[AWC] Vector -AYNETThis Pine Script code is a custom indicator designed for TradingView. Its purpose is to visualize the opening and closing prices of a specific timeframe (e.g., weekly, daily, or monthly) by drawing lines between these price points whenever a new bar forms in the specified timeframe. Below is a detailed explanation from a scientific perspective:

1. Input Parameters

The code includes user-defined inputs to customize its functionality:

tf1: This input defines the timeframe (e.g., 'W' for weekly, 'D' for daily). It determines the periodicity for analyzing price data.

icol: This input specifies the color of the lines drawn on the chart. Users can select from predefined options such as black, red, or blue.

2. Color Assignment

A switch statement maps the user’s color selection (icol) to the corresponding color object in Pine Script. This mapping ensures that the drawn lines adhere to the user's preference.

3. New Bar Detection

The script uses the ta.change(time(tf1)) function to determine when a new bar forms in the specified timeframe (tf1):

ta.change checks if the timestamp of the current bar differs from the previous one within the selected timeframe.

If the value changes, it indicates that a new bar has formed, and further calculations are triggered.

4. Data Request

The script employs request.security to fetch price data from the specified timeframe:

o1: Retrieves the opening price of the previous bar.

c1: Calculates the average price (high, low, close) of the previous bar using the hlc3 formula.

These values represent the key price levels for visualizing the line.

5. Line Drawing

When a new bar is detected:

The script uses line.new to create a line connecting the previous bar's opening price (o1) and the closing price (c1).

The line’s properties are defined as follows:

x1, y1: The starting point corresponds to the opening price at the previous bar index.

x2, y2: The endpoint corresponds to the closing price at the current bar index.

color: Uses the user-defined color (col).

style: The line style is set to line.style_arrow_right.

Additionally, the lines are stored in an array (lines) for later reference, enabling potential modifications or deletions.

6. Visual Outcome

The script visually represents price movements over the specified timeframe:

Each line connects the opening and closing price of a completed bar in the given timeframe.

The lines are drawn dynamically, updating whenever a new bar forms.

Scientific Context

This script applies concepts of time series analysis and visualization in financial data:

Time Segmentation: By isolating specific timeframes (e.g., weekly), the script provides a focused analysis of price behavior.

Price Dynamics: Connecting opening and closing prices highlights key price transitions within each period.

User Customization: The inclusion of inputs allows for adaptable use, accommodating different analytical preferences.

Applications

Trend Analysis: Identifies how price evolves between opening and closing levels across periods.

Market Behavior Comparison: Facilitates the observation of patterns or anomalies in price transitions over time.

Technical Indicators: Serves as a supplementary tool for decision-making in trading strategies.

If further enhancements or customizations are needed, let me know! 😊

Forecasting

Star of David Drawing-AYNETExplanation of Code

Settings:

centerTime defines the center time for the star pattern, defaulting to January 1, 2023.

centerPrice is the center Y-axis level for positioning the star.

size controls the overall size of the star.

starColor and lineWidth allow customization of the color and thickness of the lines.

Utility Function:

toRadians converts degrees to radians, though it’s not directly used here, it might be useful for future adjustments to angles.

Star of David Drawing Function:

The drawStarOfDavid function calculates the position of each point on the star relative to the center coordinates (centerTime, centerY) and size.

The pattern has six key points that form two overlapping triangles, creating the Star of David pattern.

The time offsets (offset1 and offset2) determine the horizontal spread of the star, scaling according to size.

The line.new function is used to draw the star lines with the calculated coordinates, casting timestamps to int to comply with line.new requirements.

Star Rendering:

Finally, drawStarOfDavid is called to render the Star of David pattern on the chart based on the input parameters.

This code draws the Star of David on a chart at a specified time and price level, with customizable size, color, and line width. Adjust centerTime, centerPrice, and size as needed for different star placements on the chart.

Straddle Charts - Live

Description :

This indicator is designed to display live prices for both call and put options of a straddle strategy, helping traders visualize the real-time performance of their options positions. The indicator allows users to select the symbols for specific call and put options and fetches their prices on a 1-minute timeframe, ensuring updated information.

Key Features :

Live Call and Put Option Prices: View individual prices for both call and put options of the straddle, plotted separately.

Straddle Price Calculation: The total price of the straddle (sum of call and put) is displayed, allowing for easy monitoring of the straddle’s combined movement.

Customizable Inputs: Easily change the call and put option symbols directly from the settings.

Use this indicator to stay on top of your straddle's value and make informed trading decisions based on real-time data.

Holt-Winters Forecast BandsDescription:

The Holt-Winters Adaptive Bands indicator combines seasonal trend forecasting with adaptive volatility bands. It uses the Holt-Winters triple exponential smoothing model to project future price trends, while Nadaraya-Watson smoothed bands highlight dynamic support and resistance zones.

This indicator is ideal for traders seeking to predict future price movements and visualize potential market turning points. By focusing on broader seasonal and trend data, it provides insight into both short- and long-term market directions. It’s particularly effective for swing trading and medium-to-long-term trend analysis on timeframes like daily and 4-hour charts, although it can be adjusted for other timeframes.

Key Features:

Holt-Winters Forecast Line: The core of this indicator is the Holt-Winters model, which uses three components — level, trend, and seasonality — to project future prices. This model is widely used for time-series forecasting, and in this script, it provides a dynamic forecast line that predicts where price might move based on historical patterns.

Adaptive Volatility Bands: The shaded areas around the forecast line are based on Nadaraya-Watson smoothing of historical price data. These bands provide a visual representation of potential support and resistance levels, adapting to recent volatility in the market. The bands' fill colors (red for upper and green for lower) allow traders to identify potential reversal zones without cluttering the chart.

Dynamic Confidence Levels: The indicator adapts its forecast based on market volatility, using inputs such as average true range (ATR) and price deviations. This means that in high-volatility conditions, the bands may widen to account for increased price movements, helping traders gauge the current market environment.

How to Use:

Forecasting: Use the forecast line to gain insight into potential future price direction. This line provides a directional bias, helping traders anticipate whether the price may continue along a trend or reverse.

Support and Resistance Zones: The shaded bands act as dynamic support and resistance zones. When price enters the upper (red) band, it may be in an overbought area, while the lower (green) band may indicate oversold conditions. These bands adjust with volatility, so they reflect the current market conditions rather than fixed levels.

Timeframe Recommendations:

This indicator performs best on daily and 4-hour charts due to its reliance on trend and seasonality. It can be used on lower timeframes, but accuracy may vary due to increased price noise.

For traders looking to capture swing trades, the daily and 4-hour timeframes provide a balance of trend stability and signal reliability.

Adjustable Settings:

Alpha, Beta, and Gamma: These settings control the level, trend, and seasonality components of the forecast. Alpha is generally the most sensitive setting for adjusting responsiveness to recent price movements, while Beta and Gamma help fine-tune the trend and seasonal adjustments.

Band Smoothing and Deviation: These settings control the lookback period and width of the volatility bands, allowing users to customize how closely the bands follow price action.

Parameters:

Prediction Length: Sets the length of the forecast, determining how far into the future the prediction line extends.

Season Length: Defines the seasonality cycle. A setting of 14 is typical for bi-weekly cycles, but this can be adjusted based on observed market cycles.

Alpha, Beta, Gamma: These parameters adjust the Holt-Winters model's sensitivity to recent prices, trends, and seasonal patterns.

Band Smoothing: Determines the smoothing applied to the bands, making them either more reactive or smoother.

Ideal Use Cases:

Swing Trading and Trend Following: The Holt-Winters model is particularly suited for capturing larger market trends. Use the forecast line to determine trend direction and the bands to gauge support/resistance levels for potential entries or exits.

Identifying Reversal Zones: The adaptive bands act as dynamic overbought and oversold zones, giving traders potential reversal areas when price reaches these levels.

Important Notes:

No Buy/Sell Signals: This indicator does not produce direct buy or sell signals. It’s intended for visual trend analysis and support/resistance identification, leaving trade decisions to the user.

Not for High-Frequency Trading: Due to the nature of the Holt-Winters model, this indicator is optimized for higher timeframes like the daily and 4-hour charts. It may not be suitable for high-frequency or scalping strategies on very short timeframes.

Adjust for Volatility: If using the indicator on lower timeframes or more volatile assets, consider adjusting the band smoothing and prediction length settings for better responsiveness.

RSI-EMA Signal by stock shooter## Strategy Description: 200 EMA Crossover with RSI, Green/Red Candles, Volume, and Exit Conditions

This strategy combines several technical indicators to identify potential long and short entry opportunities in a trading instrument. Here's a breakdown of its components:

1. 200-period Exponential Moving Average (EMA):

* The 200-period EMA acts as a long-term trend indicator.

* The strategy looks for entries when the price is above (long) or below (short) the 200 EMA.

2. Relative Strength Index (RSI):

* The RSI measures the momentum of price movements and helps identify overbought and oversold conditions.

* The strategy looks for entries when the RSI is below 40 (oversold) for long positions and above 60 (overbought) for short positions.

3. Green/Red Candles:

* This indicator filters out potential entries based on the current candle's closing price relative to its opening price.

* The strategy only considers long entries on green candles (closing price higher than opening) and short entries on red candles (closing price lower than opening).

4. Volume:

* This indicator adds a volume filter to the entry conditions.

* The strategy only considers entries when the current candle's volume is higher than the average volume of the previous 20 candles, aiming for stronger signals.

Overall:

This strategy aims to capture long opportunities during potential uptrends and short opportunities during downtrends, based on a combination of price action, momentum, and volume confirmation.

Important Notes:

Backtesting is crucial to evaluate the historical performance of this strategy before deploying it with real capital.

Consider incorporating additional risk management techniques like stop-loss orders.

This strategy is just a starting point and can be further customized based on your trading goals and risk tolerance.

Direction Coefficient Indicator# Direction Coefficient Indicator with Advanced Volume & Volatility Adjustments

The Direction Coefficient Indicator represents an advanced technical analysis tool that combines price momentum analysis with sophisticated volume and volatility adjustments. This versatile indicator measures market direction while adapting to various trading conditions, making it valuable for both trend following and momentum trading strategies.

At its core, the indicator employs a unique approach to price analysis by establishing a dynamic reference period for calculations. It processes price data through an EMA smoothing mechanism to reduce market noise and presents results as percentage-based measurements, ensuring universal applicability across different markets and timeframes.

One of the indicator's standout features is its volume integration system. When enabled, this system implements volume-weighted calculations that provide enhanced accuracy during significant market moves while effectively reducing false signals during low-volume periods. This volume weighting mechanism proves particularly valuable in highly liquid markets where volume plays a crucial role in price movement validation.

The volatility adjustment feature sets this indicator apart from traditional momentum tools. By incorporating smart volatility normalization, the indicator adapts seamlessly to changing market conditions. This adjustment helps maintain consistent signals across different volatility regimes, preventing excessive noise during highly volatile periods while remaining sensitive enough during calmer market phases.

Direction change detection forms another crucial component of the indicator. The system continuously monitors momentum shifts and provides early warning signals for potential trend reversals. This feature helps traders avoid late exits from positions and offers valuable insights for potential market turning points. When the indicator detects significant changes in momentum, it displays a warning symbol (⚠) alongside its regular signals.

The visual presentation of the indicator utilizes an intuitive color-coded system. Green labels indicate positive momentum, while red labels signify negative momentum. The display system includes customizable label sizes and positions, allowing traders to adapt the visual elements to their specific chart setup and preferences. Label distance from candles, color schemes, and reference lines can all be adjusted to create an optimal visual experience.

For practical application, the indicator offers several parameter settings that traders can adjust. The time period parameters include adjustable lookback periods and EMA length, while advanced calculation options allow for enabling or disabling volume weighting and volatility adjustment features. These parameters can be fine-tuned based on specific trading timeframes and market conditions.

In trend following scenarios, traders can use the coefficient direction for trend confirmation while monitoring warning signals for potential exits. The volume weighting feature adds another layer of confirmation for trend strength. For momentum trading, strong coefficient readings can signal entry points, while warning signals help identify potential exit timing.

Risk management becomes more systematic with this indicator. Warning signals can guide stop loss placement, while the volatility adjustment feature assists in position sizing decisions. The volume weighting component helps traders evaluate the significance of price moves, contributing to more informed entry timing decisions.

The indicator performs optimally when traders start with default settings and gradually adjust parameters based on their specific needs. For longer-term trades, increasing the lookback period often provides more stable signals. In highly liquid markets, enabling volume weighting can enhance signal quality. The volatility adjustment feature proves particularly valuable during unstable market conditions.

The Direction Coefficient Indicator stands as a comprehensive solution for traders seeking a sophisticated yet practical approach to market analysis. By combining multiple analytical components into a single, customizable tool, it provides valuable insights while remaining accessible to traders of various experience levels.

For optimal results, traders should consider using this indicator in conjunction with other technical analysis tools while paying attention to its warning signals and volume-weighted insights. Regular parameter adjustment based on changing market conditions and specific trading styles will help maximize the indicator's effectiveness in various trading scenarios.

Indicateur de Coefficient Directeur

L'Indicateur de Coefficient Directeur représente un outil d'analyse technique avancé qui combine l'analyse de momentum des prix avec des ajustements sophistiqués de volume et de volatilité. Cet indicateur polyvalent mesure la direction du marché tout en s'adaptant à diverses conditions de trading, le rendant précieux tant pour le suivi de tendance que pour les stratégies de trading momentum.

À sa base, l'indicateur emploie une approche unique de l'analyse des prix en établissant une période de référence dynamique pour les calculs. Il traite les données de prix à travers un mécanisme de lissage EMA pour réduire le bruit du marché et présente les résultats sous forme de mesures en pourcentage, assurant une applicabilité universelle à travers différents marchés et temporalités.

L'une des caractéristiques distinctives de l'indicateur est son système d'intégration du volume. Lorsqu'il est activé, ce système met en œuvre des calculs pondérés par le volume qui fournissent une précision accrue pendant les mouvements significatifs du marché tout en réduisant efficacement les faux signaux pendant les périodes de faible volume. Ce mécanisme de pondération du volume s'avère particulièrement valuable dans les marchés très liquides où le volume joue un rôle crucial dans la validation des mouvements de prix.

La fonction d'ajustement de la volatilité distingue cet indicateur des outils de momentum traditionnels. En incorporant une normalisation intelligente de la volatilité, l'indicateur s'adapte parfaitement aux conditions changeantes du marché. Cet ajustement aide à maintenir des signaux cohérents à travers différents régimes de volatilité, empêchant le bruit excessif pendant les périodes très volatiles tout en restant suffisamment sensible pendant les phases de marché plus calmes.

La détection des changements de direction forme une autre composante cruciale de l'indicateur. Le système surveille continuellement les changements de momentum et fournit des signaux d'avertissement précoces pour les potentiels renversements de tendance. Cette fonctionnalité aide les traders à éviter les sorties tardives des positions et offre des aperçus précieux des potentiels points de retournement du marché. Lorsque l'indicateur détecte des changements significatifs de momentum, il affiche un symbole d'avertissement (⚠) à côté de ses signaux réguliers.

La présentation visuelle de l'indicateur utilise un système intuitif codé par couleurs. Les étiquettes vertes indiquent un momentum positif, tandis que les étiquettes rouges signifient un momentum négatif. Le système d'affichage inclut des tailles et positions d'étiquettes personnalisables, permettant aux traders d'adapter les éléments visuels à leur configuration spécifique de graphique et leurs préférences. La distance des étiquettes par rapport aux bougies, les schémas de couleurs et les lignes de référence peuvent tous être ajustés pour créer une expérience visuelle optimale.

Pour l'application pratique, l'indicateur offre plusieurs paramètres de réglage que les traders peuvent ajuster. Les paramètres de période temporelle incluent des périodes de référence ajustables et la longueur de l'EMA, tandis que les options de calcul avancées permettent d'activer ou de désactiver les fonctionnalités de pondération du volume et d'ajustement de la volatilité. Ces paramètres peuvent être affinés en fonction des temporalités de trading spécifiques et des conditions de marché.

Dans les scénarios de suivi de tendance, les traders peuvent utiliser la direction du coefficient pour la confirmation de tendance tout en surveillant les signaux d'avertissement pour les sorties potentielles. La fonction de pondération du volume ajoute une couche supplémentaire de confirmation pour la force de la tendance. Pour le trading momentum, des lectures fortes du coefficient peuvent signaler des points d'entrée, tandis que les signaux d'avertissement aident à identifier le timing potentiel de sortie.

La gestion du risque devient plus systématique avec cet indicateur. Les signaux d'avertissement peuvent guider le placement des stops loss, tandis que la fonction d'ajustement de la volatilité aide aux décisions de dimensionnement des positions. La composante de pondération du volume aide les traders à évaluer l'importance des mouvements de prix, contribuant à des décisions de timing d'entrée plus éclairées.

L'indicateur fonctionne de manière optimale lorsque les traders commencent avec les paramètres par défaut et ajustent progressivement les paramètres en fonction de leurs besoins spécifiques. Pour les trades à plus long terme, l'augmentation de la période de référence fournit souvent des signaux plus stables. Dans les marchés très liquides, l'activation de la pondération du volume peut améliorer la qualité des signaux. La fonction d'ajustement de la volatilité s'avère particulièrement précieuse pendant les conditions de marché instables.

L'Indicateur de Coefficient Directeur s'impose comme une solution complète pour les traders recherchant une approche sophistiquée mais pratique de l'analyse de marché. En combinant plusieurs composantes analytiques en un seul outil personnalisable, il fournit des aperçus précieux tout en restant accessible aux traders de différents niveaux d'expérience.

Pour des résultats optimaux, les traders devraient envisager d'utiliser cet indicateur en conjonction avec d'autres outils d'analyse technique tout en prêtant attention à ses signaux d'avertissement et ses aperçus pondérés par le volume. L'ajustement régulier des paramètres basé sur les conditions changeantes du marché et les styles de trading spécifiques aidera à maximiser l'efficacité de l'indicateur dans divers scénarios de trading.

Financial X-RayThe Financial X-Ray is an advanced indicator designed to provide a thorough analysis of a company's financial health and market performance. Its primary goal is to offer investors and analysts a quick yet comprehensive overview of a company's financial situation by combining various key financial ratios and metrics.

How It Works

Data Collection: The indicator automatically extracts a wide range of financial data for the company, covering aspects such as financial strength, profitability, valuation, growth, and operational efficiency.

Sector-Specific Normalization: A unique feature of this indicator is its ability to normalize metrics based on the company's industry sector. This approach allows for more relevant comparisons between companies within the same sector, taking into account industry-specific characteristics.

Standardized Scoring: Each metric is converted to a score on a scale of 0 to 10, facilitating easy comparison and rapid interpretation of results.

Multidimensional Analysis: The indicator doesn't focus on just one financial dimension but offers an overview by covering several crucial aspects of a company's performance.

Fair Value Calculation: Using financial data and market conditions, the indicator provides an estimate of the company's fair value, offering a reference point for assessing current valuation.

Visual Presentation: Results are displayed directly on the TradingView chart in a tabular format, allowing for quick and efficient reading of key information.

Advantages for Users

Time-Saving: Instead of manually collecting and analyzing numerous financial data points, users get an instant comprehensive overview.

Contextual Analysis: Sector-specific normalization allows for a better understanding of the company's performance relative to its peers.

Flexibility: Users can choose which metrics to display, customizing the analysis to their specific needs.

Objectivity: By relying on quantitative data and standardized calculations, the indicator offers an objective perspective on the company's financial health.

Decision Support: The fair value estimate and normalized scores provide valuable reference points for investment decision-making.

Customization and Evolution

One of the major strengths of this indicator is its open-source nature. Users can modify the code to adjust normalization methods, add new metrics, or adapt the display to their preferences. This flexibility allows the indicator to evolve and continuously improve through community contributions.

In summary, the Financial X-Ray is a powerful tool that combines automation, contextual analysis, and customization to provide investors with a clear and comprehensive view of companies' financial health, facilitating informed decision-making in financial markets.

This Financial X-Ray indicator is provided for informational and educational purposes only. It should not be considered as financial advice or a recommendation to buy or sell any security. The data and calculations used in this indicator may not be accurate or up-to-date. Users should always conduct their own research and consult with a qualified financial advisor before making any investment decisions. The creator of this indicator is not responsible for any losses or damages resulting from its use.

Central Bank Liquidity YOY % Change - Second DerivativeThis indicator measures the acceleration or deceleration in the yearly growth rate of central bank liquidity.

By calculating the year-over-year percentage change of the YoY growth rate, it highlights shifts in the pace of liquidity changes, providing insights into market momentum or potential reversals influenced by central bank actions.

This can help reveal impulses in liquidity by identifying changes in the growth rate's acceleration or deceleration. When central bank liquidity experiences a rapid increase or decrease, the second derivative captures these shifts as sharp upward or downward movements.

These impulses often signal pivotal liquidity shifts, which may correspond to major policy changes, market interventions, or financial stability measures, offering an early signal of potential market impacts.

CAGR ProjectionThe CAGR Projection Indicator is a tool designed to visualize the potential growth of an asset over time based on a specified annual growth rate. This indicator overlays a projection line on the price chart, allowing traders and investors to compare actual price movements with a hypothetical growth trajectory.

One of the key features of this indicator is the ability for users to input their expected annual growth rate as a percentage. This flexibility allows for various scenarios to be modeled, from conservative estimates to more optimistic projections. Additionally, the indicator allows users to set a specific start date for the projection, enabling analysis from any chosen point in time.

The projection calculation is dynamic, adjusting for different timeframes and updating with each new bar on the chart. The indicator initializes either at the specified start date or when the first valid price is encountered. Using the initial price as a base, the indicator calculates the projected price for each subsequent bar using the compound growth formula. The calculation accounts for the specific timeframe of the chart, ensuring accurate projections regardless of whether the chart displays daily, weekly, or other intervals.

The projected growth is plotted as a blue line on the chart, providing a clear visual comparison between the actual price movement and the hypothetical growth trajectory. This visual representation makes it easy for users to quickly assess how an asset is performing relative to the expected growth rate.

This tool has several practical applications. Investors can use it to set realistic growth targets for their investments. By comparing actual price movements to the projection line, users can quickly assess if an asset is outperforming or underperforming relative to the expected growth rate. Furthermore, multiple instances of the indicator can be used with different growth rates to visualize various potential outcomes, facilitating scenario analysis.

The indicator also offers customization options, such as displaying a label showing the annual growth rate used for the projection, and the ability to adjust the color of the projection line to suit individual preferences or chart setups.

In summary, this CAGR Projection indicator serves as a valuable tool for both long-term investors and traders, offering a simple yet effective way to visualize potential growth scenarios and assess investment performance over time. It combines ease of use with powerful analytical capabilities, making it a useful addition to any trader's or investor's toolkit.

Crypto Wallets Profitability & Performance [LuxAlgo]The Crypto Wallets Profitability & Performance indicator provides a comprehensive view of the financial status of cryptocurrency wallets by leveraging on-chain data from IntoTheBlock. It measures the percentage of wallets profiting, losing, or breaking even based on current market prices.

Additionally, it offers performance metrics across different timeframes, enabling traders to better assess market conditions.

This information can be crucial for understanding market sentiment and making informed trading decisions.

🔶 USAGE

🔹 Wallets Profitability

This indicator is designed to help traders and analysts evaluate the profitability of cryptocurrency wallets in real-time. It aggregates data gathered from the blockchain on the number of wallets that are in profit, loss, or breaking even and presents it visually on the chart.

Breaking even line demonstrates how realized gains and losses have changed, while the profit and the loss monitor unrealized gains and losses.

The signal line helps traders by providing a smoothed average and highlighting areas relative to profiting and losing levels. This makes it easier to identify and confirm trading momentum, assess strength, and filter out market noise.

🔹 Profitability Meter

The Profitability Meter is an alternative display that visually represents the percentage of wallets that are profiting, losing, or breaking even.

🔹 Performance

The script provides a view of the financial health of cryptocurrency wallets, showing the percentage of wallets in profit, loss, or breaking even. By combining these metrics with performance data across various timeframes, traders can gain valuable insights into overall wallet performance, assess trend strength, and identify potential market reversals.

🔹 Dashboard

The dashboard presents a consolidated view of key statistics. It allows traders to quickly assess the overall financial health of wallets, monitor trend strength, and gauge market conditions.

🔶 DETAILS

🔹 The Chart Occupation Option

The chart occupation option adjusts the occupation percentage of the chart to balance the visibility of the indicator.

🔹 The Height in Performance Options

Crypto markets often experience significant volatility, leading to rapid and substantial gains or losses. Hence, plotting performance graphs on top of the chart alongside other indicators can result in a cluttered display. The height option allows you to adjust the plotting for balanced visibility, ensuring a clearer and more organized chart.

🔶 SETTINGS

The script offers a range of customizable settings to tailor the analysis to your trading needs.

Chart Occupation %: Adjust the occupation percentage of the chart to balance the visibility of the indicator.

🔹 Profiting Wallets

Profiting Percentage: Toggle to display the percentage of wallets in profit.

Smoothing: Adjust the smoothing period for the profiting percentage line.

Signal Line: Choose a signal line type (SMA, EMA, RMA, or None) to overlay on the profiting percentage.

🔹 Losing Wallets

Losing Percentage: Toggle to display the percentage of wallets in loss.

Smoothing: Adjust the smoothing period for the losing percentage line.

Signal Line: Choose a signal line type (SMA, EMA, RMA, or None) to overlay on the losing percentage.

🔹 Breaking Even Wallets

Breaking-Even Percentage: Toggle to display the percentage of wallets breaking even.

Smoothing: Adjust the smoothing period for the breaking-even percentage line.

🔹 Profitability Meter

Profitability Meter: Enable or disable the meter display, set its width, and adjust the offset.

🔹 Performance

Performance Metrics: Choose the timeframe for performance metrics (Day to Date, Week to Date, etc.).

Height: Adjust the height of the chart visuals to balance the visibility of the indicator.

🔹 Dashboard

Block Profitability Stats: Toggle the display of profitability stats.

Performance Stats: Toggle the display of performance stats.

Dashboard Size and Position: Customize the size and position of the performance dashboard on the chart.

🔶 RELATED SCRIPTS

Market-Sentiment-Technicals

Multi-Chart-Widget

Systematic Investment Tracker by Ceyhun Gonul### English Description

**Systematic Investment Tracker with Enhanced Features**

This script, titled **Systematic Investment Tracker with Enhanced Features**, is a TradingView tool designed to support systematic investments across different market conditions. It provides traders with two customizable investment strategies — **Continuous Buying** and **Declining Buying** — and includes advanced dynamic investment adjustment features for each.

#### Detailed Explanation of Script Features and Originality

1. **Two Investment Strategies**:

- **Continuous Buying**: This strategy performs purchases consistently at each interval, as set by the user, regardless of market price changes. It follows the principle of dollar-cost averaging, allowing users to build an investment position over time.

- **Declining Buying**: Unlike Continuous Buying, this strategy triggers purchases only when the asset's price has declined from the previous interval's closing price. This approach helps users capitalize on lower price points, potentially improving average costs during downward trends.

2. **Dynamic Investment Adjustment**:

- For both strategies, the script includes a **Dynamic Investment Adjustment** feature. If enabled, this feature increases the purchasing amount by 50% if the current price has fallen by a specific user-defined percentage relative to the previous price. This allows users to accumulate a larger position when the asset is declining, which may benefit long-term cost-averaging strategies.

3. **Customizable Time Frames**:

- Users can specify a **start and end date** for investment, allowing them to restrict or backtest strategies within a specific timeframe. This feature is valuable for evaluating strategy performance over specific market cycles or historical periods.

4. **Graphical Indicators and Labels**:

- The script provides graphical labels on the chart that display purchase points. These indicators help users visualize their investment entries based on the strategy selected.

- A summary **performance label** is also displayed, providing real-time updates on the total amount spent, accumulated quantity, average cost, portfolio value, and profit percentage for each strategy.

5. **Language Support**:

- The script includes English and Turkish language options. Users can toggle between these languages, allowing the summary label text and descriptions to be displayed in their preferred language.

6. **Performance Comparison Table**:

- An optional **Performance Comparison Table** is available, offering a side-by-side analysis of net profit, total investment, and profit percentage for both strategies. This comparison table helps users assess which strategy has yielded better returns, providing clarity on each approach's effectiveness under the chosen parameters.

#### How the Script Works and Its Uniqueness

This closed-source script brings together two established investment strategies in a single, dynamic tool. By integrating continuous and declining purchase strategies with advanced settings for dynamic investment adjustment, the script offers a powerful, flexible tool for both passive and active investors. The design of this script provides unique benefits:

- Enables automated, systematic investment tracking, allowing users to build positions gradually.

- Empowers users to leverage declines through dynamic adjustments to optimize average cost over time.

- Presents an easy-to-read performance label and table, enabling an efficient and transparent performance comparison for informed decision-making.

---

### Türkçe Açıklama

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi**

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi** adlı bu TradingView scripti, çeşitli piyasa koşullarında sistematik yatırım stratejilerini desteklemek üzere tasarlanmış bir araçtır. Script, kullanıcıya iki özelleştirilebilir yatırım stratejisi — **Sürekli Alım** ve **Düşen Alım** — ve her strateji için gelişmiş dinamik yatırım ayarlama seçenekleri sunar.

#### Script Özelliklerinin Detaylı Açıklaması ve Özgünlük

1. **İki Yatırım Stratejisi**:

- **Sürekli Alım**: Bu strateji, fiyat değişimlerine bakılmaksızın kullanıcının belirlediği her aralıkta sabit bir miktar yatırım yapar. Bu yaklaşım, uzun vadede pozisyonu kademeli olarak oluşturmak isteyenler için idealdir.

- **Düşen Alım**: Sürekli Alım’ın aksine, bu strateji yalnızca fiyat bir önceki aralığın kapanış fiyatına göre düştüğünde alım yapar. Bu yöntem, yatırımcıların daha düşük fiyatlardan alım yaparak ortalama maliyeti potansiyel olarak iyileştirmelerine yardımcı olur.

2. **Dinamik Yatırım Ayarlaması**:

- Her iki strateji için de **Dinamik Yatırım Ayarlaması** özelliği bulunmaktadır. Bu özellik aktif edildiğinde, mevcut fiyatın bir önceki fiyata göre kullanıcı tarafından belirlenen bir yüzde oranında düşmesi durumunda alım miktarını %50 artırır. Bu durum, uzun vadede maliyet ortalaması stratejilerine katkıda bulunur.

3. **Özelleştirilebilir Tarih Aralığı**:

- Kullanıcılar, yatırımı belirli bir tarih aralığında sınırlandırmak veya test etmek için bir **başlangıç ve bitiş tarihi** belirleyebilir. Bu özellik, strateji performansını geçmiş piyasa döngüleri veya belirli dönemlerde değerlendirmek için kullanışlıdır.

4. **Grafiksel İşaretleyiciler ve Etiketler**:

- Script, grafik üzerinde alım noktalarını gösteren işaretleyiciler sağlar. Bu görsel göstergeler, kullanıcıların seçilen stratejiye göre yatırım girişlerini görselleştirmesine yardımcı olur.

- Ayrıca, her strateji için harcanan toplam tutar, biriken miktar, ortalama maliyet, portföy değeri ve kâr yüzdesi gibi bilgileri gerçek zamanlı olarak gösteren bir **performans etiketi** sunar.

5. **Dil Desteği**:

- Script, İngilizce ve Türkçe dillerini desteklemektedir. Kullanıcılar, performans etiketi metninin ve açıklamalarının tercih ettikleri dilde görüntülenmesi için dil seçimini yapabilir.

6. **Performans Karşılaştırma Tablosu**:

- İsteğe bağlı olarak kullanılabilen bir **Performans Karşılaştırma Tablosu**, her iki strateji için net kâr, toplam yatırım ve kâr yüzdesi gibi bilgileri yan yana analiz eder. Bu tablo, kullanıcıların hangi stratejinin daha yüksek getiri sağladığını değerlendirmesine yardımcı olur.

#### Scriptin Çalışma Prensibi ve Özgünlüğü

Bu script, iki yatırım stratejisini gelişmiş bir araçta birleştirir. Sürekli ve düşen fiyatlara dayalı alım stratejilerini dinamik yatırım ayarlama özelliğiyle entegre ederek yatırımcılar için güçlü ve esnek bir çözüm sunar. Script’in tasarımı aşağıdaki benzersiz faydaları sağlamaktadır:

- Otomatik, sistematik yatırım takibi yaparak kullanıcıların pozisyonlarını kademeli olarak oluşturmalarına olanak tanır.

- Dinamik ayarlama ile düşüşlerden yararlanarak zaman içinde ortalama maliyeti optimize etme olanağı sağlar.

- Her iki stratejinin performansını basit ve anlaşılır bir şekilde karşılaştıran etiket ve tablo ile verimli bir performans değerlendirmesi sunar.

No Trade Zone Indicator [CHE]No Trade Zone Indicator

The "No Trade Zone Indicator " is a powerful tool designed to help traders identify periods when the market may not present favorable trading opportunities. By analyzing the percentage change in the 20-period Simple Moving Average (SMA20) relative to a dynamically adjusted threshold based on market volatility, this indicator highlights times when it's prudent to stay out of the market.

Why Knowing When Not to Trade Is Important

Understanding when not to trade is just as crucial as knowing when to enter or exit a position. Trading during periods of low volatility or uncertain market direction can lead to unnecessary risks and potential losses. By recognizing these "No Trade Zones," you can:

- Avoid Low-Probability Trades: Reduce the chances of entering trades with unfavorable risk-to-reward ratios.

- Preserve Capital: Protect your investment from unpredictable market movements.

- Enhance Focus: Concentrate on high-quality trading opportunities that align with your strategy.

How the Indicator Works

- SMA20 Calculation: Computes the 20-period Simple Moving Average of closing prices to identify the market's short-term trend.

- ATR Measurement: Calculates the Average True Range (ATR) over a user-defined period (default is 14) to assess market volatility.

- Dynamic Threshold: Determines an adjusted threshold by multiplying the ATR percentage by a Threshold Adjustment Factor (default is 0.05).

- Trend Analysis: Compares the percentage change of the SMA20 against the adjusted threshold to evaluate market momentum.

- Status Identification:

- Long: Indicates a rising SMA20 above the threshold—suggesting a potential upward trend.

- Short: Indicates a falling SMA20 above the threshold—suggesting a potential downward trend.

- No Trade: Signals when the SMA20 change is below the threshold, marking a period of low volatility or indecision.

Features

- Customizable Settings: Adjust the ATR period and Threshold Adjustment Factor to suit different trading styles and market conditions.

- Visual Indicators: Colored columns represent market status—green for "Long," red for "Short," and gray for "No Trade."

- On-Chart Table: An optional table displays the current market status directly on your chart for quick reference.

- Alerts: Set up alerts to receive notifications when the market enters a "No Trade Zone," helping you stay informed without constant monitoring.

How to Use the Indicator

1. Add to Chart: Apply the "No Trade Zone Indicator " to your preferred trading chart on TradingView.

2. Configure Settings: Customize the ATR period and Threshold Adjustment Factor based on your analysis and risk tolerance.

3. Interpret Signals:

- Green Columns: Consider looking for buying opportunities as the market shows upward momentum.

- Red Columns: Consider looking for selling opportunities as the market shows downward momentum.

- Gray Columns: Refrain from trading as the market lacks clear direction.

4. Monitor Alerts: Use the alert feature to get notified when the market status changes, allowing you to make timely decisions.

Conclusion

Incorporating the "No Trade Zone Indicator " into your trading toolkit can enhance your decision-making process by clearly indicating when the market may not be conducive to trading. By focusing on periods with favorable conditions and avoiding low-volatility times, you can improve your trading performance and achieve better results over the long term.

*Trade wisely, and remember—the best trade can sometimes be no trade at all.*

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

best regards

Chervolino

High/Low Location Frequency [LuxAlgo]The High/Low Location Frequency tool provides users with probabilities of tops and bottoms at user-defined periods, along with advanced filters that offer deep and objective market information about the likelihood of a top or bottom in the market.

🔶 USAGE

There are four different time periods that traders can select for analysis of probabilities:

HOUR OF DAY: Probability of occurrence of top and bottom prices for each hour of the day

DAY OF WEEK: Probability of occurrence of top and bottom prices for each day of the week

DAY OF MONTH: Probability of occurrence of top and bottom prices for each day of the month

MONTH OF YEAR: Probability of occurrence of top and bottom prices for each month

The data is displayed as a dashboard, which users can position according to their preferences. The dashboard includes useful information in the header, such as the number of periods and the date from which the data is gathered. Additionally, users can enable active filters to customize their view. The probabilities are displayed in one, two, or three columns, depending on the number of elements.

🔹 Advanced Filters

Advanced Filters allow traders to exclude specific data from the results. They can choose to use none or all filters simultaneously, inputting a list of numbers separated by spaces or commas. However, it is not possible to use both separators on the same filter.

The tool is equipped with five advanced filters:

HOURS OF DAY: The permitted range is from 0 to 23.

DAYS OF WEEK: The permitted range is from 1 to 7.

DAYS OF MONTH: The permitted range is from 1 to 31.

MONTHS: The permitted range is from 1 to 12.

YEARS: The permitted range is from 1000 to 2999.

It should be noted that the DAYS OF WEEK advanced filter has been designed for use with tickers that trade every day, such as those trading in the crypto market. In such cases, the numbers displayed will range from 1 (Sunday) to 7 (Saturday). Conversely, for tickers that do not trade over the weekend, the numbers will range from 1 (Monday) to 5 (Friday).

To illustrate the application of this filter, we will exclude results for Mondays and Tuesdays, the first five days of each month, January and February, and the years 2020, 2021, and 2022. Let us review the results:

DAYS OF WEEK: `2,3` or `2 3` (for crypto) or `1,2` or `1 2` (for the rest)

DAYS OF MONTH: `1,2,3,4,5` or `1 2 3 4 5`

MONTHS: `1,2` or `1 2`

YEARS: `2020,2021,2022` or `2020 2021 2022`

🔹 High Probability Lines

The tool enables traders to identify the next period with the highest probability of a top (red) and/or bottom (green) on the chart, marked with two horizontal lines indicating the location of these periods.

🔹 Top/Bottom Labels and Periods Highlight

The tool is capable of indicating on the chart the upper and lower limits of each selected period, as well as the commencement of each new period, thus providing traders with a convenient reference point.

🔶 SETTINGS

Period: Select how many bars (hours, days, or months) will be used to gather data from, max value as default.

Execution Window: Select how many bars (hours, days, or months) will be used to gather data from

🔹 Advanced Filters

Hours of day: Filter which hours of the day are excluded from the data, it accepts a list of hours from 0 to 23 separated by commas or spaces, users can not mix commas or spaces as a separator, must choose one

Days of week: Filter which days of the week are excluded from the data, it accepts a list of days from 1 to 5 for tickers not trading weekends, or from 1 to 7 for tickers trading all week, users can choose between commas or spaces as a separator, but can not mix them on the same filter.

Days of month: Filter which days of the month are excluded from the data, it accepts a list of days from 1 to 31, users can choose between commas or spaces as separator, but can not mix them on the same filter.

Months: Filter months to exclude from data. Accepts months from 1 to 12. Choose one separator: comma or space.

Years: Filter years to exclude from data. Accepts years from 1000 to 2999. Choose one separator: comma or space.

🔹 Dashboard

Dashboard Location: Select both the vertical and horizontal parameters for the desired location of the dashboard.

Dashboard Size: Select size for dashboard.

🔹 Style

High Probability Top Line: Enable/disable `High Probability Top` vertical line and choose color

High Probability Bottom Line: Enable/disable `High Probability Bottom` vertical line and choose color

Top Label: Enable/disable period top labels, choose color and size.

Bottom Label: Enable/disable period bottom labels, choose color and size.

Highlight Period Changes: Enable/disable vertical highlight at start of period

2024 - Median High-Low % Change - Monthly, Weekly, DailyDescription:

This indicator provides a statistical overview of Bitcoin's volatility by displaying the median high-to-low percentage changes for monthly, weekly, and daily timeframes. It allows traders to visualize typical price fluctuations within each period, supporting range and volatility-based trading strategies.

How It Works:

Calculation of High-Low % Change: For each selected timeframe (monthly, weekly, and daily), the script calculates the percentage change from the high to the low price within the period.

Median Calculation: The median of these high-to-low changes is determined for each timeframe, offering a robust central measure that minimizes the impact of extreme price swings.

Table Display: At the end of the chart, the script displays a table in the top-right corner with the median values for each selected timeframe. This table is updated dynamically to show the latest data.

Usage Notes:

This script includes input options to toggle the visibility of each timeframe (monthly, weekly, and daily) in the table.

Designed to be used with Bitcoin on daily and higher timeframes for accurate statistical insights.

Ideal for traders looking to understand Bitcoin's typical volatility and adjust their strategies accordingly.

This indicator does not provide specific buy or sell signals but serves as an analytical tool for understanding volatility patterns.

Global OECD CLI Diffusion Index YoY vs MoMThe Global OECD Composite Leading Indicators (CLI) Diffusion Index is used to gauge the health and directional momentum of the global economy and anticipate changes in economic conditions. It usually leads turning points in the economy by 6 - 9 months.

How to read: Above 50% signals economic expansion across the included countries. Below 50% signals economic contraction.

The diffusion index component specifically shows the proportion of countries with positive economic growth signals compared to those with negative or neutral signals.

The OECD CLI aggregates data from several leading economic indicators including order books, building permits, and consumer and business sentiment. It tracks the economic momentum and turning points in the business cycle across 38 OECD member countries and several other Non-OECD member countries.

Future Trend Channel [ChartPrime]The Future Trend Channel indicator is a dynamic tool for identifying trends and projecting future prices based on channel formations. The indicator uses SMA (Simple Moving Average) and volatility calculations to plot channels that visually represent trends. It also detects moments of lower momentum, indicated by neutral color changes in the channels, and projects future price levels for up to 50 bars ahead.

⯁ KEY FEATURES AND HOW TO USE

⯌ Dynamic Trend Channels :

The indicator draws channels when a trend is identified. It uses a combination of SMA and volatility to determine the direction and strength of the trend. Each channel is visualized with a specific color, where green indicates an uptrend and orange represents a downtrend.

Example of channels during uptrend and downtrend:

⯌ Momentum-Based Color Shifts :

The indicator adapts its channel colors based on momentum changes. When the starting point (Y1) of a channel is higher than its ending point (Y2) during an uptrend, the channel turns neutral, indicating lower momentum and a possible ranging market. The same applies in a downtrend, where the channel turns neutral if Y1 is lower than Y2.

Example of neutral momentum channels:

⯌ Future Price Projection :

At the end of each channel, the indicator generates a projected future price based on the midpoint of the channel. By default, this projection is made 50 bars into the future, but users can adjust the number of bars to their preference.

Example of future price projection:

⯌ Diamond Signals for Valid Trends :

Lime-colored diamonds appear when an uptrend channel is confirmed, while orange diamonds indicate valid downtrend channels. These signals confirm the presence of a strong trend and help identify valid entry and exit points. Neutral channels, which indicate lower momentum, do not show diamond signals.

Example of trend confirmation signals:

⯌ Customizable Settings :

Users can adjust the channel length (how far back the trend is analyzed) and the width (which determines the channel boundaries based on volatility). The future price projection can also be customized to forecast further or fewer bars into the future.

⯁ USER INPUTS

Trend Length : Sets the number of bars used to calculate the trend channels.

Channel Width : Adjusts the width of the channels, based on volatility (ATR multiplier).

Up and Down Colors : Allows customization of the colors used for uptrend and downtrend channels.

Future Bars : Sets the number of bars used for future price projection.

⯁ CONCLUSION

The Future Trend Channel indicator is a versatile tool for identifying and trading trends. With its ability to detect momentum shifts and project future prices, it provides traders with key insights for making more informed decisions. The use of diamond signals for trend validation adds an extra layer of confirmation, helping traders act with greater confidence during volatile or trending markets.

Stoch RSI and RSI Buy/Sell Signals with MACD Trend FilterDescription of the Indicator

This Pine Script is designed to provide traders with buy and sell signals based on the combination of Stochastic RSI, RSI, and MACD indicators, enhanced by the confirmation of candle colors. The primary goal is to facilitate informed trading decisions in various market conditions by utilizing different indicators and their interactions. The script allows customization of various parameters, providing flexibility for traders to adapt it to their specific trading styles.

Usefulness

This indicator is not just a mashup of existing indicators; it integrates the functionality of multiple momentum and trend-detection methods into a cohesive trading tool. The combination of Stochastic RSI, RSI, and MACD offers a well-rounded approach to analyzing market conditions, allowing traders to identify entry and exit points effectively. The inclusion of color-coded signals (strong vs. weak) further enhances its utility by providing visual cues about the strength of the signals.

How to Use This Indicator

Input Settings: Adjust the parameters for the Stochastic RSI, RSI, and MACD to fit your trading style. Set the overbought/oversold levels according to your risk tolerance.

Signal Colors:

Strong Buy Signal: Indicated by a green label and confirmed by a green candle (close > open).

Weak Buy Signal: Indicated by a blue label and confirmed by a green candle (close > open).

Strong Sell Signal: Indicated by a red label and confirmed by a red candle (close < open).

Weak Sell Signal: Indicated by an orange label and confirmed by a red candle (close < open).

Example Trading Strategy Using This Indicator

To effectively use this indicator as part of your trading strategy, follow these detailed steps:

Setup:

Timeframe : Select a timeframe that aligns with your trading style (e.g., 15-minute for intraday, 1-hour for swing trading, or daily for longer-term positions).

Indicator Settings : Customize the Stochastic RSI, RSI, and MACD parameters to suit your trading approach. Adjust overbought/oversold levels to match your risk tolerance.

Strategy:

1. Strong Buy Entry Criteria :

Wait for a strong buy signal (green label) when the RSI is at or below the oversold level (e.g., ≤ 35), indicating a deeply oversold market. Confirm that the MACD shows a decreasing trend (bearish momentum weakening) to validate a potential reversal. Ensure the current candle is green (close > open) if candle color confirmation is enabled.

Example Use : On a 1-hour chart, if the RSI drops below 35, MACD shows three consecutive bars of decreasing negative momentum, and a green candle forms, enter a buy position. This setup signals a robust entry with strong momentum backing it.

2. Weak Buy Entry Criteria :

Monitor for weak buy signals (blue label) when RSI is above the oversold level but still below the neutral (e.g., between 36 and 50). This indicates a market recovering from an oversold state but not fully reversing yet. These signals can be used for early entries with additional confirmations, such as support levels or higher timeframe trends.

Example Use : On the same 1-hour chart, if RSI is at 45, the MACD shows momentum stabilizing (not necessarily negative), and a green candle appears, consider a partial or cautious entry. Use this as an early warning for a potential bullish move, especially when higher timeframe indicators align.

3. Strong Sell Entry Criteria :

Look for a strong sell signal (red label) when RSI is at or above the overbought level (e.g., ≥ 65), signaling a strong overbought condition. The MACD should show three consecutive bars of increasing positive momentum to indicate that the bullish trend is weakening. Ensure the current candle is red (close < open) if candle color confirmation is enabled.

Example Use : If RSI reaches 70, MACD shows increasing momentum that starts to level off, and a red candle forms on a 1-hour chart, initiate a short position with a stop loss set above recent resistance. This is a high-confidence signal for potential price reversal or pullback.

4. Weak Sell Entry Criteria :

Use weak sell signals (orange label) when RSI is between the neutral and overbought levels (e.g., between 50 and 64). These can indicate potential short opportunities that might not yet be fully mature but are worth monitoring. Look for other confirmations like resistance levels or trendline touches to strengthen the signal.

Example Use : If RSI reads 60 on a 1-hour chart, and the MACD shows slight positive momentum with signs of slowing down, place a cautious sell position or scale out of existing long positions. This setup allows you to prepare for a possible downtrend.

Trade Management:

Stop Loss : For buy trades, place stop losses below recent swing lows. For sell trades, set stops above recent swing highs to manage risk effectively.

Take Profit : Target nearby resistance or support levels, apply risk-to-reward ratios (e.g., 1:2), or use trailing stops to lock in profits as price moves in your favor.

Confirmation : Align these signals with broader trends on higher timeframes. For example, if you receive a weak buy signal on a 15-minute chart, check the 1-hour or daily chart to ensure the overall trend is not bearish.

Real-World Example: Imagine trading on a 15-minute chart :

For a buy:

A strong buy signal (green) appears when the RSI dips to 32, MACD shows declining bearish momentum, and a green candle forms. Enter a buy position with a stop loss below the most recent support level.

Alternatively, a weak buy signal (blue) appears when RSI is at 47. Use this as a signal to start monitoring the market closely or enter a smaller position if other indicators (like support and volume analysis) align.

For a sell:

A strong sell signal (red) with RSI at 72 and a red candle signals to short with conviction. Place your stop loss just above the last peak.

A weak sell signal (orange) with RSI at 62 might prompt caution but can still be acted on if confirmed by declining volume or touching a resistance level.

These strategies show how to blend both strong and weak signals into your trading for more nuanced decision-making.

Technical Analysis of the Code

1. Stochastic RSI Calculation:

The script calculates the Stochastic RSI (stochRsiK) using the RSI as input and smooths it with a moving average (stochRsiD).

Code Explanation : ta.stoch(rsi, rsi, rsi, stochLength) computes the Stochastic RSI, and ta.sma(stochRsiK, stochSmoothing) applies smoothing.

2. RSI Calculation :

The RSI is computed over a user-defined period and checks for overbought or oversold conditions.

Code Explanation : rsi = ta.rsi(close, rsiLength) calculates RSI values.

3. MACD Trend Filter :

MACD is calculated with fast, slow, and signal lengths, identifying trends via three consecutive bars moving in the same direction.

Code Explanation : = ta.macd(close, macdLengthFast, macdLengthSlow, macdSignalLength) sets MACD values. Conditions like macdLine < macdLine confirm trends.

4. Buy and Sell Conditions :

The script checks Stochastic RSI, RSI, and MACD values to set buy/sell flags. Candle color filters further confirm valid entries.

Code Explanation : buyConditionMet and sellConditionMet logically check all conditions and toggles (enableStochCondition, enableRSICondition, etc.).

5. Signal Flags and Confirmation :

Flags track when conditions are met and ensure signals only appear on appropriate candle colors.

Code Explanation : Conditional blocks (if statements) update buyFlag and sellFlag.

6. Labels and Alerts :

The indicator plots "BUY" or "SELL" labels with the RSI value when signals trigger and sets alerts through alertcondition().

Code Explanation : label.new() displays the signal, color-coded for strength based on RSI.

NOTE : All strategies can be enabled or disabled in the settings, allowing traders to customize the indicator to their preferences and trading styles.

Trade 1 + StatergyThe Relative Strength Index (RSI) is a momentum oscillator used in technical analysis that measures the speed and change of price movements of a security within a range of 0 to 100. It is most commonly set to a 14-period timeframe and helps traders identify overbought or oversold conditions, suggesting potential reversal points in the market. Divergence occurs when the price trend and the RSI trend move in opposite directions. A bullish divergence signals potential upward movement when prices are making new lows while the RSI makes higher lows. Conversely, a bearish divergence suggests a possible downward trend when prices are making new highs but the RSI is making lower highs. These signals are crucial for traders looking to capture shifts in momentum and adjust their trading strategies accordingly.

use full to

5 min

10 min

15 min decition

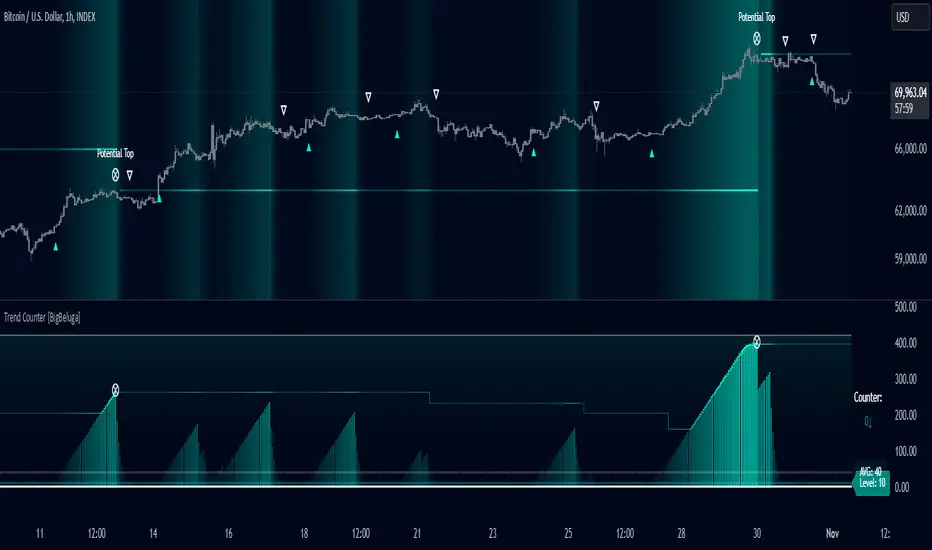

Trend Counter [BigBeluga]The Trend Counter indicator is designed to help traders identify trend conditions and potential reversals by counting the number of bars within a specified period that are above or below an average price level. By smoothing and averaging these counts, the indicator provides a clear visual representation of market trends and highlights key trend changes.

Key Features:

⦾ Trend Counting:

Counts bars above and below average price levels over a specified period.

Smooths and rounds the count for better visualization.

// Count bars over length period above highest and lowest avg with offset loop

float mid = math.avg(ta.highest(length), ta.lowest(length))

for offset = 0 to length -1

switch

hl2 > mid => counter += 1.0

=> counter := 0.0

// Smooth Count and Round

counter := math.round(ta.ema(counter > 400 ? 400 : counter, smooth))

// Count Avg

count.push(counter)

avg = math.round(count.avg())

⦿ Color Indication:

Uses gradient colors to indicate the strength of the trend.

Colors the background based on trend strength for easier interpretation.

⦿ Trend Signals:

Provides visual cues for trend changes based on the counter crossing predefined levels.

⦿ Potential Tops:

Identifies potential market tops using a specified length and highlights these levels.

⦿ Additional Features:

Displays Trend Counter value with arrows to indicate the direction of the trend movement.

Displays average trend count and level for reference.

⦿ User Inputs Description

Length: Defines the period over which the trend counting is performed.

Trend Counter Smooth: Specifies the smoothing period for the trend counter.

Level: Sets the threshold level for trend signals.

Main Color: Determines the primary color for trend indication.

The Trend Counter indicator is a powerful tool for traders seeking to identify and visualize market trends.

By counting and smoothing price bars above and below average levels, it provides clear and intuitive signals for trend strength and potential reversals.

With customizable parameters and visual cues, the Trend Counter enhances trend analysis and decision-making for traders of all levels.

Liquidity Squeeze Indicator 1The provided Pine Script code implements a "Liquidity Squeeze Indicator" in TradingView, designed to detect potential bullish or bearish market squeezes based on EMA slopes, candle wicks, and body sizes.

Code Breakdown

EMAs Calculation: Calculates the 21-period (ema_21) and 50-period (ema_50) exponential moving averages (EMAs) on closing prices.

EMA Slope Calculation: Computes the slope of the 21-period EMA over a 21-period lookback to estimate trend direction, with a threshold of 0.45 to approximate a 45-degree angle.

Candle Properties: Measures the size of the candle's body and its upper and lower wicks for comparison to detect wick-to-body ratios.

Trend Identification: Defines a bullish trend when ema_21 is above ema_50 and a bearish trend when ema_21 is below ema_50.

Wick Conditions

Bullish Condition : In a bullish trend with the EMA slope up, checks if the upper wick is at least 3x the body size and the closing price is above the 21 EMA.

Bearish Condition: In a bearish trend with the EMA slope down, checks if the lower wick is at least 3x the body size and the closing price is below the 21 EMA.

Signal Plotting: Plots a green dot above the bar for bullish signals and a red dot below the bar for bearish signals.

Alerts: Defines alert conditions for both bullish and bearish signals, providing specific alert messages when conditions are met.

Summary

This indicator helps identify potential bullish or bearish liquidity squeezes by looking at trends, EMA slopes, and wick-to-body ratios in candlesticks. The primary signals are visualized through dots on the chart and can trigger alerts for notable market conditions.

Colored Moving Averages With RSI SignalsMoving Average (MA):

Helps to determine the overall market trend. If the price is above the MA, it may indicate an uptrend, and if below, a downtrend.

In this case, a Simple Moving Average (SMA) is used, but other types can be applied as well.

Relative Strength Index (RSI):

This is an oscillator that measures the speed and changes of price movements.

Values above 70 indicate overbought conditions (possible sell signal), while values below 30 indicate oversold conditions (possible buy signal).

Purpose of This Indicator:

Trading Signals: The indicator generates "Buy" and "Sell" signals based on the intersection of the price line and the moving average, as well as RSI values. This helps traders make more informed decisions.

Signal Filtering: Using RSI in combination with MA allows for filtering false signals since it considers not only the current trend but also the state of overbought or oversold conditions.

How to Use:

For Short-Term Trading: Traders can use buy and sell signals to enter trades based on short-term market fluctuations.

In Combination with Other Indicators: It can be combined with other indicators for a more comprehensive analysis (e.g., adding support and resistance levels).

Overall, this indicator helps traders respond more quickly and accurately to changes in market conditions, enhancing the chances of successful trades.

Basic RSI Strategy with MFI Description: This Pine Script is a custom trading strategy that combines the power of the RSI (Relative Strength Index) and MFI (Money Flow Index) indicators with additional signal filters and a user-friendly dashboard. The strategy is designed to identify potential entry and exit points based on dynamic conditions, providing an advanced approach to technical analysis and decision-making in trading.

Key Features:

RSI-Based Signals:

Generates buy signals when the RSI-based moving average crosses above specific thresholds (29 and 50).

Generates sell signals when the RSI-based moving average crosses below specific thresholds (50 and 69).

MFI Filtering:

Signals are validated only if the MFI value is within the specified range of 20 to 80, ensuring that signals are generated only when market conditions are favorable.

Dynamic Signal Thresholds:

The script includes adjustable thresholds for the percentage difference between consecutive bars, as well as the range between high and low prices, to refine signal accuracy.

Dashboard:

Displays real-time statistics in the top right corner of the chart, including the total number of signals, the count of buy and sell signals, and the time duration over which these signals were generated.

How to Use:

Settings: Customize the RSI and MFI lengths, along with thresholds for price movement and MFI range. This flexibility allows the strategy to be tailored to different market conditions and timeframes.

Dashboard Insight: Track the strategy's performance in real-time, with an intuitive overview of generated signals and their time distribution on the chart.

Ideal For:

This script is suitable for traders seeking a robust, customizable, and real-time signal generation strategy that combines momentum and volume indicators. The strategy’s unique filtering mechanism provides a higher level of precision, making it an excellent tool for those who prioritize signal accuracy and clarity.

Fibonacci Buy /Sell SignalsHere is a Fibonacci-based Buy/Sell Indicator using retracement levels for potential support and resistance zones. This indicator plots Fibonacci levels and provides buy/sell signals based on price interaction with these levels.

Fibonacci Levels:

Highest high and lowest low over the lookback period.

Key levels: 38.2% (retracement), 50% (midpoint), 61.8% (strong retracement).

Buy Signal: When the price crosses above the 61.8% Fibonacci level (bullish).

Sell Signal: When the price crosses below the 38.2% Fibonacci level (bearish).