CauchyTrend [InvestorUnknown]The CauchyTrend is an experimental tool that leverages a Cauchy-weighted moving average combined with a modified Supertrend calculation. This unique approach provides traders with insight into trend direction, while also offering an optional ATR-based range analysis to understand how often the market closes within, above, or below a defined volatility band.

Core Concepts

Cauchy Distribution and Gamma Parameter

The Cauchy distribution is a probability distribution known for its heavy tails and lack of a defined mean or variance. It is characterized by two parameters: a location parameter (x0, often 0 in our usage) and a scale parameter (γ, "gamma").

Gamma (γ): Determines the "width" or scale of the distribution. Smaller gamma values produce a distribution more concentrated near the center, giving more weight to recent data points, while larger gamma values spread the weight more evenly across the sample.

In this indicator, gamma influences how much emphasis is placed on values closer to the current price versus those further away in time. This makes the resulting weighted average either more reactive or smoother, depending on gamma’s value.

// Cauchy PDF formula used for weighting:

// f(x; γ) = (1/(π*γ)) *

f_cauchyPDF(offset, gamma) =>

numerator = gamma * gamma

denominator = (offset * offset) + (gamma * gamma)

pdf = (1 / (math.pi * gamma)) * (numerator / denominator)

pdf

A chart showing different Cauchy PDFs with various gamma values, illustrating how gamma affects the weight distribution.

Cauchy-Weighted Moving Average (CWMA)

Using the Cauchy PDF, we calculate normalized weights to create a custom Weighted Moving Average. Each bar in the lookback period receives a weight according to the Cauchy PDF. The result is a Cauchy Weighted Average (cwm_avg) that differs from typical moving averages, potentially offering unique sensitivity to price movements.

// Summation of weighted prices using Cauchy distribution weights

cwm_avg = 0.0

for i = 0 to length - 1

w_norm = array.get(weights, i) / sum_w

cwm_avg += array.get(values, i) * w_norm

Supertrend with a Cauchy Twist

The indicator integrates a modified Supertrend calculation using the cwm_avg as its reference point. The Supertrend logic typically sets upper and lower bands based on volatility (ATR), and flips direction when price crosses these bands.

In this case, the Cauchy-based average replaces the usual baseline, aiming to capture trend direction via a different weighting mechanism.

When price closes above the upper band, the trend is considered bullish; closing below the lower band signals a bearish trend.

ATR Stats Range (Optional)

Beyond the fundamental trend detection, the indicator optionally computes ATR-based stats to understand price distribution relative to a volatility corridor centered on the cwm_avg line:

Volatility Range:

Defined as cwm_avg ± (ATR * atr_mult), this range creates upper and lower bands. Turning on atr_stats computes how often the daily close falls: Within the range, Above the upper ATR boundary, Below the lower ATR boundary, Within the range but above cwm_avg, Within the range but below cwm_avg

These statistics can help traders gauge how the market behaves relative to this volatility envelope and possibly identify if the market tends to revert to the mean or break out more often.

Backtesting and Performance Metrics

The code is integrated with a backtesting library that allows users to assess strategy performance historically:

Equity Curve Calculation: Compares CauchyTrend-based signals against the underlying asset.

Performance Metrics Table: Once enabled, displays key metrics such as mean returns, Sharpe Ratio, Sortino Ratio, and more, comparing the strategy to a simple Buy & Hold approach.

Alerts and Notifications

The indicator provides Alerts for key events:

Long Alert: Triggered when the trend flips bullish.

Short Alert: Triggered when the trend flips bearish.

Customization and Calibration

Important: The default parameters are not optimized for any specific instrument or time frame. Traders should:

Adjust the length and gamma parameters to influence how sharply or broadly the cwm_avg reacts to price changes.

Tune the atr_len and atr_mult for the Supertrend logic to better match the asset’s volatility characteristics.

Experiment with atr_stats on/off to see if that additional volatility distribution information provides helpful insights.

Traders may find certain sets of parameters that align better with their preferred trading style, risk tolerance, or asset volatility profile.

Disclaimer: This indicator is for educational and informational purposes only. Past performance in backtesting does not guarantee future results. Always perform due diligence, and consider consulting a qualified financial advisor before trading.

Statistics

Scatter PlotThe Price Volume Scatter Plot publication aims to provide intrabar detail as a Scatter Plot .

🔶 USAGE

A dot is drawn at every intrabar close price and its corresponding volume , as can seen in the following example:

Price is placed against the white y-axis, where volume is represented on the orange x-axis.

🔹 More detail

A Scatter Plot can be beneficial because it shows more detail compared with a Volume Profile (seen at the right of the Scatter Plot).

The Scatter Plot is accompanied by a "Line of Best Fit" (linear regression line) to help identify the underlying direction, which can be helpful in interpretation/evaluation.

It can be set as a screener by putting multiple layouts together.

🔹 Easier Interpretation

Instead of analysing the 1-minute chart together with volume, this can be visualised in the Scatter Plot, giving a straightforward and easy-to-interpret image of intrabar volume per price level.

One of the scatter plot's advantages is that volumes at the same price level are added to each other.

A dot on the scatter plot represents the cumulated amount of volume at that particular price level, regardless of whether the price closed one or more times at that price level.

Depending on the setting "Direction" , which sets the direction of the Volume-axis, users can hoover to see the corresponding price/volume.

🔹 Highest Intrabar Volume Values

Users can display up to 5 last maximum intrabar volume values, together with the intrabar timeframe (Res)

🔹 Practical Examples

When we divide the recent bar into three parts, the following can be noticed:

Price spends most of its time in the upper part, with relative medium-low volume, since the intrabar close prices are mostly situated in the upper left quadrant.

Price spends a shorter time in the middle part, with relative medium-low volume.

Price moved rarely below 61800 (the lowest part), but it was associated with high volume. None of the intrabar close prices reached the lowest area, and the price bounced back.

In the following example, the latest weekly candle shows a rejection of the 45.8 - 48.5K area, with the highest volume at the 45.8K level.

The next three successive candles show a declining maximum intrabar volume, after which the price broke through the 45.8K area.

🔹 Visual Options

There are many visual options available.

🔹 Change Direction

The Scatter Plot can be set in 4 different directions.

🔶 NOTES

🔹 Notes

The script uses the maximum available resources to draw the price/volume dots, which are 500 boxes and 500 labels. When the population size exceeds 1000, a warning is provided ( Not all data is shown ); otherwise, only the population size is displayed.

The Scatter Plot ideally needs a chart which contains at least 100 bars. When it contains less, a warning will be shown: bars < 100, not all data is shown

🔹 LTF Settings

When 'Auto' is enabled ( Settings , LTF ), the LTF will be the nearest possible x times smaller TF than the current TF. When 'Premium' is disabled, the minimum TF will always be 1 minute to ensure TradingView plans lower than Premium don't get an error.

Examples with current Daily TF (when Premium is enabled):

500 : 3 minute LTF

1500 (default): 1 minute LTF

5000: 30 seconds LTF (1 minute if Premium is disabled)

🔶 SETTINGS

Direction: Direction of Volume-axis; Left, Right, Up or Down

🔹 LTF

LTF: LTF setting

Auto + multiple: Adjusts the initial set LTF

Premium: Enable when your TradingView plan is Premium or higher

🔹 Character

Character: Style of Price/Volume dot

Fade: Increasing this number fades dots at lower price/volume

Color

🔹 Linear Regression

Toggle (enable/disable), color, linestyle

Center Cross: Toggle, color

🔹 Background Color

Fade: Increasing this number fades the background color near lower values

Volume: Background color that intensifies as the volume value on the volume-axis increases

Price: Background color that intensifies as the price value on the price-axis increases

🔹 Labels

Size: Size of price/volume labels

Volume: Color for volume labels/axis

Price: Color for price labels/axis

Display Population Size: Show the population size + warning if it exceeds 1000

🔹 Dashboard

Location: Location of dashboard

Size: Text size

Display LTF: Display the intrabar Lower Timeframe used

Highest IB volume: Display up to 5 previous highest Intrabar Volume values

Romantic Information CoefficientThis script calculates the Mutual Information (MI) between the closing prices of two assets over a defined lookback period. Mutual Information is a measure of the shared information between two time-series datasets. A higher MI indicates a stronger relationship between the two assets.

Key Features:

Ticker Inputs: You can select the tickers for two assets. For example, SPY (S&P 500 ETF) and AAPL (Apple stock) can be compared.

Lookback Period: Choose the number of bars to look back and calculate the Mutual Information. A larger lookback period incorporates more data, but may be less responsive to recent price changes.

Bins for Discretization: Control the level of granularity for discretizing the asset prices. More bins result in a more detailed MI calculation but can also reduce the signal-to-noise ratio.

Color Coded MI: The MI plot dynamically changes color to provide visual feedback on whether the relationship between the two assets is strengthening (red) or weakening (blue).

Only for educational purposes. Not in anyway, investment advice.

Weekly Opening Range and Previous Data for FuturesThis indicator will not predict future price action.

This indicator is a time based range tool. These types of tools are great to use when there is not any historical data to look back on (as in all time highs/lows). The user can use this indicator to measure distributions, use deviations of the range to identify support/resistance levels, and see how historical price action influences current price action. This indicator is unique because it uses the price range from the open of the futures market on Sunday 18:00 America/New York to the open of the Bond Market 8:00 America/New York as the range for all calculations.

This indicator collects the multiple points of data from each day of the week, and gives the user many options on how to use the data that is collected. The amount of data collected is based on the time frame of the chart (best used on a 15 minute chart), but is limited to 30 minute charts.

Data Collected:

Opening Range for the week

High of Each Day

Low of Each Day

Close of Each Day

Initially the range is plotted on the chart as a box, when the Bond market opens the high/low/mid is plotted, as well as the current week open and previous week close.

How the data is used.

Intraday: Monday does not have a previous day to pull data on, so all data for Monday is intraday data. When a new high is made, the indicator will search all previous data in the lookback period for the current day , find all highs that are within a set variance (determined by the user), and plot the corresponding lows from the matching days. It will do the same for new lows that are made, with corresponding historical highs. All of these levels are plotted on the chart, as well as the Average High, Average Low. If price moves beyond either Average, the Average of all days that distributed higher than the Average is plotted on the chart as Min/Max Average.

Previous Day Data: Tuesday - Friday. After the close of the day, the user has the option to choose either the High, Low, or Close of that day to find previous data that matches within a variance determined by the user; or an option to find the n closest matches (up to 20). That data is then matched to the corresponding next day data and plotted on the chart as a box. Example: Monday closes at +1 Deviation (Dev) of the Weekly Opening Range (WOR). The user sets the variance at 0.5 (0.5 Dev of the WOR), the indicator will search the lookback period for all Mondays that closed between 1.25 Dev and 0.75 Dev of the WOR. The matching Mondays will then be matched to their corresponding Tuesdays and the data for the High and Low from those Tuesdays will be placed on the chart as a box overlaying the current Tuesday. Each match is numbered so that corresponding Highs and Lows of each historical day can be identified. The same can be done for either the High or Low of the Previous Day.

The indicator has a table that can be shown.

Data shown in table:

Current Extension of the WOR

Maximum Extension of the WOR

Average WOR in %

Current WOR in %

Average Range for the day in % based on data set

Current Range for the day in %

Number of days in the data set

Number of Previous Day Matches

Variance for previous day data

Number of Intraday High Matches

Number of Intraday Low Matches

Variance for Intraday Matches

The table as well as all lines and boxes have the option of being shown or not, as well as have their settings customized to fit the users chart layout.

As with any indicator, do not let the data shown change your trading model. Past performance is not indicative to future performance.

Spot PositionThis TradingView indicator helps traders manage their trades by providing visual information about open trades and profit/loss ratios. The indicator allows users to enter trade details such as entry price, stop loss, number of targets, and desired profit percentage. The indicator displays the current profit or loss percentage in real time, with profitable trades highlighted in green and losing trades in red. The indicator also displays profit and loss levels as well as the risk-to-reward ratio (RRR) for each trade, helping traders make quick and informed decisions.

This indicator does not provide signals or contribute to candlestick analysis; it is only for tracking your open trades to see where they have reached in a simple and easy graphical way, allowing better access to profit and loss ratios

The indicator allows adding five open trades at once and plots the targets of each trade on the chart and displays a table with a summary of open trades in terms of profit and loss

You can write your trade targets by writing the prices of all targets and separating each price with a comma (,) or write the number of targets and the profit percentage and the indicator will distribute the targets evenly over the prices

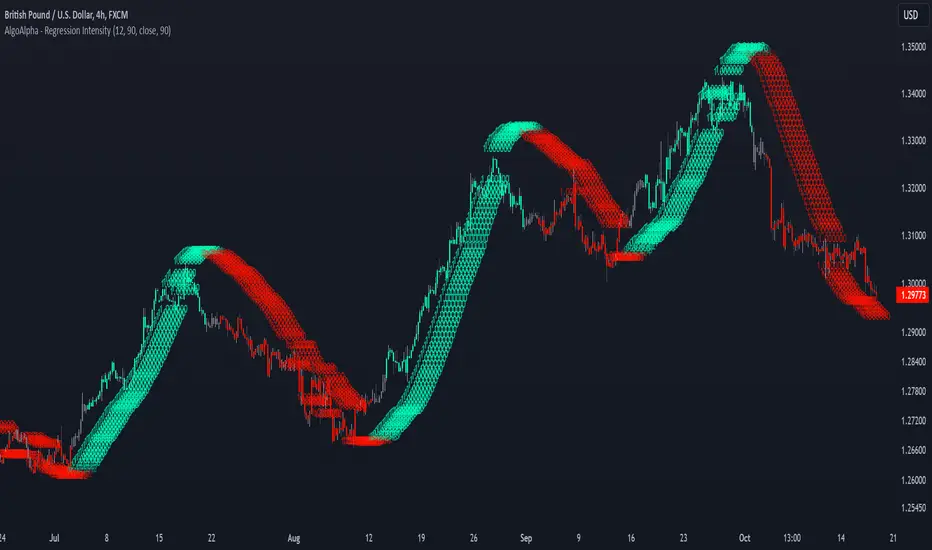

Linear Regression Intensity [AlgoAlpha]Introducing the Linear Regression Intensity indicator by AlgoAlpha, a sophisticated tool designed to measure and visualize the strength of market trends using linear regression analysis. This indicator not only identifies bullish and bearish trends with precision but also quantifies their intensity, providing traders with deeper insights into market dynamics. Whether you’re a novice trader seeking clearer trend signals or an experienced analyst looking for nuanced trend strength indicators, Linear Regression Intensity offers the clarity and detail you need to make informed trading decisions.

Key Features:

📊 Comprehensive Trend Analysis: Utilizes linear regression over customizable periods to assess and quantify trend strength.

🎨 Customizable Appearance: Choose your preferred colors for bullish and bearish trends to align with your trading style.

🔧 Flexible Parameters: Adjust the lookback period, range tolerance, and regression length to tailor the indicator to your specific strategy.

📉 Dynamic Bar Coloring: Instantly visualize trend states with color-coded bars—green for bullish, red for bearish, and gray for neutral.

🏷️ Intensity Labels: Displays dynamic labels that represent the intensity of the current trend, helping you gauge market momentum at a glance.

🔔 Alert Conditions: Set up alerts for strong bullish or bearish trends and trend neutrality to stay ahead of market movements without constant monitoring.

Quick Guide to Using Linear Regression Intensity:

🛠 Add the Indicator: Simply add Linear Regression Intensity to your TradingView chart from your favorites. Customize the settings such as lookback period, range tolerance, and regression length to fit your trading approach.

📈 Market Analysis: Observe the color-coded bars to quickly identify the current trend state. Use the intensity labels to understand the strength behind each trend, allowing for more strategic entry and exit points.

🔔 Set Up Alerts: Enable alerts for when strong bullish or bearish trends are detected or when the trend reaches a neutral zone. This ensures you never miss critical market movements, even when you’re away from the chart.

How It Works:

The Linear Regression Intensity indicator leverages linear regression to calculate the underlying trend of a selected price source over a specified length. By analyzing the consistency of the regression values within a defined lookback period, it determines the trend’s intensity based on a percentage tolerance. The indicator aggregates pairwise comparisons of regression values to assess whether the trend is predominantly upward or downward, assigning a state of bullish, bearish, or neutral accordingly. This state is then visually represented through dynamic bar colors and intensity labels, offering a clear and immediate understanding of market conditions. Additionally, the inclusion of Average True Range (ATR) ensures that the intensity visualization accounts for market volatility, providing a more robust and reliable trend assessment. With customizable settings and alert conditions, Linear Regression Intensity empowers traders to fine-tune their strategies and respond swiftly to evolving market trends.

Elevate your trading strategy with Linear Regression Intensity and gain unparalleled insights into market trends! 🌟📊

IU VaR (Value at Risk) Historical MethodThis Pine Script indicator calculates the **Value at Risk (VaR)** using the **Historical Method** to help traders understand potential losses during a given period( Chart Timeframe) with a specific level of confidence.

What is Value at Risk (VaR) ?

Value at Risk (VaR) is a measure used in finance to estimate the potential loss in value of an asset, portfolio, or investment over a specific time period, given normal market conditions, and at a certain confidence level.

Example:

Suppose you invest ₹1,00,000 in stocks. A VaR of 5% at a 95% confidence level means:

- There is a **95% chance** that you won’t lose more than **₹5,000** in a day.

- Conversely, there is a **5% chance** that your loss could exceed ₹5,000 in a day.

VaR is a helpful tool for understanding risk and making informed investment decisions!

How It Works:

1. The indicator calculates the percentage difference between consecutive bars.

2. The differences are sorted, and the VaR is determined based on the assurance level you specify.

3. A label displays the VaR value on the chart, indicating the potential maximum loss with the selected assurance level within one period eg - ( 1h, 4h , 1D, 1W, 1M etc as per your chart timeframe )

Key Features:

- Customizable Assurance Level:

Set the confidence level (e.g., 95%) to determine the probability of loss.

-Historical Approach:

Uses the past percentage changes in price to calculate the risk.

-Clear Insights:

Displays the calculated VaR value on the chart with an informative tooltip explaining the risk.

Use this tool to better understand your market exposure and manage risk!

ATR HEMA [SeerQuant]What is the ATR Holt Moving Average (HEMA)?

The ATR Holt Moving Average (HEMA) is an advanced smoothing technique that incorporates the Holt exponential smoothing method. Unlike traditional moving averages, HEMA uses two smoothing factors (alpha and gamma) to forecast both the current trend and the trend change rate. This dual-layer approach improves the responsiveness of the moving average to both stable trends and volatile price swings.

When paired with the Average True Range (ATR), the HEMA becomes even more powerful. The ATR acts as a volatility filter, defining a "neutral zone" where minor price fluctuations are ignored. This allows traders to focus on significant market movements while reducing the impact of noise.

⚙️ How the Code Works

The ATR Holt Moving Average (HEMA) combines trend smoothing with volatility filtering to provide traders with dynamic signals. Here's how it functions step by step:

User Inputs and Customization:

Traders can customize the lengths for HEMA's smoothing factors (alphaL and gammaL), the ATR calculation length, and the neutral zone multiplier (atrMult).

The src input allows users to choose the price source for calculations (e.g., hl2), while the col input offers various color themes (Default, Modern, Warm, Cool).

Holt Exponential Moving Average (HEMA) Calculation:

Alpha and Gamma Smoothing Factors:

alpha controls how much weight is given to the current price versus past prices.

gamma smooths the trend change rate, reducing noise. The HEMA formula combines the current price, the previous HEMA value, and a trend adjustment (via the b variable) to create a smooth yet responsive average. The b variable tracks the rate of change in the HEMA over time, further refining the trend detection.

ATR-Based Neutral Zone:

If the change in HEMA (hemaChange) falls within the neutral zone, it is considered insignificant, and the trend color remains unchanged.

Color and Signal Detection:

Bullish Trend: The color is set to bull when HEMA rises above the neutral zone.

Bearish Trend: The color is set to bear when HEMA falls below the neutral zone.

Neutral Zone: The color remains unchanged, signalling no significant trend.

🚀 Summary

This indicator enhances traditional moving averages by combining the Holt smoothing method with ATR-based volatility filtering. The HEMA adapts to market conditions, detecting trends and transitions while filtering out insignificant price changes. The result is a versatile tool for:

The ATR Holt Moving Average (HEMA) is ideal for traders seeking a balance between responsiveness and stability, offering precise signals in both trending and volatile markets.

📜 Disclaimer

The information provided by this script is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Past performance of any trading system or indicator, including this one, is not indicative of future results. Trading and investing in financial markets involve risk, and it is possible to lose your entire investment.

Users are advised to perform their own due diligence and consult with a licensed financial advisor before making any trading or investment decisions. The creator of this script is not responsible for any trading or investment decisions made based on the use of this script.

This script complies with TradingView's guidelines and is provided as-is, without any guarantee of accuracy, reliability, or performance. Use at your own risk.

Levy Flight Relative Strength Index [SeerQuant]Lévy Flight Relative Strength Index

A nuanced improvement on the classic RSI, the Lévy Flight RSI leverages the Lévy Flight model to calculate dynamic weighted gains and losses, offering improved responsiveness and smoothness in trend detection compared to the regular RSI. Ideal for traders seeking a balance between precision and adaptability, the Lévy Flight RSI is packed with customizable features and a sleek, modern aesthetic.

-----------------------------------------------------------------

🧠 What is Lévy Flight Modelling?

Lévy Flight modelling is a concept derived from probability theory and fractal mathematics, widely applied in fields such as finance and physics. In trading, Lévy Flights describe a random walk process characterized by small, frequent movements interspersed with larger, less frequent movements. This behaviour reflects real-world price dynamics, where markets often exhibit periods of relative calm followed by sharp, volatile movements. The Lévy Flight model introduces a weighting mechanism that amplifies extreme price changes while smoothing smaller ones, providing a more nuanced view of market trends.

In the context of the Lévy Flight RSI, this model enhances traditional RSI calculations by dynamically weighting price changes (gains and losses) based on their magnitude. This results in an RSI that is more responsive to significant price movements, making it ideal for detecting shifts in momentum and market direction.

-----------------------------------------------------------------

🌟 Key Features:

- Dynamic Lévy Flight Modelling: Adjust alpha (1 to 2) for responsive or smooth signals, making it perfect for varying market conditions.

- Custom RSI Smoothing: Choose from multiple moving average types, including TEMA, DEMA, HMA, ALMA, and more, to match your trading style.

- Visually Intuitive: Neon-inspired gradient colours and centered histogram provide instant insights into market conditions.

- Customizable Overbought/Oversold Levels: Clearly defined thresholds, with additional shaded regions for strength identification.

-----------------------------------------------------------------

⚙️ How the Code Works

The Lévy Flight RSI enhances the traditional RSI calculation by incorporating two primary elements:

Dynamic Weighting Using Lévy Flight:

The code calculates the price change (change) on each bar and applies a power function (alpha) to these changes. Gains are raised to the power of alpha (for positive price changes), and losses are similarly transformed (for negative price changes).

The parameter alpha (ranging from 1 to 2) determines the sensitivity of the weighting. Lower values emphasize responsiveness, while higher values smooth out signals.

Enhanced Moving Averages:

The weighted gains and losses are smoothed using a customizable moving average. Options include traditional averages like SMA and EMA, and more advanced ones like TEMA, HMA, and ALMA. These smoothed values are used to calculate the final RSI value.

-----------------------------------------------------------------

📈 Why Use Lévy Flight RSI?

This unique RSI indicator captures price momentum with enhanced sensitivity to market dynamics. Whether you’re trend-following, scalping, or identifying reversals, the Lévy Flight RSI provides robust insights to refine your trading decisions.

-----------------------------------------------------------------

🔧 Inputs:

RSI Settings: Control RSI length, calculation source, and smoothing type.

Lévy Flight Settings: Adjust alpha to tune the indicator's responsiveness.

Style Customization: Tailor the appearance with different colour themes and gradients.

-----------------------------------------------------------------

Global Market Strength IndicatorThe Global Market Strength Indicator is a powerful tool for traders and investors. It helps compare the strength of various global markets and indices. This indicator uses the True Strength Index (TSI) to measure market strength.

The indicator retrieves price data for different markets and calculates their TSI values. These values are then plotted on a chart. Each market is represented by a different colored line, making it easy to distinguish between them.

One of the main benefits of this indicator is its comprehensive global view. It covers major indices and country-specific ETFs, giving users a broad perspective on global market trends. This wide coverage allows for easy comparison between different markets and regions.

The indicator is highly customizable. Users can adjust the TSI smoothing period to suit their preferences. They can also toggle the visibility of individual markets. This feature helps reduce chart clutter and allows for more focused analysis.

To use the indicator, apply it to your chart in TradingView. Adjust the settings as needed, and observe the relative positions and movements of the TSI lines. Lines moving higher indicate increasing strength in that market, while lines moving lower suggest weakening markets.

The chart includes reference lines at 0.5 and -0.5. These help identify potential overbought and oversold conditions. Markets with TSI values above 0.5 may be considered strong or potentially overbought. Those below -0.5 may be weak or potentially oversold.

By comparing the movements of different markets, users can identify which markets are leading or lagging. They can also spot potential divergences between related markets. This information can be valuable for identifying sector rotations or shifts in global market sentiment.

A dynamic legend automatically updates to show only the visible markets. This feature improves chart readability and makes it easier to interpret the data.

The Global Market Strength Indicator is a versatile tool that provides valuable insights into global market performance. It helps traders and investors identify trends, compare market performances, and make more informed decisions. Whether you're looking to spot emerging global trends or identify potential trading opportunities, this indicator offers a comprehensive solution for global market analysis.

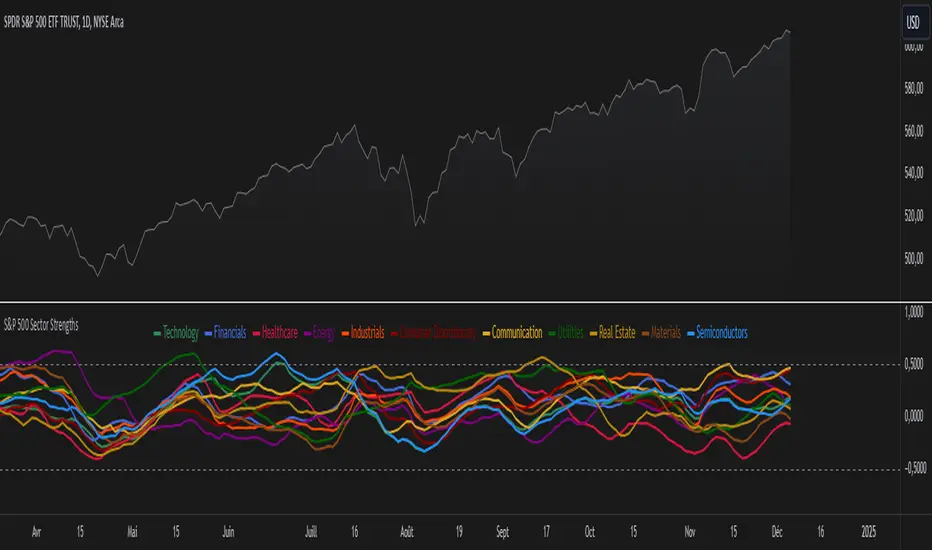

S&P 500 Sector StrengthsThe "S&P 500 Sector Strengths" indicator is a sophisticated tool designed to provide traders and investors with a comprehensive view of the relative performance of various sectors within the S&P 500 index. This indicator utilizes the True Strength Index (TSI) to measure and compare the strength of different sectors, offering valuable insights into market trends and sector rotations.

At its core, the indicator calculates the TSI for each sector using price data obtained through the request.security() function. The TSI, a momentum oscillator, is computed using a user-defined smoothing period, allowing for customization based on individual preferences and trading styles. The resulting TSI values for each sector are then plotted on the chart, creating a visual representation of sector strengths.

To use this indicator effectively, traders should focus on comparing the movements of different sector lines. Sectors with lines moving higher are showing increasing strength, while those with descending lines are exhibiting weakness. This comparative analysis can help identify potential investment opportunities and sector rotations. Additionally, when multiple sector lines move in tandem, it may signal a broader market trend.

The indicator includes dashed lines at 0.5 and -0.5, serving as reference points for overbought and oversold conditions. Sectors with TSI values above 0.5 might be considered overbought, suggesting caution, while those below -0.5 could be viewed as oversold, potentially indicating buying opportunities.

One of the key advantages of this indicator is its flexibility. Users can toggle the visibility of individual sectors and customize their colors, allowing for a tailored analysis experience. This feature is particularly useful when focusing on specific sectors or reducing chart clutter for clearer visualization.

The indicator's ability to provide a comprehensive overview of all major S&P 500 sectors in a single chart is a significant benefit. This consolidated view enables quick comparisons and helps in identifying relative strengths and weaknesses across sectors. Such insights can be invaluable for portfolio allocation decisions and in spotting emerging market trends.

Moreover, the dynamic legend feature enhances the indicator's usability. It automatically updates to display only the visible sectors, improving chart readability and interpretation.

By leveraging this indicator, market participants can gain a deeper understanding of sector dynamics within the S&P 500. This enhanced perspective can lead to more informed decision-making in sector allocation strategies and individual stock selection. The indicator's ability to potentially detect early trends by comparing sector strengths adds another layer of value, allowing users to position themselves ahead of broader market movements.

In conclusion, the "S&P 500 Sector Strengths" indicator is a powerful tool that combines technical analysis with sector comparison. Its user-friendly interface, customizable features, and comprehensive sector coverage make it an valuable asset for traders and investors seeking to navigate the complexities of the S&P 500 market with greater confidence and insight.

ETF-Benchmark AnalyzerHave you ever wondered which ETF performs the best? Which one is the most volatile, or which one has the smallest drawdown?

This Pine Script™ "ETF-Benchmark Analyzer" compares the performance of an ETF (such as SPY, the S&P 500 ETF) against a benchmark, which can also be adjusted by the user. It provides several key financial metrics, such as:

Performance (%): Displays the total return over a specified lookback period (e.g., 1 year). It compares the performance of the ETF against the benchmark and shows the difference.

Alpha (%): Measures the excess return of the ETF over the expected return, which is calculated using the benchmark’s return. Positive alpha indicates that the ETF has outperformed the benchmark, while negative alpha suggests underperformance. This metric is important because it isolates performance that cannot be explained by exposure to the benchmark's movements.

Sharpe Ratio: A risk-adjusted measure of return. It is calculated by dividing the excess return of the ETF (above the risk-free rate) by its standard deviation (volatility). A higher Sharpe ratio indicates better risk-adjusted returns. The Sharpe ratio is calculated for both the ETF and the benchmark, and their difference is displayed as well.

Drawdown: The percentage decrease from the highest price to the lowest price over the lookback period. This is a critical measure of risk, as it shows the largest potential loss an investor might face during a specific period.

Beta: Measures the ETF’s sensitivity to movements in the benchmark. A beta of 1 means the ETF moves in line with the benchmark; greater than 1 means it is more volatile, while less than 1 means it is less volatile.

These metrics provide a holistic view of the ETF’s performance compared to the benchmark, allowing traders to assess the risk and return profile more effectively.

Scientific Sources

Sharpe Ratio: Sharpe, W. F. (1994). The Sharpe Ratio. Journal of Portfolio Management, 21(1), 49-58. This paper defines and develops the Sharpe ratio as a measure of risk-adjusted return.

Alpha and Beta: Jensen, M. C. (1968). The Performance of Mutual Funds in the Period 1945–1964. The Journal of Finance, 23(2), 389-416. This paper discusses the concepts of alpha and beta in the context of mutual fund performance.

Kalman PredictorThe **Kalman Predictor** indicator is a powerful tool designed for traders looking to enhance their market analysis by smoothing price data and projecting future price movements. This script implements a Kalman filter, a statistical method for noise reduction, to dynamically estimate price trends and velocity. Combined with ATR-based confidence bands, it provides actionable insights into potential price movement, while offering clear trend and momentum visualization.

---

#### **Key Features**:

1. **Kalman Filter Smoothing**:

- Dynamically estimates the current price state and velocity to filter out market noise.

- Projects three future price levels (`Next Bar`, `Next +2`, `Next +3`) based on velocity.

2. **Dynamic Confidence Bands**:

- Confidence bands are calculated using ATR (Average True Range) to reflect market volatility.

- Visualizes potential price deviation from projected levels.

3. **Trend Visualization**:

- Color-coded prediction dots:

- **Green**: Indicates an upward trend (positive velocity).

- **Red**: Indicates a downward trend (negative velocity).

- Dynamically updated label displaying the current trend and velocity value.

4. **User Customization**:

- Inputs to adjust the process and measurement noise for the Kalman filter (`q` and `r`).

- Configurable ATR multiplier for confidence bands.

- Toggleable trend label with adjustable positioning.

---

#### **How It Works**:

1. **Kalman Filter Core**:

- The Kalman filter continuously updates the estimated price state and velocity based on real-time price changes.

- Projections are based on the current price trend (velocity) and extend into the future (Next Bar, +2, +3).

2. **Confidence Bands**:

- Calculated using ATR to provide a dynamic range around the projected future prices.

- Indicates potential volatility and helps traders assess risk-reward scenarios.

3. **Trend Label**:

- Updates dynamically on the last bar to show:

- Current trend direction (Up/Down).

- Velocity value, providing insight into the expected magnitude of the price movement.

---

#### **How to Use**:

- **Trend Analysis**:

- Observe the direction and spacing of the prediction dots relative to current candles.

- Larger spacing indicates a potential strong move, while clustering suggests consolidation.

- **Risk Management**:

- Use the confidence bands to gauge potential price volatility and set stop-loss or take-profit levels accordingly.

- **Pullback Detection**:

- Look for flattening or clustering of dots during trends as a signal of potential pullbacks or reversals.

---

#### **Customizable Inputs**:

- **Kalman Filter Parameters**:

- `lookback`: Adjusts the smoothing window.

- `q`: Process noise (higher values make the filter more reactive to changes).

- `r`: Measurement noise (controls sensitivity to price deviations).

- **Confidence Bands**:

- `band_multiplier`: Multiplies ATR to define the range of confidence bands.

- **Visualization**:

- `show_label`: Option to toggle the trend label.

- `label_offset`: Adjusts the label’s distance from the price for better visibility.

---

#### **Examples of Use**:

- **Scalping**: Use on lower timeframes (e.g., 1-minute, 5-minute) to detect short-term price trends and reversals.

- **Swing Trading**: Identify pullbacks or continuations on higher timeframes (e.g., 4-hour, daily) by observing the prediction dots and confidence bands.

- **Risk Assessment**: Confidence bands help visualize potential price volatility, aiding in the placement of stops and targets.

---

#### **Notes for Traders**:

- The **Kalman Predictor** does not predict the future with certainty but provides a statistically informed estimate of price movement.

- Confidence bands are based on historical volatility and should be used as guidelines, not guarantees.

- Always combine this tool with other analysis techniques for optimal results.

---

This script is open-source, and the Kalman filter logic has been implemented uniquely to integrate noise reduction with dynamic confidence band visualization. If you find this indicator useful, feel free to share your feedback and experiences!

---

#### **Credits**:

This script was developed leveraging the statistical principles of Kalman filtering and is entirely original. It incorporates ATR for dynamic confidence band calculations to enhance trader usability and market adaptability.

BTC Price Percentage Difference( Bitfinex - Coinbase)Introduction:

The BTC Price Percentage Difference Histogram Indicator is a powerful tool designed to help traders visualize and capitalize on the price discrepancies of Bitcoin (BTC) between two major exchanges: Bitfinex and Coinbase. By calculating the real-time percentage difference of BTC-USD prices and displaying it as a color-coded histogram, this indicator enables you to quickly spot potential arbitrage opportunities and gain deeper insights into market dynamics.

Features:

• Real-Time Percentage Difference Calculation:

• Computes the percentage difference between BTC-USD prices on Bitfinex and Coinbase.

• Color-Coded Histogram Visualization:

• Green Bars: Indicate that the BTC price on Bitfinex is higher than on Coinbase.

• Red Bars: Indicate that the BTC price on Bitfinex is lower than on Coinbase.

• User-Friendly and Intuitive:

• Simple setup with no additional inputs required.

• Automatically adapts to the chart’s timeframe for seamless integration.

Why Bitfinex Whales Matter:

Bitfinex is renowned for hosting some of the largest Bitcoin traders, often referred to as “whales.” These influential players have the capacity to move the market, and historically, they’ve demonstrated a high success rate in buying at market bottoms and selling at market tops. By tracking the price discrepancies between Bitfinex and other exchanges like Coinbase, you can gain valuable insights into the sentiment and actions of these key market participants.

lib_kernelLibrary "lib_kernel"

Library "lib_kernel"

This is a tool / library for developers, that contains several common and adapted kernel functions as well as a kernel regression function and enum to easily select and embed a list into the settings dialog.

How to Choose and Modify Kernels in Practice

Compact Support Kernels (e.g., Epanechnikov, Triangular): Use for localized smoothing and emphasizing nearby data.

Oscillatory Kernels (e.g., Wave, Cosine): Ideal for detecting periodic patterns or mean-reverting behavior.

Smooth Tapering Kernels (e.g., Gaussian, Logistic): Use for smoothing long-term trends or identifying global price behavior.

kernel_Epanechnikov(u)

Parameters:

u (float)

kernel_Epanechnikov_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Triangular(u)

Parameters:

u (float)

kernel_Triangular_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Rectangular(u)

Parameters:

u (float)

kernel_Uniform(u)

Parameters:

u (float)

kernel_Uniform_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Logistic(u)

Parameters:

u (float)

kernel_Logistic_alt(u)

Parameters:

u (float)

kernel_Logistic_alt2(u, sigmoid_steepness)

Parameters:

u (float)

sigmoid_steepness (float)

kernel_Gaussian(u)

Parameters:

u (float)

kernel_Gaussian_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Silverman(u)

Parameters:

u (float)

kernel_Quartic(u)

Parameters:

u (float)

kernel_Quartic_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Biweight(u)

Parameters:

u (float)

kernel_Triweight(u)

Parameters:

u (float)

kernel_Sinc(u)

Parameters:

u (float)

kernel_Wave(u)

Parameters:

u (float)

kernel_Wave_alt(u)

Parameters:

u (float)

kernel_Cosine(u)

Parameters:

u (float)

kernel_Cosine_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel(u, select, alt_modificator)

wrapper for all standard kernel functions, see enum Kernel comments and function descriptions for usage szenarios and parameters

Parameters:

u (float)

select (series Kernel)

alt_modificator (float)

kernel_regression(src, bandwidth, kernel, exponential_distance, alt_modificator)

wrapper for kernel regression with all standard kernel functions, see enum Kernel comments for usage szenarios. performance optimized version using fixed bandwidth and target

Parameters:

src (float) : input data series

bandwidth (simple int) : sample window of nearest neighbours for the kernel to process

kernel (simple Kernel) : type of Kernel to use for processing, see Kernel enum or respective functions for more details

exponential_distance (simple bool) : if true this puts more emphasis on local / more recent values

alt_modificator (float) : see kernel functions for parameter descriptions. Mostly used to pronounce emphasis on local values or introduce a decay/dampening to the kernel output

GapDetectGap Severity Analysis Library

This library, GapDetect , simplifies the identification and evaluation of overnight gaps by leveraging statistical metrics such as standard deviation and percentage moves. It is ideal for detecting large abnormal gaps which may be used to modify how strategies may decide to enter or exit.

Key Features:

Overnight Gap Detection

Provides two core functions:

today : Computes the value of today's overnight gap.

todayPercent : Computes the percentage change for today's overnight gap.

Volatility Analysis

Includes functions for statistical gap analysis:

normal : Calculates the normal daily standard deviation of the overnight gap, filtering outliers using customizable thresholds.

normalPercent : Similar to normal , but for percentage-based gap moves.

Gap Severity Metric

severity : a positive or negative value that represents the ratio of the current overnight move compared to the standard deviation of previous ones.

Customizable Parameters

Supports custom session specifications, resolutions, and outlier thresholds.

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

Volatility and Tick Size DataThis indicator, titled "Tick Information & Standard Deviation Table," provides detailed insights into market microstructure, including tick size, point value, and standard deviation values calculated based on the True Range. It helps visualize essential trading parameters that influence transaction costs, risk management, and portfolio performance, including volatility measures that can guide investment strategies.

Why These Data Points Are Important for Portfolio Management

Tick Size and Point Value:

Tick size refers to the smallest possible price movement in a given asset. It defines the granularity of the price changes, affecting how precise the market price can be at any moment. Point value reflects the monetary value of a single price movement (one tick). These two data points are essential for understanding transaction costs and for evaluating how much capital is at risk per price movement. Smaller tick sizes may lead to more efficient pricing in high-frequency trading strategies (Hasbrouck, 2009).

Reference: Hasbrouck, J. (2009). Empirical Market Microstructure. Foundations and Trends® in Finance, 3(4), 169-272.

Standard Deviations and Volatility:

Standard deviation measures the variability or volatility of an asset's price over a set period. This data point is critical for portfolio management, as it helps to quantify risk and predict potential price movements. True Range and its standard deviations provide a more comprehensive measure of market volatility than just price fluctuations, as they include gaps and extreme price changes. Investors use volatility data to assess the potential risk and adjust portfolio allocations accordingly (Ang, 2006).

Reference: Ang, A. (2006). Asset Management: A Systematic Approach to Factor Investing. Oxford University Press.

Risk Management:

The ability to quantify risk through metrics like the 1st, 2nd, and 3rd standard deviations of the true range is essential for implementing risk controls within a portfolio. By incorporating volatility data, portfolio managers can adjust their strategies for different market conditions, potentially reducing exposure to high-risk environments. These volatility measures help in setting stop-loss levels, optimizing position sizes, and managing the portfolio’s overall risk-return profile (Black & Scholes, 1973).

Reference: Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637-654.

Portfolio Diversification and Hedging:

Understanding asset volatility and transaction costs is critical when constructing a diversified portfolio. By using the standard deviations from this indicator, investors can better identify assets that may provide diversification benefits, potentially reducing the overall portfolio risk. Moreover, the point values and tick sizes help assess the cost-effectiveness of various assets, enabling portfolio managers to implement more efficient hedging strategies (Markowitz, 1952).

Reference: Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), 77-91.

Conclusion

The Tick Information & Standard Deviation Table provides critical market data that informs the risk management, diversification, and pricing strategies used in portfolio management. By incorporating tick size, point value, and volatility metrics, investors can make more informed decisions, better manage risk, and optimize the returns on their portfolios. The data serves as an essential tool for aligning asset selection and portfolio allocations with the investor's risk tolerance and market conditions.

Statistical Volatility Injections [neo.|]Introduction:

The Statistical Volatility indicator is a versatile tool designed to help traders gauge market volatility over time. By analyzing historical data through a customizable lookback period, it highlights zones of high and low volatility using intuitive colored gradients. This indicator enables traders to make informed decisions by identifying patterns in price movement or volume fluctuations, helping to optimize entries, exits, and overall trading strategy.

Description:

Volatility plays a critical role in financial markets, influencing price movements and trader behavior. This indicator calculates historical volatility using two approaches:

Ranges: Evaluates the price movement by measuring the high-to-low range of candles relative to their closing price.

Volume: Considers trading activity by analyzing the volume associated with each candle.

By mapping out periods of high and low volatility, the indicator provides traders with actionable insights into time where potential breakouts, reversals, or consolidations are more likely to happen. High volatility zones may indicate strong market movements, while low volatility zones often precede significant price action, giving traders a valuable edge.

Key Features:

Compare time based volatility between assets:

Adaptive display will calculate intraday volatility when under the 1h timeframe, and weekly volatility if on the 1h timeframe or above:

OANDA:GBPJPY On the 5min timeframe:

OANDA:GBPJPY On the 1h timeframe:

Display modes allow the volatility to be viewed as ranges and as bars:

How It Works:

Data Collection: The script analyzes historical candles using the user-defined lookback period and calculation type.

Data Processing: Each candle’s volatility is calculated and stored, enabling comparisons across the selected timeframe.

Visual Representation: Using a gradient color scheme, the indicator overlays the results on your chart, highlighting areas of interest based on historical volatility levels.

How to Use:

Setup:

Add the indicator to your chart.

Adjust the lookback period, gradient colors, and choose your preferred calculation mode (Ranges or Volume).

Interpretation:

Look for red zones to identify high-volatility periods—potential breakout or reversal areas.

Use yellow zones to anticipate consolidation or low-activity phases.

Customization:

Enable "Display ranges" to see box height variations reflecting volatility intensity.

Use the "Use Table" feature to summarize volatility data for quick reference.

Advanced Settings:

Adjust style options such as color gradients and overlapping controls for a cleaner chart view.

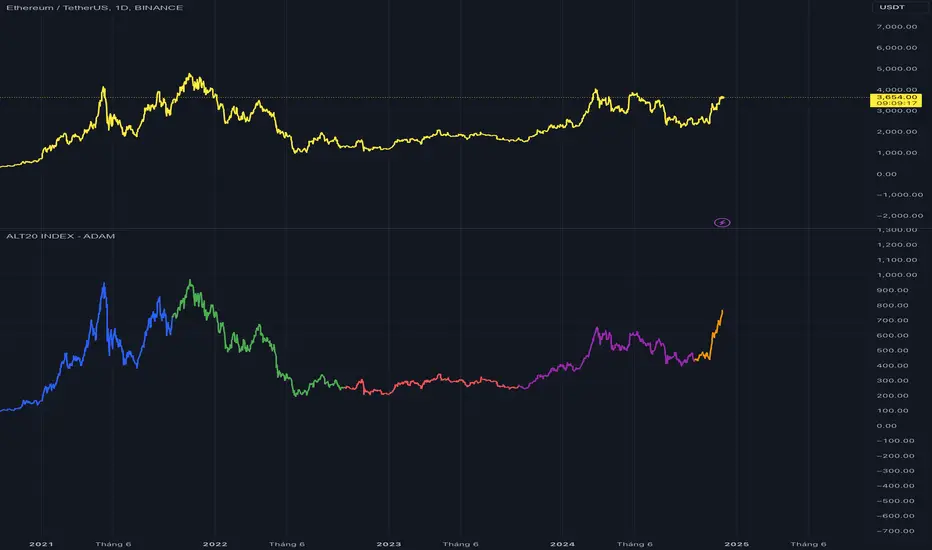

TOP 20 ALTCOIN INDEXIndicator Description

The "ALT20 INDEX" is a financial analysis tool designed to track the aggregate value of the top 20 cryptocurrencies by market capitalization and closing prices over specific periods. This indicator reflects changes in the combined value of these 20 ALTCOINs, providing an overview of trends in the cryptocurrency market.

=================================

Purpose and Practical Applications

1. Tracking Top Cryptocurrencies:

- The indicator allows monitoring the value of the top 20 ALTCOINs, reflecting the general volatility of the cryptocurrency market.

- Helps investors focus on high-capitalization assets.

2. Performance Comparison:

- Serves as a tool to compare the performance of the ALT20 group against other assets like Bitcoin, Ethereum, or traditional financial indices.

3. Assessing Market Health:

- Enables evaluation of market trends, identifying growth or decline periods.

4. Practical Applications:

- Suitable for fund managers, long-term investors, or trend traders to make decisions based on the overall ALTCOIN market performance.

-------------------------------------------

How the Indicator Works

1. Selection of Top 20 ALTCOINs:

- Cryptocurrencies are selected based on their market capitalization at each rebalancing period.

2. Weight Allocation and Calculation:

- Weight: Determined by the market capitalization of each ALTCOIN relative to the total market capitalization of the top 20.

- Token Quantity: Calculated based on weight, total allocation points (e.g., 100 points for T1, 722.63 points for T2, etc.), and each ALTCOIN's closing price.

Formula: Token Quantity = Weight × Total Allocation Points/Closing Price

3. Periodic Rebalancing:

- Rebalancing frequency: Once a year.

- At each rebalancing period, the weights and token quantities are adjusted based on new market capitalization and prices.

4. Portfolio Value Calculation:

- The value of each ALTCOIN is calculated as:

Token Value = Closing Price × Token Quantity

- Index Total: ALT20 Index = 20∑'i=1'Token Value'i'

------------------------------------------

Rebalancing Periods

T1 (2020-2021): Initial period, token quantities calculated based on weights and a total of 100 points.

T2 (2021-2022): Rebalanced with a total allocation of 722.63 points.

T3 (2022-2023): Total allocation of 252.26 points, reflecting portfolio adjustments based on new prices and market caps.

T4 (2023-2024): Total allocation of 261.43 points.

T5 (2024-Present): Total allocation of 437.42 points, updated to reflect the current market.

-----------------------------------------

Indicator Features

- Displays Index Value Over Time:

+ index_value_T1 to index_value_T5 represent the portfolio value during specific timeframes.

+ Values are calculated based on the daily closing prices of ALTCOINs.

- Visualization:

+ The index for each period is plotted on the chart, enabling easy observation of market trends over time.

---------------------------------------

Practical Applications

- Portfolio Management:

+ The indicator helps track the performance of asset groups within the ALTCOIN portfolio.

- Integration into Trading Systems:

+ Used as a reference for automated or manual trading strategies.

- Market Analysis:

+ Assists analysts in evaluating cryptocurrency market movements based on the top 20 ALTCOINs.

Let me know if further optimization or additional information is needed! Thank!

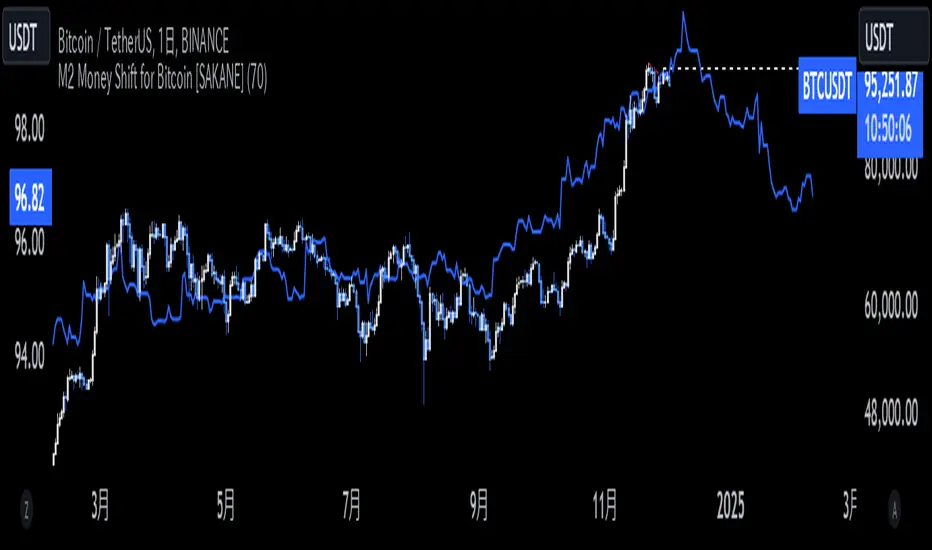

M2 Money Shift for Bitcoin [SAKANE]M2 Money Shift for Bitcoin was developed to visualize the impact of M2 Money, a macroeconomic indicator, on the Bitcoin market and to support trade analysis.

Bitcoin price fluctuations have a certain correlation with cycles in M2 money supply.In particular, it has been noted that changes in M2 supply can affect the bitcoin price 70 days in advance.Very high correlations have been observed in recent years in particular, making it useful as a supplemental analytical tool for trading.

Support for M2 data from multiple countries

M2 supply data from the U.S., Europe, China, Japan, the U.K., Canada, Australia, and India are integrated and all are displayed in U.S. dollar equivalents.

Slide function

Using the "Slide Days Forward" setting, M2 data can be slid up to 500 days, allowing for flexible analysis that takes into account the time difference from the bitcoin price.

Plotting Total Liquidity

Plot total liquidity (in trillions of dollars) by summing the M2 supply of multiple countries.

How to use

After applying the indicator to the chart, activate the M2 data for the required country from the settings screen. 2.

2. adjust "Slide Days Forward" to analyze the relationship between changes in M2 supply and bitcoin price

3. refer to the Gross Liquidity plot to build a trading strategy that takes into account macroeconomic influences.

Notes.

This indicator is an auxiliary tool for trade analysis and does not guarantee future price trends.

The relationship between M2 supply and bitcoin price depends on many factors and should be used in conjunction with other analysis methods.

N-Degree Moment-Based Adaptive Detection🙏🏻 N-Degree Moment-Based Adaptive Detection (NDMBAD) method is a generalization of MBAD since the horizontal line fit passing through the data's mean can be simply treated as zero-degree polynomial regression. We can extend the MBAD logic to higher-degree polynomial regression.

I don't think I need to talk a lot about the thing there; the logic is really the same as in MBAD, just hit the link above and read if you want. The only difference is now we can gather cumulants not only from the horizontal mean fit (degree = 0) but also from higher-order polynomial regression fit, including linear regression (degree = 1).

Why?

Simply because residuals from the 0-degree model don't contain trend information, and while in some cases that's exactly what you need, in other cases, you want to model your trend explicitly. Imagine your underlying process trends in a steady manner, and you want to control the extreme deviations from the process's core. If you're going to use 0-degree, you'll be treating this beautiful steady trend as a residual itself, which "constantly deviates from the process mean." It doesn't make much sense.

How?

First, if you set the length to 0, you will end up with the function incrementally applied to all your data starting from bar_index 0. This can be called the expanding window mode. That's the functionality I include in all my scripts lately (where it makes sense). As I said in the MBAD description, choosing length is a matter of doing business & applied use of my work, but I think I'm open to talk about it.

I don't see much sense in using degree > 1 though (still in research on it). If you have dem curves, you can use Fourier transform -> spectral filtering / harmonic regression (regression with Fourier terms). The job of a degree > 0 is to model the direction in data, and degree 1 gets it done. In mean reversion strategies, it means that you don't wanna put 0-degree polynomial regression (i.e., the mean) on non-stationary trending data in moving window mode because, this way, your residuals will be contaminated with the trend component.

By the way, you can send thanks to @aaron294c , he said like mane MBAD is dope, and it's gonna really complement his work, so I decided to drop NDMBAD now, gonna be more useful since it covers more types of data.

I wanned to call it N-Order Moment Adaptive Detection because it abbreviates to NOMAD, which sounds cool and suits me well, because when I perform as a fire dancer, nomad style is one of my outfits. Burning Man stuff vibe, you know. But the problem is degree and order really mean two different things in the polynomial context, so gotta stay right & precise—that's the priority.

∞

AadTrend [InvestorUnknown]The AadTrend indicator is an experimental trading tool that combines a user-selected moving average with the Average Absolute Deviation (AAD) from this moving average. This combination works similarly to the Supertrend indicator but offers additional flexibility and insights. In addition to generating Long and Short signals, the AadTrend indicator identifies RISK-ON and RISK-OFF states for each trade direction, highlighting areas where taking on more risk may be considered.

Core Concepts and Features

Moving Average (User-Selected Type)

The indicator allows users to select from various types of moving averages to suit different trading styles and market conditions:

Simple Moving Average (SMA)

Exponential Moving Average (EMA)

Hull Moving Average (HMA)

Double Exponential Moving Average (DEMA)

Triple Exponential Moving Average (TEMA)

Relative Moving Average (RMA)

Fractal Adaptive Moving Average (FRAMA)

Average Absolute Deviation (AAD)

The Average Absolute Deviation measures the average distance between each data point and the mean, providing a robust estimation of volatility.

aad(series float src, simple int length, simple string avg_type) =>

avg = // Moving average as selected by the user

abs_deviations = math.abs(src - avg)

ta.sma(abs_deviations, length)

This provides a volatility measure that adapts to recent market conditions.

Combining Moving Average and AAD

The indicator creates upper and lower bands around the moving average using the AAD, similar to how the Supertrend indicator uses Average True Range (ATR) for its bands.

AadTrend(series float src, simple int length, simple float aad_mult, simple string avg_type) =>

// Calculate AAD (volatility measure)

aad_value = aad(src, length, avg_type)

// Calculate the AAD-based moving average by scaling the price data with AAD

avg = switch avg_type

"SMA" => ta.sma(src, length)

"EMA" => ta.ema(src, length)

"HMA" => ta.hma(src, length)

"DEMA" => ta.dema(src, length)

"TEMA" => ta.tema(src, length)

"RMA" => ta.rma(src, length)

"FRAMA" => ta.frama(src, length)

avg_p = avg + (aad_value * aad_mult)

avg_m = avg - (aad_value * aad_mult)

var direction = 0

if ta.crossover(src, avg_p)

direction := 1

else if ta.crossunder(src, avg_m)

direction := -1

A chart displaying the moving average with upper and lower AAD bands enveloping the price action.

Signals and Trade States

1. Long and Short Signals

Long Signal: Generated when the price crosses above the upper AAD band,

Short Signal: Generated when the price crosses below the lower AAD band.

2. RISK-ON and RISK-OFF States

These states provide additional insight into the strength of the current trend and potential opportunities for taking on more risk.

RISK-ON Long: When the price moves significantly above the upper AAD band after a Long signal.

RISK-OFF Long: When the price moves back below the upper AAD band, suggesting caution.

RISK-ON Short: When the price moves significantly below the lower AAD band after a Short signal.

RISK-OFF Short: When the price moves back above the lower AAD band.

Highlighted areas on the chart representing RISK-ON and RISK-OFF zones for both Long and Short positions.

A chart showing the filled areas corresponding to trend directions and RISK-ON zones

Backtesting and Performance Metrics

While the AadTrend indicator focuses on generating signals and highlighting risk areas, it can be integrated with backtesting frameworks to evaluate performance over historical data.

Integration with Backtest Library:

import InvestorUnknown/BacktestLibrary/1 as backtestlib

Customization and Calibration

1. Importance of Calibration

Default Settings Are Experimental: The default parameters are not optimized for any specific market condition or asset.

User Calibration: Traders should adjust the length, aad_mult, and avg_type parameters to align the indicator with their trading strategy and the characteristics of the asset being analyzed.

2. Factors to Consider

Market Volatility: Higher volatility may require adjustments to the aad_mult to avoid false signals.

Trading Style: Short-term traders might prefer faster-moving averages like EMA or HMA, while long-term traders might opt for SMA or FRAMA.

Alerts and Notifications

The AadTrend indicator includes built-in alert conditions to notify traders of significant market events:

Long and Short Alerts:

alertcondition(long_alert, "LONG (AadTrend)", "AadTrend flipped ⬆LONG⬆")

alertcondition(short_alert, "SHORT (AadTrend)", "AadTrend flipped ⬇Short⬇")

RISK-ON and RISK-OFF Alerts:

alertcondition(risk_on_long, "RISK-ON LONG (AadTrend)", "RISK-ON LONG (AadTrend)")

alertcondition(risk_off_long, "RISK-OFF LONG (AadTrend)", "RISK-OFF LONG (AadTrend)")

alertcondition(risk_on_short, "RISK-ON SHORT (AadTrend)", "RISK-ON SHORT (AadTrend)")

alertcondition(risk_off_short, "RISK-OFF SHORT (AadTrend)", "RISK-OFF SHORT (AadTrend)")

Important Notes and Disclaimer

Experimental Nature: The AadTrend indicator is experimental and should be used with caution.

No Guaranteed Performance: Past performance is not indicative of future results. Backtesting results may not reflect real trading conditions.

User Responsibility: Traders and investors should thoroughly test and calibrate the indicator settings before applying it to live trading.

Risk Management: Always use proper risk management techniques, including stop-loss orders and position sizing.