3.RSI LIJO 45*55//@version=6

indicator(title="3.RSI LIJO 45*55", shorttitle="RSI-LIJO-45-55", format=format.price, precision=2, timeframe="", timeframe_gaps=true)

rsiLengthInput = input.int(9, minval=1, title="RSI Length", group="RSI Settings")

rsiSourceInput = input.source(close, "Source", group="RSI Settings")

calculateDivergence = input.bool(false, title="Calculate Divergence", group="RSI Settings", display=display.data_window, tooltip="Calculating divergences is needed in order for divergence alerts to fire.")

change = ta.change(rsiSourceInput)

up = ta.rma(math.max(change, 0), rsiLengthInput)

down = ta.rma(-math.min(change, 0), rsiLengthInput)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

// Change RSI line color based on bands

rsiColor = rsi > 50 ? color.green : rsi < 50 ? color.red : color.white

rsiPlot = plot(rsi, "RSI", color=rsiColor)

rsiUpperBand = hline(55, "RSI Upper Band", color=color.rgb(5, 247, 22))

midline = hline(50, "RSI Middle Band", color=color.new(#787B86, 50))

rsiLowerBand = hline(45, "RSI Lower Band", color=color.rgb(225, 18, 14))

fill(rsiUpperBand, rsiLowerBand, color=color.rgb(126, 87, 194, 90), title="RSI Background Fill")

midLinePlot = plot(50, color=na, editable=false, display=display.none)

fill(rsiPlot, midLinePlot, 100, 55, top_color=color.new(color.green, 0), bottom_color=color.new(color.green, 100), title="Overbought Gradient Fill")

fill(rsiPlot, midLinePlot, 45, 0, top_color=color.new(color.red, 100), bottom_color=color.new(color.red, 0), title="Oversold Gradient Fill")

// Smoothing MA inputs

GRP = "Smoothing"

TT_BB = "Only applies when 'SMA + Bollinger Bands' is selected. Determines the distance between the SMA and the bands."

maTypeInput = input.string("SMA", "Type", options= , group=GRP, display=display.data_window)

maLengthInput = input.int(31, "Length", group=GRP, display=display.data_window)

bbMultInput = input.float(2.0, "BB StdDev", minval=0.001, maxval=50, step=0.5, tooltip=TT_BB, group=GRP, display=display.data_window)

var enableMA = maTypeInput != "None"

var isBB = maTypeInput == "SMA + Bollinger Bands"

// Smoothing MA Calculation

ma(source, length, MAtype) =>

switch MAtype

"SMA" => ta.sma(source, length)

"SMA + Bollinger Bands" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA (RMA)" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

// Smoothing MA plots

smoothingMA = enableMA ? ma(rsi, maLengthInput, maTypeInput) : na

smoothingStDev = isBB ? ta.stdev(rsi, maLengthInput) * bbMultInput : na

plot(smoothingMA, "RSI-based MA", color=color.yellow, display=enableMA ? display.all : display.none, editable=enableMA)

bbUpperBand = plot(smoothingMA + smoothingStDev, title="Upper Bollinger Band", color=color.green, display=isBB ? display.all : display.none, editable=isBB)

bbLowerBand = plot(smoothingMA - smoothingStDev, title="Lower Bollinger Band", color=color.green, display=isBB ? display.all : display.none, editable=isBB)

fill(bbUpperBand, bbLowerBand, color=isBB ? color.new(color.green, 90) : na, title="Bollinger Bands Background Fill", display=isBB ? display.all : display.none, editable=isBB)

// Divergence

lookbackRight = 5

lookbackLeft = 5

rangeUpper = 60

rangeLower = 5

bearColor = color.red

bullColor = color.green

textColor = color.white

noneColor = color.new(color.white, 100)

_inRange(bool cond) =>

bars = ta.barssince(cond)

rangeLower <= bars and bars <= rangeUpper

plFound = false

phFound = false

bullCond = false

bearCond = false

rsiLBR = rsi

if calculateDivergence

//------------------------------------------------------------------------------

// Regular Bullish

// rsi: Higher Low

plFound := not na(ta.pivotlow(rsi, lookbackLeft, lookbackRight))

rsiHL = rsiLBR > ta.valuewhen(plFound, rsiLBR, 1) and _inRange(plFound )

// Price: Lower Low

lowLBR = low

priceLL = lowLBR < ta.valuewhen(plFound, lowLBR, 1)

bullCond := priceLL and rsiHL and plFound

//------------------------------------------------------------------------------

// Regular Bearish

// rsi: Lower High

phFound := not na(ta.pivothigh(rsi, lookbackLeft, lookbackRight))

rsiLH = rsiLBR < ta.valuewhen(phFound, rsiLBR, 1) and _inRange(phFound )

// Price: Higher High

highLBR = high

priceHH = highLBR > ta.valuewhen(phFound, highLBR, 1)

bearCond := priceHH and rsiLH and phFound

plot(

plFound ? rsiLBR : na,

offset = -lookbackRight,

title = "Regular Bullish",

linewidth = 2,

color = (bullCond ? bullColor : noneColor),

display = display.pane,

editable = calculateDivergence)

plotshape(

bullCond ? rsiLBR : na,

offset = -lookbackRight,

title = "Regular Bullish Label",

text = " Bull ",

style = shape.labelup,

location = location.absolute,

color = bullColor,

textcolor = textColor,

display = display.pane,

editable = calculateDivergence)

plot(

phFound ? rsiLBR : na,

offset = -lookbackRight,

title = "Regular Bearish",

linewidth = 2,

color = (bearCond ? bearColor : noneColor),

display = display.pane,

editable = calculateDivergence)

plotshape(

bearCond ? rsiLBR : na,

offset = -lookbackRight,

title = "Regular Bearish Label",

text = " Bear ",

style = shape.labeldown,

location = location.absolute,

color = bearColor,

textcolor = textColor,

display = display.pane,

editable = calculateDivergence)

alertcondition(bullCond, title='Regular Bullish Divergence', message="Found a new Regular Bullish Divergence, Pivot Lookback Right number of bars to the left of the current bar.")

alertcondition(bearCond, title='Regular Bearish Divergence', message='Found a new Regular Bearish Divergence, Pivot Lookback Right number of bars to the left of the current bar.')

Indicators and strategies

UT Bot + LinReg Candles (Dual Sensitivity)

Script Description:

This indicator combines the popular UT Bot Alerts system with Linear Regression Candles (open source) for enhanced trend detection and trading signals in one singel script. The UT Bot features independent, then 2 x ATR sensitivity and periods controls for buy and sell signals, allowing you to fine-tune entries and exits to match your strategy. The script also overlays colored Linear Regression Candles with an optional signal line, helping you visually identify trend strength and direction. All calculations are performed on standard chart prices (no Heikin Ashi). Suitable for all asset classes and timeframes.

Eample setting for usdjpy 5 min chart for repeated buy and sell singnals based on trend:

BUY ATR period 300 multiplier 1

SELL ATR period 1 multiplier 2

Disclaimer:

This script is for informational and educational purposes only. It is not financial advice. Use at your own risk; the author assumes no responsibility for any trading results or losses.

Credits goes to to Ugurvu for linreg candles and quantnomad for UT Bot alerts that make this script possible.

Author: Patrick

Jumping watermark# Jumping watermark

## Function description

- Dynamic watermark: Mainly used to add dynamic watermarks to prevent theft and transfer when recording videos.

- Static watermark: Sharing opinions can easily include information such as trading pairs, cycles, current time, and individual signatures.

### Static watermark:

Display the watermark related to the current trading pair in the center of the chart.

- Configuration items:

- You can choose to configure the display content: current trading pair code and name, cycle, date, time, and individual signature content

### Dynamic watermark

Display the configured watermark content in a dynamic random position.

- Configuration items:

- Turn on or off the display of watermark jumping

- Modify the display text content and style by yourself

----- 中文简介-----

# 跳动水印

## 功能描述

- 动态水印: 主要可用于视频录制时添加动态水印防盗、防搬运。

- 静态水印:观点分享是可方便的带上交易对、周期、当前时间、个签等信息。

### 静态水印:

在图表中心位置显示当前交易对相关信息水印。

- 配置项:

- 可选择配置显示内容:当前交易对代码及名称、周期、日期、时间、个签内容

### 动态水印

动态随机位置显示配置水印内容。

- 配置项:

- 开启或关闭显示水印跳动

- 自行修改配置显示文字内容和样式

Candle Emotion Oscillator [CEO]Candle Emotion Oscillator (CEO) - Revolutionary User Guide

🧠 World's First Market Psychology Oscillator

The Candle Emotion Oscillator (CEO) is a groundbreaking indicator that measures market emotions through pure candle price action analysis. This is the first oscillator ever created that translates candle patterns into psychological states, giving you unprecedented insight into market sentiment.

🚀 Revolutionary Concept

What Makes CEO Unique

100% Pure Price Action: No volume, no external data - just candle analysis

Market Psychology: Measures actual emotions: Fear, Greed, Panic, Euphoria

Never Been Done Before: First oscillator to analyze market emotions

Exhaustion Prediction: Detects emotional fatigue before reversals

Fast Response: Perfect for your 2-5 minute scalping setup

The Four Core Emotions

🟢 GREED (Positive Values)

What it measures: Market conviction and decisiveness

Candle Pattern: Large bodies, small wicks

Psychology: Traders are confident and decisive

Oscillator: Positive values (0 to +100)

Trading Implication: Trend continuation likely

🔴 FEAR (Negative Values)

What it measures: Market uncertainty and indecision

Candle Pattern: Small bodies, large wicks

Psychology: Traders are uncertain and hesitant

Oscillator: Negative values (0 to -100)

Trading Implication: Consolidation or reversal likely

🚀 EUPHORIA (Extreme Positive)

What it measures: Excessive optimism and buying pressure

Candle Pattern: Large green bodies with upper wicks

Psychology: Extreme bullish sentiment

Oscillator: Values above +60

Trading Implication: Overbought, reversal warning

💥 PANIC (Extreme Negative)

What it measures: Capitulation and selling pressure

Candle Pattern: Large red bodies with lower wicks

Psychology: Extreme bearish sentiment

Oscillator: Values below -60

Trading Implication: Oversold, reversal opportunity

📊 Visual Elements Explained

Main Components

Thick Colored Line: Primary emotion oscillator

Green: Greed (positive emotions)

Red: Fear (negative emotions)

Bright Green: Euphoria (extreme positive)

Dark Red: Panic (extreme negative)

Thin Blue Line: Emotion trend (longer-term context)

Background Gradient: Emotional intensity

Darker = stronger emotions

Lighter = weaker emotions

Diamond Signals: 🔶 Emotional exhaustion detected

Rocket Signals: 🚀 Extreme euphoria warning

Explosion Signals: 💥 Extreme panic warning

Information Table (Top Right)

Dynamic Gap Probability ToolDynamic Gap Probability Tool measures the percentage gap between price and a chosen moving average, then analyzes your chart history to estimate the likelihood of the next candle moving up or down. It dynamically adjusts its sample size to ensure statistical robustness while focusing on the exact deviation level.

Originality and Value:

• Combines gap-based analysis with dynamic sample aggregation to balance precision and reliability.

• Automatically extends the sample when exact matches are scarce, avoiding misleading signals on rare extreme moves.

• Provides real “next-candle” probabilities based on historical occurrences rather than fixed thresholds or untested heuristics.

• Adds value by giving traders an evidence-based edge: you see how similar past deviations actually played out.

How It Works:

1. Calculate gap = (close – moving average) / moving average * 100.

2. Round the absolute gap to nearest percent (X%).

3. Count historical bars where gap ≥ X% above or ≤ –X% below.

4. If exact X% count is below the minimum occurrences threshold, include gaps at X+1%, X+2%, etc., until threshold is reached.

5. Compute “next-candle” green vs. red probabilities from the aggregated sample.

6. Display current gap, sample size, green probability, and red probability in a table.

Inputs:

• Moving Average Type (SMA, EMA, WMA, VWMA, HMA, SMMA, TMA)

• Moving Average Period (default 200)

• Minimum Occurrences Threshold (default 50)

• Table position and styling options

Examples:

• If price is 3% above the 200-period SMA and 120 occurrences ≥3% are found, with 84 green next candles (70%) and 36 red (30%), the script displays “3% | 120 | 70% green | 30% red.”

• If price is 8% below the SMA but only 20 exact matches exist, the script will include 9% and 10% gaps until it reaches 50 samples, then calculate probabilities from that broader set.

Why It’s Useful:

• Mean-reversion traders see green-probability signals at extreme overbought or oversold levels.

• Trend-followers identify continuation likelihood when red probability is high.

• Risk managers gauge reliability by inspecting sample size before acting on any signal.

Limitations:

• Historical probabilities do not guarantee future performance.

• Results depend on timeframe and symbol, backtest with your data before trading.

• Use realistic slippage and commission when overlaying on strategy scripts.

Gann Octave 8 - Professional V 1.0Gann Octave 8 Indicator:

Core Concept: This indicator divides the price range between highest high and lowest low into 8 equal parts (octaves), creating support/resistance levels based on W.D. Gann's trading principles.

Key Components:

1. Price Range Calculation:

o Finds highest high and lowest low over a lookback period (default 50 bars)

o Divides this range into 8 equal segments (12.5% each)

2. 8 Octave Levels:

o 0% (Low Support) - Strongest support

o 12.5%, 25%, 37.5% - Minor levels

o 50% (CRITICAL) - Most important level

o 62.5%, 75%, 87.5% - Minor levels

o 100% (High Resistance) - Strongest resistance

3. Gann Angles: Projects trend lines from high/low points at various angles (1x1, 2x1, 1x2, etc.)

4. Visual Features:

o Color-coded levels

o Information table showing current position

o Background highlighting when near critical levels

o Trend analysis (bullish/bearish zones)

Trading Strategy

Entry Signals:

BULLISH TRADES:

• Price crosses above 50% level → Strong buy signal

• Price bounces from 25% or 37.5% levels → Support bounce

• Price in upper zone (above 50%) → Bullish bias

BEARISH TRADES:

• Price crosses below 50% level → Strong sell signal

• Price rejects at 75% or 87.5% levels → Resistance rejection

• Price in lower zone (below 50%) → Bearish bias

Key Trading Rules:

1. 50% Level is Critical: Most important for trend direction

2. Zone Trading:

o Above 50% = Bullish zone (look for longs)

o Below 50% = Bearish zone (look for shorts)

3. Strength Levels:

o Above 75% or below 25% = Strong moves

o Near 100% (high) or 0% (low) = Extreme levels

Risk Management:

• Stop Loss: Place below previous octave level

• Take Profit: Target next octave level

• Position Size: Reduce size near extreme levels (0%, 100%)

Example Trade:

If price breaks above 50% level:

• Entry: Long position

• Stop: Below 37.5% level

• Target: 75% level

• Risk: Monitor for rejection at resistance levels

The indicator works best in trending markets and helps identify high-probability reversal zones.

Works for both Stocks & Derivatives. Experiment with code and share your feedback in comments..

ITM 2x15// © 2025 Intraday Trading Machine

// This script is open-source. You may use and modify it, but please give credit.

// Colors the current 15-minute candle body green or red if the two previous candles were both bullish or bearish.

This script is designed for traders using the Scalping Intraday Trading Machine technique. It highlights when two consecutive 15-minute candles close in the same direction — either both bullish or both bearish.

For example, if you see two consecutive bearish candles, you might look for a long entry on a break above the high of the first bearish candle. This tool helps you visually identify these setups with clean, directional candle coloring — no clutter.

Kelly Optimal Leverage IndicatorThe Kelly Optimal Leverage Indicator mathematically applies Kelly Criterion to determine optimal position sizing based on market conditions.

This indicator helps traders answer the critical question: "How much capital should I allocate to this trade?"

Note that "optimal position sizing" does not equal the position sizing that you should have. The Optima position sizing given by the indicator is based on historical data and cannot predict a crash, in which case, high leverage could be devastating.

Originally developed for gambling scenarios with known probabilities, the Kelly formula has been adapted here for financial markets to dynamically calculate the optimal leverage ratio that maximizes long-term capital growth while managing risk.

Key Features

Kelly Position Sizing: Uses historical returns and volatility to calculate mathematically optimal position sizes

Multiple Risk Profiles: Displays Full Kelly (aggressive), 3/4 Kelly (moderate), 1/2 Kelly (conservative), and 1/4 Kelly (very conservative) leverage levels

Volatility Adjustment: Automatically recommends appropriate Kelly fraction based on current market volatility

Return Smoothing: Option to use log returns and smoothed calculations for more stable signals

Comprehensive Table: Displays key metrics including annualized return, volatility, and recommended exposure levels

How to Use

Interpret the Lines: Each colored line represents a different Kelly fraction (risk tolerance level). When above zero, positive exposure is suggested; when below zero, reduce exposure. Note that this is based on historical returns. I personally like to increase my exposure during market downturns, but this is hard to illustrate in the indicator.

Monitor the Table: The information panel provides precise leverage recommendations and exposure guidance based on current market conditions.

Follow Recommended Position: Use the "Recommended Position" guidance in the table to determine appropriate exposure level.

Select Your Risk Profile: Conservative traders should follow the Half Kelly or Quarter Kelly lines, while more aggressive traders might consider the Three-Quarter or Full Kelly lines.

Adjust with Volatility: During high volatility periods, consider using more conservative Kelly fractions as recommended by the indicator.

Mathematical Foundation

The indicator calculates the optimal leverage (f*) using the formula:

f* = μ/σ²

Where:

μ is the annualized expected return

σ² is the annualized variance of returns

This approach balances potential gains against risk of ruin, offering a scientific framework for position sizing that maximizes long-term growth rate.

Notes

The Full Kelly is theoretically optimal for maximizing long-term growth but can experience significant drawdowns. You should almost never use full kelly.

Most practitioners use fractional Kelly strategies (1/2 or 1/4 Kelly) to reduce volatility while capturing most of the growth benefits

This indicator works best on daily timeframes but can be applied to any timeframe

Negative Kelly values suggest reducing or eliminating market exposure

The indicator should be used as part of a complete trading system, not in isolation

Enjoy the indicator! :)

P.S. If you are really geeky about the Kelly Criterion, I recommend the book The Kelly Capital Growth Investment Criterion by Edward O. Thorp and others.

Breakout LabelsThis script labels the highest price of the lowest candle over a period of time. It then labels any bullish breakouts where the close price is higher than the high of the lowest candle.

Crypto Risk-Weighted Allocation SuiteCrypto Risk-Weighted Allocation Suite

This indicator is designed to help users explore dynamic portfolio allocation frameworks for the crypto market. It calculates risk-adjusted allocation weights across major crypto sectors and cash based on multi-factor momentum and volatility signals. Best viewed on INDEX:BTCUSD 1D chart. Other charts and timeframes may give mixed signals and incoherent allocations.

🎯 How It Works

This model systematically evaluates the relative strength of:

BTC Dominance (CRYPTOCAP:BTC.D)

Represents Bitcoin’s share of the total crypto market. Rising dominance typically indicates defensive market phases or BTC-led trends.

ETH/BTC Ratio (BINANCE:ETHBTC)

Gauges Ethereum’s relative performance versus Bitcoin. This provides insight into whether ETH is leading risk appetite.

SOL/BTC Ratio (BINANCE:SOLBTC)

Measures Solana’s performance relative to Bitcoin, capturing mid-cap layer-1 strength.

Total Market Cap excluding BTC and ETH (CRYPTOCAP:TOTAL3ES)

Represents Altcoins as a broad category, reflecting appetite for higher-risk assets.

Each of these series is:

✅ Converted to a momentum slope over a configurable lookback period.

✅ Standardized into Z-scores to normalize changes relative to recent behavior.

✅ Smoothed optionally using a Hull Moving Average for cleaner signals.

✅ Divided by ATR-based volatility to create a risk-weighted score.

✅ Scaled to proportionally allocate exposure, applying user-configured minimum and maximum constraints.

🪙 Dynamic Allocation Logic

All signals are normalized to sum to 100% if fully confident.

An overall confidence factor (based on total signal strength) scales the allocation up or down.

Any residual is allocated to cash (unallocated capital) for conservative exposure.

The script automatically avoids “all-in” bias and prevents negative allocations.

📊 Outputs

The indicator displays:

Market Phase Detection (which asset class is currently leading)

Risk Mode (Risk On, Neutral, Risk Off)

Dynamic Allocations for BTC, ETH, SOL, Alts, and Cash

Optional momentum plots for transparency

🧠 Why This Is Unique

Unlike simple dominance indicators or crossovers, this model:

Integrates multiple cross-asset signals (BTC, ETH, SOL, Alts)

Adjusts exposure proportionally to signal strength

Normalizes by volatility, dynamically scaling risk

Includes configurable constraints to reflect your own risk tolerance

Provides a cash fallback allocation when conviction is low

Is entirely non-repainting and based on daily closing data

⚠️ Disclaimer

This script is provided for educational and informational purposes only.

It is not financial advice and should not be relied upon to make investment decisions.

Past performance does not guarantee future results.

Always consult a qualified financial advisor before acting on any information derived from this tool.

🛠 Recommended Use

As a framework to visualize relative momentum and risk-adjusted allocations

For research and backtesting ideas on portfolio allocation across crypto sectors

To help build your own risk management process

This script is not a turnkey strategy and should be customized to fit your goals.

✅ Enjoy exploring dynamic crypto allocations responsibly!

Low Price RSI CrossoverThis Pine Script indicator is a Multi-Timeframe Low RSI Crossover system that combines three key filtering criteria to identify high-probability buy signals. Here's what it does:

Core Concept

The indicator only generates buy signals when all three conditions are met simultaneously:

Price at Multi-Period Low: Current price must be at or near the lowest point within your selected timeframe (1 week to 5 years, or custom)

RSI Momentum Shift: The smoothed RSI must cross above its signal line (EMA), indicating upward momentum

Below Threshold Entry: Both the RSI and its signal line must be below your threshold level (default 50) when the crossover occurs

Key Features

RSI Smoothing: Uses Hull Moving Average (HMA) to smooth the raw RSI, reducing noise and false signals while maintaining responsiveness.

Flexible Timeframes: Choose from predefined periods (1W, 2W, 3W, 1M, 2M, 3M, 6M, 9M, 1Y, 2Y, 3Y, 5Y) or set a custom number of bars.

Visual Feedback:

Plots the smoothed RSI (blue line) and its signal line (red line)

Shows threshold and overbought levels

Highlights signal bars with green background

Displays tiny green triangles at signal points

Real-time status table showing all conditions

Trading Logic

This is essentially a mean-reversion strategy that waits for:

Price to reach significant lows (value zone)

Momentum to start shifting upward (RSI crossover)

Entry from oversold/neutral territory (below 50 RSI)

Why This Works

By requiring price to be at multi-period lows, you avoid buying during downtrends or sideways chop. The RSI crossover confirms that selling pressure is starting to ease, while the threshold filter ensures you're not buying into overbought conditions.

The combination of these filters should significantly reduce false signals compared to using any single indicator alone.

Logistic Regression ICT FVG🚀 OVERVIEW

Welcome to the Logistic Regression Fair Value Gap (FVG) System — a next-gen trading tool that blends precision gap detection with machine learning intelligence.

Unlike traditional FVG indicators, this one evolves with each bar of price action, scoring and filtering gaps based on real market behavior.

🔧 CORE FEATURES

✨ Smart Gap Detection

Automatically identifies bullish and bearish Fair Value Gaps using volatility-aware candle logic.

📊 Probability-Based Filtering

Uses logistic regression to assign each gap a confidence score (0 to 1), showing only high-probability setups.

🔁 Real-Time Retest Tracking

Continuously watches how price interacts with each gap to determine if it deserves respect.

📈 Multi-Factor Assessment

Evaluates RSI, MACD, and body size at gap formation to build a full context snapshot.

🧠 Self-Learning Engine

The logistic regression model updates on each bar using gradient descent, refining its predictions over time.

📢 Built-In Alerts

Get instant alerts when a gap forms, gets retested, or breaks.

🎨 Custom Display Options

Control the color of bullish/bearish zones, and toggle on/off probability labels for cleaner charts.

🚩 WHAT MAKES IT DIFFERENT

This isn’t just another box-drawing indicator.

While others mark every imbalance, this system thinks before it draws — using statistical modeling to filter out noise and prioritize high-impact zones.

By learning from how price behaves around gaps (not just how they form), it helps you trade only what matters — not what clutters.

⚙️ HOW IT WORKS

1️⃣ Detection

FVGs are identified using ATR-based thresholds and sharp wick imbalances.

2️⃣ Behavior Monitoring

Every gap is tracked — and if respected enough times, it becomes part of the elite training set.

3️⃣ Context Capture

Each new FVG logs RSI, MACD, and body size to provide a feature-rich context for prediction.

4️⃣ Prediction (Logistic Regression)

The model predicts how likely the gap is to be respected and assigns it a probability score.

5️⃣ Classification & Alerts

Gaps above the threshold are plotted with score labels, and alerts trigger for entry/respect/break.

⚙️ CONFIGURATION PANEL

🔧 System Inputs

• Max Retests – How many times a gap must be respected to train the model

• Prediction Threshold – Minimum score to show a gap on the chart

• Learning Rate – Controls how fast the model adapts (default: 0.009)

• Max FVG Lifetime – Expiration duration for unused gaps

• Show Historic Gaps – Show/hide expired or invalidated gaps

🎨 Visual Options

• Bullish/Bearish Colors – Set gap colors to fit your chart style

• Confidence Labels – Show probability scores next to FVGs

• Alert Toggles – Enable alerts for:

– New FVG detected

– FVG respected (entry)

– FVG invalidated (break)

💡 WHY LOGISTIC REGRESSION?

Traditional FVG tools rely on candle shapes.

This system relies on probability — by training on RSI, MACD, and price behavior, it predicts whether a gap will act as a true liquidity zone.

Logistic regression lets the system continuously adapt using new data, making it more accurate the longer it runs.

That means smarter signals, fewer false positives, and a clearer view of where real opportunities lie.

Greer Book Value Yield📘 Script Title

Greer Book Value Yield – Valuation Insight Based on Balance Sheet Strength

🧾 Description

Greer Book Value Yield is a valuation-focused indicator in the Greer Financial Toolkit, designed to evaluate how much net asset value (book value) a company provides per share relative to its current market price. This script calculates the Book Value Per Share Yield (BV%) using the formula:

Book Value Yield (%) = Book Value Per Share ÷ Stock Price × 100

This yield helps investors assess whether a stock is trading at a discount or premium to its underlying assets. It dynamically highlights when the yield is:

🟢 Above its historical average (potentially undervalued)

🔴 Below its historical average (potentially overvalued)

🔍 Use Case

Analyze valuation through asset-based metrics

Identify buy opportunities when book value yield is historically high

Combine with other scripts in the Greer Financial Toolkit:

📘 Greer Value – Tracks year-over-year growth consistency across six key metrics

📊 Greer Value Yields Dashboard – Visualizes multiple valuation-based yields

🟢 Greer BuyZone – Highlights long-term technical buy zones

🛠️ Inputs & Data

Uses Book Value Per Share (BVPS) from TradingView’s financial database (Fiscal Year)

Calculates and compares against a static average yield to assess historical valuation

Clean visual feedback via dynamic coloring and overlays

⚠️ Disclaimer

This tool is for educational and informational purposes only and should not be considered financial advice. Always conduct your own research before making investment decisions.

Greer EPS Yield📘 Script Title

Greer EPS Yield – Valuation Insight Based on Earnings Productivity

🧾 Description

Greer EPS Yield is a valuation-focused indicator from the Greer Financial Toolkit, designed to evaluate how efficiently a company generates earnings relative to its current stock price. This script calculates the Earnings Per Share Yield (EPS%), using the formula:

EPS Yield (%) = Earnings Per Share ÷ Stock Price × 100

This yield metric provides a quick snapshot of valuation through the lens of profitability per share. It dynamically highlights when the EPS yield is:

🟢 Above its historical average (potentially undervalued)

🔴 Below its historical average (potentially overvalued)

🔍 Use Case

Quickly assess valuation attractiveness based on earnings yield.

Identify potential buy opportunities when EPS% is above its long-term average.

Combine with other indicators in the Greer Financial Toolkit for a fundamentals-driven investment strategy:

📘 Greer Value – Tracks year-over-year growth consistency across six key metrics

📊 Greer Value Yields Dashboard – Visualizes valuation-based yield metrics

🟢 Greer BuyZone – Highlights long-term technical buy zones

🛠️ Inputs & Data

Uses fiscal year EPS data from TradingView’s built-in financial database.

Tracks a static average EPS Yield to compare current valuation to historical norms.

Clean, intuitive visual with automatic color coding.

⚠️ Disclaimer

This tool is for educational and informational purposes only and should not be considered financial advice. Always conduct your own research before making investment decisions.

Bullish & Bearish Wick MarkerMarks bullish and bearish engulfing candles

Bullish engulfing candle:

when the low is lower than the previous candle low and the body close is higher than the previous candle body

Bearish engulfing cande:

when the high is higher than the previous candle high and the body close is lower than the previous candle body

Custom Daily Session Zones by KoenigseggCustom Daily Session Zones

🟣 Description

This indicator displays customizable trading session time zones as background highlights on your chart, on any timeframe you choose. The inline info tooltip provides the precise start and end times of the three largest market sessions—the US, the EU, and ASIA—for quick reference. It provides flexible control over session times for different days of the week, making it ideal for traders who need to visualize specific market hours or trading sessions.

🟣 Key Features

- Flexible Session Configuration: Set a common session time for all days or customize individual sessions for each day of the week

- Per-Day Control: Enable or disable sessions for specific days (Monday through Sunday)

- Color Customization: Choose unique colors for each day's session zones

- UTC Timezone Standard: All session times are defined in UTC to ensure consistency across charts

- Clean Visual Display: Non-intrusive background highlighting that doesn't interfere with price action

🟣 How to Use

- Common Session Mode: Use the default mode to apply the same session time across all enabled days

- Manual Per-Day Mode: Enable "Manual per-day sessions" to set different session times for each day

- Day Selection: Toggle individual days on/off based on your trading schedule

- Color Coding: Customize colors for each day to easily distinguish between different sessions

🟣 Technical Details

- Uses Pine Script v6 for optimal performance

- Implements proper session time detection using TradingView's built-in time functions

- Operates in UTC timezone for all session calculations

- Lightweight code that doesn't impact chart performance

🟣 Use Cases

- Highlight specific trading sessions (London, New York, Tokyo, etc.)

- Mark important market hours for your trading strategy

- Visualize different session overlaps

- Create custom trading time windows

- Track market activity during specific hours

🟣 Compatibility

- Works on all timeframes

- Compatible with all asset classes (Forex, Stocks, Crypto, Futures, etc.)

- Supports all TradingView chart types

- Responsive design that adapts to different screen sizes

🟣 Image Descriptions

- First Image (main image): Shows multiple New York Stock Exchange sessions from 1:30 p.m. to 8:00 p.m. (UTC), on the 15-minute timeframe, with each day’s zone colored differently to demonstrate the indicator’s customizable color settings.

- Second Image: A zoomed‑in fractal chart view of the same New York session on the 15-minute timeframe, illustrating how the background session zone appears even at higher detail levels.

Third Image: A close‑up of the New York session (1:30 p.m. to 8:00 p.m.) on the 3-minute timeframe, reaffirming the consistency of zone highlighting across different zoom levels.

🟣 Future Updates (v2)

In the next release, you’ll be able to define multiple session blocks per day—displaying two distinct colored zones within the same trading day. This will help you visualize when one market session ends and another begins without losing chart clarity.

🟣 Conclusion

This indicator is perfect for traders who need precise control over Market Session visualization and want to maintain a clean, professional chart appearance.

🟣 Disclaimer

This script is provided for educational and illustrative purposes only. It is not financial or trading advice, nor a recommendation to buy or sell any asset. Always conduct your own research and consult a professional before making any trading decisions.

GX Credit Spread SignalThe GX Credit Spread Signal is an advanced indicator designed for traders who trade options strategies on the SPX index, especially using vertical credit spreads. It combines traditional technical analysis with volatility and option pricing concepts to provide relevant signals and projections on the chart.

Main features:

Trend analysis: Uses opening gap, position relative to VWAP and simple moving average (SMA 50) to indicate bullish or bearish bias right after the first 15-minute candle.

Safe range projection: Calculates a range based on the ATR (Average True Range) multiplied by a safety factor, suggesting potential strikes for credit spreads.

Quantitative estimates:

Calculates the estimated delta of options via the Black-Scholes formula approximation.

Estimated probability of expiring out of the money (OTM).

Chart visualizations: Displays projected ATR lines, previous day's levels (high, low, close) and an informative panel with strikes, delta, OTM probability, ATR and VWAP data.

Configurable alerts: Notifications for detected bullish or bearish bias, helping the trader to identify opportunities quickly.

This indicator is ideal for those who day trade with SPX options, facilitating decision-making by combining technical analysis, volatility and option probabilities in one place.

Fast Fourier Transform [ScorsoneEnterprises]The SCE Fast Fourier Transform (FFT) is a tool designed to analyze periodicities and cyclical structures embedded in price. This is a Fourier analysis to transform price data from the time domain into the frequency domain, showing the rhythmic behaviors that are otherwise invisible on standard charts.

Instead of merely observing raw prices, this implementation applies the FFT on the logarithmic returns of the asset:

Log Return(𝑚) = log(close / close )

This ensures stationarity and stabilizes variance, making the analysis statistically robust and less influenced by trends or large price swings.

For a user-defined lookback window 𝑁:

Each frequency component 𝑘 is computed by summing real and imaginary projections of log-returns multiplied by complex exponential functions:

𝑒^−𝑖𝜃 = cos(𝜃)−𝑖sin(𝜃)

where:

θ = 2πkm / N

he result is the magnitude spectrum, calculated as:

Magnitude(𝑘) = sqrt(Real_Sum(𝑘)^2 + Imag_Sum(𝑘)^2)

This spectrum represents the strength of oscillations at each frequency over the lookback period, helping traders identify dominant cycles.

Visual Analysis & Interpretation

To give traders context for the FFT spectrum’s values, this script calculates:

25th Percentile (Purple Line)

Represents relatively low cyclical intensity.

Values below this threshold may signal quiet, noisy, or trendless periods.

75th Percentile (Red Line)

Represents heightened cyclical dominance.

Values above this threshold may indicate significant periodic activity and potential trend formation or rhythm in price action.

The FFT magnitude of the lowest frequency component (index 0) is plotted directly on the chart in teal. Observing how this signal fluctuates relative to its percentile bands provides a dynamic measure of cyclical market activity.

Chart examples

In this NYSE:CL chart, we see the regime of the price accurately described in the spectral analysis. We see the price above the 75th percentile continue to trend higher until it breaks back below.

In long trending markets like NYSE:PL has been, it can give a very good explanation of the strength. There was confidence to not switch regimes as we never crossed below the 75th percentile early in the move.

The script is also usable on the lower timeframes. There is no difference in the usability from the different timeframes.

Script Parameters

Lookback Value (N)

Default: 30

Defines how many bars of data to analyze. Larger N captures longer-term cycles but may smooth out shorter-term oscillations.

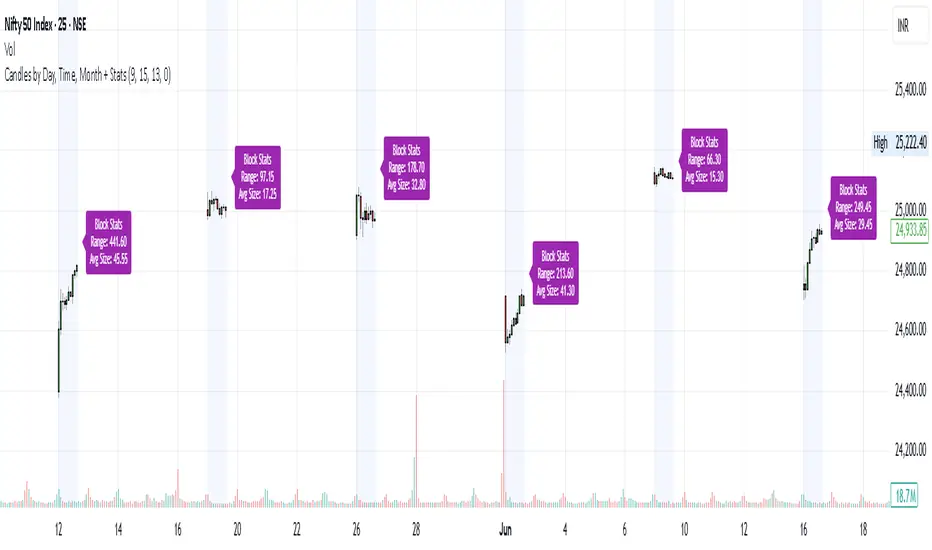

Candles by Day, Time, Month + StatsThis Pine Script allows you to filter and display candles based on:

📅 Specific days of the week

🕒 Custom intraday time ranges (e.g., 9:15 to 10:30)

📆 Selected months

📊 Shows stats for each filtered block:

🔼 Range (High – Low)

📏 Average candle body size

⚙️ Key Features:

✅ Filter by day, time, and month

🎛 Toggle to show/hide the stats label

🟩 Candles are drawn only for selected conditions

📍 Stats label is positioned above session high (adjustable)

⚠️ Important Setup Instructions:

✅ 1. Use it on a blank chart

To avoid overlaying with default candles:

Open the chart of your preferred symbol

Click on the chart type (top toolbar: "Candles", "Bars", etc.)

Select "Blank" from the dropdown (this will hide all native candles)

Apply this indicator

This ensures only the filtered candles from the script are visible.

Adjust for your local timezone

This script uses a hardcoded timezone: "Asia/Kolkata"

If you are in a different timezone, change it to your own (e.g. "America/New_York", "Europe/London", etc.) in all instances of:

time(timeframe.period, "Asia/Kolkata")

timestamp("Asia/Kolkata", ...)

Use Cases:

Opening range behavior on specific weekdays/months

Detecting market anomalies during exact windows

Building visual logs of preferred trade hours

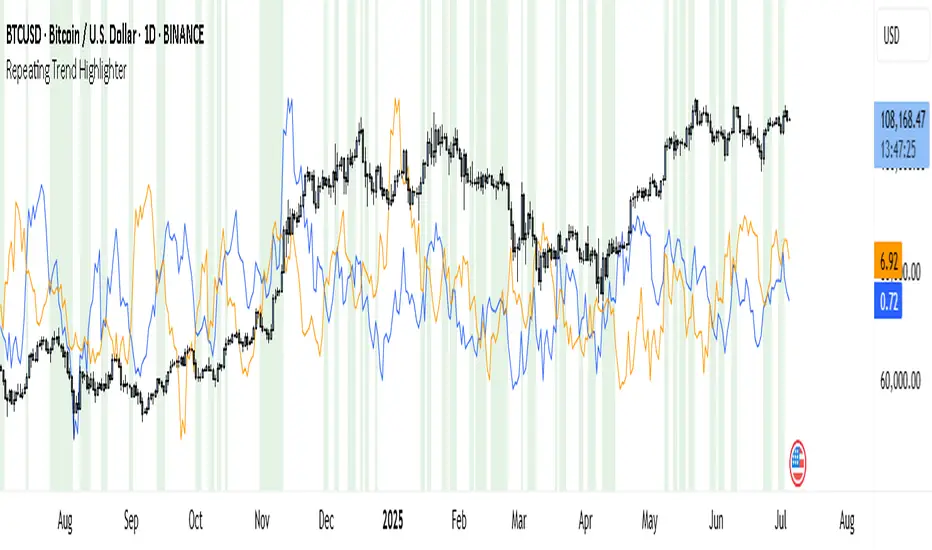

Repeating Trend HighlighterThis custom indicator helps you see when the current price trend is similar to a past trend over the same number of candles. Think of it like checking whether the market is repeating itself.

You choose three settings:

• Lookback Period: This is how many candles you want to measure. For example, if you set it to 10, it looks at the price change over the last 10 bars.

• Offset Bars Ago: This tells the indicator how far back in time to look for a similar move. If you set it to 50, it compares the current move to what happened 50 bars earlier.

• Tolerance (%): This is how closely the moves must match to be considered similar. A smaller number means you only get a signal if the moves are almost the same, while a larger number allows more flexibility.

When the current price move is close enough to the past move you picked, the background of your chart turns light green. This makes it easy to spot repeating trends without studying numbers manually.

You’ll also see two lines under your chart if you enable them: a blue line showing the percentage change of the current move and an orange line showing the change in the past move. These help you compare visually.

This tool is useful in several ways. You can use it to confirm your trading setups, for example if you suspect that a strong rally or pullback is happening again. You can also use it to filter trades by combining it with other indicators, so you only enter when trends repeat. Many traders use it as a learning tool, experimenting with different lookback periods and offsets to understand how often similar moves happen.

If you are a scalper working on short timeframes, you can set the lookback to a small number like 3–5 bars. Swing traders who prefer daily or weekly charts might use longer lookbacks like 20–30 bars.

Keep in mind that this indicator doesn’t guarantee price will move the same way again—it only shows similarity in how price changed over time. It works best when you use it together with other signals or market context.

In short, it’s like having a simple spotlight that tells you: “This move looks a lot like what happened before.” You can then decide if you want to act on that information.

If you’d like, I can help you tweak the settings or combine it with alerts so it notifies you when these patterns appear.

EVaR Indicator and Position SizingThe Problem:

Financial markets consistently show "fat-tailed" distributions where extreme events occur with higher frequency than predicted by normal distributions (Gaussian or even log-normal). These fat tails manifest in sudden price crashes, volatility spikes, and black swan events that traditional risk measures like volatility can underestimate. Standard deviation and conventional VaR calculations assume normally distributed returns, leaving traders vulnerable to severe drawdowns during market stress.

Cryptocurrencies and volatile instruments display particularly pronounced fat-tailed behavior, with extreme moves occurring 5-10 times more frequently than normal distribution models would predict. This reality demands a more sophisticated approach to risk measurement and position sizing.

The Solution: Entropic Value at Risk (EVAR)

EVaR addresses these limitations by incorporating principles from statistical mechanics and information theory through Tsallis entropy. This advanced approach captures the non-linear dependencies and power-law distributions characteristic of real financial markets.

Entropy is more adaptive than standard deviations and volatility measures.

I was inspired to create this indicator after reading the paper " The End of Mean-Variance? Tsallis Entropy Revolutionises Portfolio Optimisation in Cryptocurrencies " by by Sana Gaied Chortane and Kamel Naoui.

Key advantages of EVAR over traditional risk measures:

Superior tail risk capture: More accurately quantifies the probability of extreme market moves

Adaptability to market regimes: Self-calibrates to changing volatility environments

Non-parametric flexibility: Makes less assumptions about the underlying return distribution

Forward-looking risk assessment: Better anticipates potential market changes (just look at the charts :)

Mathematically, EVAR is defined as:

EVAR_α(X) = inf_{z>0} {z * log(1/α * M_X(1/z))}

Where the moment-generating function is calculated using q-exponentials rather than conventional exponentials, allowing precise modeling of fat-tailed behavior.

Technical Implementation

This indicator implements EVAR through a q-exponential approach from Tsallis statistics:

Returns Calculation: Price returns are calculated over the lookback period

Moment Generating Function: Approximated using q-exponentials to account for fat tails

EVAR Computation: Derived from the MGF and confidence parameter

Normalization: Scaled to for intuitive visualization

Position Sizing: Inversely modulated based on normalized EVAR

The q-parameter controls tail sensitivity—higher values (1.5-2.0) increase the weighting of extreme events in the calculation, making the model more conservative during potentially turbulent conditions.

Indicator Components

1. EVAR Risk Visualization

Dynamic EVAR Plot: Color-coded from red to green normalized risk measurement (0-1)

Risk Thresholds: Reference lines at 0.3, 0.5, and 0.7 delineating risk zones

2. Position Sizing Matrix

Risk Assessment: Current risk level and raw EVAR value

Position Recommendations: Percentage allocation, dollar value, and quantity

Stop Parameters: Mathematically derived stop price with percentage distance

Drawdown Projection: Maximum theoretical loss if stop is triggered

Interpretation and Application

The normalized EVAR reading provides a probabilistic risk assessment:

< 0.3: Low risk environment with minimal tail concerns

0.3-0.5: Moderate risk with standard tail behavior

0.5-0.7: Elevated risk with increased probability of significant moves

> 0.7: High risk environment with substantial tail risk present

Position sizing is automatically calculated using an inverse relationship to EVAR, contracting during high-risk periods and expanding during low-risk conditions. This is a counter-cyclical approach that ensures consistent risk exposure across varying market regimes, especially when the market is hyped or overheated.

Parameter Optimization

For optimal risk assessment across market conditions:

Lookback Period: Determines the historical window for risk calculation

Q Parameter: Controls tail sensitivity (higher values increase conservatism)

Confidence Level: Sets the statistical threshold for risk assessment

For cryptocurrencies and highly volatile instruments, a q-parameter between 1.5-2.0 typically provides the most accurate risk assessment because it helps capturing the fat-tailed behavior characteristic of these markets. You can also increase the q-parameter for more conservative approaches.

Practical Applications

Adaptive Risk Management: Quantify and respond to changing tail risk conditions

Volatility-Normalized Positioning: Maintain consistent exposure across market regimes

Black Swan Detection: Early identification of potential extreme market conditions

Portfolio Construction: Apply consistent risk-based sizing across diverse instruments

This indicator is my own approach to entropy-based risk measures as an alterative to volatility and standard deviations and it helps with fat-tailed markets.

Enjoy!

Stochastic Money Flow IndexThe Stochastic Money Flow Index (or Stochastic MFI ), is a variation of the classic Stochastic RSI that uses the Money Flow Index (MFI) rather than the Relative Strength Index (RSI) in its calculation.

While the RSI focuses solely on price momentum, the MFI is a volume-weighted indicator, meaning it incorporates both price and volume data.

The Stochastic MFI is intended to provide a more precise and sensitive reading of the MFI by measuring the level of the MFI relative to its range over a specific period.

Settings

Stochastic Settings

%K Length : The number of periods used to calculate the Stochastic. (Default: 14)

%K Smoothing : The SMA length used to 'smooth' the %K line. (Default: 3)

%D Smoothing : The SMA length used to 'smooth' the %D line. (Default: 1)

Money Flow Index Settings

MFI Length : The number of periods used to calculate the Money Flow Index. (Default: 14)

MFI Source : The source used to calculate the Money Flow Index. (Default: close)

Additional Settings

Show Overbought/Oversold Gradients? : Toggle the display of overbought/oversold gradients. (Default: true)

EVWAPThis indicator plots two Volume-Weighted Average Price (VWAP) lines anchored to earnings events:

EVWAP (Earnings Day): Resets VWAP on the day of the earnings release.

EVWAP (Post-Earnings Day): Resets VWAP on the first trading day after earnings.

These earnings-based VWAPs help identify average price zones impacted by earnings, providing insight into post-earnings support/resistance and potential trend shifts. Works on all timeframes.

Useful for traders analyzing price reactions around earnings reports.