings Indicator Stands Out

1. First-Ever Integration of All Financial Metrics

- It's an exclusive tool which offers the ability to explore all 269 financial metrics available on TradingView for a single stock research in-depth for quarters, years or TTM periods.

2. Period Customization

- Users have complete flexibility to select and analyze data across any range of time periods, allowing for customized insights tailored to specific research goals.

3. Data Visualization

- The intuitive use of color-coded symbols (green for positive trends, red for negative) makes complex data easy to interpret at a glance.

4. Actionable Insights

- The automated average calculations provide actionable insights for making informed decisions without manual computations.

5. Unique Metrics

- Metrics such as research and development costs, CapEx, and per-employee efficiency data offer unique angles that aren’t typically available in traditional analysis tools.

Why to Use FuTech : Earnings Indicator ?

1. Boost Your Research Power

- With FuTech, you can unlock a world of data that gives you the edge in analyzing stocks. Whether you’re a seasoned analyst or a beginner, this tool offers something for everyone.

2. Save Time and Effort

- The automated features and intuitive interface eliminate the need for time-consuming manual calculations and formatting.

3. Make Better Decisions

- "FuTech : Earnings Indicator's" detailed comparison capabilities and insightful visual aids allow for more accurate assessments of a stock’s performance and potential.

4. Broad Appeal

- From individual investors to financial institutions, FuTech is a valuable tool for anyone in the world of finance.

---

Conclusion

- The FuTech : Earnings Indicator is a must-have for anyone serious about financial analysis.

- It combines the depth of all 269 fundamental metrics with intuitive tools for comparison, visualization, and calculation.

- Designed for ease of use and powerful insights, FuTech : Earnings Indicator is set to transform the way financial data is analyzed and understood.

Thank you !

Jai Swaminarayan Dasna Das !

He Hari ! Bas Ek Tu Raji Tha !

Kalman PredictorThe **Kalman Predictor** indicator is a powerful tool designed for traders looking to enhance their market analysis by smoothing price data and projecting future price movements. This script implements a Kalman filter, a statistical method for noise reduction, to dynamically estimate price trends and velocity. Combined with ATR-based confidence bands, it provides actionable insights into potential price movement, while offering clear trend and momentum visualization.

---

#### **Key Features**:

1. **Kalman Filter Smoothing**:

- Dynamically estimates the current price state and velocity to filter out market noise.

- Projects three future price levels (`Next Bar`, `Next +2`, `Next +3`) based on velocity.

2. **Dynamic Confidence Bands**:

- Confidence bands are calculated using ATR (Average True Range) to reflect market volatility.

- Visualizes potential price deviation from projected levels.

3. **Trend Visualization**:

- Color-coded prediction dots:

- **Green**: Indicates an upward trend (positive velocity).

- **Red**: Indicates a downward trend (negative velocity).

- Dynamically updated label displaying the current trend and velocity value.

4. **User Customization**:

- Inputs to adjust the process and measurement noise for the Kalman filter (`q` and `r`).

- Configurable ATR multiplier for confidence bands.

- Toggleable trend label with adjustable positioning.

---

#### **How It Works**:

1. **Kalman Filter Core**:

- The Kalman filter continuously updates the estimated price state and velocity based on real-time price changes.

- Projections are based on the current price trend (velocity) and extend into the future (Next Bar, +2, +3).

2. **Confidence Bands**:

- Calculated using ATR to provide a dynamic range around the projected future prices.

- Indicates potential volatility and helps traders assess risk-reward scenarios.

3. **Trend Label**:

- Updates dynamically on the last bar to show:

- Current trend direction (Up/Down).

- Velocity value, providing insight into the expected magnitude of the price movement.

---

#### **How to Use**:

- **Trend Analysis**:

- Observe the direction and spacing of the prediction dots relative to current candles.

- Larger spacing indicates a potential strong move, while clustering suggests consolidation.

- **Risk Management**:

- Use the confidence bands to gauge potential price volatility and set stop-loss or take-profit levels accordingly.

- **Pullback Detection**:

- Look for flattening or clustering of dots during trends as a signal of potential pullbacks or reversals.

---

#### **Customizable Inputs**:

- **Kalman Filter Parameters**:

- `lookback`: Adjusts the smoothing window.

- `q`: Process noise (higher values make the filter more reactive to changes).

- `r`: Measurement noise (controls sensitivity to price deviations).

- **Confidence Bands**:

- `band_multiplier`: Multiplies ATR to define the range of confidence bands.

- **Visualization**:

- `show_label`: Option to toggle the trend label.

- `label_offset`: Adjusts the label’s distance from the price for better visibility.

---

#### **Examples of Use**:

- **Scalping**: Use on lower timeframes (e.g., 1-minute, 5-minute) to detect short-term price trends and reversals.

- **Swing Trading**: Identify pullbacks or continuations on higher timeframes (e.g., 4-hour, daily) by observing the prediction dots and confidence bands.

- **Risk Assessment**: Confidence bands help visualize potential price volatility, aiding in the placement of stops and targets.

---

#### **Notes for Traders**:

- The **Kalman Predictor** does not predict the future with certainty but provides a statistically informed estimate of price movement.

- Confidence bands are based on historical volatility and should be used as guidelines, not guarantees.

- Always combine this tool with other analysis techniques for optimal results.

---

This script is open-source, and the Kalman filter logic has been implemented uniquely to integrate noise reduction with dynamic confidence band visualization. If you find this indicator useful, feel free to share your feedback and experiences!

---

#### **Credits**:

This script was developed leveraging the statistical principles of Kalman filtering and is entirely original. It incorporates ATR for dynamic confidence band calculations to enhance trader usability and market adaptability.

SMT Divergence ICT 01 [TradingFinder] Smart Money Technique🔵 Introduction

SMT Divergence (short for Smart Money Technique Divergence) is a trading technique in the ICT Concepts methodology that focuses on identifying divergences between two positively correlated assets in financial markets.

These divergences occur when two assets that should move in the same direction move in opposite directions. Identifying these divergences can help traders spot potential reversal points and trend changes.

Bullish and Bearish divergences are clearly visible when an asset forms a new high or low, and the correlated asset fails to do so. This technique is applicable in markets like Forex, stocks, and cryptocurrencies, and can be used as a valid signal for deciding when to enter or exit trades.

Bullish SMT Divergence : This type of divergence occurs when one asset forms a higher low while the correlated asset forms a lower low. This divergence is typically a sign of weakness in the downtrend and can act as a signal for a trend reversal to the upside.

Bearish SMT Divergence : This type of divergence occurs when one asset forms a higher high while the correlated asset forms a lower high. This divergence usually indicates weakness in the uptrend and can act as a signal for a trend reversal to the downside.

🔵 How to Use

SMT Divergence is an analytical technique that identifies divergences between two correlated assets in financial markets.

This technique is used when two assets that should move in the same direction move in opposite directions.

Identifying these divergences can help you pinpoint reversal points and trend changes in the market.

🟣 Bullish SMT Divergence

This divergence occurs when one asset forms a higher low while the correlated asset forms a lower low. This divergence indicates weakness in the downtrend and can signal a potential price reversal to the upside.

In this case, when the correlated asset is forming a lower low, and the main asset is moving lower but the correlated asset fails to continue the downward trend, there is a high probability of a trend reversal to the upside.

🟣 Bearish SMT Divergence

Bearish divergence occurs when one asset forms a higher high while the correlated asset forms a lower high. This type of divergence indicates weakness in the uptrend and can signal a potential trend reversal to the downside.

When the correlated asset fails to make a new high, this divergence may be a sign of a trend reversal to the downside.

🟣 Confirming Signals with Correlation

To improve the accuracy of the signals, use assets with strong correlation. Forex pairs like OANDA:EURUSD and OANDA:GBPUSD , or cryptocurrencies like COINBASE:BTCUSD and COINBASE:ETHUSD , or commodities such as gold ( FX:XAUUSD ) and silver ( FX:XAGUSD ) typically have significant correlation. Identifying divergences between these assets can provide a strong signal for a trend change.

🔵 Settings

Second Symbol : This setting allows you to select another asset for comparison with the primary asset. By default, "XAUUSD" (Gold) is set as the second symbol, but you can change it to any currency pair, stock, or cryptocurrency. For example, you can choose currency pairs like EUR/USD or GBP/USD to identify divergences between these two assets.

Divergence Fractal Periods : This parameter defines the number of past candles to consider when identifying divergences. The default value is 2, but you can change it to suit your preferences. This setting allows you to detect divergences more accurately by selecting a greater number of candles.

Bullish Divergence Line : Displays a line showing bullish divergence from the lows.

Bearish Divergence Line : Displays a line showing bearish divergence from the highs.

Bullish Divergence Label : Displays the "+SMT" label for bullish divergences.

Bearish Divergence Label : Displays the "-SMT" label for bearish divergences.

🔵 Conclusion

SMT Divergence is an effective tool for identifying trend changes and reversal points in financial markets based on identifying divergences between two correlated assets. This technique helps traders receive more accurate signals for market entry and exit by analyzing bullish and bearish divergences.

Identifying these divergences can provide opportunities to capitalize on trend changes in Forex, stocks, and cryptocurrency markets. Using SMT Divergence along with risk management and confirming signals with other technical analysis tools can improve the accuracy of trading decisions and reduce risks from sudden market changes.

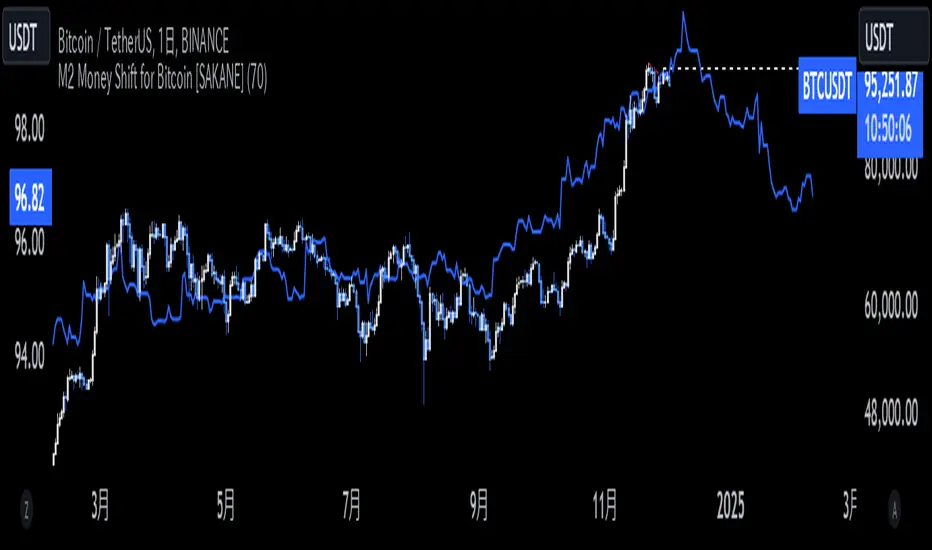

M2 Money Shift for Bitcoin [SAKANE]M2 Money Shift for Bitcoin was developed to visualize the impact of M2 Money, a macroeconomic indicator, on the Bitcoin market and to support trade analysis.

Bitcoin price fluctuations have a certain correlation with cycles in M2 money supply.In particular, it has been noted that changes in M2 supply can affect the bitcoin price 70 days in advance.Very high correlations have been observed in recent years in particular, making it useful as a supplemental analytical tool for trading.

Support for M2 data from multiple countries

M2 supply data from the U.S., Europe, China, Japan, the U.K., Canada, Australia, and India are integrated and all are displayed in U.S. dollar equivalents.

Slide function

Using the "Slide Days Forward" setting, M2 data can be slid up to 500 days, allowing for flexible analysis that takes into account the time difference from the bitcoin price.

Plotting Total Liquidity

Plot total liquidity (in trillions of dollars) by summing the M2 supply of multiple countries.

How to use

After applying the indicator to the chart, activate the M2 data for the required country from the settings screen. 2.

2. adjust "Slide Days Forward" to analyze the relationship between changes in M2 supply and bitcoin price

3. refer to the Gross Liquidity plot to build a trading strategy that takes into account macroeconomic influences.

Notes.

This indicator is an auxiliary tool for trade analysis and does not guarantee future price trends.

The relationship between M2 supply and bitcoin price depends on many factors and should be used in conjunction with other analysis methods.

Simple Decesion Matrix Classification Algorithm [SS]Hello everyone,

It has been a while since I posted an indicator, so thought I would share this project I did for fun.

This indicator is an attempt to develop a pseudo Random Forest classification decision matrix model for Pinescript.

This is not a full, robust Random Forest model by any stretch of the imagination, but it is a good way to showcase how decision matrices can be applied to trading and within Pinescript.

As to not market this as something it is not, I am simply calling it the "Simple Decision Matrix Classification Algorithm". However, I have stolen most of the aspects of this machine learning algo from concepts of Random Forest modelling.

How it works:

With models like Support Vector Machines (SVM), Random Forest (RF) and Gradient Boosted Machine Learning (GBM), which are commonly used in Machine Learning Classification Tasks (MLCTs), this model operates similarity to the basic concepts shared amongst those modelling types. While it is not very similar to SVM, it is very similar to RF and GBM, in that it uses a "voting" system.

What do I mean by voting system?

How most classification MLAs work is by feeding an input dataset to an algorithm. The algorithm sorts this data, categorizes it, then introduces something called a confusion matrix (essentially sorting the data in no apparently order as to prevent over-fitting and introduce "confusion" to the algorithm to ensure that it is not just following a trend).

From there, the data is called upon based on current data inputs (so say we are using RSI and Z-Score, the current RSI and Z-Score is compared against other RSI's and Z-Scores that the model has saved). The model will process this information and each "tree" or "node" will vote. Then a cumulative overall vote is casted.

How does this MLA work?

This model accepts 2 independent variables. In order to keep things simple, this model was kept as a three node model. This means that there are 3 separate votes that go in to get the result. A vote is casted for each of the two independent variables and then a cumulative vote is casted for the overall verdict (the result of the model's prediction).

The model actually displays this system diagrammatically and it will likely be easier to understand if we look at the diagram to ground the example:

In the diagram, at the very top we have the classification variable that we are trying to predict. In this case, we are trying to predict whether there will be a breakout/breakdown outside of the normal ATR range (this is either yes or no question, hence a classification task).

So the question forms the basis of the input. The model will track at which points the ATR range is exceeded to the upside or downside, as well as the other variables that we wish to use to predict these exceedences. The ATR range forms the basis of all the data flowing into the model.

Then, at the second level, you will see we are using Z-Score and RSI to predict these breaks. The circle will change colour according to "feature importance". Feature importance basically just means that the indicator has a strong impact on the outcome. The stronger the importance, the more green it will be, the weaker, the more red it will be.

We can see both RSI and Z-Score are green and thus we can say they are strong options for predicting a breakout/breakdown.

So then we move down to the actual voting mechanisms. You will see the 2 pink boxes. These are the first lines of voting. What is happening here is the model is identifying the instances that are most similar and whether the classification task we have assigned (remember out ATR exceedance classifier) was either true or false based on RSI and Z-Score.

These are our 2 nodes. They both cast an individual vote. You will see in this case, both cast a vote of 1. The options are either 1 or 0. A vote of 1 means "Yes" or "Breakout likely".

However, this is not the only voting the model does. The model does one final vote based on the 2 votes. This is shown in the purple box. We can see the final vote and result at the end with the orange circle. It is 1 which means a range exceedance is anticipated and the most likely outcome.

The Data Table Component

The model has many moving parts. I have tried to represent the pivotal functions diagrammatically, but some other important aspects and background information must be obtained from the companion data table.

If we bring back our diagram from above:

We can see the data table to the left.

The data table contains 2 sections, one for each independent variable. In this case, our independent variables are RSI and Z-Score.

The data table will provide you with specifics about the independent variables, as well as about the model accuracy and outcome.

If we take a look at the first row, it simply indicates which independent variable it is looking at. If we go down to the next row where it reads "Weighted Impact", we can see a corresponding percent. The "weighted impact" is the amount of representation each independent variable has within the voting scheme. So in this case, we can see its pretty equal, 45% and 55%, This tells us that there is a slight higher representation of z-score than RSI but nothing to worry about.

If there was a major over-respresentation of greater than 30 or 40%, then the model would risk being skewed and voting too heavily in favour of 1 variable over the other.

If we move down from there we will see the next row reads "independent accuracy". The voting of each independent variable's accuracy is considered separately. This is one way we can determine feature importance, by seeing how well one feature augments the accuracy. In this case, we can see that RSI has the greatest importance, with an accuracy of around 87% at predicting breakouts. That makes sense as RSI is a momentum based oscillator.

Then if we move down one more, we will see what each independent feature (node) has voted for. In this case, both RSI and Z-Score voted for 1 (Breakout in our case).

You can weigh these in collaboration, but its always important to look at the final verdict of the model, which if we move down, we can see the "Model prediction" which is "Bullish".

If you are using the ATR breakout, the model cannot distinguish between "Bullish" or "Bearish", must that a "Breakout" is likely, either bearish or bullish. However, for the other classification tasks this model can do, the results are either Bullish or Bearish.

Using the Function:

Okay so now that all that technical stuff is out of the way, let's get into using the function. First of all this function innately provides you with 3 possible classification tasks. These include:

1. Predicting Red or Green Candle

2. Predicting Bullish / Bearish ATR

3. Predicting a Breakout from the ATR range

The possible independent variables include:

1. Stochastics,

2. MFI,

3. RSI,

4. Z-Score,

5. EMAs,

6. SMAs,

7. Volume

The model can only accept 2 independent variables, to operate within the computation time limits for pine execution.

Let's quickly go over what the numbers in the diagram mean:

The numbers being pointed at with the yellow arrows represent the cases the model is sorting and voting on. These are the most identical cases and are serving as the voting foundation for the model.

The numbers being pointed at with the pink candle is the voting results.

Extrapolating the functions (For Pine Developers:

So this is more of a feature application, so feel free to customize it to your liking and add additional inputs. But here are some key important considerations if you wish to apply this within your own code:

1. This is a BINARY classification task. The prediction must either be 0 or 1.

2. The function consists of 3 separate functions, the 2 first functions serve to build the confusion matrix and then the final "random_forest" function serves to perform the computations. You will need all 3 functions for implementation.

3. The model can only accept 2 independent variables.

I believe that is the function. Hopefully this wasn't too confusing, it is very statsy, but its a fun function for me! I use Random Forest excessively in R and always like to try to convert R things to Pinescript.

Hope you enjoy!

Safe trades everyone!

Weekly Bullish Pattern DetectorThis script is a TradingView Pine Script designed to detect a specific bullish candlestick pattern on the weekly chart. Below is a detailed breakdown of its components:

1. Purpose

The script identifies a four-candle bullish pattern where:

The first candle is a long green (bullish) candlestick.

The second and third candles are small-bodied candles, signifying consolidation or indecision.

The fourth candle is another long green (bullish) candlestick.

When this pattern is detected, the script:

Marks the chart with a visual label.

Optionally triggers an alert to notify the trader.

2. Key Features

Overlay on Chart:

indicator("Weekly Bullish Pattern Detector", overlay=true) ensures the indicator draws directly on the price chart.

Customizable Inputs:

length (Body Size Threshold):

Defines the minimum percentage of the total range that qualifies as a "long" candle body (default: 14%).

smallCandleThreshold (Small Candle Body Threshold):

Defines the maximum percentage of the total range that qualifies as a "small" candle body (default: 10%).

Candlestick Property Calculations:

bodySize: Measures the absolute size of the candle body (close - open).

totalRange: Measures the total high-to-low range of the candle.

bodyPercentage: Calculates the proportion of the body size relative to the total range ((bodySize / totalRange) * 100).

isGreen and isRed: Identify bullish (green) or bearish (red) candles based on their open and close prices.

Pattern Conditions:

longGreenCandle:

Checks if the candle is bullish (isGreen) and its body percentage exceeds the defined length threshold.

smallCandle:

Identifies small-bodied candles where the body percentage is below the smallCandleThreshold.

consolidation:

Confirms the second and third candles are both small-bodied (smallCandle and smallCandle ).

Bullish Pattern Detection:

bullishPattern:

Detects the full four-candle sequence:

The first candle (longGreenCandle ) is a long green candle.

The second and third candles (consolidation) are small-bodied.

The fourth candle (longGreenCandle) is another long green candle.

Visualization:

plotshape(bullishPattern):

Draws a green label ("Pattern") below the price chart whenever the pattern is detected.

Alert Notification:

alertcondition(bullishPattern):

Sends an alert with the message "Bullish Pattern Detected on Weekly Chart" whenever the pattern is found.

3. How It Works

Evaluates Candle Properties:

For each weekly candle, the script calculates its size, range, and body percentage.

Identifies Each Component of the Pattern:

Checks for a long green candle (first and fourth).

Verifies the presence of two small-bodied candles (second and third).

Detects and Marks the Pattern:

Confirms the sequence and marks the chart with a label if the pattern is complete.

Sends Alerts:

Notifies the trader when the pattern is detected.

4. Use Cases

This script is ideal for:

Swing Traders:

Spotting weekly patterns that indicate potential bullish continuations.

Breakout Traders:

Identifying consolidation zones followed by upward momentum.

Pattern Recognition:

Automatically detecting a commonly used bullish formation.

5. Key Considerations

Timeframe: Works best on weekly charts.

Customization: The thresholds for "long" and "small" candles can be adjusted to suit different markets or volatility levels.

Limitations:

It doesn't confirm the pattern's success; further analysis (e.g., volume, support/resistance levels) may be required for validation

ATR% Multiple from Key Moving AverageThis script gives signal when the ATR% multiple from any chosen moving average is beyond the configurable threshold value. This indicator quantifies how extended the stock is from a given key moving average.

A lot of traders use ATR% multiple from 10DMA, 21EMA, 50SMA or 200SMA to determine how extended a stock is and accordingly sell partials or exit. By default the indicator takes 50SMA and when the ATR% multiple is greater than 7 then it gives the signal to take partials. You can back test this indicator with previous trades and determine the ideal threshold for the signal. For small and midcaps a threshold of 7 to 10 ATR% multiples from 50SMA is where partials can be taken while large caps can revert to mean even earlier at 3 to 5 ATR% multiples from 50SMA.

You can modify this script and use it anyway you please as long as you make it opensource on TradingView.

Hybrid Triple Exponential Smoothing🙏🏻 TV, I present you HTES aka Hybrid Triple Exponential Smoothing, designed by Holt & Winters in the US, assembled by me in Saint P. I apply exponential smoothing individually to the data itself, then to residuals from the fitted values, and lastly to one-point forecast (OPF) errors, hence 'hybrid'. At the same time, the method is a closed-form solution and purely online, no need to make any recalculations & optimize anything, so the method is O(1).

^^ historical OPFs and one-point forecasting interval plotted instead of fitted values and prediction interval

Before the How-to, first let me tell you some non-obvious things about Triple Exponential smoothing (and about Exponential Smoothing in general) that not many catch. Expo smoothing seems very straightforward and obvious, but if you look deeper...

1) The whole point of exponential smoothing is its incremental/online nature, and its O(1) algorithm complexity, making it dope for high-frequency streaming data that is also univariate and has no weights. Consequently:

- Any hybrid models that involve expo smoothing and any type of ML models like gradient boosting applied to residuals rarely make much sense business-wise: if you have resources to boost the residuals, you prolly have resources to use something instead of expo smoothing;

- It also concerns the fashion of using optimizers to pick smoothing parameters; honestly, if you use this approach, you have to retrain on each datapoint, which is crazy in a streaming context. If you're not in a streaming context, why expo smoothing? What makes more sense is either picking smoothing parameters once, guided by exogenous info, or using dynamic ones calculated in a minimalistic and elegant way (more on that in further drops).

2) No matter how 'right' you choose the smoothing parameters, all the resulting components (level, trend, seasonal) are not pure; each of them contains a bit of info from the other components, this is just how non-sequential expo smoothing works. You gotta know this if you wanna use expo smoothing to decompose your time series into separate components. The only pure component there, lol, is the residuals;

3) Given what I've just said, treating the level (that does contain trend and seasonal components partially) as the resulting fit is a mistake. The resulting fit is level (l) + trend (b) + seasonal (s). And from this fit, you calculate residuals;

4) The residuals component is not some kind of bad thing; it is simply the component that contains info you consciously decide not to include in your model for whatever reason;

5) Forecasting Errors and Residuals from fitted values are 2 different things. The former are deltas between the forecasts you've made and actual values you've observed, the latter are simply differences between actual datapoints and in-sample fitted values;

6) Residuals are used for in-sample prediction intervals, errors for out-of-sample forecasting intervals;

7) Choosing between single, double, or triple expo smoothing should not be based exclusively on the nature of your data, but on what you need to do as well. For example:

- If you have trending seasonal data and you wanna do forecasting exclusively within the expo smoothing framework, then yes, you need Triple Exponential Smoothing;

- If you wanna use prediction intervals for generating trend-trading signals and you disregard seasonality, then you need single (simple) expo smoothing, even on trending data. Otherwise, the trend component will be included in your model's fitted values → prediction intervals.

8) Kind of not non-obvious, but when you put one smoothing parameter to zero, you basically disregard this component. E.g., in triple expo smoothing, when you put gamma and beta to zero, you basically end up with single exponential smoothing.

^^ data smoothing, beta and gamma zeroed out, forecasting steps = 0

About the implementation

* I use a simple power transform that results in a log transform with lambda = 0 instead of the mainstream-used transformers (if you put lambda on 2 in Box-Cox, you won't get a power of 2 transform)

* Separate set of smoothing parameters for data, residuals, and errors smoothing

* Separate band multipliers for residuals and errors

* Both typical error and typical residuals get multiplied by math.sqrt(math.pi / 2) in order to approach standard deviation so you can ~use Z values and get more or less corresponding probabilities

* In script settings → style, you can switch on/off plotting of many things that get calculated internally:

- You can visualize separate components (just remember they are not pure);

- You can switch off fit and switch on OPF plotting;

- You can plot residuals and their exponentially smoothed typical value to pick the smoothing parameters for both data and residuals;

- Or you might plot errors and play with data smoothing parameters to minimize them (consult SAE aka Sum of Absolute Errors plot);

^^ nuff said

More ideas on how to use the thing

1) Use Double Exponential Smoothing (data gamma = 0) to detrend your time series for further processing (Fourier likes at least weakly stationary data);

2) Put single expo smoothing on your strategy/subaccount equity chart (data alpha = data beta = 0), set prediction interval deviation multiplier to 1, run your strat live on simulator, start executing on real market when equity on simulator hits upper deviation (prediction interval), stop trading if equity hits lower deviation on simulator. Basically, let the strat always run on simulator, but send real orders to a real market when the strat is successful on your simulator;

3) Set up the model to minimize one-point forecasting errors, put error forecasting steps to 1, now you're doing nowcasting;

4) Forecast noisy trending sine waves for fun.

^^ nuff said 2

All Good TV ∞